TKAMY - thyssenkrupp Does Not Know What Kind Of Company It Wants To Be

2023-06-02 09:18:15 ET

Summary

- thyssenkrupp has been in a transformation for several years now.

- Discussions about the company strategy and especially the fate of the large Steel division prevented the stock from going anywhere (at least in a positive way).

- In a sum-of-the-parts valuation, thyssenkrupp looks undervalued, but it is not clear how shareholders will profit from this.

- thyssenkrupp shareholders might not benefit much from an upcoming IPO of the hydrogen business.

(Note: All amounts in the article are in EUR. At the current exchange rate 1 EUR is around USD 1.07.)

Investment Thesis

thyssenkrupp (TKAMY) (TYEKF) is a German holding company with a variety of industrial holdings, the largest by far being the European Steel and the Materials divisions, which produce and trade steel and steel products.

I have started building a position in the company twice over the last two years, only to stop shortly afterwards due to unexpected bad news. Each time I managed to sell with a small profit, and maybe this has kept my interest in the company alive. Also, the share price kept falling back to my baseline. The new CEO and the upcoming Nucera IPO made me consider again, but I decided to stay on the side-lines. The reasons are twofold.

Firstly, I think that thyssenkrupp will probably hold on to the Steel division after various divestment efforts over several years did not produce any tangible result. The company will need to put a lot of money into the green transformation of its steel production, which it does not really have. So it will depend on public funding and subsidies, and going forward no decisions will be made without a go ahead from the powerful IG Metall union and government approval. Both entities not necessarily prioritise shareholder interests - which is not even unfair given that public subsidies will be used to keep the business afloat.

Secondly, my opinion on the Nucera IPO is that it will likely not benefit thyssenkrupp shareholders much. They will be diluted as the money raised will stay with Nucera to be invested there. If a recent Bloomberg article is right, thyssenkrupp will sell additional shares out of its holding. In a worst case scenario for me, the money from that sale will be used to finance the steel transformation. For me this would be like selling the future to finance the past.

Steel or no Steel?

Since the merger of Krupp and Thyssen in 1999, thyssenkrupp has been looking for ways to withdraw from the steel production business. The steel business is obviously very cyclical. When times are good, it can bring in a lot of money, but when times are bad the steel business drags the rest of the company down with it into a loss.

The previous CEO, Martina Merz, stuck to the divestment strategy, but was unable to come up with a working concept. Whatever thyssenkrupp considered - a merger, a sale, a spin-off, or an IPO - failed. It seems that nobody wanted to invest. After years of efforts, according to the German newspaper Handelsblatt the best Merz managed to come up with was an unofficial offer of EUR 1 from the finance investor CVS.

In April 2023 Merz was forced to resign after heavy criticism from the powerful IG Metall union and the thyssenkrupp works council. Besides the undecided fate of the Steel division, she liked to call thyssenkrupp a Group of Companies, but at the end said failed to explain convincingly how that concept was more than a different name for a holding company.

Significant investments in green transformation will be necessary

If thyssenkrupp keeps its Steel division, which in my opinion is quite possible, the company will have to finance the transformation to reusable energy. This will not be cheap. FCF in H1 2022/2023 (October 1, 2022 to March 31, 2023) was negative at -551mn euros. thyssenkrupp has limited financial means and the company will depend on public subsidies. Discussions are ongoing and at the end will depend on EU approval. I expect this to go through, but public funding will come with employment and location obligations.

The new CEO does not look like an obvious choice

The credentials of the new CEO Miguel Ángel López Borrego are mixed - in my view. In his previous job he was the interim CEO of the auto parts supplier Norma Group (NOEJF). But the had been in that position only for a few months. He has spent most of his career at Siemens ([[SIEGY]], [[SMAWF]]) where he was the country head in Spain and chairman of the board of Siemens Gamesa ([[GCTAF]], [[GCTAY]]). Siemens Gamesa has been unprofitable for years. That is why I am not so excited about him, but his experience in mergers and acquisitions from his time with Siemens was probably a factor in his appointment. He managed to push the Gamesa problem away from Siemens to the spin-off Siemens Energy ([[SMEGF]], [[SMNEY]]), which has taken it over and now needs to sort out the profitability problem

He will need that kind of experience. The divestment of the steel division is still the official thyssenkrupp strategy. In addition, the company plans to sell or spin off its thyssenkrupp Marine Systems subsidiary , and has revived the plans to do an IPO for its hydrogen subsidiary, Nucera.

Before I talk about the planned IPO of Nucera, which made me reconsider investing in thyssenkrupp, a few words on thyssenkrupp Marine Systems.

thyssenkrupp Marine Systems has a bright future

thyssenkrupp Marine Systems is one of the world's leading manufacturers of conventional (meaning - non-nuclear) submarines and military surface vessels. In addition to Germany, customers include Singapore, Norway, and Israel. Business is booming and there is a renewed focus on investments in military technology across Europe. A significant part of the 100 billion euros of additional investments in the German military, which the German Chancellor Scholz announced last year, will go into upgrading the German navy. But I suspect again that thyssenkrupp lacks the capital for the necessary upfront investments and wants to get additional outside capital or completely sell the company at a good price.

Nucera IPO

According to Bloomberg thyssenkrupp also intends to initiate a process to do a public listing of its hydrogen subsidiary Nucera already in June 2023. This has been in discussion for a while now, but due to adverse market conditions nothing has actually happened so far.

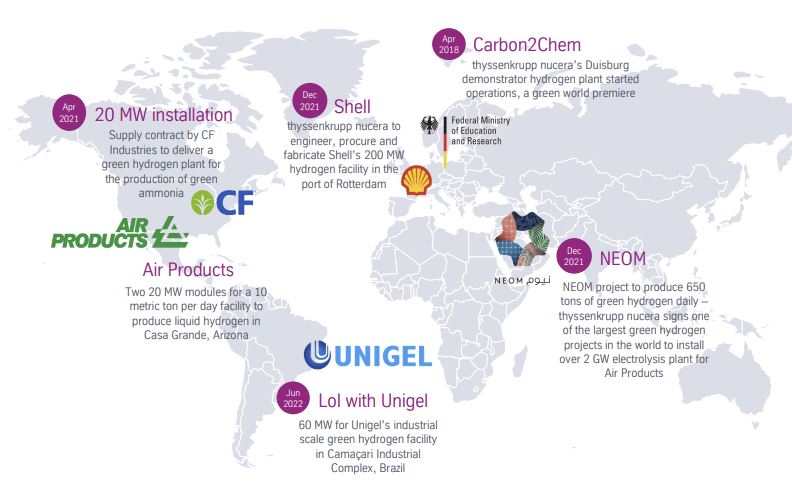

Nucera specialises in alkaline water electrolysis for the production of green hydrogen from renewable energy. The company has a global footprint and a list of prominent clients and projects.

Nucera projects (Source: thyssenkrupp nucera)

{kind=link}

thyssenkrupp only holds a 66 percent stake in Nucera. 34 percent are held by the Italian renewable technology specialist De Nora .

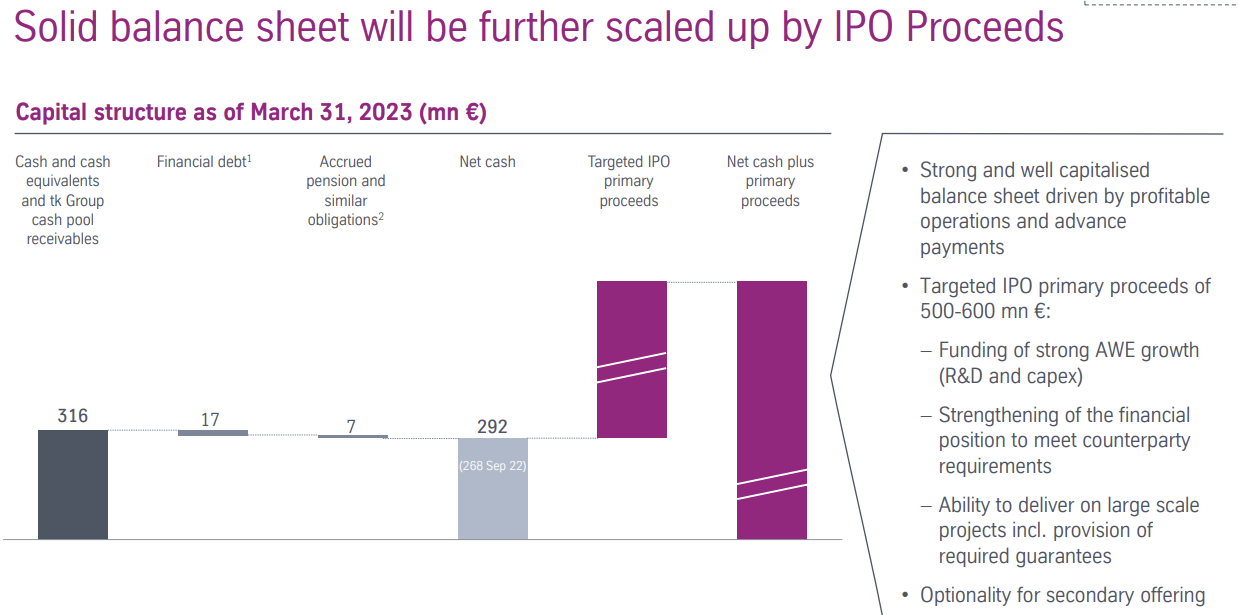

Nucera could be valued about 4 billion euros (around USD 4.33bn), which is quite a lot for a company with annual around sales of 600mn euros and an EBIT of around 30mn (see page 21 of a recent analyst presentation ). The IPO has been anticipated for quite some time and rumoured price ranges were between 2-5 billion euros. I think everything above 4bn would be a really good price. The current market capitalisation of thyssenkrupp is just 4 billion euros, the same as the reported Nucera value.

But if reports are correct, the bottom line though is that thyssenkrupp shareholders will be diluted down from a 66% stake to something above 50%. The analyst presentation confirms that the expected proceeds of 500-600mn euros will stay with Nucera.

Nucera analyst presentation (Source: thyssenkrupp nucera)

{kind=link}

To me it looks again like the IPO is a necessity to finance ongoing Nucera operations and business growth, as thyssenkrupp cannot come up with the required capital itself.

And I do not look favourably on a potential plan for thyssenkrupp to sell an additional stake in Nucera. If the prospects of the hydrogen business are so good, why sell? If the purpose is to finance the transformation of the legacy steel business, I think this is selling out the future for the past.

Conclusion

In a sum-of-the-parts valuation thyssenkrupp looks clearly undervalued. thyssenkrupp Marine Systems and the Nucera holding alone should make up more than the current market capitalization of just 4bn euros. But I do not see a clear path how shareholders can profit from this. A worst case scenario for me is that the company hangs on to the cyclical steel business and sells off other, more future-proof enterprises to finance the green transformation of the European Steel division.

Therefore, until the fate of the Steel division is clear, I suggest staying away from new investments in thyssenkrupp. There could be short-term market gains from good news, so I do not recommend selling at this low price. But the long-term share development is unclear.

For further details see:

thyssenkrupp Does Not Know What Kind Of Company It Wants To Be