CMF - Thoughts From The Municipal Bond Desk

2023-09-16 04:30:00 ET

Summary

- New York City’s Metropolitan Transportation Authority anticipates five consecutive years of balanced budgets.

- Adding extreme heat to FEMA’s major disasters list can help cities and states avoid credit rating downgrades.

- Credit rating upgrades outpaced downgrades by significant margins during the second quarter of 2023.

By Mark Paris, Chief Investment Officer, Head of Municipal Strategies, Invesco Fixed Income and Stephanie Larosiliere, Head of Municipal Business Strategies and Development

Originally published on August 31, 2023

In our latest update on what’s going on in the muni market, we ask and answer key questions and highlight munis by the numbers for a quick look at some commonly used muni market data points.

Stephanie: One of the biggest post-COVID-19 comebacks we’ve seen came from the Metropolitan Transportation Authority ((MTA)), which runs New York City’s subways, buses, and commuter rail lines. The MTA went from losing $200 million a week in farebox and toll revenue in 2020 as subway ridership plummeted by a staggering 90%, 1 to projecting five straight years of balanced budgets. What are your thoughts on this turnaround?

Mark: I think the MTA holds the current title of comeback kid in the muni market. Federal aid certainly helped to stem the losses, but as the assistance ended, the MTA had to find ways to address its financial future. In July, the agency announced it had eliminated its budget deficits through 2027, benefiting from $5.1 billion in payroll tax revenue savings as well as fare hikes and toll increases. 1 The MTA has also said that beginning in 2025, it will realize $500 million of annual operating savings, which could also help the agency keep its budget in balance. 1 And if that wasn’t enough, it’s currently installing tolling systems for its congestion pricing initiative, which is projected to raise revenue for $15 billion for transit projects, like upgrading the signaling system, improving accessibility, and expanding access to the transit system. 2

Stephanie: July was the hottest month on earth since U.S. temperature records began. Cities are now pushing for extreme heat to be added to the list of major disasters that are eligible for broad federal support. Should we be adding extreme heat to that list?

Mark: I will start by saying that this is bipartisan legislation in Congress, which is very rare these days. The Extreme Heat Emergency Act of 2023 would add extreme heat events to the Federal Emergency Management Agency’s (FEMA) list of major disasters. As the average season for heat waves has increased by 47 days across 50 major US cities since the 1960s, heat has become the leading cause of weather-related deaths in the US. 3 Extreme heat can also damage power grids and essential transportation infrastructure systems. If extreme heat is added to the definition of major disasters, state and local governments would be reimbursed by FEMA for costs associated with establishing cooling centers, supporting their vulnerable populations, and repairing critical infrastructure. Historically, FEMA assistance has been important in protecting cities and states from credit ratings downgrades during major disasters, such as wildfires and flooding. The passage of this bill would be a net positive for municipalities.

Stephanie: According to second-quarter data, it looks like the positive credit trends in munis haven’t skipped a beat. I noticed some impressive upgrade/downgrade ratios.

Mark: We certainly did. In the second quarter, there were significantly more ratings upgrades than downgrades. S&P Global Ratings announced 465 upgrades versus 76 downgrades, an upgrade/downgrade ratio of 6.1 to 1.4. It’s the ninth consecutive quarter where upgrades exceeded downgrades. Moody’s Investors Service also reported positive data, with 189 rating upgrades versus 35 downgrades in the second quarter — a 5.4 to 1 upgrade/downgrade ratio and the 10th consecutive quarter of overall credit quality improvements. 4

Munis by the numbers:

A quick look at some commonly used municipal market data points.

Fund flows: Weekly and monthly reporters in $ millions

Week ending Aug. 30, 2023

| Actual | YTD total | 4-wk avg | |

|---|---|---|---|

| All term muni funds | |||

| 408 | |||

| (7,573) | |||

| (88) | |||

| Open-end muni mutual funds | |||

| (352) | |||

| (11,095) | |||

| (306) | |||

| Municipal ETFs | |||

| 760 | |||

| 3,522 | |||

| 218 | |||

| New York | |||

| (12) | |||

| (753) | |||

| (11) | |||

| California | |||

| (42) | |||

| (308) | |||

| (1) | |||

| National | |||

| 522 | |||

| (4,114) | |||

| (16) | |||

| High yield | |||

| 63 | |||

| 1,464 | |||

| 43 | |||

| Intermediate | |||

| (51) | |||

| 1,164 | |||

| 20 | |||

| Long term | |||

| 676 | |||

| 8,642 | |||

| 304 | |||

| Tax-exempt money market | |||

| 1,440 | |||

| 3,240 | |||

| 159 |

| Sources: Lipper US Fund Flows, JP Morgan, as of August 30, 2023. YTD = year to date. |

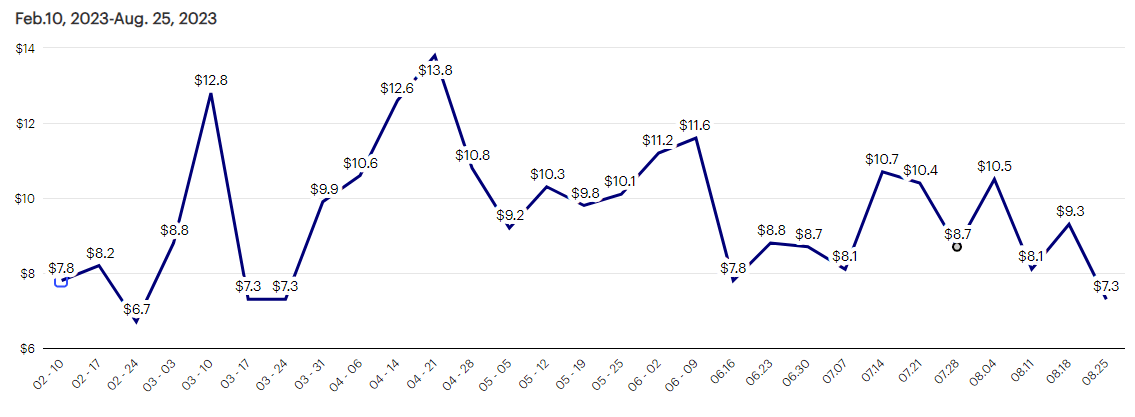

30-day visible supply in $ billions

{kind=link}

| Source: The Bond Buyer from February 10, 2023 – August 25, 2023. The 30-day visible supply is compiled daily from The Bond Buyer’s Competitive and Negotiated Bond and Note Offerings calendars. It reflects the dollar volume of bonds expected to reach the market in the next 30 days. Issues maturing in 13 months or more are included. |

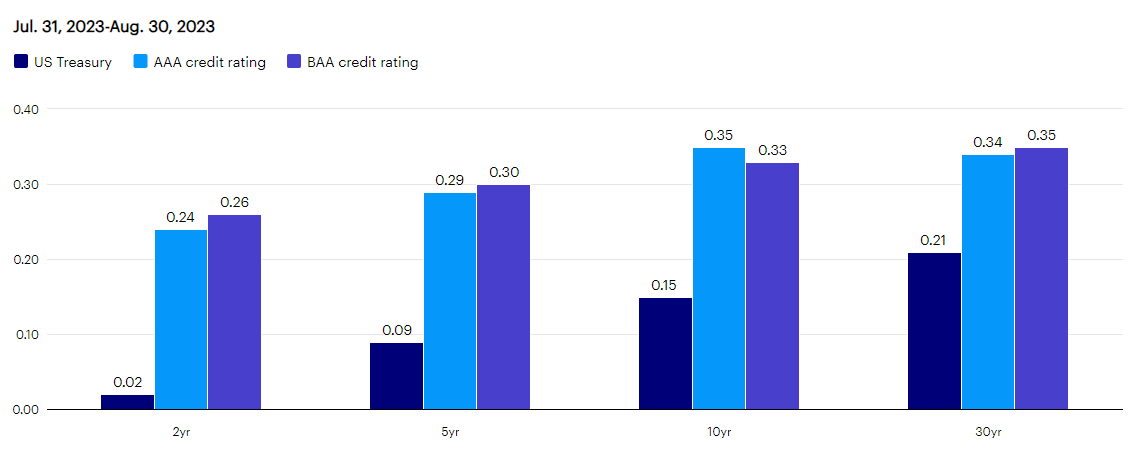

One-month yield percent change:

{kind=link}

| Sources: Refinitiv MMD Curve and US Department of the Treasury, from July 31, 2023 – August 30, 2023. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments, or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice. For more information on rating methodologies, visit the following NRSRO websites: www.standardandpoors.com |

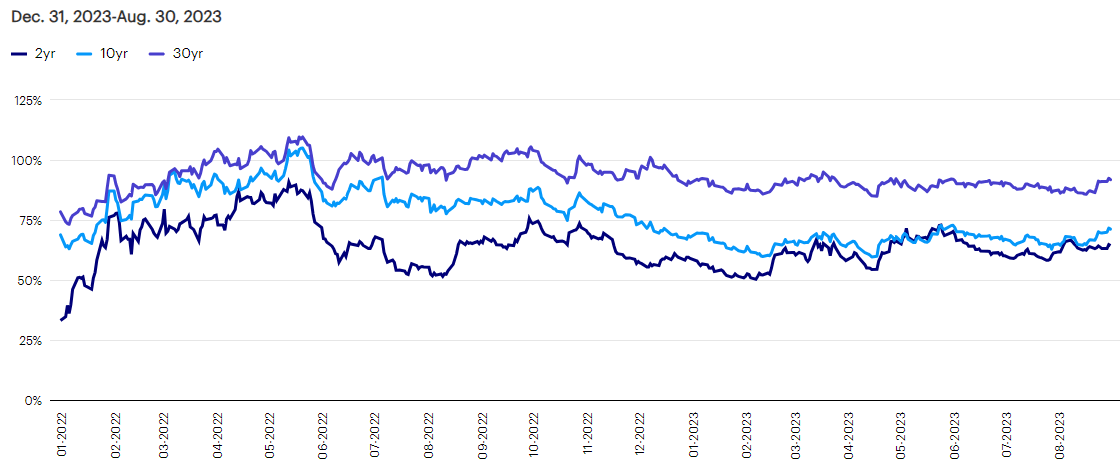

Municipal/Treasury ratio

{kind=link}

| Source: Thomson Reuters TM3, as of August 30, 2023. Treasuries are backed by the full faith and credit of the US government as to the timely payment of principal and interest, while legislative or economic conditions could affect a municipal securities issuer's ability to make payments of principal or interest. |

Footnotes

1 Sources: Metropolitan Transportation Authority (MTA), Bloomberg L.P., as of July 17, 2023.

2 Source: MTA, NYC Central Business District Tolling Program ((MTA)), as of August 17, 2023.

3 Source: Federal Emergency Management Agency, NPB Climate Change Response and Recovery Planning Guide ( FEMA.gov ), July 2023.

4 Source: Bank of America Global Research, as of August 18, 2023.

Important information

NA3115086

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/or interest.

Junk bonds involve greater risk of default or price changes due to changes in the issuer’s credit quality.

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations), and investors may not get back the full amount invested.

The values of junk bonds fluctuate more than those of high-quality bonds and can decline significantly over short time periods.

All fixed income securities are subject to two types of risk: credit risk and interest rate risk. Credit risk refers to the possibility that the issuer of a security will be unable to make interest payments and/ or repay the principal on its debt. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

Municipal bonds are issued by state and local government agencies to finance public projects and services. They typically pay interest that is a tax in their state of issuance.

Because of their tax benefits, municipal bonds usually offer lower pre-tax yields than similar taxable bonds.

All data as of August 31, 2023, unless otherwise stated.

All data provided by Invesco unless otherwise noted.

The opinions expressed are those of the author, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. It is not intended or written to be used, and it cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on the taxpayer under US federal tax laws. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Past performance does not guarantee future results. An investment cannot be made into an index.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

There is no guarantee the outlooks mentioned will come to pass.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Thoughts From The Municipal Bond Desk