AY - Thoughts On Atlantica Sustainable Infrastructure Brookfield Renewable And The Sector In General

2023-12-04 22:10:07 ET

Summary

- Renewable energy producers are facing pressure due to increasing interest rates worldwide.

- The impact of interest rates on each company will vary depending on their debt management and contract structures.

- Some companies in the sector may be trading below fair value and are worth further examination.

It is no secret that renewable energy producers ( RNRG ) have been under pressure as a result of increasing interest rates around the world. While it is true that the sector uses significant amounts of debt to finance projects, the impact will vary from company to company. Some were very prudent, locking in low financing for many years, while others were less careful and will have to refinance significant amounts of debt in the short to medium term.

Another important difference is the way each company structured its contracts, with some companies being smarter in anticipating inflation and negotiating agreements where the price was indexed to inflation or at least adding annual escalators. There are also important differences in the type of technology, diversification, and growth pipeline of each company. For these reasons, we believe it is worth looking more closely at each company, as we believe some companies in the sector are trading significantly below fair value.

The Interest Rate Effect

The past year has seen a sharp increase in interest rates, as can be seen in the iShares 0-3 Month Treasury Bond ETF ( SGOV ), which has gone from yielding next to nothing to roughly 4.5%. This has put downward pressure on renewable energy producers, especially those that had attracted investors because of their dividends. As a result, a lot of the companies in the sector have much higher dividend yields compared to a year ago. Still, there is wide dispersion in the dividend yields, and for good reason. Let's analyze each of these companies to better understand their specifics, and whether they might represent a good opportunity at the moment.

NextEra Energy Partners

NextEra Energy Partners ( NEP ) had been under pressure because of the higher interest rate environment, but what triggered a massive sell-off was when it slashed its growth outlook. The company reduced limited partner distribution per unit growth to 5% to 8% annually, through at least 2026, with a target of 6% growth, as a result of higher interest rates and tighter monetary policy. NEP had previously guided distribution growth of 12%-15% through at least 2026.

While this is obviously disappointing, we believe the market overreacted. It does, however, show the importance of not depending on the price of your shares/units to finance growth. We prefer companies that favor growth through a combination of free cash flow reinvestment, long-term fixed interest rate debt, and asset recycling strategies.

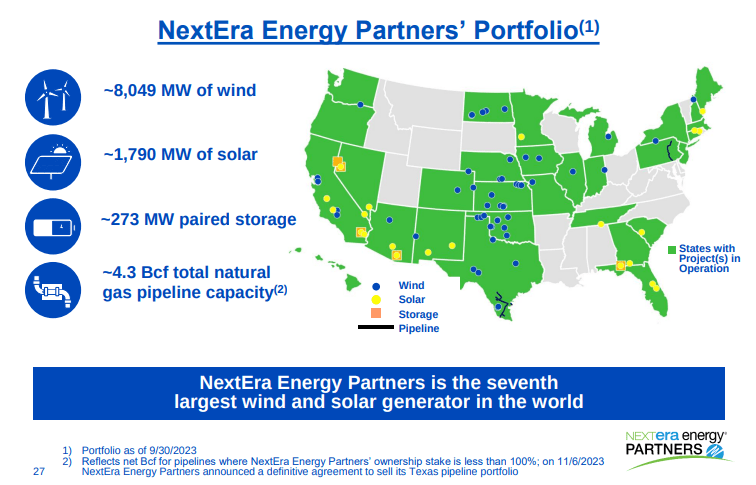

We do believe that NEP deserves a lower valuation multiple compared to other renewable energy producers, as much of the value creation is captured by its parent company NextEra Energy ( NEE ). NEP is therefore mostly a yield-co that acquires projects from its sponsor. Still, with a 2023 expected dividend per unit of $3.52, and dividend growth expected to be around 6% for the next few years, units look attractive. Although NEP will have to perform a careful balancing act, executing on accretive growth, completing key divestitures, and successfully refinancing debt that matures in the next couple of years. Compared to other renewable energy producers, we believe NEP has less diversification, as its portfolio is dominated by wind energy.

{kind=link}

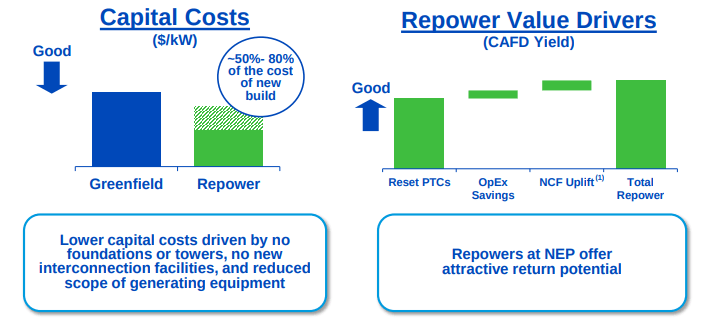

We think NextEra Energy Partners' strategy of refocusing its growth plan to where it can get highly attractive returns with modest spending is the right one. For example, the company recently announced plans to re-power ~740 MW of wind facilities through 2026.

{kind=link}

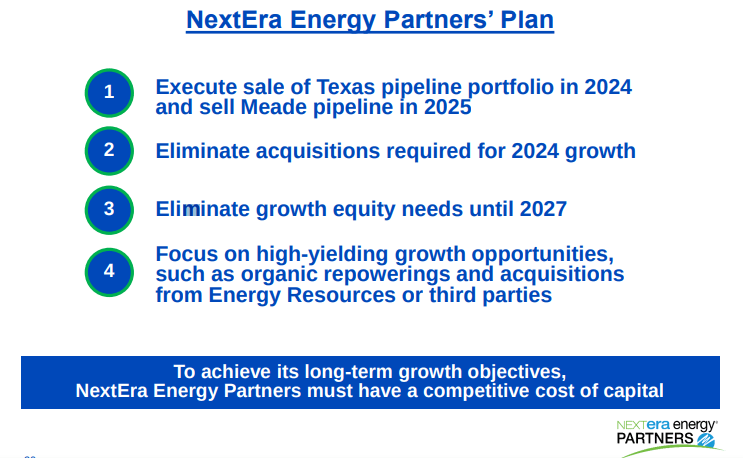

NextEra Energy Partners also announced a transition plan aiming to improve the partnership's cost of capital. The plan includes the sale of some pipeline assets, and to refocus on high-yielding opportunities like repowerings.

{kind=link}

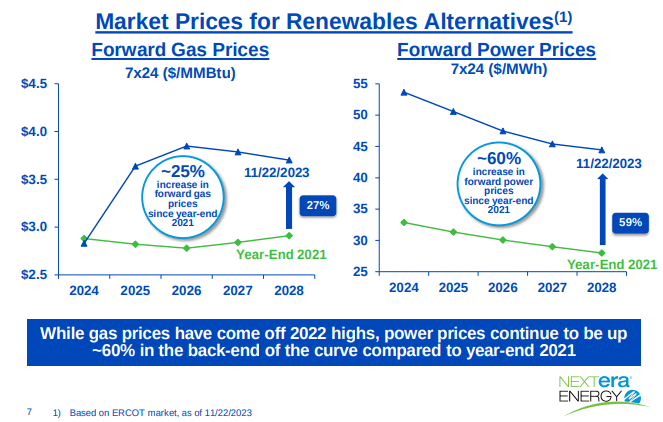

Longer-term we remain optimistic that renewable energy producers can continue growing in a profitable way. Power purchase agreements for renewables remain high, and the price for alternatives like natural gas has increased.

{kind=link}

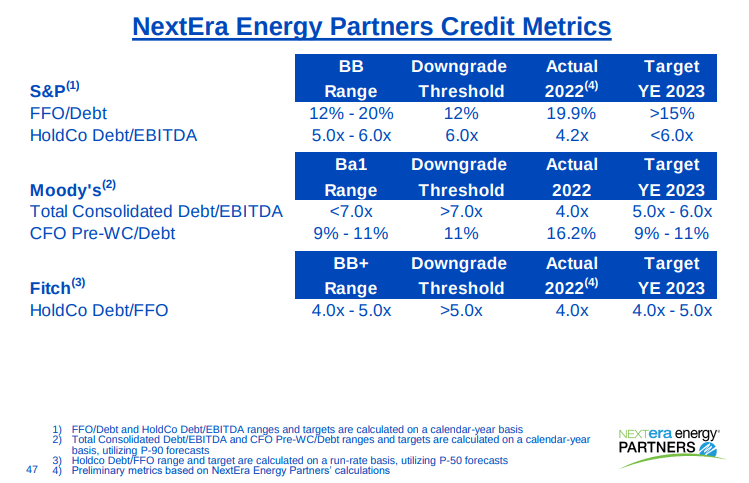

Looking at the amount of debt on NEP's balance sheet is scary, but debt to assets has actually decreased, as the company has added numerous projects to its fleet.

NextEra Energy Partners believes that its credit metrics remain within the necessary values to retain its credit rating. Still, it is clear there has been a very noticeable deterioration from 2022 to what is expected for the year-end 2023 and refinancing will prove increasingly difficult.

{kind=link}

Atlantica Sustainable Infrastructure

The next biggest yield on the list belongs to Atlantica ( AY ), with a ~9% dividend yield at current prices. They also have their own idiosyncratic risks and issues, including its sponsor Algonquin Power ( AQN ) having some financial issues, which caused speculation that they might sell their stake in AY or be a less reliable sponsor. The company has assured investors that for them it is "business as usual", while a strategic review is still ongoing. Besides the uncertainty related to its sponsor, the company has been delivering disappointing cash available for distribution growth.

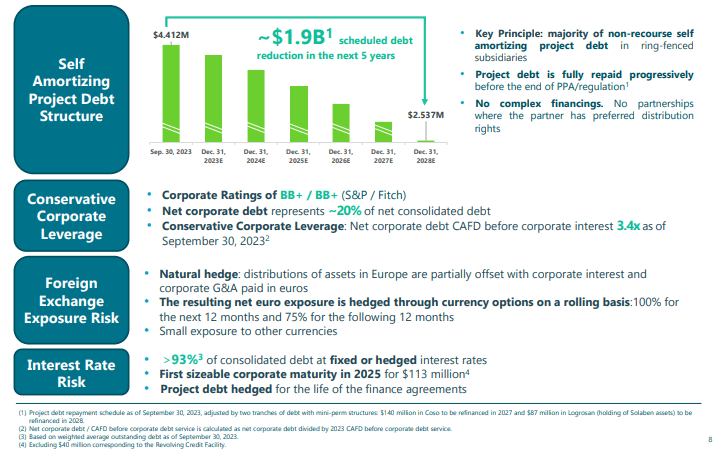

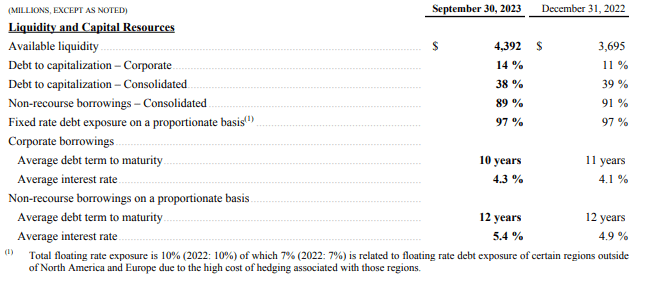

On the positive side, Atlantica has a healthy balance sheet and strong credit profile, boasting about 93% of its debt fixed or hedged, with ~3.4 years average maturity for its current corporate debt. It has a self-amortizing project debt structure and conservative corporate leverage.

Atlantica Sustainable Infrastructure Investor Presentation

{kind=link}

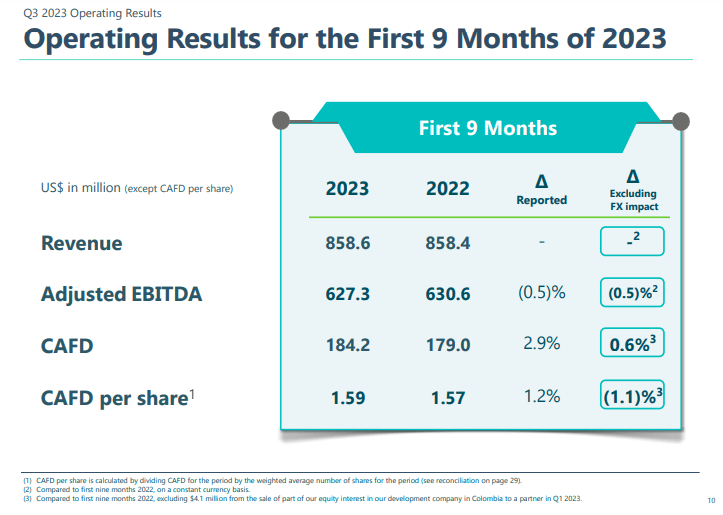

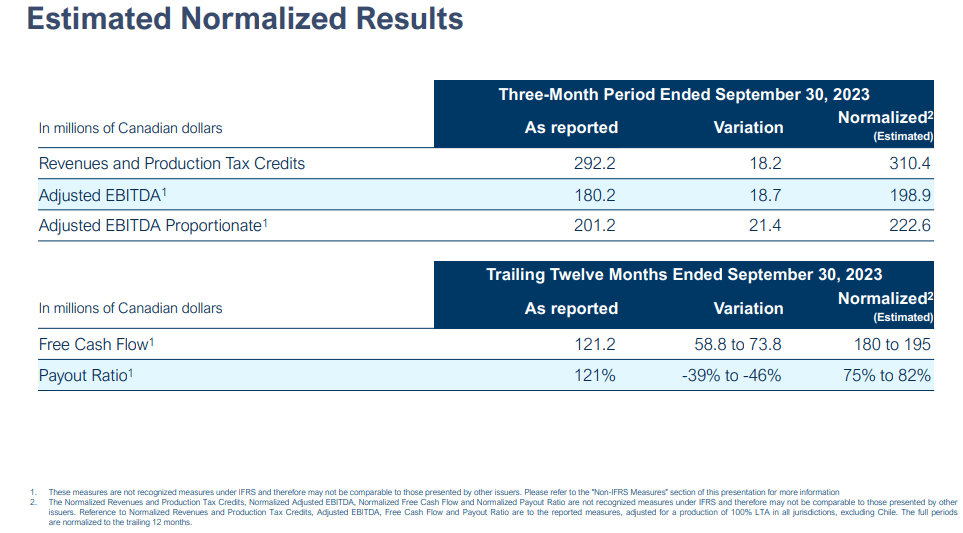

For the first nine months of 2023, cash available for distribution per share grew only 1.2%, and CAFD per share growth for 2022 was also very disappointing at ~2%.

Atlantica Sustainable Infrastructure Investor Presentation

{kind=link}

Innergex

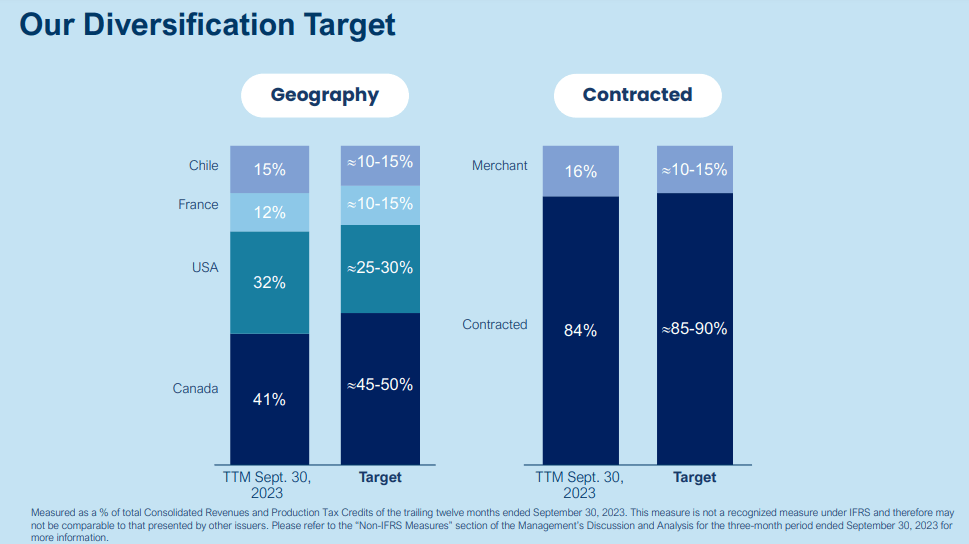

Innergex ( INGXF ) is a Canadian renewable energy producer that also pays an attractive dividend, and its shares currently yield ~7.5%. The company remains committed to maintain a Fitch Investment Grade rating of BBB-, but there is some concern as only 71% of its debt has a fixed interest rate or has long-term hedging agreements. The company has proactively financed some previously unencumbered assets to increase liquidity and plans to do this again next year with other assets. Most of the energy it generates is sold through long-term contracts, and the company is geographically diversified. It has important operations in Canada, the USA, France, and Chile.

Innergex Investor Presentation

{kind=link}

While the dividend yield is quite attractive, there is some concern given that its free cash flow has not been covering it in recent quarters. One key reason has been lower than expected energy generation due to negative weather effects. Innergex estimates that if it had generated power at its long-term average, results would have been significantly better, and its dividend payout ratio would be around 80%.

Innergex Investor Presentation

{kind=link}

The company is expecting some new projects to start contributing to its cash flows, helping reduce the dividend payout ratio too. There is no question that the company is highly leveraged, and interest rates and financing conditions will influence the share price significantly.

Brookfield Renewable

Even though the current dividend yield is considerably lower at ~5%, Brookfield Renewable ( BEP )( BEPC ) is one of our preferred operators in this industry. We believe that it can probably challenge the total return of the other companies mentioned, even with a smaller dividend yield. The company has historically grown funds from operations at a ~10% CAGR, and they have been very opportunistic in buying and selling assets. For example, they invested in Terraform Power at a very attractive valuation when their sponsor got in trouble, and often sell mature assets at high multiples of invested capital.

We believe they have some competitive advantages, including massive access to capital, which has meant it can make huge deals that are off-limits to many of its competitors. The company likes to emphasize this point by saying that some of its best deals have also been some of its largest where it has brought co-investors. We believe they have also proven to be an efficient operator, and good at negotiating contracts which often include inflation indexing. According to the company, ~70% of its revenues are inflation-linked.

Another thing we appreciate is that hydroelectric power remains its largest segment in their portfolio, as it has a very long life and very low cost, generates high cash margins, and provides storage capacity with the ability to dispatch power at all hours of the day.

Not everything is perfect either with Brookfield Renewable, like Innergex, they have recently been producing power below their expected long-term average. Their financing costs are also rapidly increasing, despite the company pointing out that ~90% of their borrowings are project-level non-recourse debt, with an average remaining term of over 10 years, no material near-term maturities in the next five years, and only 3% exposure to floating rate debt. Despite this, their non-recourse average interest rate has increased about 50 bps in just nine months.

{kind=link}

Still, we believe Brookfield Renewable offers one of the best risk/reward options in this industry. We like their develop, build, and operate strategy, creating significant value for investors. They often recycle assets to low cost-of-capital buyers and re-deploy into new opportunities expected to generate higher returns.

Brookfield Renewable Investor Presentation

{kind=link}

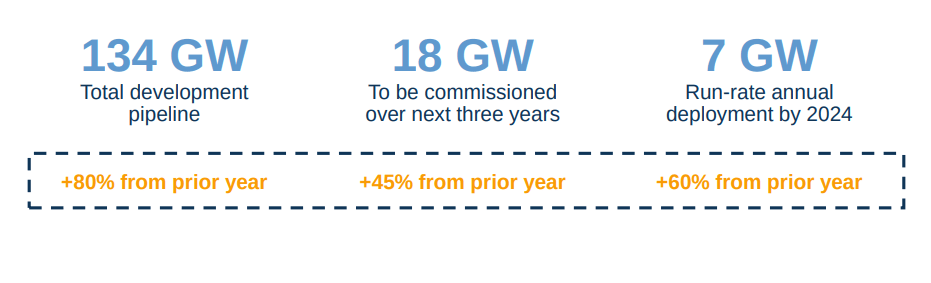

Fortunately, they are not short on opportunities, as their global development pipeline has reached 134 GW, and is one of the biggest in the world. This makes the company confident that they can put capital to work at 12-15% returns. Just over the past twelve months, the company has already commissioned a record ~3.4 GW of projects expected to add ~$50 million in annualized FFO.

Brookfield Renewable Investor Presentation

{kind=link}

The company believes it can deliver 10%+ FFO per unit growth through 2028, which could result in ~15% total returns when adding the dividend.

Brookfield Renewable Investor Presentation

{kind=link}

The company is accelerating its annual deployment rate, expected to reach 7 GW next year, which is a 60% increase year over year. The total development pipeline is growing at an even faster rate, meaning the company has a lot of optionality. They can decide to structure very profitable partnerships to develop some of these opportunities, or simply have their pick as to which assets to develop where they see the best risk-adjusted returns.

Brookfield Renewable Investor Presentation

{kind=link}

Developing these assets is not cheap, of course, which has meant a significant increase in total long-term debt. We are not overly worried, as the debt to assets ratio has remained relatively stable.

Orsted

The last one we put on the list is Orsted ( DNNGY )( DOGEF ), which has the lowest yield of the group at ~4%, and recently experienced a massive decrease in share price after it shocked investors with enormous write-downs of its US offshore wind projects.

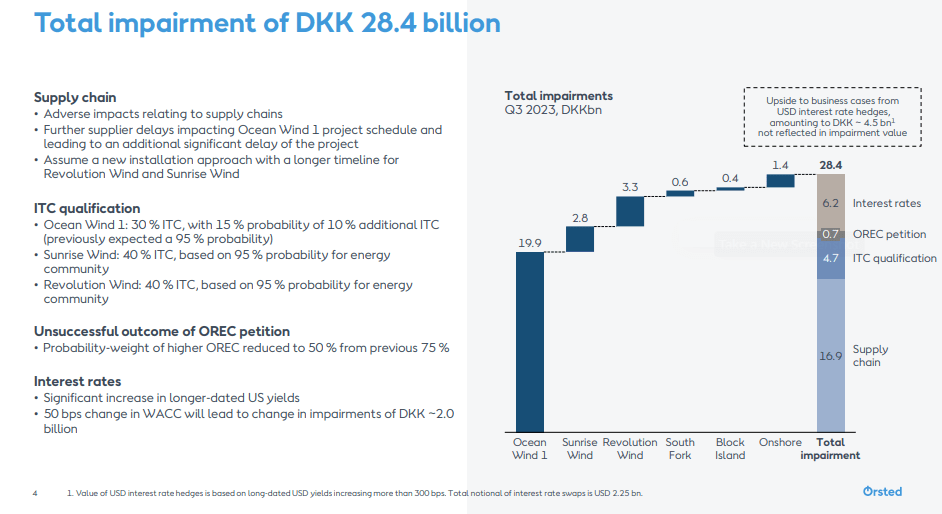

It was known that there were issues with these projects. These are big multi-year projects where costs had increased, there were supply chain issues, financing had gotten more expensive, and there was unwillingness to pay more for the energy produced. Particularly significant are Ocean Wind 1 (1,100 MW) and Ocean Wind 2 (1,148 MW), which are very big projects. Total impairment of DKK 28.4 billion is roughly $4.1 billion.

{kind=link}

What really surprised investors was the magnitude of the impairments the company took, and that it took them in phases. The losses are the result of things like non-refundable payments to suppliers and other non-recoverable expenses. Some investments might be recovered by reusing certain pre-paid components, but management does not sound too optimistic about the amounts it can recover, and it is probably better to take assume the write-downs are good estimates of the value lost in these projects.

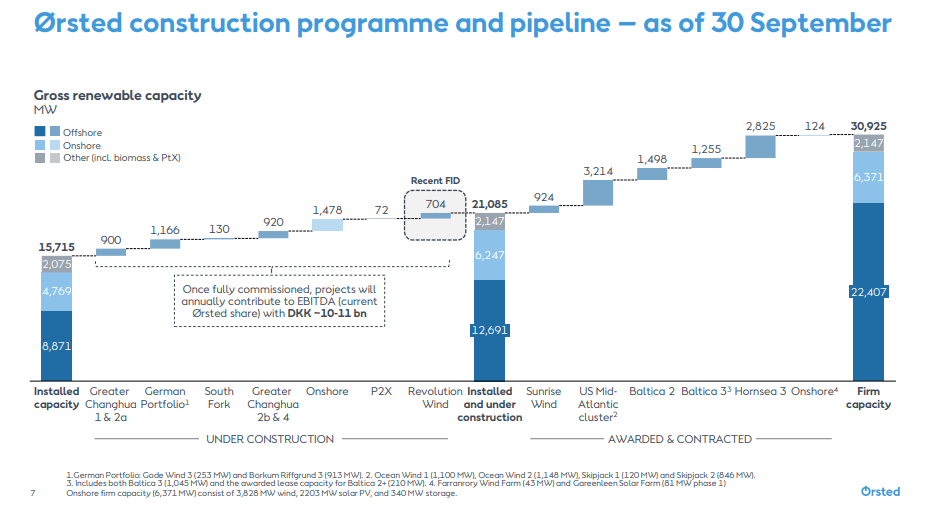

It was a shame the company had to take these write-downs, as the operational performance of its existing fleet had been quite good. The company reported Q3 2023 underlying EBITDA was up by more than 70%. We also appreciate the clear line-of-sight to multi-year growth, with the company expected to double its capacity by 2030. Importantly, these only take into consideration under construction, and awarded and contracted projects.

{kind=link}

Despite the huge disappointment for investors from these impairments, we believe shares are now trading at an attractive valuation. EBITDA, excluding new partnerships and provision, is guided for 2023 at DKK 20 to 23 billion. That is roughly $3 billion, which given Orsted's ~$26 billion enterprise value puts the EV/EBITDA at ~9x. While this might seem an extreme bargain, it is important to remember just the under construction projects are estimated to add ~50% to the company's EBITDA. Once the awarded and contracted projects are added to, operational EBITDA will probably roughly double from current levels. We believe off-shore wind remains an important component of the energy transition, and prices will have to adjust to make projects profitable. We agree with Morningstar's analyst that puts fair value around DKK 540, significantly above current prices of DKK 326 for the native shares.

Valuations

As we have seen, most of the best-known companies in the renewable energy generation sector are facing issues of some type, in addition to the general headwind coming from higher interest rates. Still, valuations have come down significantly, and we believe this is a good time to look for opportunities in the sector.

Most of these companies are trading with a price/book multiple below their ten-year averages, with Brookfield Renewable being the only exception. NextEra Energy Partners and Innergex are trading at less than half their ten-year average multiple. Of course, things look different for each company, as they have different idiosyncratic risks, different technologies, financing strategies, development pipelines, etc.

Risks

The whole sector faces the risk that interest rates might have to further increase, or stay elevated for a long time, making refinancing more difficult and expensive.

Companies in the sector also face write-down risks, as Orsted recently experienced, from projects that become no longer viable, or the risk of a potential credit downgrade, as could happen with NextEra Energy Partners if its credit metrics continue to deteriorate further. Still, we believe that in most cases the market is already properly discounting these risks, and in some cases perhaps going too far.

Conclusion

We believe this is a great time to look at some of the main companies operating in the renewable energy sector, as their shares and units have seen significant price declines. Which of these companies is the most undervalued is difficult to tell, as they face different risks, and have a different technology mix, financing strategies, and track records. As a group we do believe they are undervalued, and they are on average trading below their ten-year price/book value multiples. Interest rates have not been this high in a long time, but support has also increased significantly for the energy transition. The price for alternatives like natural gas has increased significantly as well, increasingly corporations are making plans to source their energy from renewable sources, and most experts forecast more renewable energy assets will have to be built. For these reasons, we believe this is a good time to take a look at the sector in general.

For further details see:

Thoughts On Atlantica Sustainable Infrastructure, Brookfield Renewable, And The Sector In General