GLV - These 7 High-Yield CEFs Reduced Distributions In 2024 Consider Buying Anyway

2024-01-18 10:43:45 ET

Summary

- abrdn, a UK-based fund manager, has been aggressively acquiring and merging closed-end funds aka CEFs from other managers to expand its offerings.

- CEFs have advantages over traditional dividend-paying stocks and offer a wide range of asset types and classes.

- The article reviews seven CEFs that have adjusted their annual distributions downward but still offer monthly payouts exceeding 10%.

For income investors who wish to generate passive income in retirement, or who simply want to support a lavish lifestyle, one option to consider includes CEFs, or closed-end funds. There are multiple advantages to CEFs over more traditional dividend paying stocks such as business development companies ((BDCs)), master limited partnerships ((MLPs)), or real estate investment trusts ((REITs)). The fund manager based in the UK who call themselves abrdn (with lower case "a") offers a wide range of CEFs and have been aggressively expanding by acquiring and merging funds from other fund managers.

Some of those acquired funds include the Tekla healthcare funds - HQH, HQL, THW, THQ, and others such as Macquarie/First Trust Global Infrastructure/Utilities Dividend & Income Fund (MFD), which is being merged into ASGI, and First Trust Specialty Finance and Financial Opportunities Fund (FGB), which is being merged with AOD. Two other funds from First Trust - FSD and FAM, are being merged with ACP as explained in this press release .

One reason why abrdn has been so aggressively acquiring and merging funds from other managers with their own existing funds is because no new CEFs have gone public since October 2022, as I explain here . Instead, fund sponsors such as abrdn and Carlyle are acquiring and/or merging old funds into "new" CEFs without going through an IPO. For example, Carlyle took over the fund with the former ticker symbol VCIF to create a new CLO fund, CCIF as I explain here .

Why do income investors like CEFs?

There are multiple advantages to the CEF model, which differs from an ETF (exchange-traded fund) in several key aspects. Some of those advantages are well explained in this brief article from abrdn. One of the keys to buying CEFs is to buy them when they trade at a wider than average discount (or lower than average premium) to NAV, as my colleague Steven Bavaria explains in his article . There is even an ETF that holds CEFs that is managed by activist investor Saba Capital, Saba Closed-End Funds ETF ( CEFS ), if you prefer investing in an ETF for whatever reason.

Nuveen is one of the largest fund sponsors for CEFs and if you are interested in learning more, go to their website , or take a look at CEFConnect.com , which is managed by Nuveen and is used to share data about all the CEFs that are publicly listed in the U.S.

There are CEFs that hold different asset types and classes ranging from equities to credit, fixed income, global hybrid, municipal, healthcare, utilities, and just about anything else that you can imagine. A CEF is simply a vehicle for holding investments, and some are even a "fund of funds" such as SPE (which holds other CEFS, BDCs, stocks, etc.), which I discussed in my previous article on five CEFs that raised the distribution in January. Many income CEFs use a managed or level distribution policy, which involves adjusting the monthly distribution once per year in January and then paying that same distribution for the next 12 months. This article will review 7 funds that adjusted the annual distribution downward, yet still yield a monthly payout that exceeds 10% annually and in some cases much more.

The Not so Magnificent, but High-Yielding Seven

The seven CEFs that I will review in this installment include:

Two of the Clough Global fund trio:

- Clough Global Dividend and Income Fund ( GLV )

- Clough Global Equity Fund ( GLQ ) * increased in January

- Clough Global Opportunities Fund ( GLO )

The Cornerstone funds:

Two of the 3 RiverNorth funds:

- RiverNorth/DoubleLine Strategic Opp Fund ( OPP )

- RiverNorth Opportunities Fund ( RIV ) * increased in January

- RiverNorth Capital and Income Fund ( RSF )

And O FS Credit Company, Inc. ( OCCI ).

Before I get into the details, I would like to preface this review by stating that I own shares in 4 of the 7 funds - CLM, CRF, OPP, OCCI - that I am covering in this article.

The Clough Global funds

The trio of CEFs offered by Clough include GLO, GLQ, and GLV. The fund manager is Clough Capital Partners, founded by Chuck Clough after he left Merrill Lynch in 1999.

{kind=link}

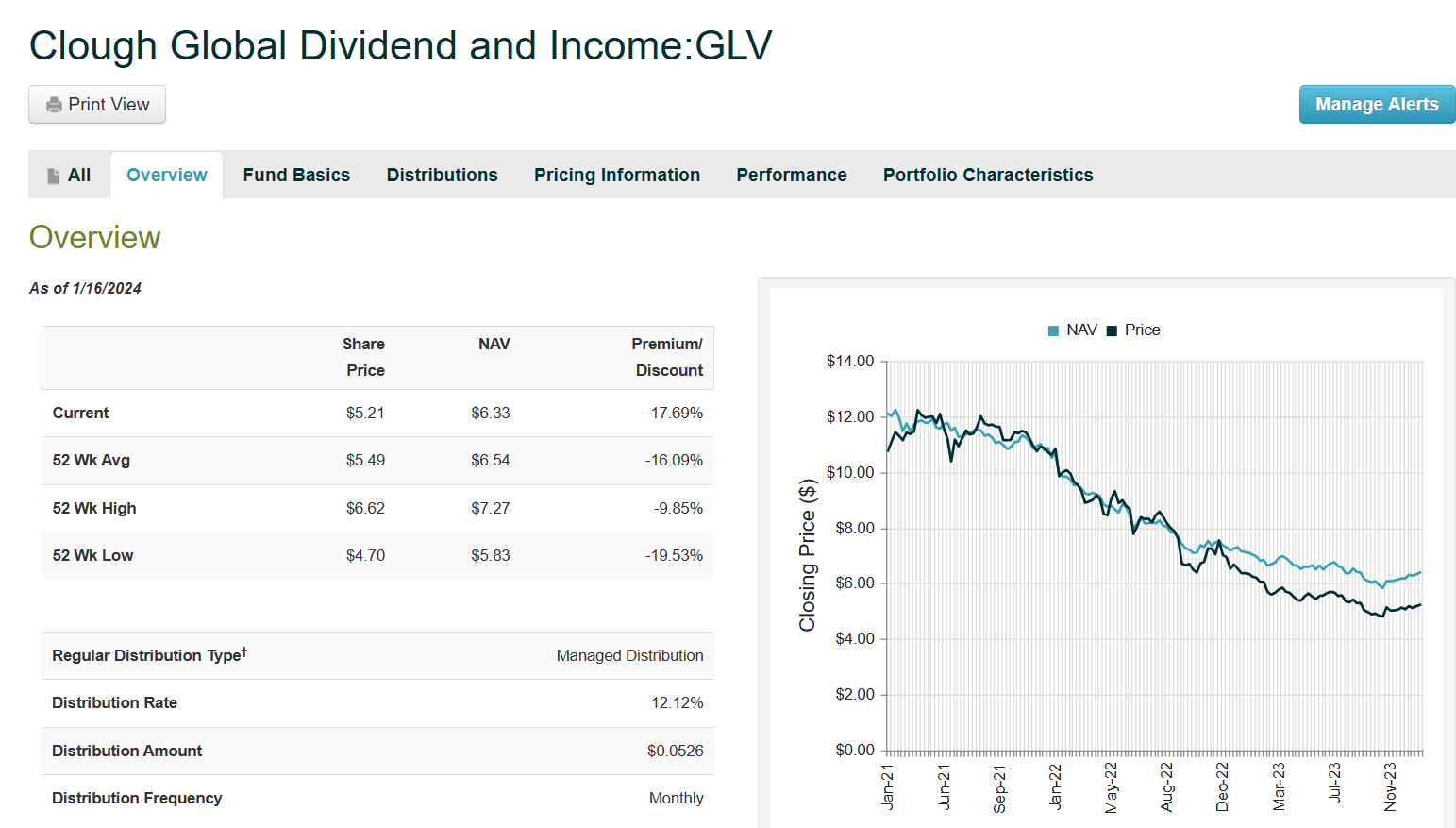

Clough Global Dividend and Income Fund - GLV

The GLV fund experienced mixed performance over the past 10 years (as have the other Clough funds), as seen in this screenshot from the fund website , and 2022 was an exceptionally rough year for the fund, losing -31%.

{kind=link}

Over the past 3 years, the discount has widened considerably from the slight premium that the fund traded at in 2021, as shown in this screenshot from CEFConnect.

{kind=link}

The fund NAV appears to be turning the corner in 2024 and as the fund recovers from its 3-year funk it may be worth considering now for the 12% yield while it trades at a discount greater than -17%. The monthly distribution was decreased in January from $.0597 to $.0526.

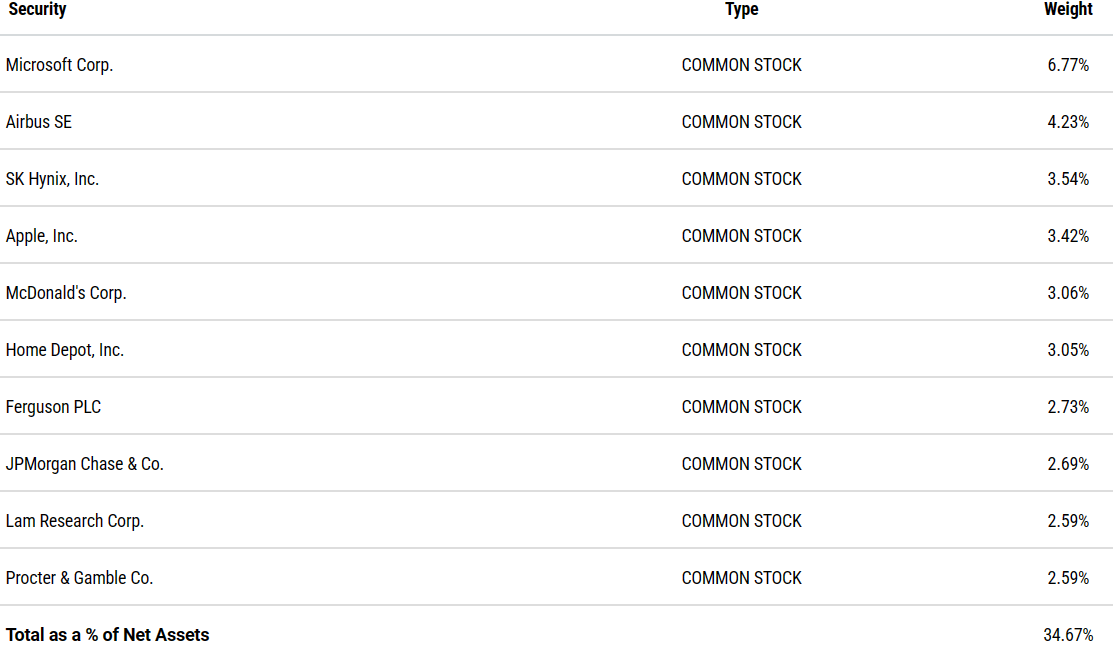

The top 10 holdings in GLV (as of 11/30/23) include many familiar large-cap names:

{kind=link}

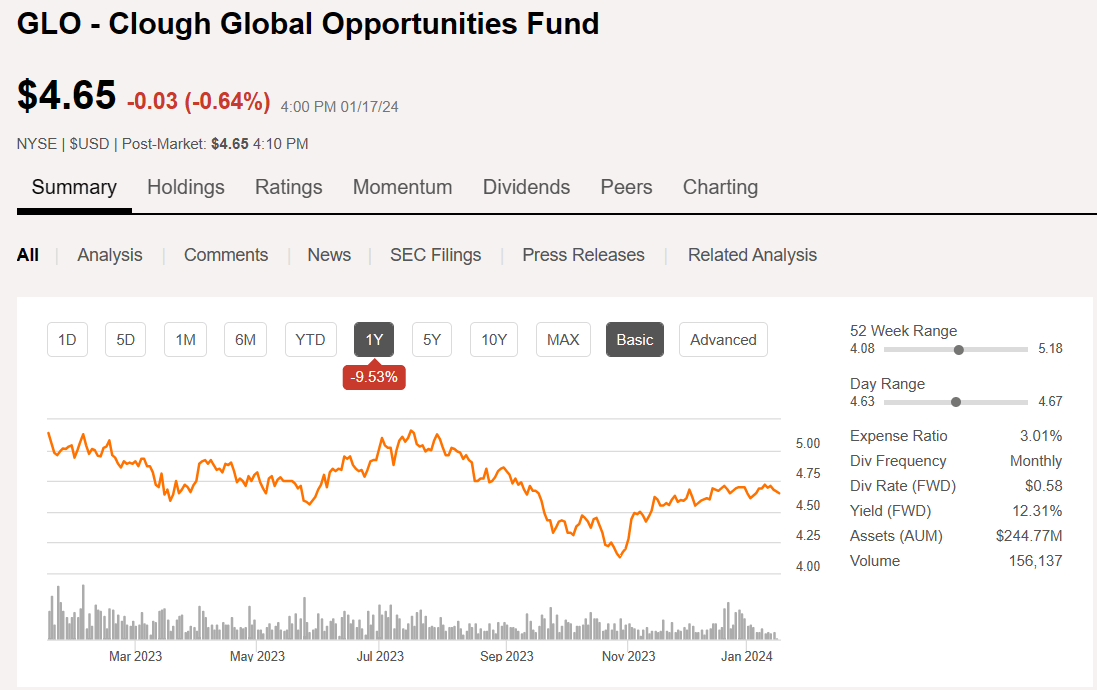

Clough Global Opportunities Fund - GLO

Like its sibling fund, GLV, the GLO fund slightly decreased the monthly distribution in January from $.0483 to $.0480. GLO yields just over 12% and is trading at a discount of about -18% to NAV as of 1/17/24. The GLO fund is a bit larger with about $245M in AUM compared to about $80M for GLV.

{kind=link}

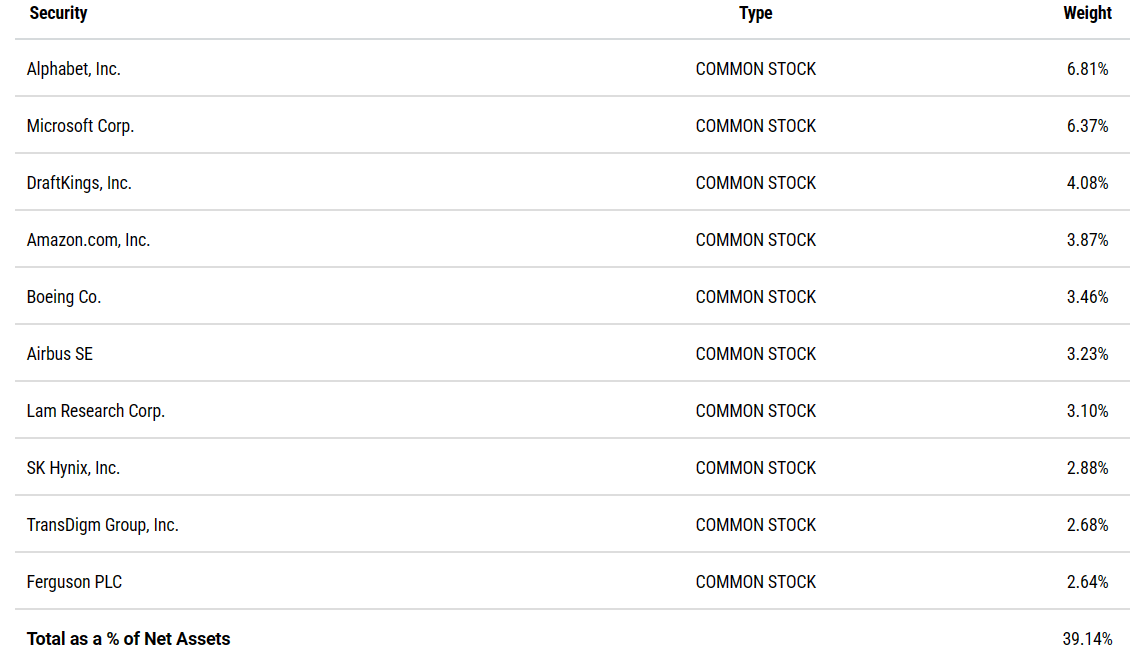

The top 10 holdings in GLO (as of 11/30/23) include some overlap along with more of the Magnificent Seven stocks (e.g., Alphabet and Amazon) as compared to GLV.

{kind=link}

The Clough funds are all equity based CEFs that generate most of their returns from capital gains using leverage and also tend to have a large amount of ROC, which is appealing to some investors who hold the CEFs in a taxable account.

Cornerstone Funds

Like the Clough funds, the two Cornerstone funds, CLM and CRF, are taxable equity funds that offer a high yield distribution and hold mostly large cap, top performing stocks including most or all of the Magnificent Seven. For the most part, the two funds are very similar in terms of the holdings, the distribution amounts, the discounted DRIP policy (you can reinvest shares at NAV which is typically a substantial discount to market price), and the use of rights offerings to increase the share count and grow the NAV when those new shares are issued at a substantial premium.

The differences between the two include the fact that CLM is much larger with about $1.5B in AUM while CRF holds about $680M. Also, CRF has been trading for a higher premium than CLM recently, even though the NAV is nearly $.30 less than CLM's NAV. They track fairly closely in terms of total return although CRF has been the better performer over the past 6 months.

{kind=link}

Currently, CLM trades at a premium of about 5% and after reducing the monthly distribution in January from $.1228 to $.1086 it now offers a distribution yield of just over 18%. Likewise, CRF reduced the distribution in January from $.1173 to $.1037 which works out to an annual yield of about 17.7% while trading at a premium of just over 9%.

Both funds utilize a managed distribution policy that is based on 21% of the NAV as of the last day of October as explained in this press release announcing the 2024 distribution amounts. Once that amount is set it is typically maintained for the entire year even if it means using ROC to cover part of the distribution.

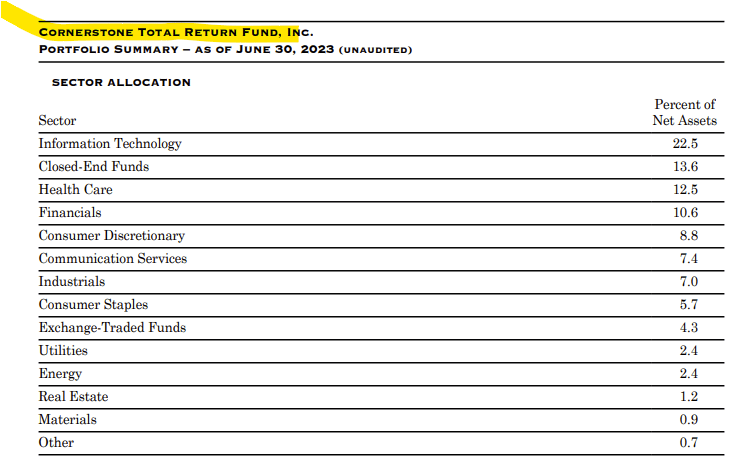

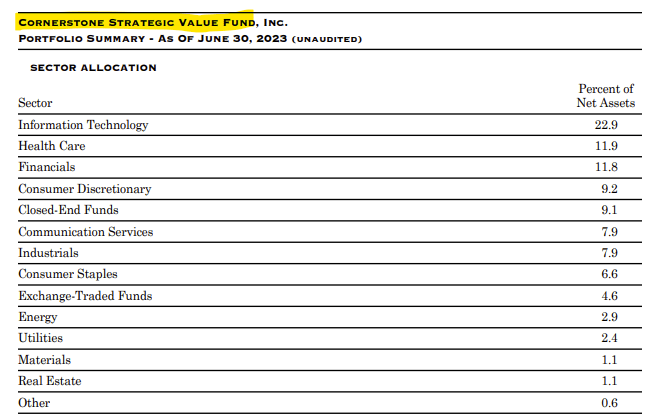

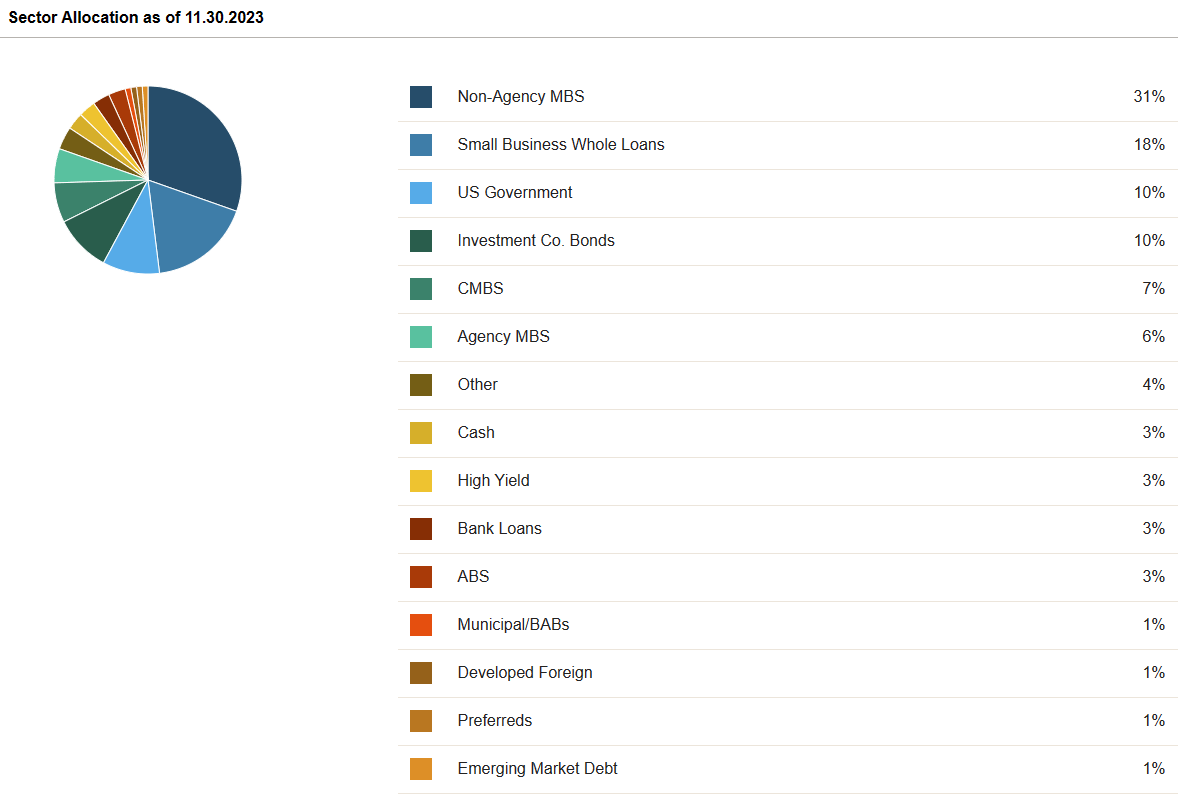

The holdings in both funds are well diversified with a concentration of about 22% in Tech stocks (including the Mag 7) followed by roughly 12% each in Healthcare, Financials, and other CEFs.

{kind=link}

{kind=link}

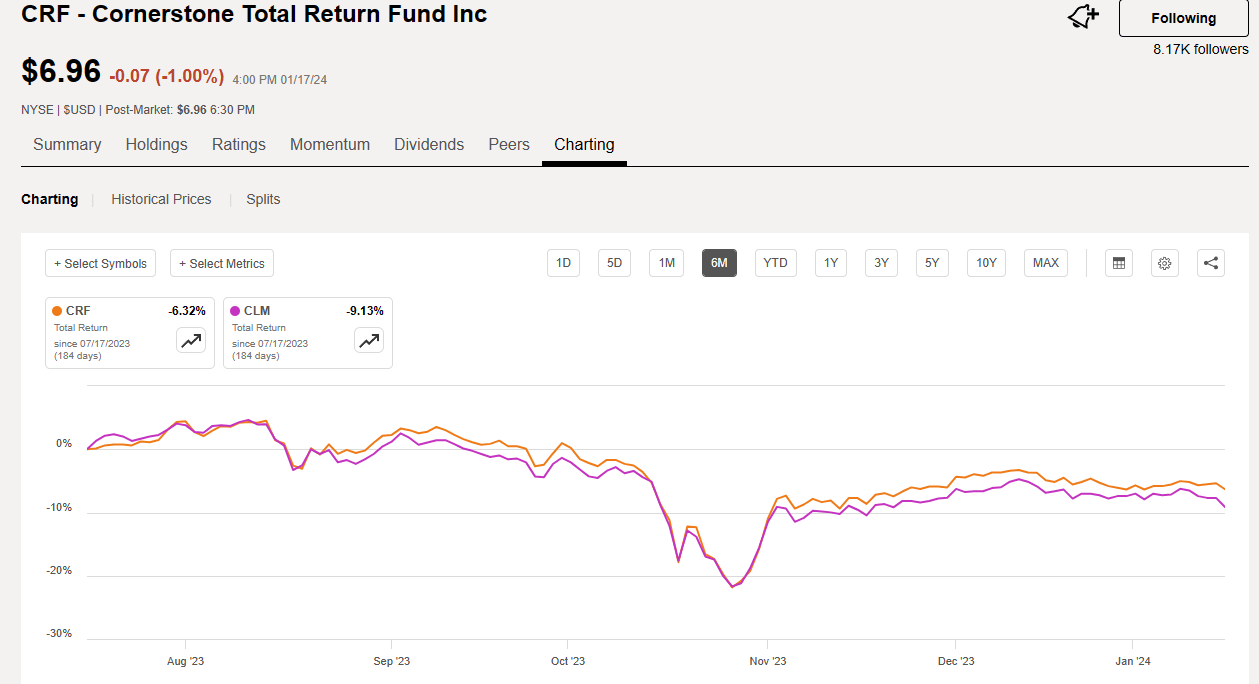

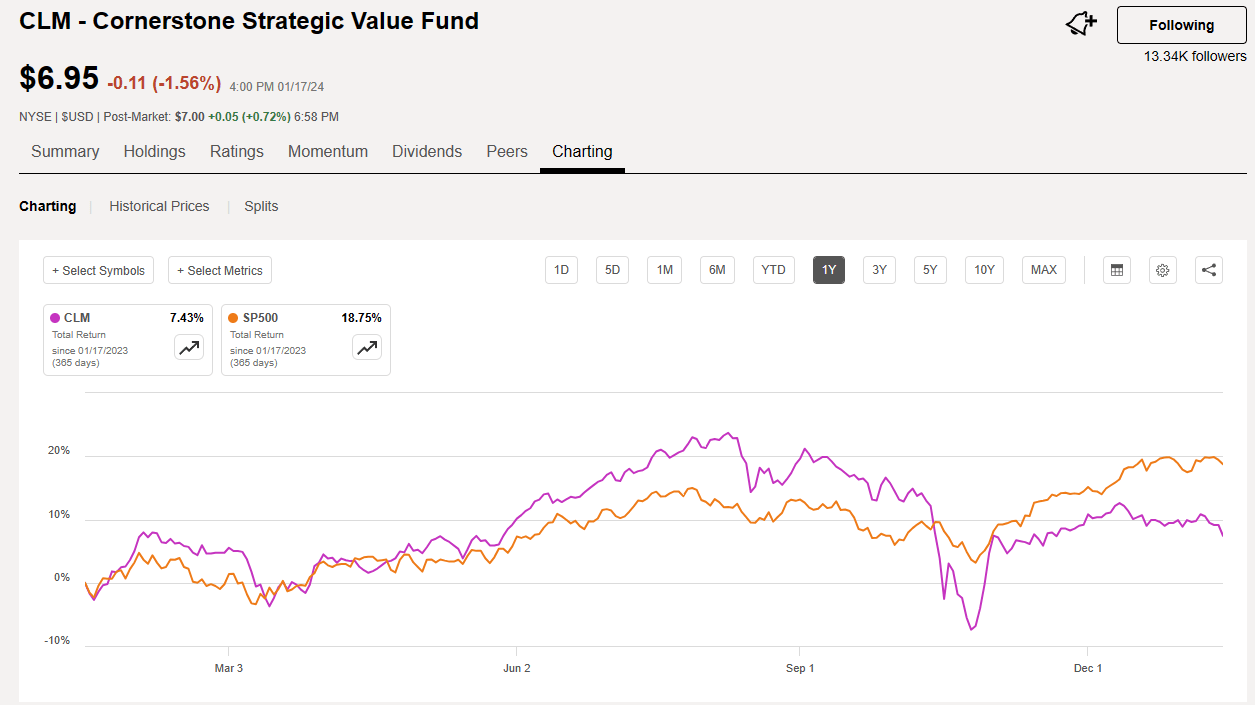

Both funds offer a fairly reliable monthly income distribution that can be counted on to remain steady for the whole year, even as the NAV goes up and down along with the broader market. Although due to leverage employed by the funds, the up and down NAV movements are accentuated as can be seen in this chart comparing the total return of CLM as compared to the S&P 500 over the past one year. This makes the Cornerstone funds solid income investments, but they are not "buy and forget" funds.

{kind=link}

The Cornerstone funds are not suitable for all investors so please consider your own risk tolerance and investment objectives before deciding whether to invest in CRF or CLM. I hold long positions in both funds in my Income Compounder portfolio and they currently make up nearly 10% of my total holdings by market value.

RiverNorth Funds

The funds from Clough and Cornerstone are not the only ones that offer high yield income using a managed or level distribution policy. There are 3 taxable CEFs: RIV, OPP, and RSF, from RiverNorth that also use a level distribution policy and two of those (OPP, RSF) just reduced the distribution in January. This is how RiverNorth describes their distribution policy:

Each Fund maintains a level distribution policy with the intention of providing monthly distributions to shareholders at a constant and fixed (but not guaranteed) rate that is reset annually. Although there can be no guarantee that the distribution policy will be successful in its goals, shareholders may potentially benefit from both increased liquidity and flexibility in managing their Fund investments. Each Fund's ability to maintain a stable level of distributions to shareholders will depend on a number of factors, including changes in the financial market, market interest rates, and performance of overall equity and fixed income markets. As portfolio and market conditions change, the ability of each Fund to continue to make distributions in accordance with the level distribution policy may be affected.

Also, the RiverNorth funds do offer a discount to reinvest shares rather than taking the distribution as cash. The fund DRIP policy is explained in detail in the fund's Annual Report (see page 45), but essentially the fund will reinvest shares at either the NAV or the market price, whichever is cheaper at the time of reinvestment.

The OPP fund reduced the 2024 distribution in January from $.1021 per month to $.1003. The forward annual yield based on the new distribution is about 14.5% and OPP currently trades at a discount to NAV of more than -12%.

RSF also decreased the 2024 distribution in January, from $.1424 monthly to $.1398. At the current market price of $15.85, RSF offers an annual yield of about 10.5% based on the new distribution and currently trades at a discount of about -5.5%.

I do currently own shares of OPP in my Income Compounder portfolio and may add more while it trades at such a substantial discount and pays a steady high yield monthly distribution. I feel that the fund holdings will benefit from any reductions in interest rates that are expected to occur later this year.

{kind=link}

OFS Credit Company, Inc.

The final CEF that I wanted to review in this segment of reducers in 2024 is a little bit unusual in the way that it manages the fund distributions. OCCI does not employ a managed distribution policy, but the fund does offer a regular, monthly distribution that was reduced back in December. Previously, OCCI paid a quarterly distribution of $.55 per share but with a maximum of 20% of that distribution paid in cash and the remainder in reinvested shares.

The fund changed its distribution policy to now pay $.10 monthly, which appears to be a reduction ($.30 per quarter compared to $.55) except that they removed the maximum cash requirement and offered a discount to reinvest shares instead. For investors who wish to take the distribution as cash and choose for themselves where to reinvest that cash each month, the new distribution policy actually represents an increase (from approximately $.11 quarterly in cash to $.30). Some view the new policy as a better option and I agree.

OCCI DRIP Discount

The number of shares to be issued to a holder of common stock is determined by dividing the total dollar amount of the distribution payable to such holder of common stock by ninety-five percent (95%) of the market price per share of common stock at the close of regular trading on the Nasdaq Capital Market on the valuation date fixed by the Board for such distribution.

With the new monthly distribution and at the current market price of about $7, OCCI now offers a distribution yield of more than 17% and currently trades at a substantial discount to NAV, which was recently estimated to be between $7.61 and $7.71 as of the end of December.

According to the fund website , most of the fund holdings include CLOs (collateralized loan obligations):

OFS Credit Company is a non-diversified, publicly traded, closed-end management company that is registered under the Investment Company Act of 1940. Its objective is to generate current income, with a secondary objective of generating capital appreciation primarily through investment in collateralized loan obligation equity and debt securities.

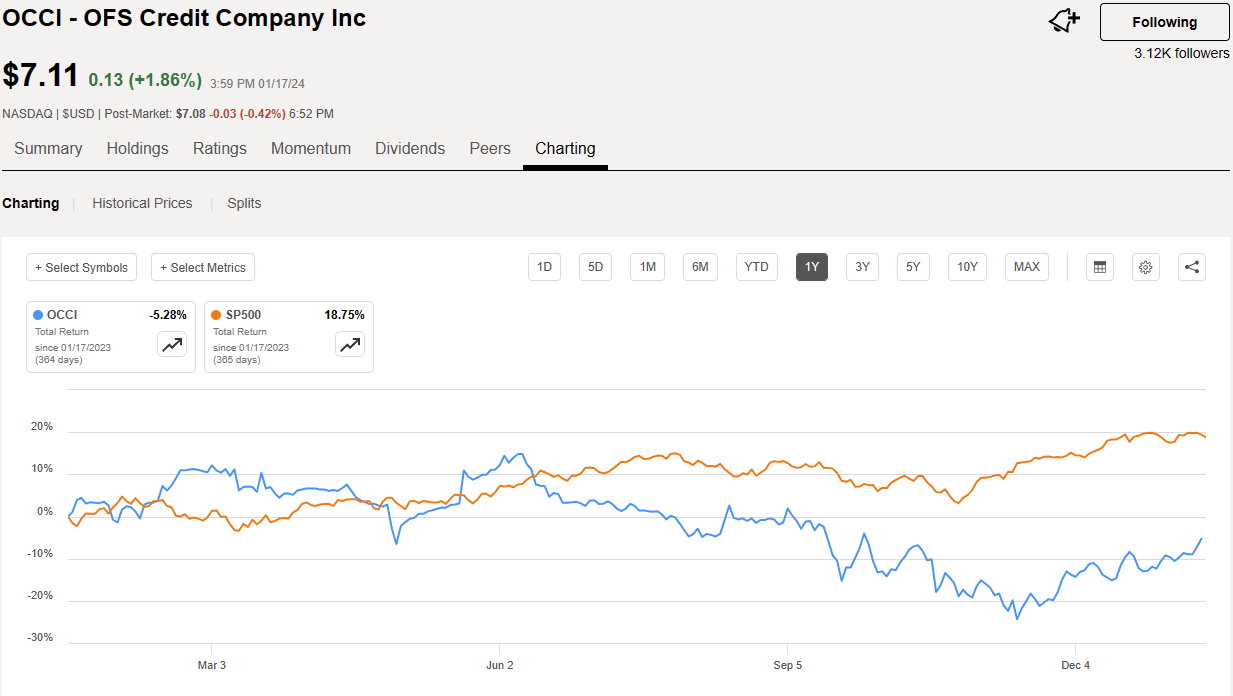

The total return performance for OCCI was unremarkable in 2023, however, the new distribution policy appears to have increased investor interest and the trend has improved over the past couple of months.

{kind=link}

I am personally a big proponent of funds that invest in CLOs including ECC, OXLC, XFLT, CCIF, JBBB, and others, and I am happy to see that OCCI has turned the corner in terms of performance while offering a generous 17% yield for income hungry investors. I hold a substantial position in OCCI in my Income Compounder portfolio and look forward to the regular monthly distributions going forward.

Thanks for reading and let me know if you are aware of any CEFs that use a level distribution policy and either increased or reduced the monthly distribution in January that I may have missed. Good luck with all your investments.

For further details see:

These 7 High-Yield CEFs Reduced Distributions In 2024, Consider Buying Anyway