BURBY - The Swatch Group: Improving Margins Optimistic Outlook

Summary

- The Swatch Group has performed better in 2023 so far compared to most other luxury companies. I think it could do even better.

- Its operating margins have improved in 2022, and it appears optimistic about growth this year as China's economy recovers. Its P/E is also relatively attractive compared to peers.

- Its long-term price performance is wanting, and its dependence on a single market is uncomfortable, for now, it is still a Buy.

The Swiss luxury watchmaker The Swatch Group ( SWGAY ) has seen one of the best price performances in 2023 among all luxury stocks' ADRs. With an increase of 16%, it is second only to the British trench coat manufacturer Burberry ( BURBY ), which has risen by 19%. This is a significant change for the better for it, considering that the last time I wrote on it in December last year, it had seen a year-to-date (YTD) decline of 11.8%.

Seen in a larger context, that was hardly a good time for the luxury sector in the stock markets. While prices had started recovering, all of them were still trading below the levels at which they had started the year. But 2023 has started on a good note for consumer stocks as such, given that it is becoming increasingly evident that inflation is on the declining path, and luxury stocks are no exception.

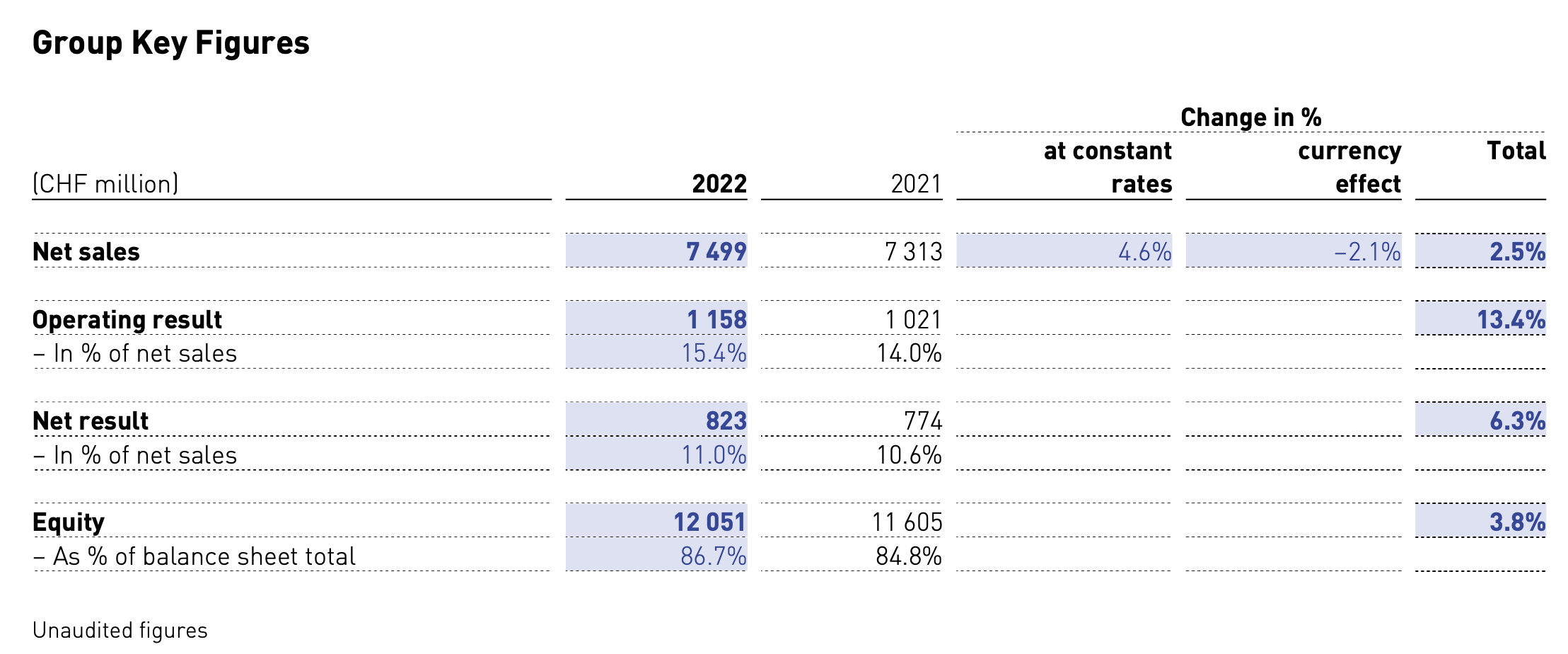

Improved operating margin, slow sales

For companies like Hermes ( HESAY ) and LVMH ( LVMUY ), which had high operating margins despite inflation, easing off the rate of price increases is less material than for a company like Swatch. At 14%, its operating margin was the lowest among luxury companies last year, implying relatively limited pricing power. But on the plus side, this also means the potential for margin expansion during times of more limited inflation, as is evident from its recent figures for 2022. The operating margin has risen to 15.4% in 2022 on a slower pace of increases in operating costs.

{kind=link}

This is despite its slow revenue growth. The company's net sales grew by a slow 2.5% at market exchange rates and a slightly better 4.6% at constant exchange rates. This is a sharp decline even from the first half of 2022 when its sales grew by 7.4%. The reason? China. Swatch says that "Consistent double-digit sales growth in Europe, America, the Middle East, and most of the Asian markets was severely dampened by the significant decline in sales in China."

Optimistic outlook

But the company, which owns 17 brands including Omega and Harry Winston, a maker of watches and jewelry respectively, is quite upbeat for 2023. In its latest update, it says that it "aims for a record year in 2023". That is quite encouraging, but I would take it with a pinch of salt. Last year, the company had anticipated "double-digit sales growth in local currencies in 2022". As we know from the results, that has not happened.

To be fair, though, last year turned out to be a challenging one for companies with significant interests in China. The country accounts for 42% of Swatch's sales, so it felt the drag from COVID-19 related challenges there. Not just Swatch, but all luxury companies have shown lower growth from Asia in the past year because of this reason.

Some of them have been able to sustain strong growth nevertheless on account of robust demand from other markets. Not Swatch, though. In the context of its Watch & Jewelry segment, which generates most of its revenues, it mentions a negative impact of CHF 700 million because of the demand slowdown in China. If this were not the case, its revenue would have grown by a far healthier 12.1%.

It is exactly because of the expected improvement in sales to China that the company expects a better 2023. Among key country economies, the IMF expects China to see higher growth in the year. Also, the growth rate is expected to be at 5.2%, which is second only to India among these economies. Signs of improvement in the market are already visible in the context of Swatch. In its latest release, it mentions the sales growth in China in January. Specifically, it talks about the return of quick consumption recovery after the end of restrictions in the country, as well as in markets like Hong Kong and Macau. It expects that sales in travel destinations will revitalize as well.

Relatively attractive P/E

At this point, Swatch is trading at a trailing twelve months ((TTM)) GAAP price-to-earnings (P/E) ratio of 20.2x, which is nowhere close to being the highest for luxury stocks (see chart below). It is true that some of them like LVMH and Hermes have shown much better performance this year, so it is not entirely comparable. So let us consider the example of Burberry, which has also been impacted by the China lockdowns. Even that is trading at a higher 23.1x, a higher P/E than that for Swatch. So there is likely to be more upside for the company for now in my view. Swatch's P/S is also attractive compared to peers.

Seeking Alpha

Long-term performance underwhelming

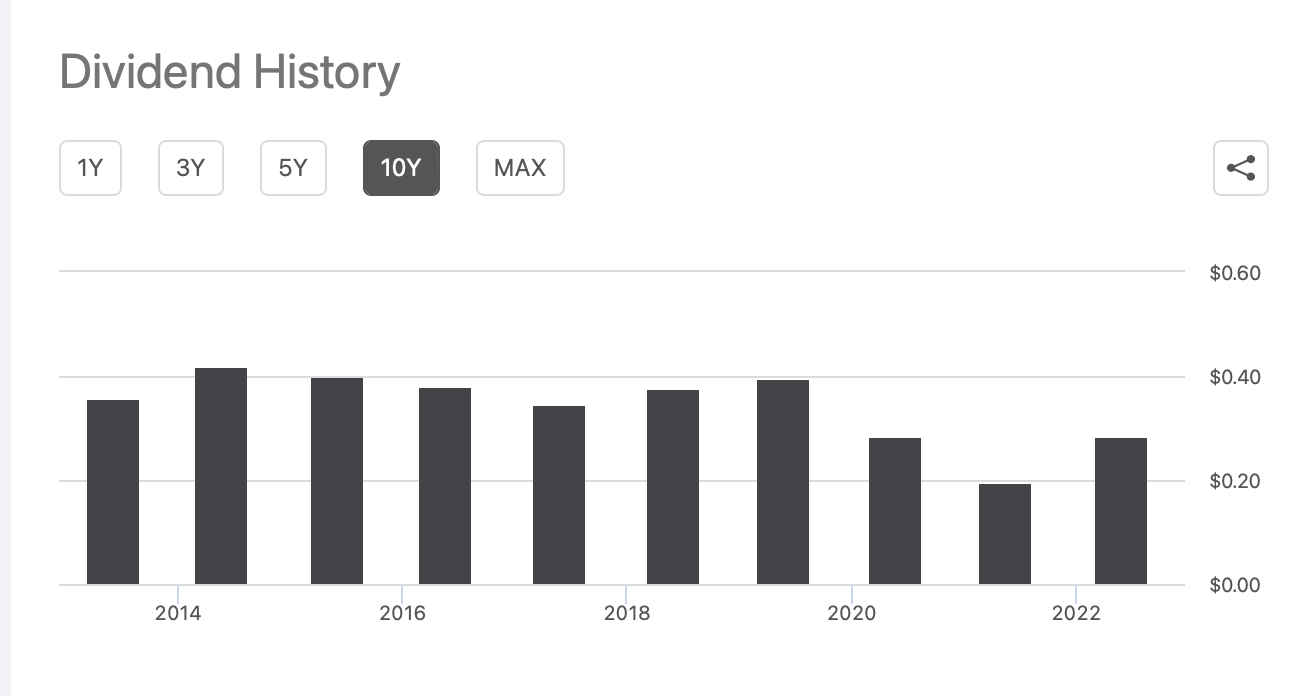

It is not like China was the only downer for it, though. Swatch's price returns over the long term are poor. An investor who had bought it 10 years ago, would have seen a 40% decline in their investment by now. And if it was bought five years ago, the capital would have shrunk by 18%. It is some small consolation that it pays a dividend, but the payouts have not grown consistently (see chart below) either and its TTM yield of 1.7% is not particularly attractive.

{kind=link}

What next?

For now, though, I think there is an upside to Swatch. In the luxury segment, it is still far more affordable than most other ADRs. Its growth can improve with China's recovery, even though there could be an impact from a growth slowdown in Europe and the US. Its operating margin can also improve, as is reflected in its 2022 figures. For these reasons, it is a Buy for me. At the same time, I would still not consider it a long-term buy for now, considering its past price performance and the extent to which it is dependent on one market for growth.

For further details see:

The Swatch Group: Improving Margins, Optimistic Outlook