SWGNF - The Swatch Group: Undervalued Despite Issues

2023-06-12 10:57:14 ET

Summary

- Swatch Group's high-quality business model and impressive margins make it an attractive investment despite stagnating sales due to increased competition.

- The luxury watch industry experienced a boom post-Covid, with Swatch's luxury brands and jewelry benefiting from it, but the hype seems to be subsiding.

- The non-luxury segment is struggling with increased competition and a difficulty with conveying its value proposition to consumers.

Investment thesis

Our current investment thesis is:

- Swatch (SWGAY) has a high-quality business model, operating a range of watch brands, as well as other related services, allowing the business to benefit from shared competencies and scale. This gives the company impressive margins.

- The bubble in the luxury watch industry looks to have popped but we are still bullish.

- Swatch's sales have stagnated in the last decade, as interest in its mass-market offering slows and the company faces increased competition. We are concerned that Management is unable to deliver consistent growth.

- Despite the concerns, Swatch is far too cheap given its performance, even if demand is currently underwhelming.

Company description

Swatch Group AG is a global company that specializes in the design, manufacturing, and sale of finished watches, jewelry, watch movements, and components.

It operates in two main segments: Watches & Jewelry and Electronic Systems.

{kind=link}

Share price

Swatch's share price has performed poorly in the last decade, trading flat when accounting for dividends. This is a reflection of the difficult period the company has faced, with increased competition and poor brand development.

Financial analysis

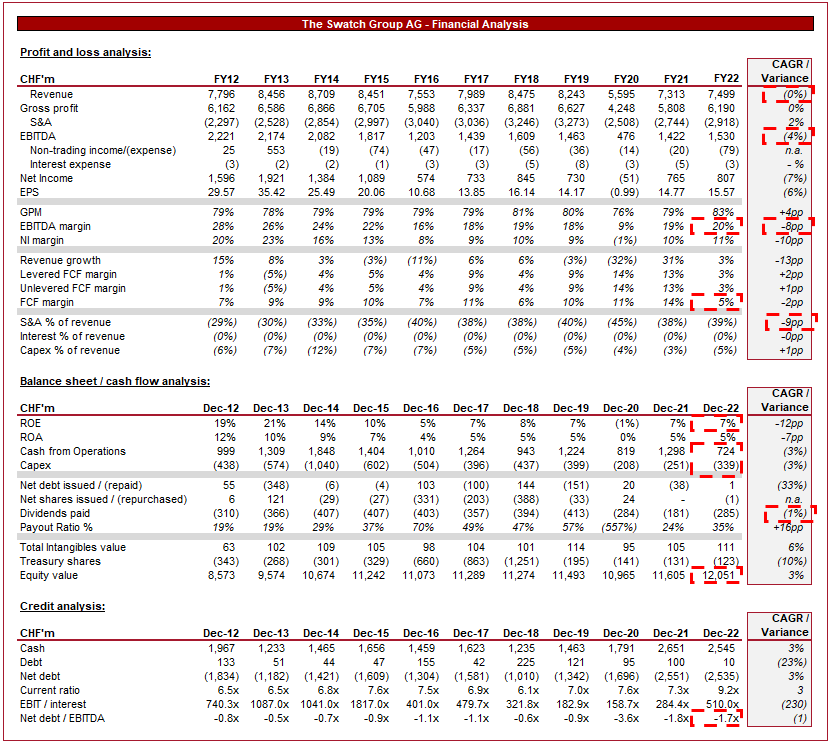

Swatch financials (Tikr Terminal)

{kind=link}

Presented above is Swatch's financial performance for the last decade.

Revenue & Commercial Factors

Swatch has experienced revenue stagnation, with a growth rate of <1% in the last 10 years. The difficulty for the business has been the achievement of consistent growth.

Business model

Swatch operates across the horological value spectrum. The Swatch and Certina brand sell watches as cheap as $150, Tissot and Longines operate in the $1000-$5000 range, Omega and GO in the $5k-$30k range, and Breguet and Blancpain beyond this. Further, the company owns related productions services within its supply chain. The Swatch business model is built on exploiting shared competencies to generate scale benefits. The primary example of this is mechanical watch movements, which are built by the Swatch brand and shared among many brands (Not in every case, such as with Breguet). The cost of developing a high-quality, reliable movement is substantial, and the alternative is to buy from a 3rd party (Which is also not cheap). One of the most popular movement producers is ETA, which is owned by the Swatch Group.

We like the Swatch business model. It is simplistic in its approach but allows the business to free up resources for marketing, as well as achieve strong profitability. The retail industry is highly competitive and so a cost advantage is critical to outperforming.

Luxury watches & Jewelry

The luxury watch industry experienced an unexpected boom post-Covid, with many luxury brands unable to meet demand. To this day, most Rolex dealers globally have little to no stock, with new deliveries sold immediately. This led to a rapid increase in the second hand value of watches and consumers having to purchase less desirable watches and jewelry in order to be considered worthy enough to buy the in-demand models.

Unsurprisingly, many wealthy individuals flocked to a range of highly regarded brands as a means of getting in on the hype. Breguet, Blancpain, and Omega benefited well from this, propelling the company to an impressive 31% growth rate in FY21.

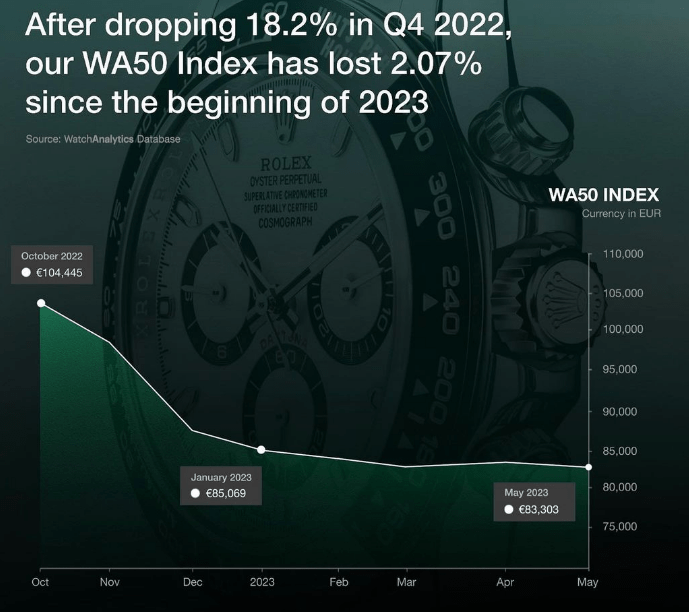

This hype looks to have subsided, likely due to the rapid increase in rates and the onset of a bear market. Watch Analytics has created an index of the most popular luxury watches, which suggests the market continues to decline as demand evaporates. This is a concerning trend that could imply a further slowdown in sales, and more likely a decline (Given the index is weighted toward Rolex, Audemars Piguet, and Patek Philippe, which are the most popular brands and most resilient).

{kind=link}

Although the near-term is concerning, we are bullish on the luxury segment long term. Firstly, and most importantly, the luxury watch industry has operated successfully for over a century. The demand for complex machinery on the wrist will remain so long as the rich have excess money to spend. Further, much of the increased demand is from emerging markets, particularly in Asia, which now presents a significant growth opportunity. Rising disposable incomes, increasing urbanization, and importantly, rapid growth in millionaires are driving this. We expect demand from these regions to continue in line with economic development.

Non-luxury watches

The increasing popularity of smartwatches, with advanced features like fitness tracking, notifications, and mobile connectivity, has disrupted the traditional watch market and represents a key risk to Swatch. Swatch has developed its own range of smartwatches but the brand lacks the credibility of Apple (AAPL), Samsung (SSNLF), Garmin (GRMN), Fitbit, etc in this space. On the affordable side, Swatch is competing against cheap imports which are a fraction of the price.

The growth of e-commerce and online retail channels has transformed the way consumers purchase watches in the affordable segment. Consumers now have significantly more choices and ease of shopping around, creating increased competition for Swatch. Further, as the company operates a brick-and-mortar approach, it is unable to compete on price with online marketplaces.

These two factors are key drivers for the underperformance in our view, and we do not see a material change in circumstances. Swatch has struggled to fight back in the non-luxury segment and we believe this is due to a lack of development in its value proposition. Consumers choosing cheaper products, or alternatives is a reflection of undesirability. The issue with retail is that demand is high and tastes change, so it could just be that Swatch's mainstream brands are no longer considered desirable.

The rise of social media platforms and influencer marketing has transformed the way brands connect with consumers. We believe marketing is one of Swatch's strong competencies, with the business regularly doing limited additions and partnerships in its namesake brand as a means of driving interest. We recently saw the company do something unheard of in the industry as a means of driving interest. It took a luxury model from its portfolio (the Omega MoonSwatch) and created a cheap version... the MoonSwatch. The hype around this watch was massive and was a success both financially and from a marketing perspective. We would like to see Swatch do this with more of its heritage models.

Economic & External Consideration

Swatch's near-term performance is being impacted by the current economic conditions, which pose a risk to the company. The prevailing situation of heightened inflation has led to a decrease in consumers' willingness to spend on non-essential items, focusing on the defense of capital. We believe this is a contributing factor to the low growth in FY22.

Looking ahead, inflation will gradually decline in the coming quarters, as rates are beginning to work. The key factor that needs to be addressed for a more positive outlook is the return of expansionary monetary policy.

Margins

Swatch has great margins, with a GPM of 83%, EBITDA-M of 20%, and a NIM of 11%.

These margins are a reflection of the scale benefits we identified previously, allowing the business to minimize production costs despite many of its brands creating watches by hand.

Margins below GPM have slipped across the decade, however, reflecting a failed effort to revitalize growth. S&A spending has increased from 29% of revenue to 39%, illustrating this. Although we think the marketing strategy itself is good, there are certainly questions to be asked about capital allocation and whether there are other things the company could try.

Balance sheet

Swatch is conservatively financed, using little-to-no debt. This gives the company flexibility to acquire new brands or fund expansion if required.

Distributions have been underwhelming, reflecting the poor financial performance. Despite poor financial performance, cash flow generation has been consistent and strong, allowing Management the capacity to increase distributions if they desired.

Peer analysis

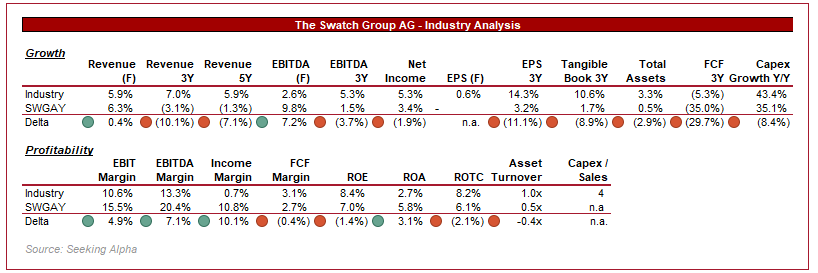

Apparel, Accessories and Luxury (Seeking Alpha)

{kind=link}

Presented above is a comparison of Swatch to the "Apparel, Accessories and Luxury Goods" industry as defined by Seeking Alpha.

Swatch's underwhelming growth is worsened when compared to the industry, as it suggests a fundamental issue with the business rather than a systemic issue.

As we have already established, Swatch's profitability is very good. Margins have slipped but they remain attractive on a relative and absolute basis.

Valuation

Valuation (Tikr Terminal)

Presented above, Swatch's valuation compared to its historical average trading range.

Swatch is trading at a discount to its historical average on almost every basis, implying negative market sentiment around the business.

Our view is that a discount is warranted given the continued weakness in growth and sliding margins. The degree looks overdone, however.

The company still owns some incredibly valuable brands and is generating strong FCF. With an equity value of CHF12bn and a market cap of CHF c.13bn, the company looks oversold.

Final thoughts

Swatch is an interesting case of why valuation matters. The company has a lot of issues, stemming from increased competition and reduced interest in some of its brands. That said, there is underlying quality. We like the brands, we like the strategy of shared competencies, and we like the absolute margins. Given the valuation, we believe the commercial weakness is more than priced in, representing an opportunity.

For further details see:

The Swatch Group: Undervalued Despite Issues