THR - Thermon Group: Growth Through Future Operational Excellence Combined With Improved Cash Flows

2023-09-21 09:32:21 ET

Summary

- Thermon Group focuses on optimizing manufacturing processes and enhancing productivity while keeping operational costs in check.

- They implemented and will continue to improve manufacturing principles, automation technologies, and data analytics to reduce lead times, minimize waste, and improve product quality.

- Thermon's balance sheet is solid and has improved since my previous article.

- Assuming my DCF figures, Thermon is fairly valued, resulting in a buy rating.

Since my previous article, Thermon (THR) has performed rather well, resulting in the need for reevaluation due to the valuation being potentially concerning. Although the share price has continued to rise, I believe that my maintenance of a buy rating for Thermon would be prudent as the firm's solid balance sheet, strong performance, future operational excellence and fair valuation will allow for continued returns in the medium term.

Business Overview

For various process sectors, Thermon Group Holdings, Inc. provides customized heating solutions on a global scale. They offer a variety of controls, monitoring systems, and heat tracing technologies. They provide under prestigious trademarks like Ruffneck and Caloritech and are well known for their environmental heating solutions. Additionally, the business offers heating equipment for transportation, filtration goods, and rail and transit solutions. They have a wide network of sales representatives and distributors, serving industries such as semiconductors, medicines, renewable energy, and more.

Thermon

Previous Article

In my last article , I rated Thermon as a buy indicating its undervaluation and acquisition strategy providing long-term value to shareholders. The stock has now returned 8.52% compared to the S&P's -0.04% demonstrating the firm's recent outperformance due to recent strong earnings. In this article, I will demonstrate why Thermon still remains a buy even though fundamentals declined slightly due to positive price action.

Performance Compared to the Broader Market

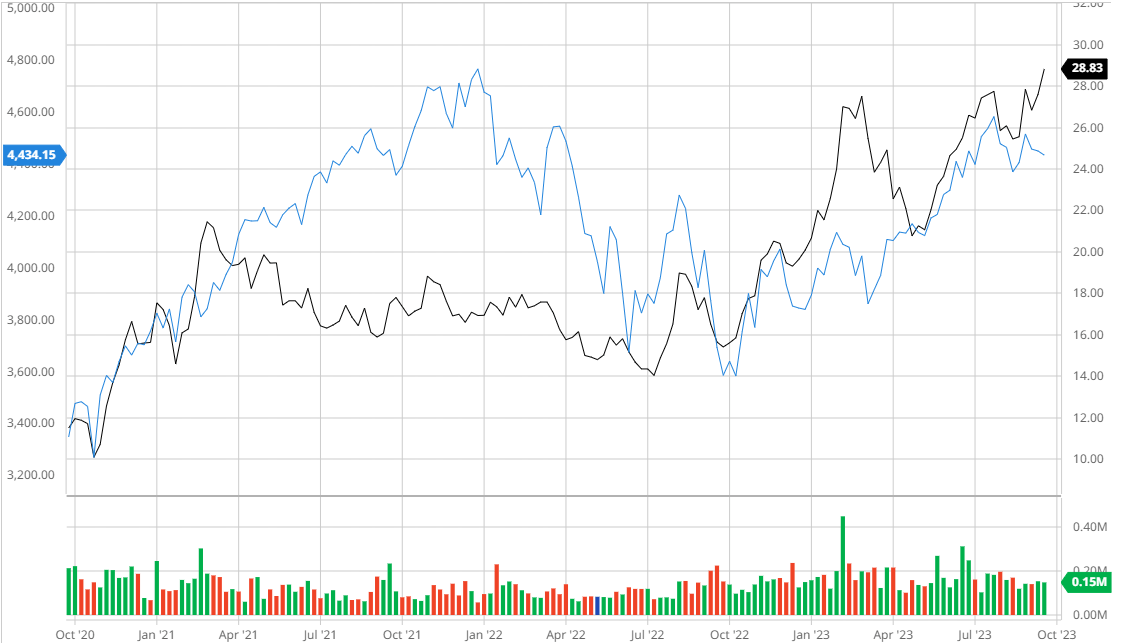

Over the past 3 years, Thermon has outperformed the broader market, demonstrating its ability to not only succeed in the short term since my previous article but also on a multi-year basis.

Thermon Compared to the Broader Market 3Y (Created by author using Bar Charts)

{kind=link}

Financials

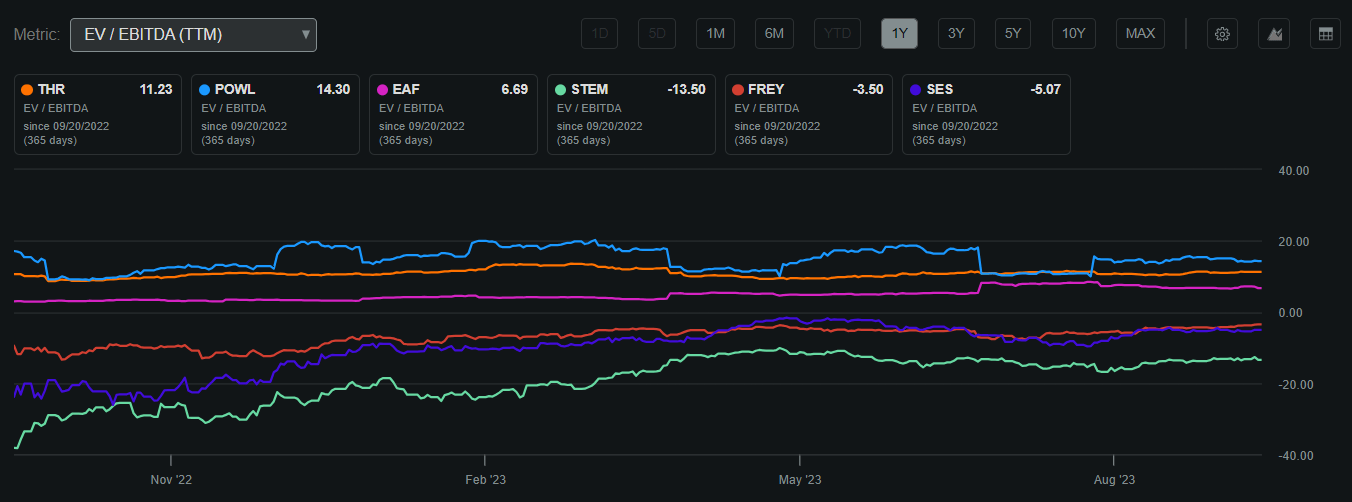

Thermon's current market capitalization stands at $926.74 million, and it maintains a respectable Return on Invested Capital of 8%. The stock is presently trading at $28.78 per share, slightly below its 52-week high of $29.17. An interesting point to note is the company's EV/EBITDA ratio, which is at 11.23. While slightly elevated, it outperforms most of its peer companies, showcasing its relative strength in the market.

Thermon EV/EBITDA Compared to Peers (Seeking Alpha)

{kind=link}

While Thermon currently does not distribute dividends, its 8% ROIC and recent growth trajectory underline the company's sound core operational strategy aimed at enhancing long-term shareholder value. If growth slows down in the future due to scalability challenges, the firm might consider issuing dividends. However, leveraging free cash flow to drive growth by outperforming competitors has proven to be a potent strategy for achieving robust growth, as evidenced by the firm's performance in the past year.

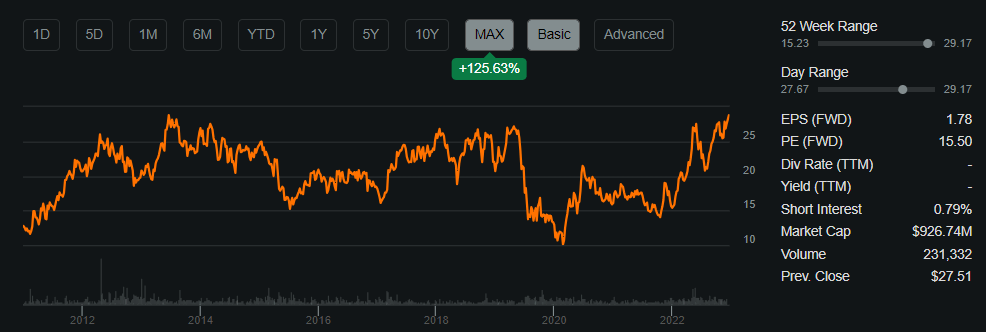

Share Performance (Seeking Alpha)

{kind=link}

Earnings

In fiscal Q1 2024, Thermon exceeded expectations on both the top and bottom lines. The EPS surpassed estimates by $0.11, reaching $0.4, and the revenues exceeded predictions by $7.17 million, totaling $106.89 million, showcasing an impressive 11.99% YoY growth. These consistent and strong results highlight Thermon's resilience in the face of prevailing macroeconomic challenges. The sustained demand and a robust backlog of $475 million signify a promising outlook for the company's long-term cash flows. This financial strength not only positions Thermon for ongoing outperformance but also allows for strategic leveraging compared to its industry counterparts without risking solvency. With earnings estimates also being upgraded since my previous article, we must maintain a close eye on CPI along with the Fed's rate decisions such as today's recent maintenance at current levels.

Earnings Estimate (Seeking Alpha) Thermon Compared to the S&P 500 3Y (Created by author using Bar Charts)

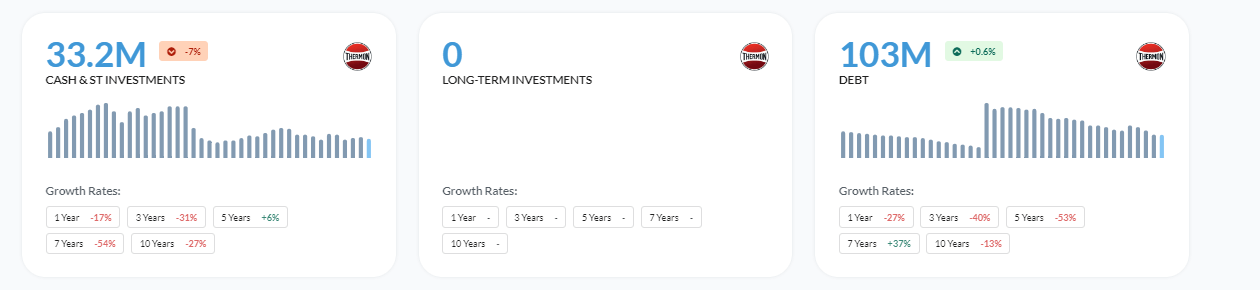

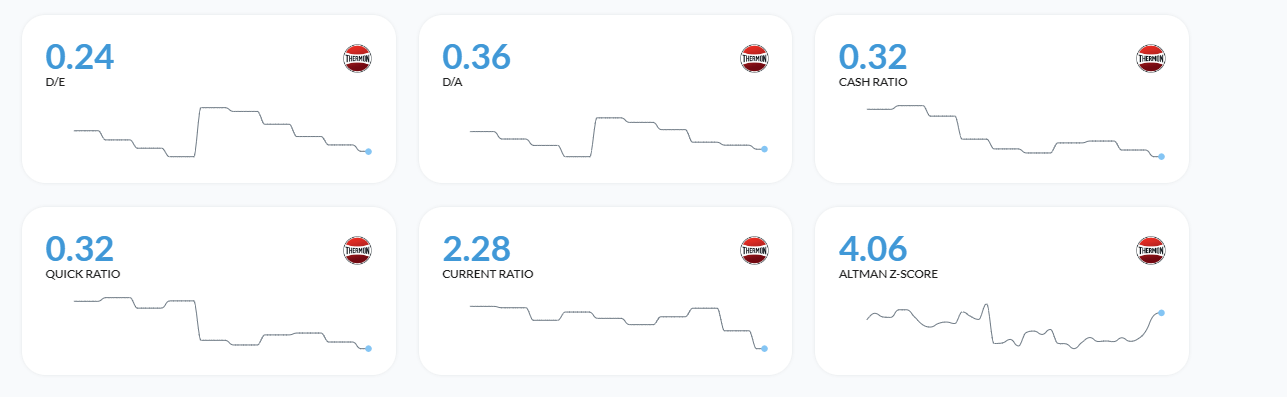

Balance Sheet

Thermon has made significant enhancements to its financial position concerning debt and solvency. The improvement in operating income is evident in Thermon's interest coverage, which has now strengthened to 11.84. This showcases the company's capacity to leverage effectively, even in high-rate environments, benefiting from its unleveraged balance sheet. Additionally, the current ratio of 2.28 and Altman-Z-Score of 4.06 provide a strong indication of the firm's ability to maintain solvency in the medium term.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

{kind=link}

{kind=link}

{kind=link}

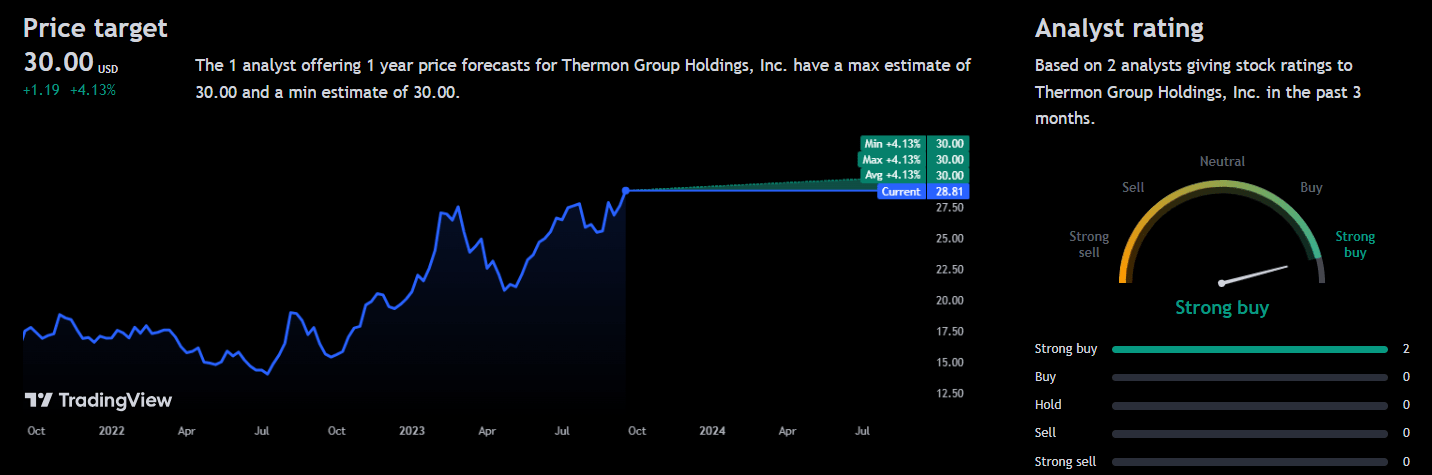

Analyst Consensus

Analysts have also maintained its current rating of "Strong Buy" on Thermon with a sustained price target of $30.00. I believe that although the potential upside is only 4.2%, analysts have demonstrated that the firm's long-term ability to scale is rather promising, which allows me to conclude that these price targets may be raised in the near future.

Analyst Consensus (Trading View)

{kind=link}

Valuation

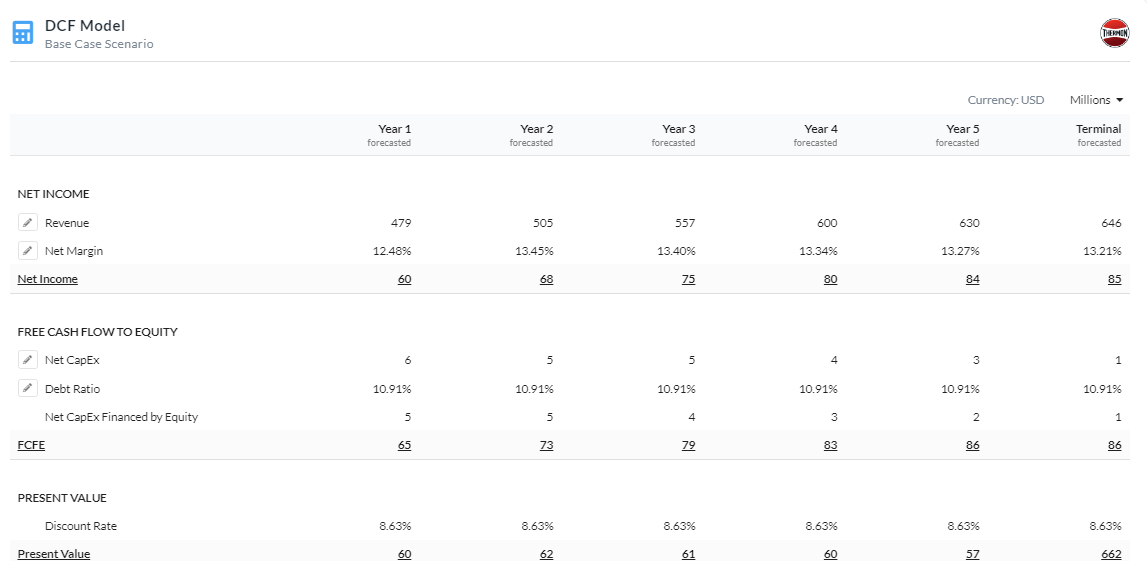

In determining an accurate fair value for Thermon, establishing an appropriate discount rate that encompasses the Cost of Equity and cost of capital is crucial. Initially, I derived a risk-free rate of 4.36%, based on the 10-year treasury yield , to compute the Cost of Equity. Consequently, this led to a Cost of Equity of 8.63%, which is higher than my previous estimation. This adjustment is due to the recent increase in rates and, consequently, bond yields.

Cost of Equity (Created by author using Alpha Spread)

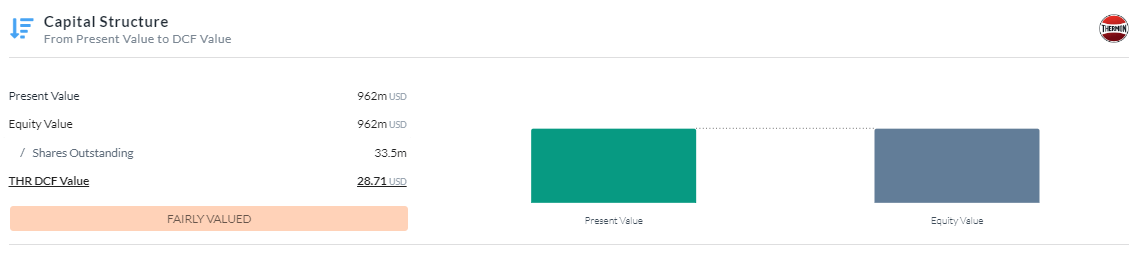

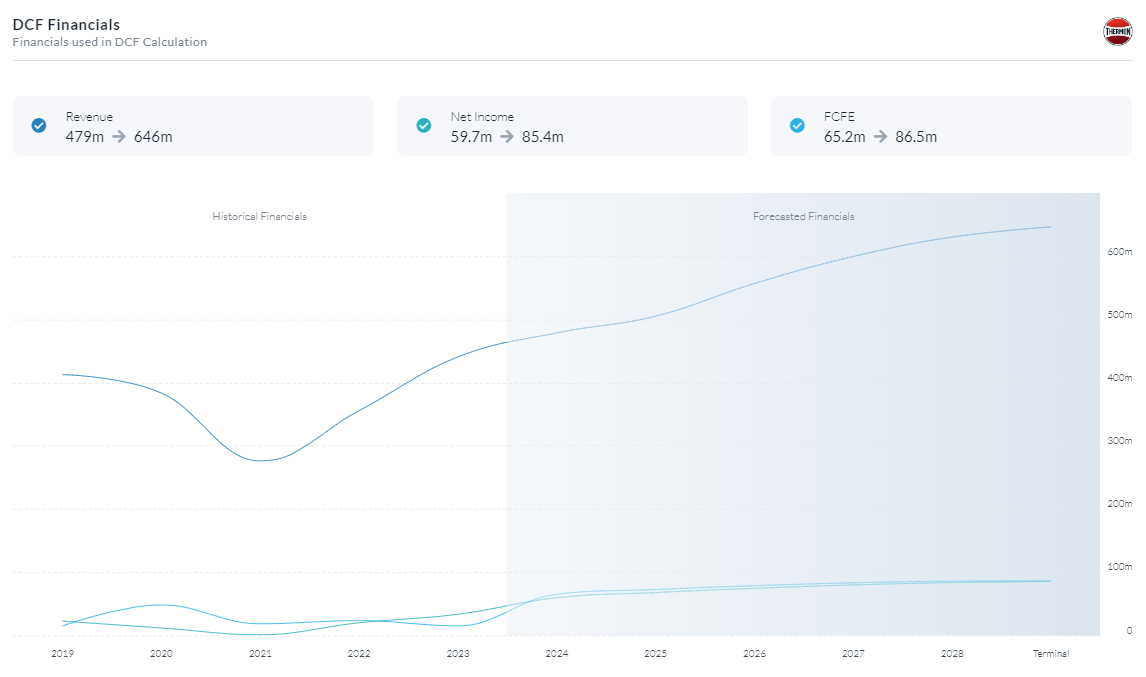

Now equipped with a suitable discount rate, I applied a 5-year Equity Model DCF utilizing FCFE. Enhancements were made to my revenue growth and margin expansion estimates to align with the latest analyst expectations. This was coupled with a discount rate of 8.63%, devoid of any risk premium owing to the substantial backlog, and a balanced sheet devoid of excessive leverage, acting as a hedge against potential macroeconomic challenges. This resulted in a fair value of $28.71 indicating the equity is fairly valued as of now.

5 Year Equity Model DCF Using FCFE (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

{kind=link}

{kind=link}

{kind=link}

Thermon's Operational Excellence Will Propel Growth Further

Thermon Group's emphasis on streamlining operations and increasing productivity while controlling expenses serves as an example of their commitment to operational excellence and cost-efficiency. They were able to drastically cut lead times and waste by carefully examining their manufacturing processes, finding bottlenecks, and optimizing operations. They optimized production schedules through the effective use of space and resources, which eventually reduced inventory holding costs and improved responsiveness to client demand. This illustrates the company's efficient use of FCF, which is only going to increase now that net income is higher.

Thermon also adopted automation technology to improve the productivity of their production lines. Automation sped up production, increased accuracy, decreased errors, and resulted in higher-quality goods while containing labor and operational costs. By incorporating data analytics into their operations, they were able to predict maintenance needs and cut downtime by monitoring equipment performance in real time. This proactive approach to maintenance provided uninterrupted production while also reducing costs.

I believe that these methods of improving profitability and efficiency will not only produce more cash flows and improve future investment ability, but it will also allow the firm to outperform competitors through price competition if needed enabling Thermon to take on more leverage and margin decline if price competition were to occur allowing for future market share to look positive.

Risks

Market Demand Volatility: Different industries affect the demand for Thermon's products, and abrupt changes in that demand can have an impact on sales and revenue.

Raw Material Costs: Price changes for raw materials, particularly petrochemicals and electrical components, can have an impact on manufacturing costs and profit margins.

Conclusion

To summarize, I believe that my maintenance of a buy rating for Thermon would be prudent as the firm's solid balance sheet, strong performance, future operational excellence and fair valuation will allow for continued returns in the medium term.

For further details see:

Thermon Group: Growth Through Future Operational Excellence Combined With Improved Cash Flows