SWGNF - The Swatch Group: Moderated China Expectations But Growth Still Likely

2023-06-30 08:15:13 ET

Summary

- The Swatch Group's stock price has declined by 18.3% since February, despite no significant price-moving numbers being released.

- The company is optimistic about 2023, however, expecting strong sales growth.

- Other luxury companies have reported good Q1 2023 results for the Asia market too, indicating potential for recovery.

- I maintain a Buy rating on it, but look out for changes in its outlook in the upcoming results in July.

Since the last time I wrote about the Swiss watchmaker, The Swatch Group ( SWGNF ) in February this year, it has not released any price-moving numbers. Its key figures for 2022 were available even at the time, so I reckon they were priced in by the time the company released its detailed full-year financial results . This makes it a curious fact that its price has declined by 18.3% since, even while some other luxury stocks have picked up.

{kind=link}

Strong Asia Market

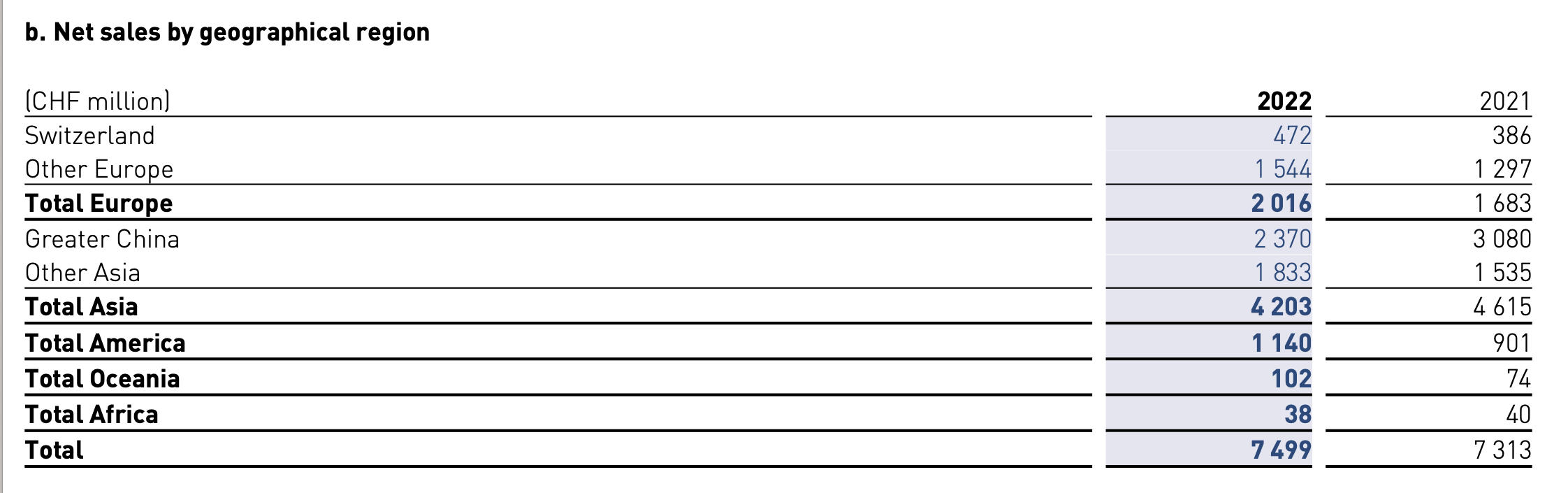

There is something to consider however, that can impact its numbers significantly. And that is the China market. As it happens, The Swatch Group has far more exposure to China than its luxury peers. Reciprocally, Europe and America have a smaller share. In 2022, even when China was a drag on the company's growth, it still contributed to 31.6% of the revenues and the Asia market was a huge 56% of its total sales. The figure was even higher at 63% in 2021 for Asia, with China making a 42% contribution, while the share of Europe and America put together was at 35.3%.

{kind=link}

This year started with high hopes for the Chinese economy and luxury spending trends during the Lunar New Year period indicated a good year for the sector. Expectedly, even The Swatch Group has been optimistic about its prospects for 2023. In its initial outlook for 2023, the company had said "The sales growth in January in China reinforces the Group's expectation to aim for a record year in 2023.". It noted that not only had China's recovery since the lifting of the COVID-19 restrictions been swift, but that it would also encourage sales in tourist destinations.

Macroeconomic weakness

Interestingly, in its annual report it no longer made a mention of "record growth", though it retained the fact that it is anticipating "strong sales growth in 2023". This is not surprising considering the slowdown in Europe and America as well as the fact that its fastest growth it has seen in the past decade is 30.7% in 2021, which is probably not easy to beat. For context, in the last 10 years, the company's growth has actually shrunk slightly on a compounded annual growth rate [CAGR] basis.

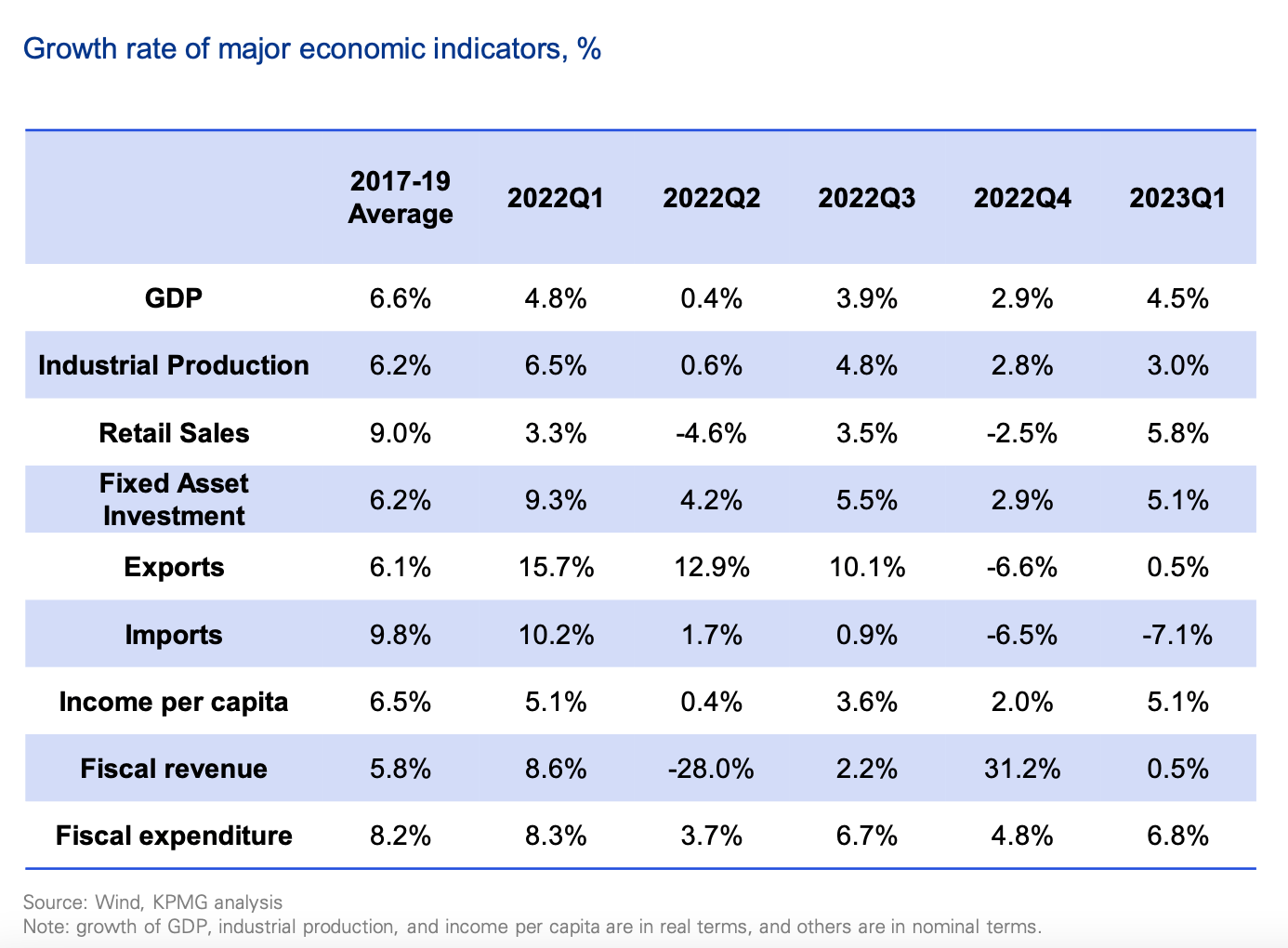

Moreover, going by the latest weakening in China's economy, it is just as well, in hindsight. While there is no doubt that the China market saw promising luxury spending during the Lunar new year period, it is doubtful if it will indeed be a robust year for luxury sales moving forward, as indicators of growth from industrial production to exports and investments showed a come-off even in Q1 2023 (see table below).

China's Key Economic Indicators (Source: KPMG)

{kind=link}

The impact of China's weakness

This can be really bad news for The Swatch Group, going by its 2022 growth figures. Even though the company showed strong growth in Europe and America of 19.8% and 26.5%, the decline in Asia revenues by 8.9% brought its total revenue growth down to a measly 2.5%. It is unlikely that 2023 will be a repeat of 2022, but the past year is still indicative of the extent of effect China has. Moreover, if all its big markets slow down, growth can be underwhelming.

At the same time, there is some reason for optimism as well. Other luxury companies reported a good Q1 2023 for the Asia market. LVMH ( LVMUY ), for instance, saw a 14% year-on-year (YoY) growth, which had a steadying effect on its overall figures even as the American market slowed down. A similar story is visible for Richemont (CFRUY), which saw a 26% growth in Asia Pacific revenues in the quarter (its Q4 FY23).

Also, the slowing down in China's economy needs to be seen in perspective. It is still projected to grow at 5.6% in 2023 by the World Bank, even as risks are "tilted to the downside ". This is still much higher than the 3% growth it saw in 2022.

The future in numbers

So far, analysts are also relatively bullish on The Swatch Group's growth for this year, which is estimated to be at 11.9% in USD terms. If the company's net profit margin remains the same as in 2022, at 11%, the company will see a 14.7% growth in EPS.

This in turn translates into a forward price-to-earnings (P/E) ratio of 14.3x. On the face of it, this looks rather competitive compared to peers like LVMH and Richemont at 23.7x and 18.9x respectively. At the same time, these companies have a far stronger history of growth, have higher margins and we have more visibility on their performance for 2023 so far. The same arguments apply when we consider the trailing twelve months [TTM] P/E, which is at 16.9x compared to LVMH's 30.9x, Richemont's 22.6x and even Kering's ( PPRUY ) 17.4x. In other words, there are good reasons for why Swatch is trailing its luxury peers.

What next?

It is worth noting, however, that SWGNF's P/E is lower now than it was in February, at 20.2x and in fact, is rather low even compared to its past year's P/E . This is despite the fact that there is no direct news on the group that could impact the stock. And other luxury companies have actually reported healthy numbers in Q1 2023, not the least of which is down to the recovery in China and despite a slowing down in America.

The company itself is quite upbeat on its prospects based on the China factor alone, as would be expected, based on considering the massive share of the market in its revenues. Analysts, too, are positive on its prospects for 2023. My estimates based on these revenue projections, for its EPS also indicate that its future P/E looks competitive.

There is of course the fact that The Swatch Group is not as financially robust as its peers, but if it did indeed see robust growth and earnings this year, this would be a good time to buy it now. I would temper my expectations about the extent of growth it can see, based on some recent weakness in China. But that is not enough to make SWGNF a total write-off, especially after its recent price decline. I maintain a Buy rating on it now, but would look out for changes to its outlook in the upcoming results in July

For further details see:

The Swatch Group: Moderated China Expectations, But Growth Still Likely