PSO - The New York Times Continues To Soar But Investors Should Be Wary

2023-12-24 07:52:40 ET

Summary

- The New York Times has reached an agreement with Apple to include content from The Athletic on Apple News+.

- The New York Times' digital-only platform, The Athletic, has seen growth in subscribers and revenue in recent years.

- The company's financial data shows positive results, but the stock is still considered expensive.

One of the biggest weaknesses of value investing is that companies that are high quality and that trade at rather high multiples can sometimes be disregarded as overpriced. Even the most seasoned investors who practiced this ideology can succumb to this kind of pitfall. The worst-case scenario from this is not all that bad. And that is that you just miss out on what would have been an attractive opportunity. But that's better, at the end of the day, than buying something that is overpriced and experiencing significant downside.

One of the firms that I have, in recent memory, been rather neutral on because of how pricey the stock has been, is The New York Times Company ( NYT ). Once thought a relic of a bygone era, the management team at the firm has reinvented the enterprise and turned it into a digital first publisher of news and other information. Management has eliminated debt and has accumulated tremendous amounts of cash on hand. The firm continues to grow and, at the same time, its share price has jumped nicely. Back when I last wrote about it in May of this year, I took a neutral stance by rating it a ‘hold’, which is the rating that I assign companies that I believe should see performance that more or less matches the broader market for the foreseeable future. I couldn't get past how pricey the stock was. Fast forward to today, and the stock is up 27.8% compared to the 15.2% rise seen by the S&P 500 over the same window of time.

Just recently, on December 19th, news broke from Apple ( AAPL ) that it and The New York Times had reached an agreement to include content from The Athletic, The New York Times’ sports-oriented publication, on Apple’s Apple News+ service. It was only a couple of years ago that The New York Times severed its relationship with Apple, but now, seeking further growth, it has once again dipped its toes into the Apple ecosystem. Naturally, this should bode well for both companies, though this is most certainly a bigger positive for The New York Times since Apple is such a large business that it is difficult for any single business change to have a material impact on the firm. But even with this arrangement, I cannot bring myself to become bullish on the publication even as I acknowledge that the company's future is bright.

Some good news

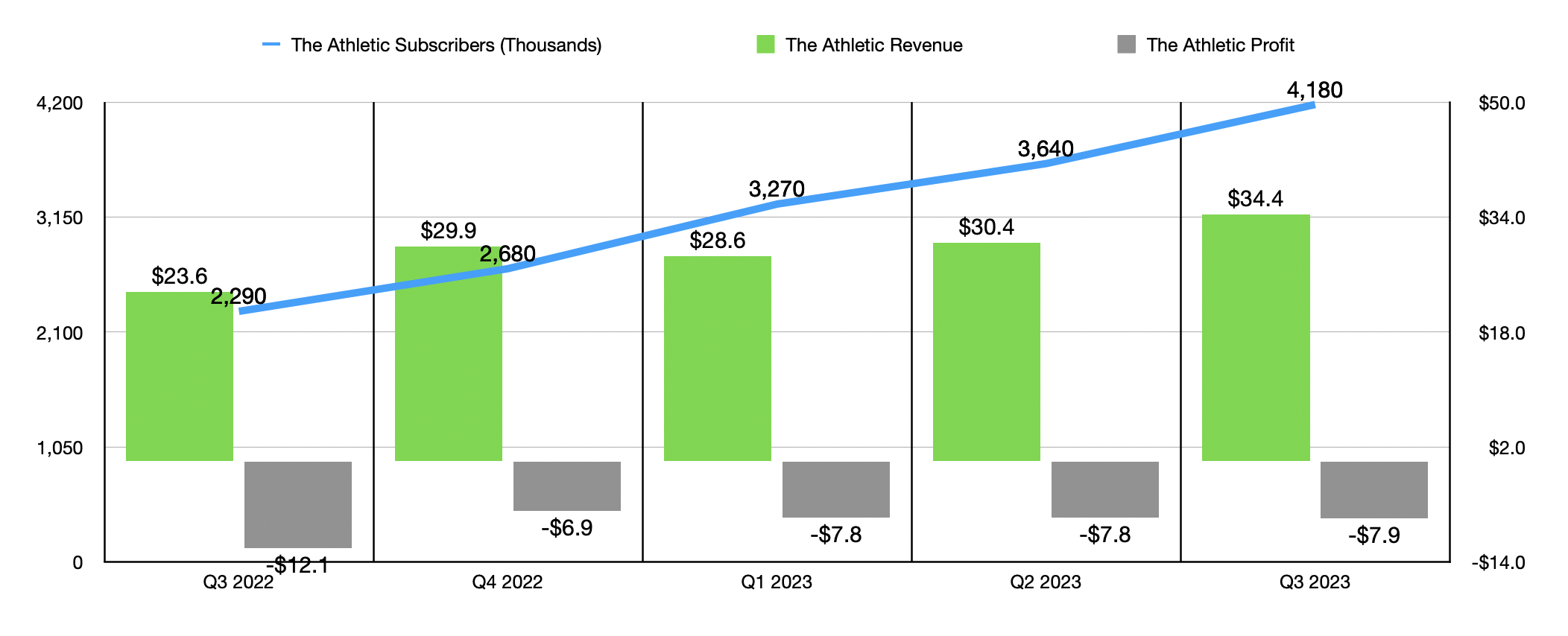

As I mentioned already, on December 19th, technology giant Apple announced that subscribers to the Apple News+ platform will now have access to premium daily sports journalism provided by The New York Times through its sports-oriented publication known as The Athletic. The New York Times purchased The Athletic for $550 million in cash and stock back in 2022. Since then, the company has made growing that platform a major priority. And so far, there has been some success on that front. In the final quarter of 2022, the digital-only platform boasted 2.68 million subscribers. By the third quarter of this year, that number had grown to 4.18 million. Quarter after quarter, the service has continued to generate operating losses. With an aggregate loss over the past four quarters totaling $30.4 million. However, revenue for the service continues to climb. In the third quarter of 2022, for instance, revenue was $23.6 million. That time this year, it totaled $34.4 million.

{kind=link}

Growing the reader base of the service can only be in that positive. It's highly likely that the company will receive some sort of financial kickback from Apple, but terms have not been made public. All that we know is that anybody paying the $12.99 per month for access to Apple News+ , as well as those paying the $37.95 per month for the Premier version of Apple One , will get access to the content provided by The New York Times. No official numbers have ever been released, but estimates provided by third parties suggest that around 19 million people are subscribed to Apple News+. This, combined with the addition of The New York Times’ Wirecutter service, which is a test and review site for products that will join The Athletic on Apple News+ early next year as part of the deal, will mean more eyeballs for the company's content that could convert into paying customers exclusive to The New York Times down the road.

Still not a great play

{kind=link}

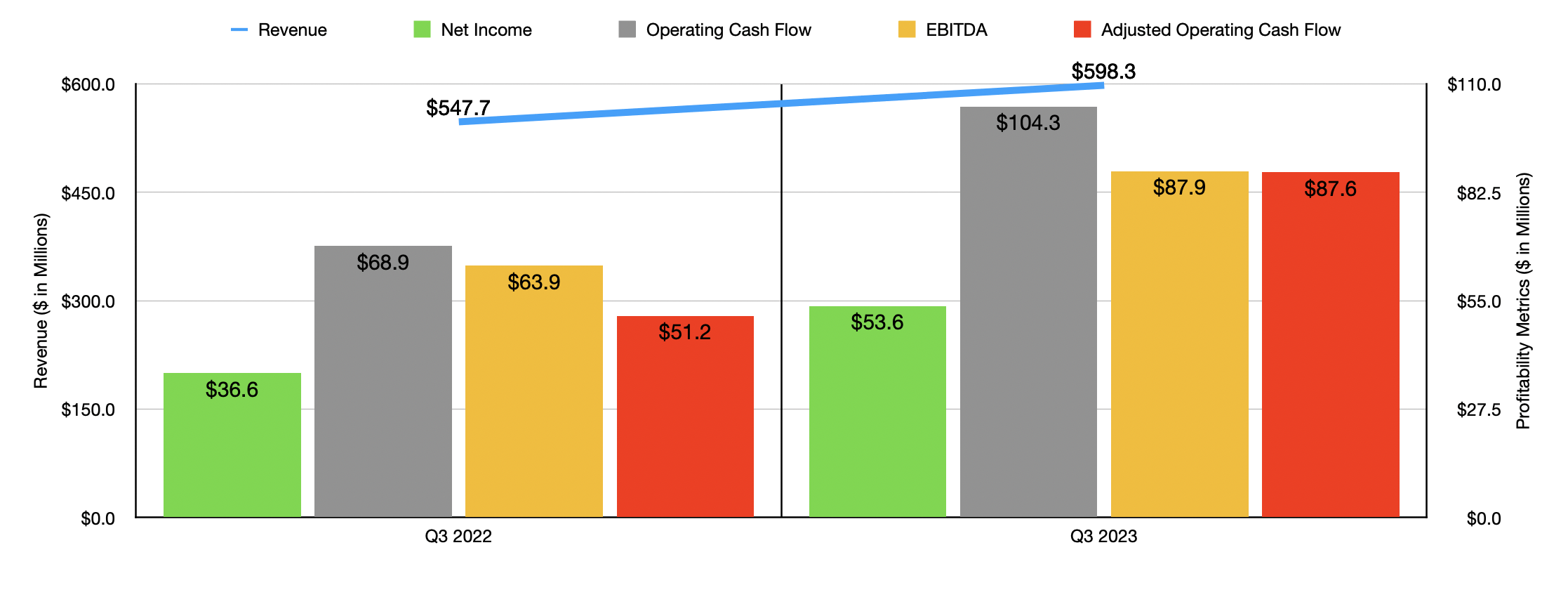

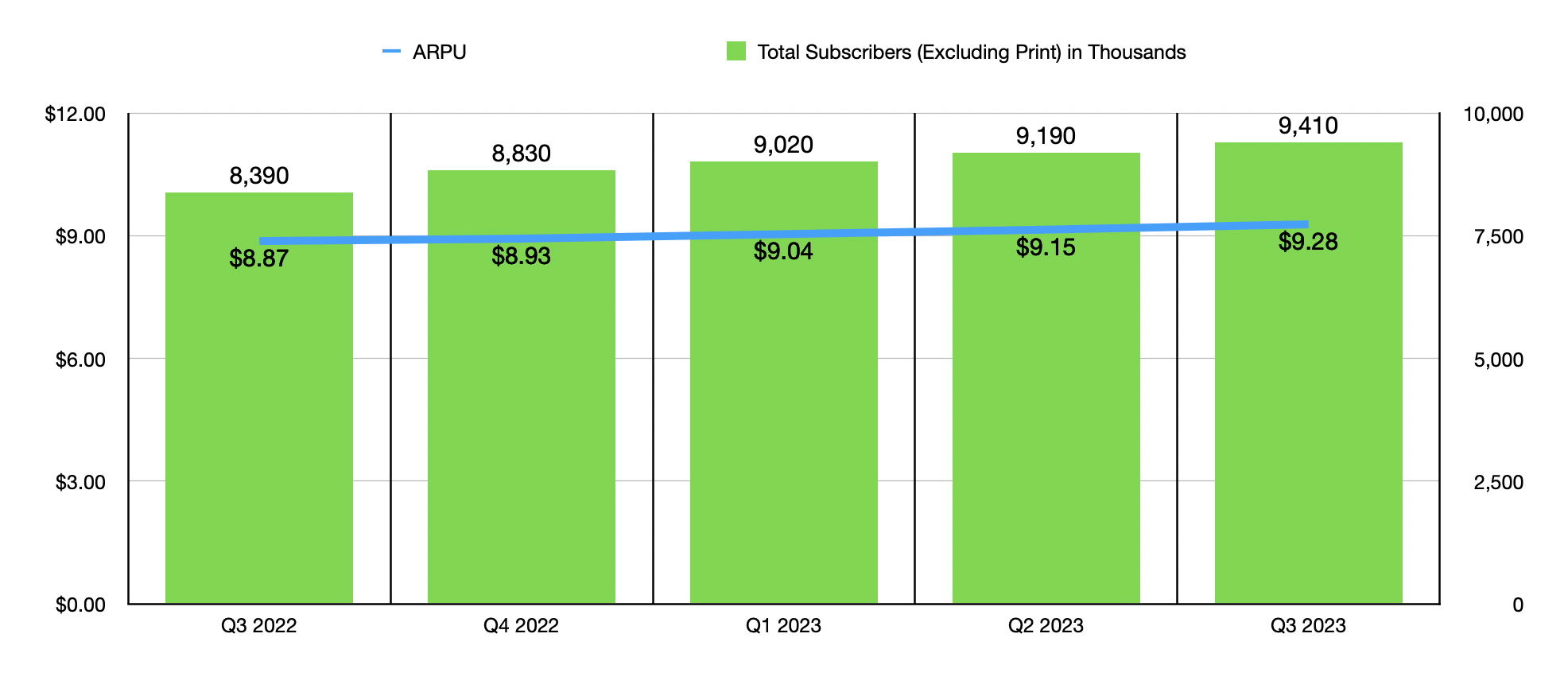

Pretty much any way you stack it, The New York Times has proven itself to be a quality company. As an example, we need only look at recent financial data provided by management. In the latest quarter, which would be the third quarter of the 2023 fiscal year, the company generated $598.3 million in revenue. That's up from the $547.7 million generated the same time last year. A 6% rise in advertising revenue was partially responsible for this increase. But there were other factors that played a major role as well. As an example, across the company's ecosystem, The New York Times boasted 9.41 million paid subscribers during the most recent quarter. That's up from the 8.59 million reported one year earlier. Over the same window of time, digital only ARPU for the company managed to grow from $8.87 to $9.28. Although this might not seem like much, this amount, spread over the 9.41 million paid subscribers that are on the platform today, would translate to an extra $46.3 million per year.

{kind=link}

Net profits have skyrocketed from $36.6 million to $53.6 million. Other profitability metrics have followed the exact same trajectory. As an example, operating cash flow grew from $68.9 million in the third quarter of 2022 to $104.3 million the same time of the 2023 fiscal year. If we adjust for changes in working capital, we would get an increase from $51.2 million to $87.6 million. And lastly, there is EBITDA. It popped from $63.9 million in the third quarter of last year to $87.9 million the same time this year.

{kind=link}

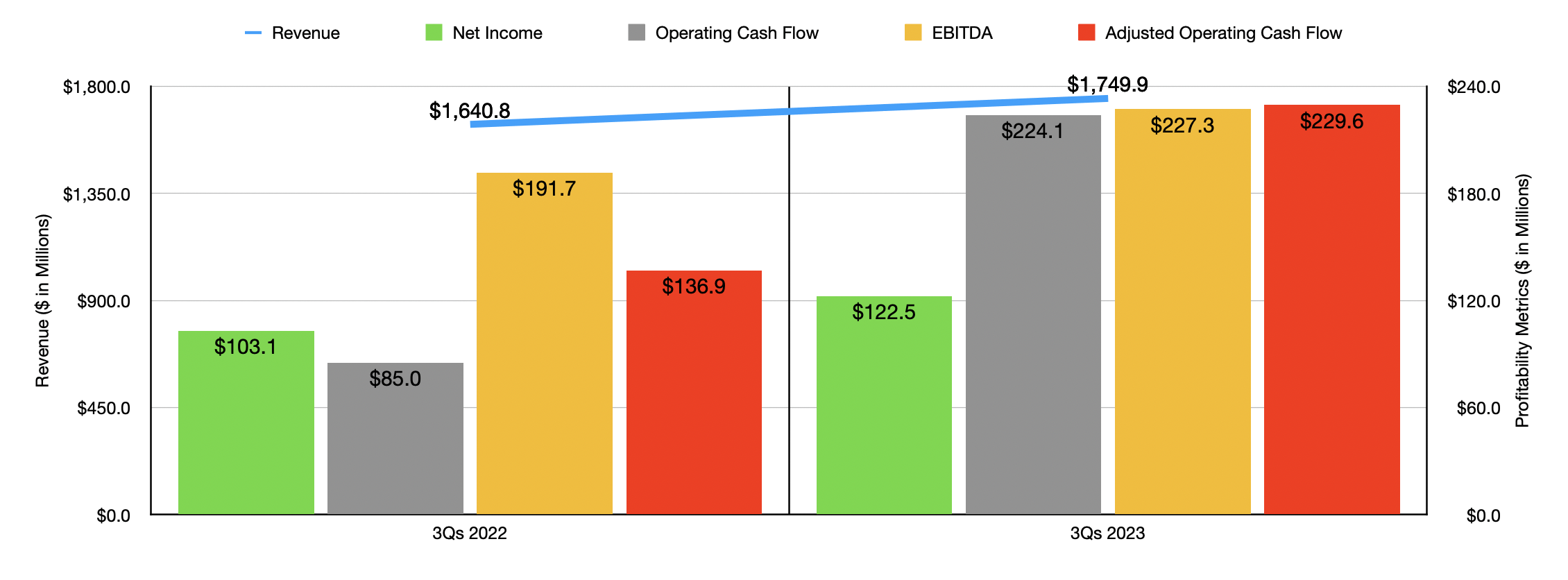

The third quarter was not a blip on the radar. If you look at the chart above, you can see financial results for the first nine months of 2023 compared to the same time of the 2022 fiscal year. Growth in digital only subscribers, combined with higher ARPU, was responsible for the increase in sales that the company reported. And in turn, it was also responsible for the rather material improvements on the company's bottom line.

It should also be said that there is another benefit to buying stock in The New York Times. That benefit is that the company has no debt on its books. In fact, if you look at cash, short term investments insecurities, and long-term investments in securities, and equate all of these to cash and cash equivalents, you would see that the company has gone from having $468.6 million on hand in the third quarter of last year to $587.8 million by the end of the third quarter of this year. This gives the company plenty of fuel that it can use in order to grow, plus it gives it a tremendous amount of flexibility should economic times deteriorate.

{kind=link}

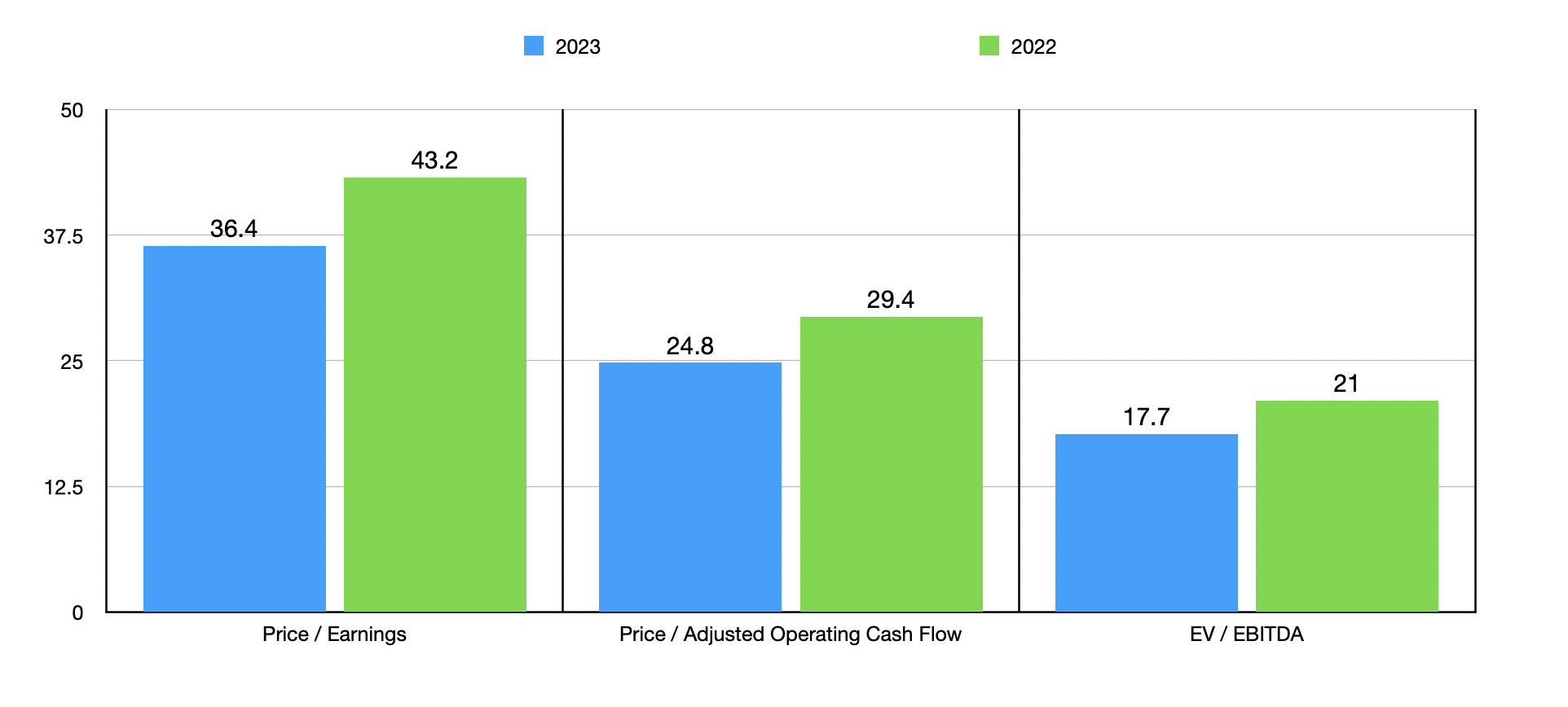

Given all of these facts, I have no problem classifying The New York Times as a high-quality company that likely has a bright future ahead for it. However, the stock is a bit too expensive for my liking. If we annualize out financial results for 2023, we would expect to have net profits of $206.6 million, adjusted operating cash flow of $303.1 million, and EBITDA totaling $390.1 million. Using these figures, as well as figures from 2022, I was able to value the company as shown in the chart above. I then compared the company to five similar firms in the table below. On a price to earnings basis, three of the five companies ended up being cheaper than The New York Times. This increases to four of the five when it comes to the EV to EBITDA multiple. But when it comes to the price to operating cash flow approach, our target ends up being the most expensive of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The New York Times Company |

| 36.4 |

| 24.8 |

| 17.7 |

| News Corp ( NWS ) |

| 99.5 |

| 13.4 |

| 14.4 |

| Pearson ( PSO ) |

| 24.4 |

| 18.3 |

| 7.0 |

| John Wiley & Son ( WLY ) |

| 117.1 |

| 6.9 |

| 23.5 |

| Scholastic ( SCHL ) |

| 20.8 |

| 6.1 |

| 6.7 |

| Gannett ( GCI ) |

| 19.7 |

| 4.4 |

| 4.8 |

Takeaway

From all that I can see, I'm very happy with The New York Times from an operational perspective. The company's decision to partner up with Apple will likely be thought of as a positive one down the road, even though we don't know the specifics of the transaction. For Apple, any news is good news, but this is unlikely to be material to that firm's story. Long term, I suspect that The New York Times will go on to do fine for itself. However, given how pricey the stock is, I still cannot in good faith rate it any higher than a ‘hold’ at this time.

For further details see:

The New York Times Continues To Soar, But Investors Should Be Wary