TNGRF - Thungela: Stay The Course

Summary

- Thungela's share price has declined sharply, following thermal coal prices.

- Despite temporary headwinds, the company is extremely cheap, even at $135 per tonne.

- Thungela is going to pay out one-fourth of its current market capitalization as a final dividend for FY 2022.

- The thermal coal market is likely to remain strong in 2023, thanks to a pick-up in imports from China and robust demand from India.

Since publishing in December my buy recommendation for Thungela ( OTCPK:TNGRF , TGA.L, TGA.JO), the stock has returned -20%. I believe that there is a lot of value in reassessing one's own trading decisions and trying to evaluate their goodness, separating the noise from the signal. This is especially true when the stock moves against initial expectations.

To clarify, I invest with a medium- to long-term horizon of a few years. However, I also consider more immediate factors. A stock may be cheap, for instance, but if I see no immediate catalysts, it is best to wait before deploying capital. I believed that such catalysts were in place in the case of Thungela, which has not been the case for now. First of all, let me recap my reasoning at the end of last year.

Like many coal producers, Thungela is producing a significant amount of free cash flow, and returning it to shareholders in the form of dividends. Since its spinoff from Anglo American in June 2021, the company has had a truly spectacular ride, which has been accelerated in 2022 by Russian-Ukrainian tensions. Its main driver, the price of thermal coal ( API4 ), reached its high at the end of August, but then, after a short rally back above $200 per tonne, it has declined to the current level of around $135 per tonne.

{kind=link}

The share price has clearly followed fluctuations in the coal market. To add to the woes, Thungela disclosed in December that full-year production has been significantly impaired by on-going problems along the Transnet railway line. It has also revised its costs upward because of inflationary pressures and logistical challenges.

Despite all these known headwinds, I remained bullish on Thungela for several reasons. First of all, the company is extremely cheap. This is true all the more so after the recent decline in the stock price. The math is pretty straightforward. The current market cap is around R32 billion and, at the end of November, the company had no debt and a cash position of R19.8 billion. Assuming my estimate of R8.8 billion for the H2 2022 dividend is correct, Thungela is going to return more than one fourth of its total market cap in March via its final dividend.

Of course, it is unlikely that next year the company will be able to pay out R17 billion in dividends, because it is unlikely that the price of thermal coal will reach in the near future the same levels as last year (which were the results of a unique combination of factors). But one should not underestimate the huge margin of safety that is implied by a distressed valuation. At the current coal prices of around $150 per tonne (which I speculate will probably turn out to be lower than the year average), the dividend yield may not be 50%, but it should still be around 20%. If one's investing horizon extends beyond a few months, it seems unwarranted to be bearish just because of where thermal coal prices are currently trading. This is especially true considering that this winter has been quite mild, re-stocking will need to occur for the next winter, and the structural problems of the energy markets (years of underinvestments, because of low prices and ESG policies restricting the flow of capital) are still in place.

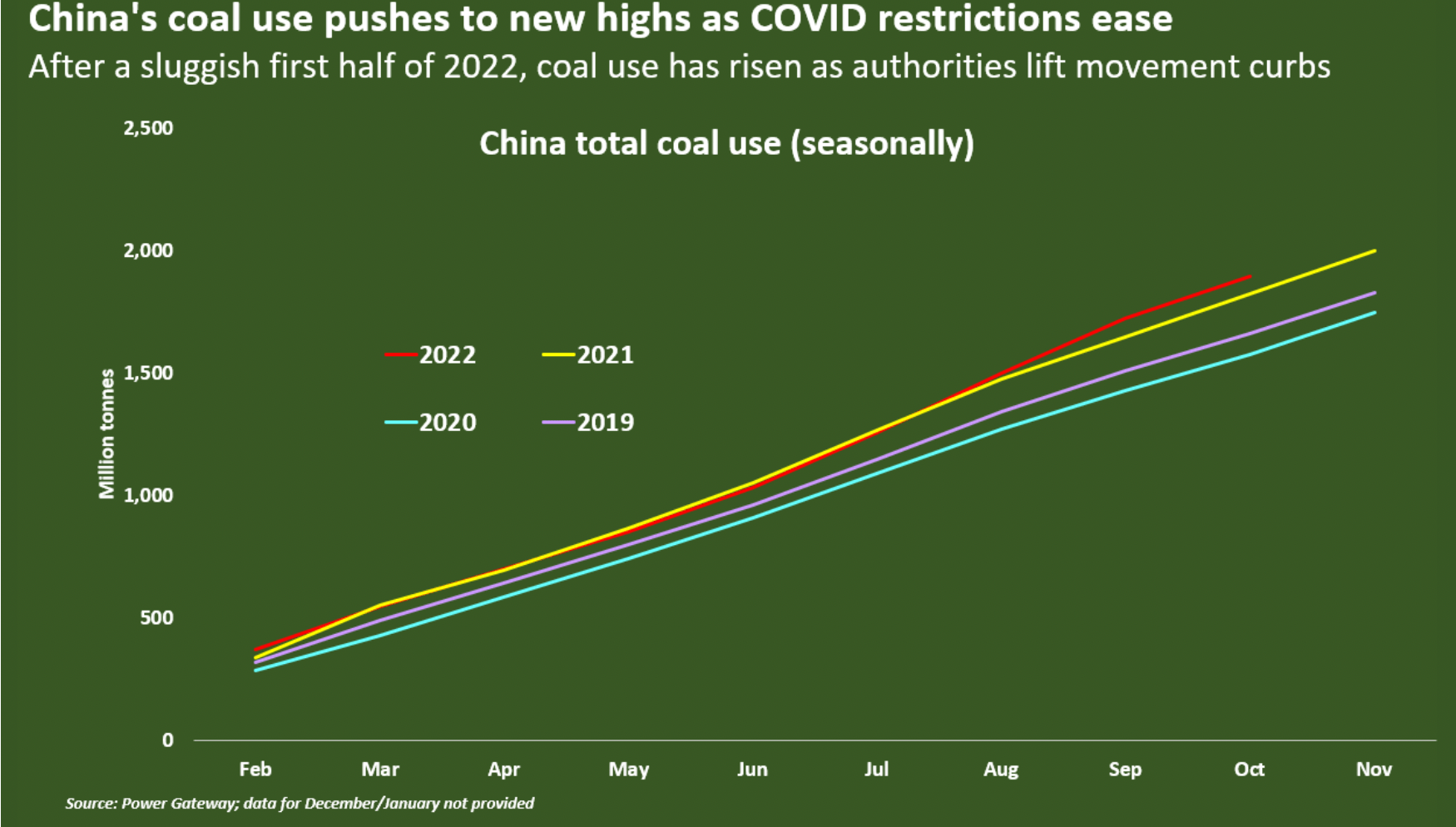

In addition, I had reason to be optimistic because winter was approaching, which is usually supportive for thermal coal prices. On top of that, China seemed ready to reopen after abandoning its zero-covid policies, which should also have been bullish for coal prices. Finally, the disruptions along the Transnet railway line seemed to have reached their climax and be gradually abating. It seemed to me that peak pessimism had already been reached, and the situation could only improve.

We don't know whether next year Thungela will manage to solve, at least in part, its logistical railroad problems and increase sales. However, it still seems likely that thermal coal demand will remain robust . In particular, China is going to play a bigger role in coal markets in 2023. It should be remembered that China covers around 90% of its total demand from domestic sources, and that in 2022 it ramped up production. As a result, demand was largely flat compared to the previous year, but imports were sharply down. This helped to balance the coal markets, given the increase in demand from Europe, where coal demand has replaced gas demand from Russia.

{kind=link}

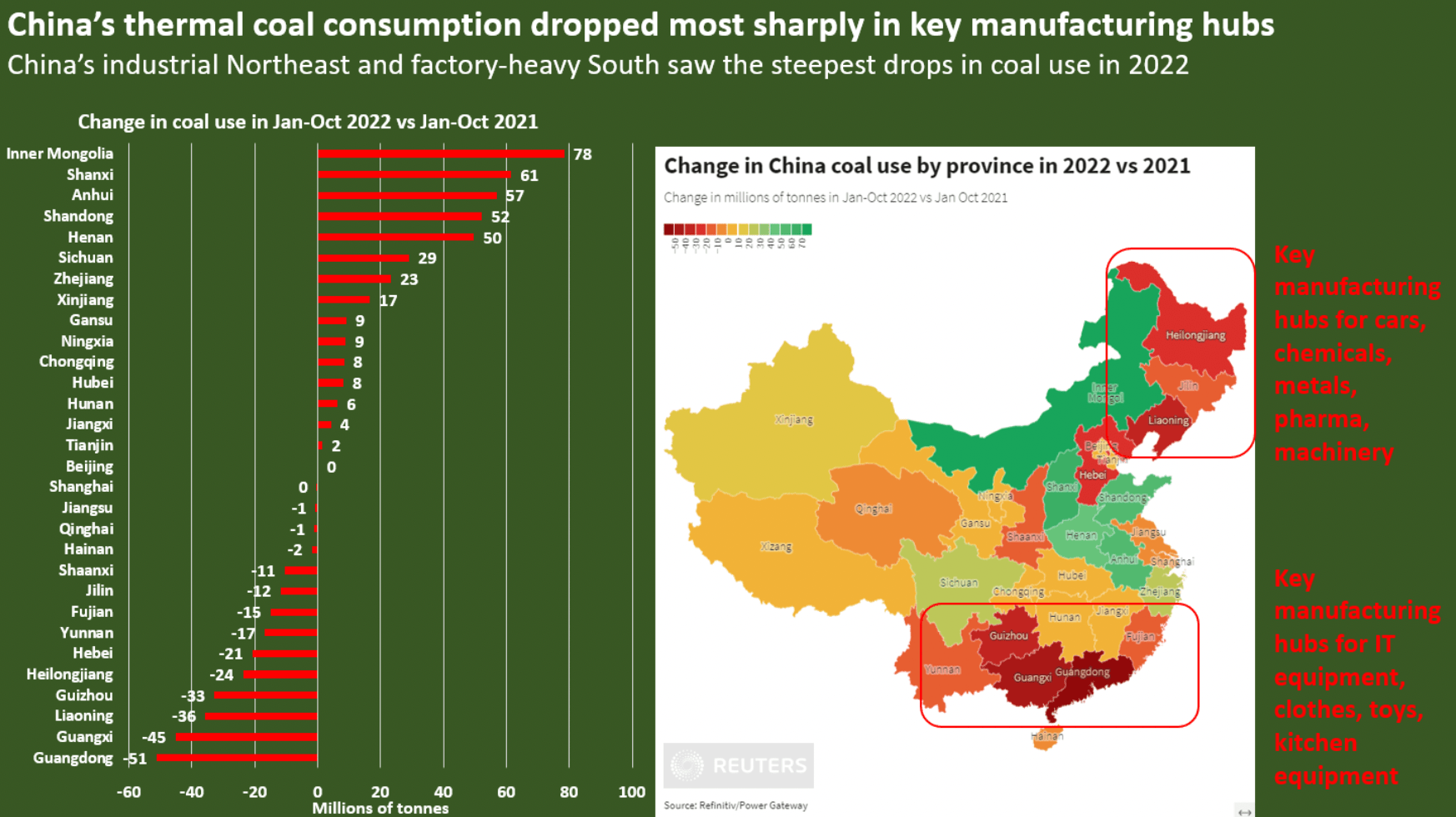

Now, however, the wind is turning. Chinese coal demand has dropped more remarkably in key manufacturing regions. These are likely the regions that will see coal demand rebound more strongly, as the Chinese authorities lift COVID restrictions and stimulate economic activity. Crucially, China's industrial regions are heavily dependent on imports, since they are located far from main domestic mining centers, but close to port facilities. Therefore, I expect China's coal imports to grow compared to last year. A first confirmation is the lifting of the ban on coal imports from Australia.

{kind=link}

European demand may decline, as alternative sources come online to replace Russian gas, while demand from India remains strong. Barring a synchronized global recession significantly denting demand (a scenario I don't see as likely), coal prices are expected to remain sustained through much of 2023. The recent volatility could be explained by the easing of fears over winter's supply in the northern hemisphere (one only has to look at the collapse of gas prices for an example), while the effect of Chinese activity picking up may require more time to have an impact. Sentiment may also be playing a role, with many investors sitting on huge gains and wanting to realize them, while a lot of tourists have recently entered the sector and may be tempted to sell at the first sign of weakness.

In conclusion, I see the current decline in coal prices, and as a result, Thungela's share price, as a buying opportunity. The fundamentals of the coal market remain strong, while the company keeps getting cheaper, making it even more attractive. I would like to conclude, however, with a note of caution. The easy money in coal has already been made in 2021 and 2022. Coal names went from left-for-dead to massive cash flow machines. While they will continue to print cash for several years to come, a repeat of 2022 is unlikely. Comparisons will be tough and many coal names may decline further in the short term. From my point of view, any such temporary weakness provides an opportunity to accumulate, given that the structural fundamentals are unchanged. Still, I believe that, going forward, it is going to be a completely different trade from the last two years, in the sense that the exciting price actions are not going to be repeated, and most of the capital returns will now come in the form of dividends. Not a reason to complain, but something to consider when dealing with the day-to-day volatility.

For further details see:

Thungela: Stay The Course