SWGNF - The Swatch Group: Growth In China And U.S. Markets Supports Price Rise Probability

2023-09-21 05:39:40 ET

Summary

- Swatch Group's stock price saw its biggest single day rise YTD on the release of its results in July. But the stock hasn't retained its momentum.

- It does, however, hold potential after the company reported robust sales growth in H12023, improved its margins and remains bullish for the remainder of the year.

- The company's forward P/E looks increasingly attractive on improved performance. I reiterate a Buy.

Since I last wrote about the Swiss company Swatch Group (SWGAY) in June, its price has declined by 3.3%. This isn’t a notable movement, but the lack of momentum is something to consider in light of my Buy rating and the fact that it released its half year (H1 2023) report in the interim.

In fact, year-to-date, the owner of the jewellery brand Harry Winston and of watch brands like Omega and Longines has declined by 9.5%. This raises the question, is it now a good time to buy it while it's still down or has the Swatch Group lost its mojo?

{kind=link}

Reasons for the earlier Buy rating

First, a quick look at the reasons for my Buy call. The company expected "strong sales growth in 2023” after a lacklustre performance in 2022. It was particularly optimistic about the China market’s prospects after it re-opened. During 2021, when the country first opened up after COVID-19 lockdowns, it made a big 42% contribution to the group’s revenues. By comparison, both Europe and America together contributed 35.3%.

Further, assuming that its net profit margin stayed steady at 2022’s levels of 11%, a revenue growth rate of 11.9% as per analysts’ estimates, yielded a 14.7% earnings per share [EPS] growth. This in turn translated into a competitive forward price-to-earnings (P/E) ratio of 14.3x compared to luxury peers. It was further reinforced by its trailing twelve months [TTM] P/E at 16.9x, which was not just lower than that for peers, but its own past levels too.

The financial update

With a positive outlook and attractive market multiples, however, the stock has still not gained momentum. This raises the question, what’s holding the Swatch Group back? To answer it, let’s take a look at its H1 2023 report.

First things first, on the day of its release, July 13, the stock jumped by 8.1%, the biggest single day gain seen YTD. Clearly, investors were happy with it. And indeed, there are noteworthy developments there.

{kind=link}

Robust sales growth, and across markets

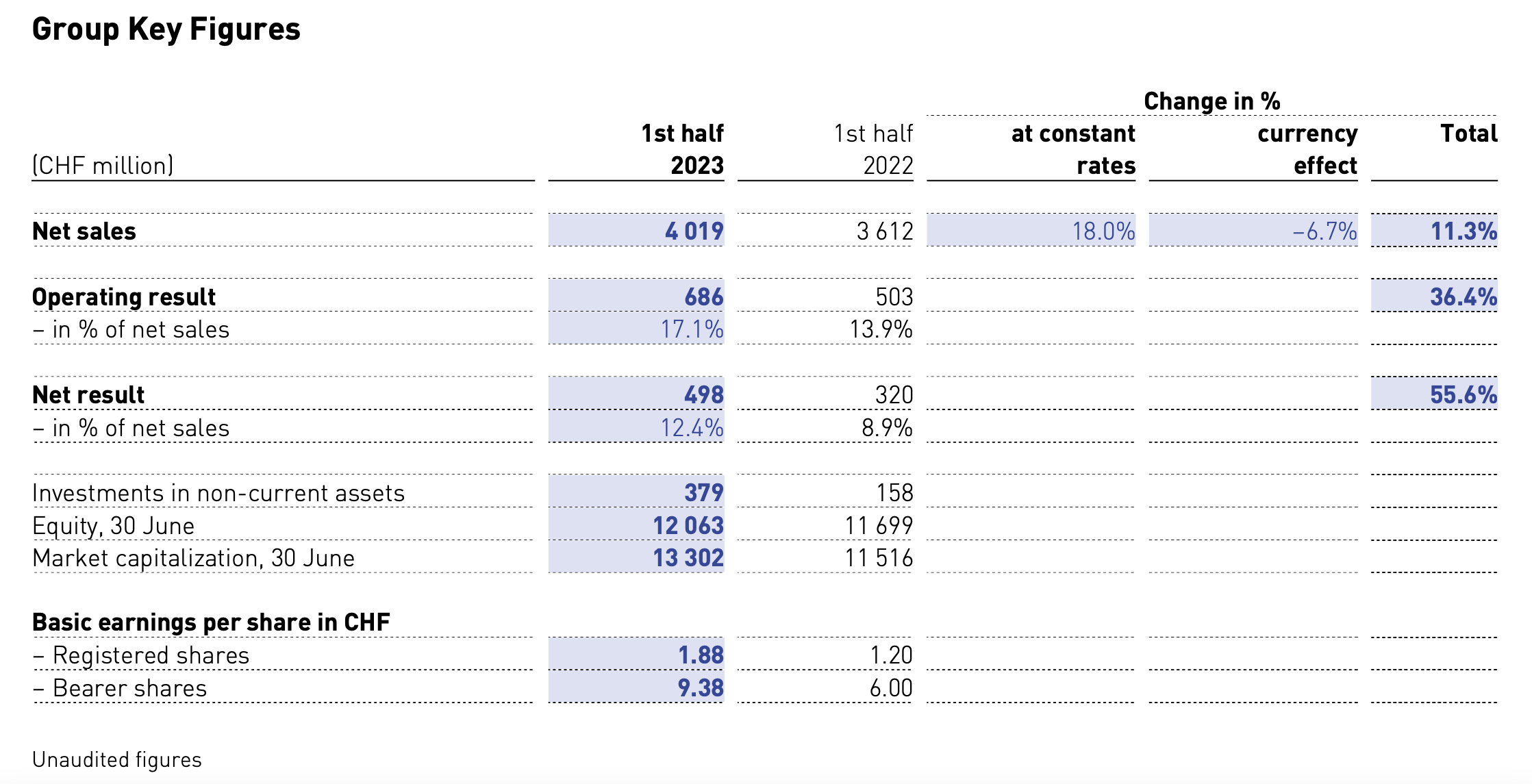

The group’s net sales at constant currency rose by 18% year-on-year [YoY], a vast improvement over the 7.4% growth in H1 2022. While the reopening of China was definitely a shot in the arm, it also revitalised sales at tourist destinations like Thailand and Macao.

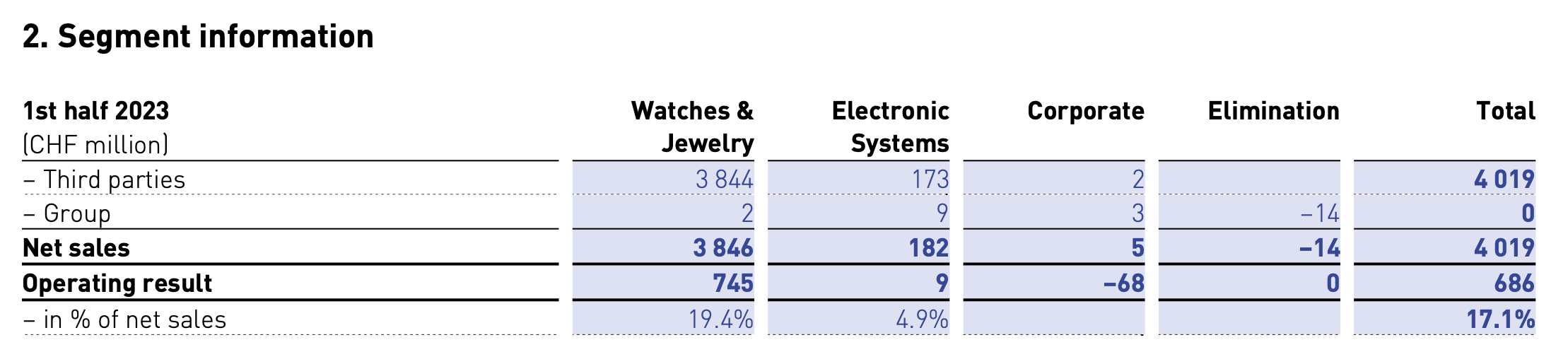

The company’s European market also remained healthy, with growth in its home country, Switzerland, increasing by almost 50% for the watches and jewellery segment. For context, this segment accounts for almost 96% of the company’s revenues, with the remainder contributed to by the electronic systems segment.

{kind=link}

Interestingly, it also says that “Sales in North America developed extremely well..”. This is refreshing to know considering that the weakening US market has held back luxury companies’ growth recently. Like in the cases of the big French luxury company LVMH ( LVMUY ) and Gucci owner Kering (PPRUY).

But here’s the really interesting part. It adds that sales growth was strong “particularly in the lower and medium price segments, with high double-digit growth rates”. It mentions Tissot as one brand that has made “significant market share gains in North America”. The group’s namesake watches also saw accelerated demand globally.

Rising margins

Despite the buoyancy in its lower-priced segments, the company has seen a notable rise in operating profit margin to 17.1%, which is not just 3.2 percentage points higher than that in H1 2022, it’s also higher than the full year 2022 margin of 15.4%. Similarly, the net margin has improved too, to 12.4%, up 3.5 percentage points from H1 last year.

This is of course partly due to much better revenue growth, but also because the cost of revenues at 14.2% of revenues, is a smaller figure than the 17.4% seen in H1 2022. Also operating expenses as a proportion of revenues remained essentially unchanged at 68.8%.

Positive outlook

While it doesn’t provide numerical guidance, the Swatch Group does continue to remain bullish for the remainder of the year. It says it expects “excellent growth opportunities in local currencies for the second half of 2023 in all regions and price segments.” It will continue to focus on the relatively lower-priced segment, which appears to be a sound strategic move considering its recent successes.

It is, however, diffident about the exchange rate effect, which shaved off 6.7 percentage points from its reported growth, which ended up at 11.3%. That the effect was just 0.9 percentage points in H1 2022 puts it in perspective.

The market multiples

Assuming that the company sustains its 11.3% reported revenue growth for all of 2023 and that its net margin sustains at the current higher levels of 12.4%, SWGAY’s forward P/E drops to 11.7x from 14.3x when I estimated it last. Further, its TTM GAAP P/E has already fallen to 16.1x from 16.9x the last time.

It does need to be mentioned though, that its TTM P/E is higher than that for the consumer discretionary sector at 15.3x . I say this, keeping in mind the expanding sales for its lower to medium-range segments, which would bring it closer to the average consumer discretionary sector stock. At the same time, the fact that it has high-end brands in its portfolio suggests that some premium is justified. LVMH for instance, has a 22.7x TTM P/E.

What next?

Looking at the overall market multiples picture, at the very least, there’s a case for more sideways movement from the Swatch Group stock or its ADRs. But as I see it, the more probable outcome is a price rise going by the decline in its forward P/E ratio. I expect to see a 15-20% upside to it, especially considering that there will be no financial releases from the company until early 2024, which tends to move the stock.

There could be sentiment driven fluctuations on account of trends for other luxury companies, but fundamentally it has differentiated itself with good sales in the US market. Sure, there are risks stemming from a potential slowdown not just in the US, but also because there are continued concerns about China. But barring a black swan event, it’s really too late in the year now for much to go wrong. I’m retaining the Buy on Swatch.

For further details see:

The Swatch Group: Growth In China And U.S. Markets Supports Price Rise Probability