HTAB - The Worst Is Behind Us With Better Times Ahead

2023-12-27 01:01:00 ET

Summary

- The average annual returns for taxable and tax-exempt funds were negative 10.2% and negative 9.12%, respectively.

- With only three modest and widely expected rate hikes through the first half of the year, fixed income funds got off to a strong start with back-to-back quarters of gains.

- It is my opinion that if we stay higher for longer and recession is likely, investors will favour short-duration passive fixed income.

By Jack Fischer, Senior Research Analyst, Lipper

Are we finally coming to the end of interest rate hikes and what will today’s higher-for-longer mean for fixed income allocations?

Looking back, fixed income funds suffered their worst year on record during 2022. The average annual returns for taxable and tax-exempt funds were negative 10.2% and negative 9.12%, respectively. The historical pace at which the Federal Reserve increased interest rates choked the bond market dry and sent investors running for the sidelines as a record-breaking US$695.9 billion piled into money market funds since the start of the year.

With only three modest and widely expected rate hikes through the first half of the year, fixed income funds got off to a strong start with back-to-back quarters of gains. The party ended in the third quarter as yields jumped and longer-duration investments struggled – Treasury funds fell hardest, with Lipper General US Treasury Funds realising negative 6.40% on average.

The key to strong performance in 2023 in the bond markets was finding oneself in a floating-rate fund or one with short-end exposure – Lipper Loan Participation (+8.54%) and Short High Yield Funds (+4.94%) have reported the highest year-to-date returns through October month end.

To be inactive or not to be, that is the question

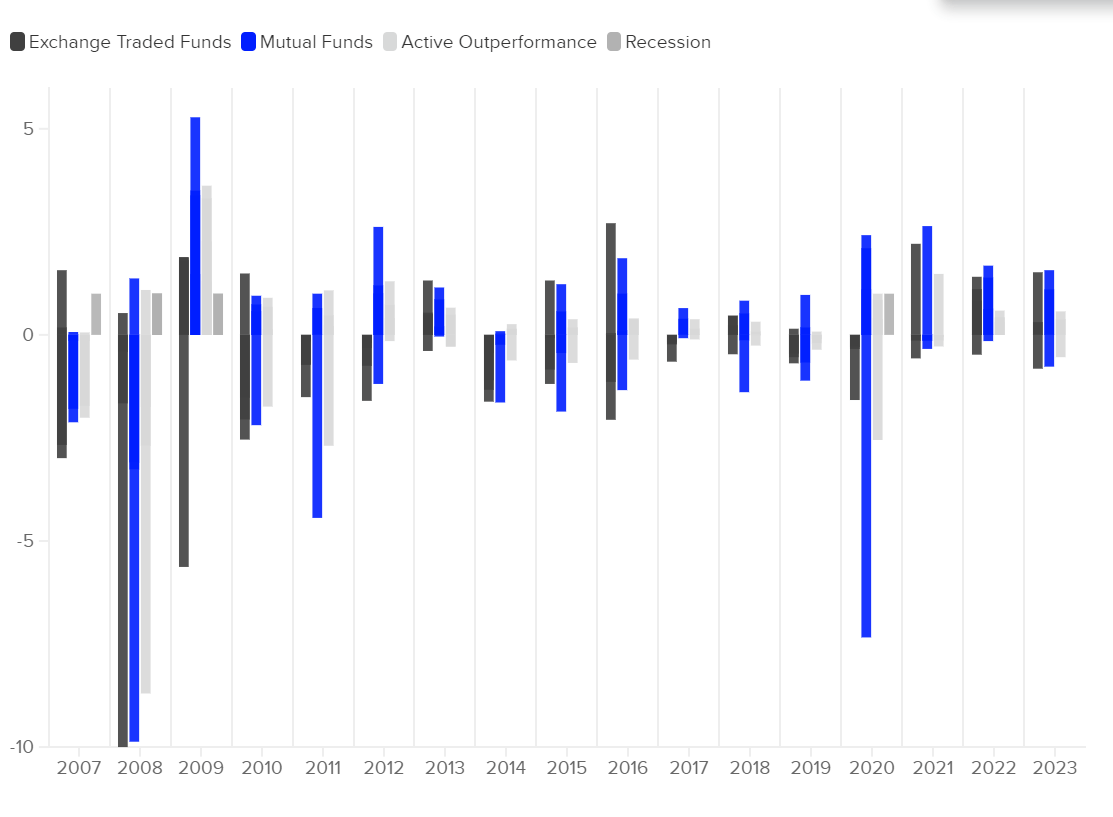

Although Q3 was a rough quarter for fixed income funds, actively managed funds outperformed their passive counterparts for the sixth quarter in seven. At year-end, actively managed fixed income funds had close to 8.0% in cash on average and as the year progressed, they saw that allocation drop to an average of 4.7% as of their most recent reporting date.

With their cash positions falling, the average duration of active funds increased with fixed income managers suddenly moving to own duration – for reference, passive funds have seen their cash and duration steady around 3.0% and 5.2%, respectively.

Exhibit 1: Actively managed fixed income fund outperformance

{kind=link}

We have seen tremendous volatility in fixed income markets, and what tends to beat beta during these times is actively managed investments.

While passive flows have been dominated by investors looking to take advantage of short-term Treasury yields and capital preservation, active inflows this year have been into Lipper classifications that allow portfolio managers more leeway to manage their funds.

The top three in year-to-date inflows are Core Bond Funds (+US$48.1 billion), Multi-Sector Income Funds (+US$17.5 billion) and Core Plus Bond Funds (+US$16.8 billion). These three classifications have average durations of 6.11, 4.29 and 6.14 years, respectively, with Multi-Sector Income Funds increasing their duration by 32 basis points (bps) since the start of the year.

Exhibit 2: Top 5 inflows/outflows year-to-date by Lipper classification

{kind=link}

Ongoing inflation risk

The risk in that lies in long interest rates is our old nemesis, inflation. If the market believes inflation has been subdued and a soft landing is likely, then we will continue to see these three classifications lead in active net flows throughout the start of next year.

Is it possible the effects of rates have not yet been fully realised? Student loan payments have just begun, the commercial real estate market is struggling, credit card balances are soaring, and geopolitical tensions remain high. If we see short-term rates stabilise and market uncertainty continue to grow with fear of oncoming recession, short-duration, floating-rate and Treasury funds may will be the focus for investors.

Year to date, we have seen 62 newly launched actively managed funds, with 21 coming in Q3 - most falling under either securitised debt or floating-rate funds.

With market uncertainty comes market opportunities – but will the opportunities be long- or short-dated?

It is my opinion that if we stay higher for longer and recession is likely, investors will favour short-duration passive fixed income. If inflation is indeed handled and a soft landing becomes the prevalent outlook, longer interest rates may fall faster than anticipated, leading to actively managed intermediate to long fixed income funds reigning in 2024.

Legal Disclaimer

Republication or redistribution of LSE Group content is prohibited without our prior written consent.

The content of this publication is for informational purposes only and has no legal effect, does not form part of any contract, does not, and does not seek to constitute advice of any nature and no reliance should be placed upon statements contained herein. Whilst reasonable efforts have been taken to ensure that the contents of this publication are accurate and reliable, LSE Group does not guarantee that this document is free from errors or omissions; therefore, you may not rely upon the content of this document under any circumstances and you should seek your own independent legal, investment, tax and other advice. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon.

Copyright © 2023 London Stock Exchange Group. All rights reserved.

The content of this publication is provided by London Stock Exchange Group plc, its applicable group undertakings and/or its affiliates or licensors (the “LSE Group” or “We”) exclusively.

Neither We nor our affiliates guarantee the accuracy of or endorse the views or opinions given by any third party content provider, advertiser, sponsor or other user. We may link to, reference, or promote websites, applications and/or services from third parties. You agree that We are not responsible for, and do not control, such non-LSE Group websites, applications or services.

The content of this publication is for informational purposes only. All information and data contained in this publication is obtained by LSE Group from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data are provided "as is" without warranty of any kind. You understand and agree that this publication does not, and does not seek to, constitute advice of any nature. You may not rely upon the content of this document under any circumstances and should seek your own independent legal, tax or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the publication and its content is at your sole risk.

To the fullest extent permitted by applicable law, LSE Group, expressly disclaims any representation or warranties, express or implied, including, without limitation, any representations or warranties of performance, merchantability, fitness for a particular purpose, accuracy, completeness, reliability and non-infringement. LSE Group, its subsidiaries, its affiliates and their respective shareholders, directors, officers employees, agents, advertisers, content providers and licensors (collectively referred to as the “LSE Group Parties”) disclaim all responsibility for any loss, liability or damage of any kind resulting from or related to access, use or the unavailability of the publication (or any part of it); and none of the LSE Group Parties will be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, howsoever arising, even if any member of the LSE Group Parties are advised in advance of the possibility of such damages or could have foreseen any such damages arising or resulting from the use of, or inability to use, the information contained in the publication. For the avoidance of doubt, the LSE Group Parties shall have no liability for any losses, claims, demands, actions, proceedings, damages, costs or expenses arising out of, or in any way connected with, the information contained in this document.

LSE Group is the owner of various intellectual property rights ("IPR”), including but not limited to, numerous trademarks that are used to identify, advertise, and promote LSE Group products, services and activities. Nothing contained herein should be construed as granting any licence or right to use any of the trademarks or any other LSE Group IPR for any purpose whatsoever without the written permission or applicable licence terms.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

The Worst Is Behind Us, With Better Times Ahead