OXLCZ - The Retiree's Dividend Portfolio Jane's May Update: Account Balances Make A Large Recovery

2023-06-17 09:00:00 ET

Summary

- Jane's retirement accounts generated a total of $1,952.59 of dividend income for May 2023 vs. $1,514.11 of dividend income for May 2022.

- Only one company paid an increased dividend or issued a special dividend during the month of May.

- May was a busy month for trades in both Jane's Traditional and Roth IRAs, with a separate article planned to discuss these transactions in more detail.

- The primary focus of the portfolio is generating a stable and growing dividend income with an emphasis on capital preservation, aiming to provide a comfortable retirement for John and Jane.

Since the Taxable article was published a week ago we have continued to see improvement across all three indexes. A little over a month ago many investors probably felt like the person in the image above, but as I mentioned in the Taxable article we have seen all three indexes improve in recent weeks. The Nasdaq Composite continues to maintain a strong lead after seeing major benefits from the rally behind AI-related investments.

Even looking at John and Jane's current account balances in their accounts compared to what we saw at the end of the month is significant considering it has been just over two weeks.

| May 31st Balance |

| June 15th Balance |

| Taxable Account |

| $500,333.33 |

| $529,966.98 |

| Jane Traditional IRA |

| $405,164.90 |

| $424,082.37 |

| Jane Roth IRA |

| $195,153.82 |

| $201,813.88 |

| John Traditional IRA |

| $328,884.73 |

| $340,640.18 |

| John Roth IRA |

| $196,431.10 |

| $206,713.62 |

When you add up the differences in the numbers above it works out to be a change of over $75K in the span of two weeks. John and Jane have quite a bit of money invested but this large of a change in such a short time frame is pretty impressive.

Just as markets go down they can rise as well and this provides a great argument as to why we focus on selecting investments that we believe will generate consistent and growing dividends because these are more reliable than hoping for large market swings in a retiree's favor. While the core of the account focuses on the consistency of dividends we do take advantage of buying and selling shares when we think it makes sense to do so. May was a month with quite a few transactions (this will be covered more later in the article).

Background

For those interested in John and Jane's full background, you can find at least three articles a month published for the last five years detailing the performance of their portfolio. I have continued to evolve the report over time by adding and removing information/images to make the updates more useful to the average investor. Here are the key details that should be understood when reading these updates.

- This is a real portfolio with actual shares being traded. This is not a practice portfolio which is why I include screenshots from Charles Schwab to document every change that is made.

- I am not a financial advisor and merely provide guidance based on a relationship that goes back several years.

- John retired in January 2018 and has collected Social Security income as his regular source of income. John also currently withdraws $1,000/month from his Traditional IRA.

- Jane retired at the beginning of 2021 and decided to begin collecting Social Security early and has not made any withdrawals from her retirement accounts yet.

- John and Jane began drawing funds from the Taxable Account in 2022 at $1,000/month. After speaking with them this amount has been increased to $1,700/month. This withdrawal is still covered entirely by dividend and interest income.

- John and Jane have other investments outside of what I manage. These investments primarily consist of minimal-risk bonds and low-yield certificates.

- John and Jane have no debt or monthly payments other than basic recurring bills such as water, power, property taxes, etc.

The reason why I started helping John and Jane with their retirement accounts is that I was infuriated by the fees they were being charged by their previous financial advisor. I do not charge John and Jane for anything that I do .

The only request I have made of John and Jane is that they allow me to publish their portfolio anonymously because I want to help as many people as I can while holding myself accountable and improving my thought process.

I started this series to address issues I have had when reading other authors with similar types of updates (I am not saying they are wrong but I found myself questioning their actual performance because they never provided enough information to cover loose ends).

Here is My Promise to Readers:

- I aim to give as much information as needed so readers can feel confident that what I do is real.

- Even if you agree the results are real this does not mean I expect you to agree with me and I will always answer constructive criticism whenever possible. I will respond with the same genuine intent that the question was asked with.

- I am very transparent about the portfolio and consistency is a significant goal of mine. All of my data points (unless noted otherwise) are derived from month-end statements from Charles Schwab. Even when things aren't looking great (Spring 2020 for example) you will know because I provide enough information that it would be impossible for me to manipulate.

- This article is not intended to be advice or a call to action and is for informational purposes only (I am not a financial advisor and I don't claim to be one). My goal is to challenge conventional thinking and empower you to take control of your investments (if that's something you want to do).

While many authors require paid subscriptions to see their portfolio, I do not want to go that route and will continue to publish this series for free as long as there is enough interest to make it worth my time (and I spend A LOT of time on these articles).

Generating a stable and growing dividend income with an emphasis on capital preservation has become the primary focus of this portfolio. I am least concerned about capital appreciation which is why the decisions made will seem pretty conservative most of the time. I may measure the performance of the portfolio relative to indexes and ETFs but the key metric I am focused on is delivering a more stable source of cash flow to John and Jane over time that allows them to live a comfortable retirement that includes minimal stress related to finances.

Dividend Decreases

No companies in Jane's Traditional and Roth IRA accounts eliminated or reduced their dividend during the month of May.

Dividend Increases

One company paid increased dividends/distributions or a special dividend during the month of May.

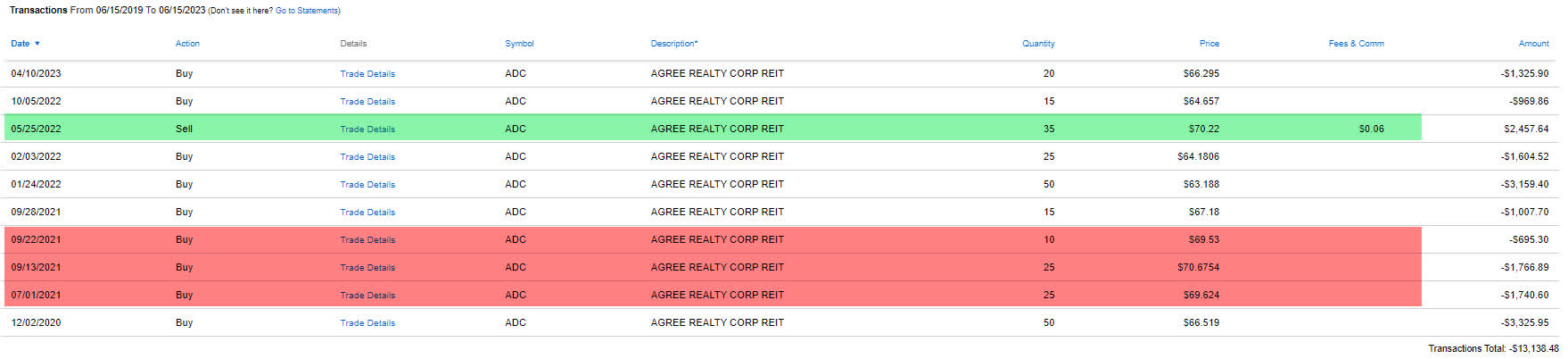

- Agree Realty ( ADC )

Agree Realty - Over the last five years we have seen ADC develop a strong pricing baseline at $60/share. During this five-year time frame management has been able to commit to a very reasonable dividend growth rate of 6.9% CAGR. We recently added more shares on the recent pullback (we consider the stock to be a very strong buy under $65/share) because we have reached a point where the yield is being maximized and therefore trading at the optimal price. Now what makes this true is that the company's earnings have been steady and offer no glaring concerns that would justify why the stock is trading at the low end of the 52-week price range.

ADC - SeekingAlpha - Dividend Yield (Seeking Alpha)

{kind=link}

This is a great time for us to continue accumulating shares so that we can ultimately reduce our cost basis and improve how effectively we are recycling capital. The trades below show that we reduced over half of our highest-cost shares back in May 2022 and now we are adding those shares back at a $4-5 discount. We may still add more shares but if prices push back above $70 we would likely take the remaining high-cost shares off the table.

ADC - Trade History (Charles Schwab)

{kind=link}

As you can see this is something that is done with the long game in mind which is why I try to really emphasize that this has nothing to do with day trading because it requires certain events and price points. I also have to factor in how much reserve capital Jane has at the time because a better opportunity might be a justification for not taking advantage of an attractively priced stock simply because capital constraints exist.

Retirement Account Positions

There are currently 38 positions in Jane's Traditional IRA and 22 in Jane's Roth IRA. While this may seem like a lot, it is important to remember that many of these stocks cross over in both accounts and are also held in the Taxable Portfolio.

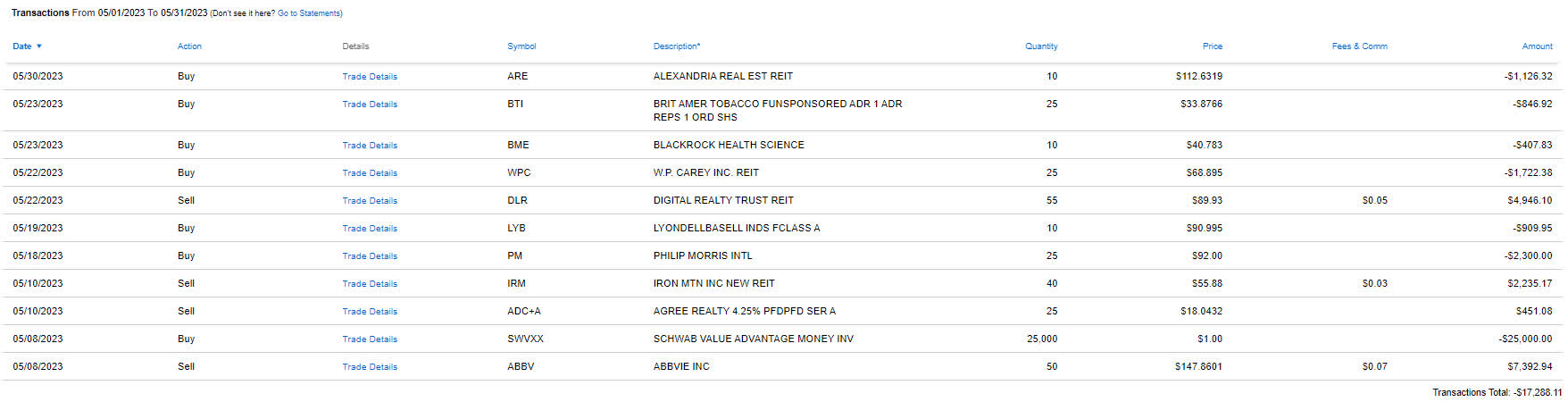

Below is a list of the trades that took place in the Traditional IRA during the month of May.

Traditional IRA - 5-2023 - Trades (Charles Schwab)

{kind=link}

Below is a list of the trades that took place in the Roth IRA during the month of May

Roth IRA - 5-2023 - Trades (Charles Schwab)

{kind=link}

As you can see there are a lot of transactions that took place during the month of May in both of Jane's retirement accounts. I will be doing a more in-depth review of these trades in a separate article. In that article, I will explain the most controversial trades shown which include the large sale of Digital Realty ( DLR ) and Broadcom ( AVGO ) shares.

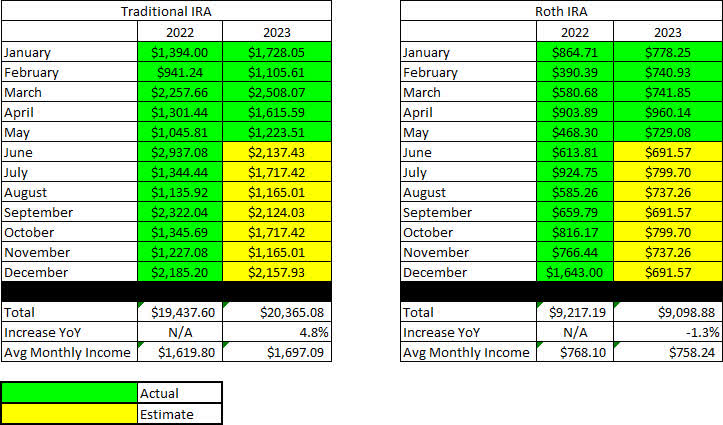

May Income Tracker - 2022 Vs. 2023

The account is set for modest dividend growth in the Traditional IRA and a slight decrease in the dividend income generated by the Roth IRA. Similar to the Taxable Account, the number of special dividend payouts in 2022 increased the yield of the portfolio at a faster pace (16.9% and 29.6% growth, respectively). While it's possible we could see more special dividends in 2023 I think it's more likely that management will focus on deleveraging the balance sheet or stock buybacks in most cases.

The Traditional IRA is expected to generate an average of $1,697.09/month of dividend income in 2023 compared to the average monthly income of $1,619.80 generated in FY-2022. The Roth IRA is expected to generate an average of $758.24/month of dividend income in 2023 compared to the average monthly income of $768.10 generated in FY-2022.

Remember that these figures above are provided as a snapshot in time and do not include dividend increases that have not occurred and err on the side of a more conservative payout. Almost every month when I update these numbers there is growth over my original projections, some of which, are related to human error because it's possible I forgot to increase/update the dividends expected in future months. With higher yields on money markets and CDs, I expect we will see a very light increase in dividend income for the year of around 3-4% (Roth & Traditional IRA combined growth).

At this point, Jane has decided she will not be making any withdrawals from these accounts which means that the dividends will be collected as cash and potentially reinvested when it makes sense.

SNLH = Stocks No Longer Held - Dividends in this row represent the dividends collected on stocks that are no longer held in that portfolio. We still count the dividend income from stocks no longer held in the portfolio, even though it is non-recurring. All images below come from Consistent Dividend Investor, LLC. (also referred to as CDI as the source below).

The tables below represent which companies paid dividends in May and how that income source has changed compared to the same month of the previous year.

Traditional IRA - 2022 V 2023 - May Dividends (CDI) Roth IRA - 2022 V 2023 - May Dividends (CDI)

The table below represents all income generated in 2022 and collected/expected dividends in 2023.

Retirement Projections - 2023 - May (CDI)

{kind=link}

Below gives an extended look back at the dividend income generated when I first began writing these articles. I find this table to be most useful when comparing how dividend income has improved for a specific month over the course of six years.

Retirement Projections - 2023 - May - 6 YR History (CDI)

{kind=link}

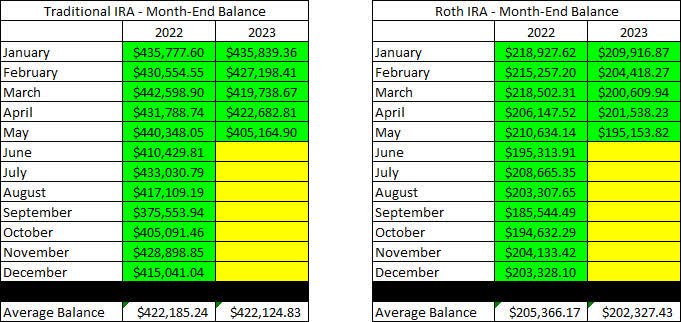

The balances below are from May 31, 2023, and all previous month's balances are taken from the end-of-month statement provided by Charles Schwab.

Retirement Account Balances - 2023 - May (CDI)

{kind=link}

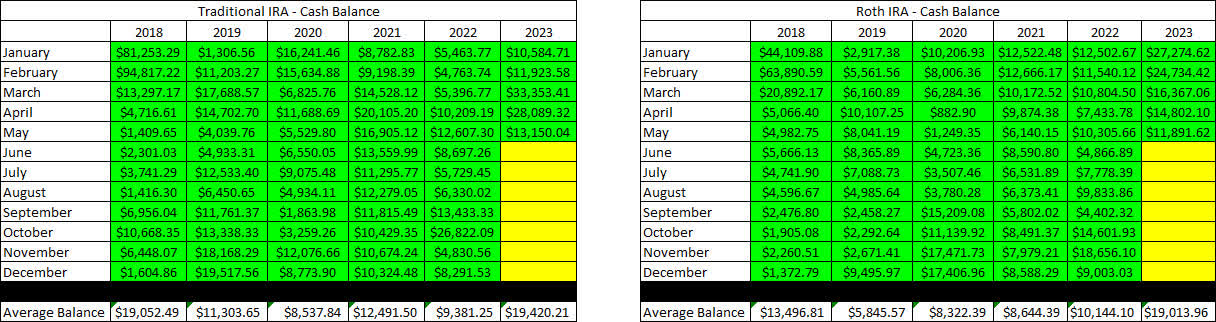

The next image is also pulled from the end-of-month statement provided by Charles Schwab which shows the cash balance of the account.

**Please note that cash balances may fluctuate based on CD renewal dates and the use of SWVXX because I only count the cash that is 100% liquid. There were larger fluctuations in 2019 and 2020 that we the result of deposits and withdrawals being made. There will be no contributions made into either account in 2023 now that Jane is no longer working.

Retirement Projections - 2023 - May - Cash Balances (CDI)

{kind=link}

The next image provides a history of the unrealized gain/loss at the end of each month going back to the beginning of January 2018.

Retirement Projections - 2023 - May - Unrealized Gain-Loss (CDI)

{kind=link}

I think the table above is one of the most important for readers to understand because it paints a story of volatile markets and why we employ the strategy of generating consistent cash flows to overcome the uncertainty of the market. If we were dependent on selling shares to generate income for John and Jane's retirement, they would have to be much more considerate of when they withdraw and how much they choose to withdraw.

For example, a withdrawal in 2020 where shares must be sold would destroy more value by locking in losses or poor performance by stocks being sold compared to making the same withdrawal in 2021.

In an effort to be transparent about Jane's Accounts, I like to include an unrealized Gain/Loss summary. The numbers used are based on the closing prices from June 15, 2023.

Traditional IRA - 2023 - May - Gain-Loss (CDI) Roth IRA - 2023 - May - Gain-Loss (CDI)

**I received some feedback on the yield column and have updated the column to now reflect the actual yield of the stock based on the most recently updated share price.

Conclusion

May has always been an uneventful month when it comes to the review of the accounts and this is because so many companies announce increased dividend payouts in the month of April. While the dividend increases were limited to ADC, the month was eventful in terms of trades and I will be writing a separate article to discuss that in more detail.

May Articles

I have provided the link to the most recent Watchlist article referenced at the beginning of the article as well as the article for the May 2023 Taxable Account.

Undervalued Dividend Stocks Watchlist - Adding LyondellBasell

The Retirees' Dividend Portfolio: John And Jane's May 2023 Taxable Account Update

In Jane's Traditional and Roth IRAs, she is currently long the following mentioned in this article: AbbVie ( ABBV ), Agree Realty ((ADC)), Agree Realty Preferred Series A ( ADC.PA ), Archer-Daniels-Midland ( ADM ), Broadcom ((AVGO)), Avient ( AVNT ), Bank of America ( BAC ), BlackRock Health Sciences Trust ( BME ), Bank of Nova Scotia ( BNS ), BP ( BP ), British American Tobacco ( BTI ), Canadian Imperial Bank of Commerce ( CM ), Cummins ( CMI ), Concentrix ( CNXC ), Digital Realty ((DLR)), Eaton Vance Floating-Rate Advantage Fund A ( EAFAX ), Enbridge ( ENB ), EOG Resources, EPR Properties Preferred Series E ( EPR.PE ), Eaton Corporation ( ETN ), East West Bancorp ( EWBC ), Essex, General Mills ( GIS ), GasLog Partners Preferred C ( GLOP.PC ), Honeywell ( HON ), Iron Mountain ( IRM ), Lexington Realty Preferred Series C ( LXP.PC ), Lumen Technologies ( LUMN ), LyondellBasell ( LYB ), Main Street Capital ( MAIN ), 3M ( MMM ), Altria ( MO ), NextEra Energy ( NEE ), New York Community Bank ( NYCB ), Realty Income ( O ), OGE Energy Corp. ( OGE ), Oxford Lane Capital Corp. 6.75% Cum Red Pdf Shares Series 2024 ( OXLCM ), Philip Morris ( PM ), PPG Industries ( PPG ), PIMCO Corporate & Income Opportunity Fund ( PTY ), Cohen & Steers REIT & Preferred Income Fund ( RNP ), Royal Bank of Canada ( RY ), Schwab Value Advantage Money Fund, TD SYNNEX ( SNX ), Toronto-Dominion Bank ( TD ), T. Rowe Price ( TROW ), Unilever ( UL ), UMH Properties ( UMH ), Verizon ( VZ ), Williams Companies ( WMB ), W. P. Carey.

For further details see:

The Retiree's Dividend Portfolio, Jane's May Update: Account Balances Make A Large Recovery