ASM - Tokyo Electron: Attractive Prospect In Anticipated WFE Market Rebound

2023-11-15 07:35:24 ET

Summary

- Tokyo Electron benefits from the surge in demand for computing power, similar to selling shovels in a gold rush.

- The company's revenue drivers depend on the Capex of semiconductor companies, which is expected to increase due to AI, automotive, and IoT trends.

- Tokyo Electron is positioned for a significant rebound in the WFE market, expected to begin as early as 2024.

Investment Thesis

Tokyo Electron ( OTCPK:TOELF ) ( OTCPK:TOELY ), a leading provider of wafer fabrication equipment 'WFE,' is an attractive prospect for investors seeking to leverage the anticipated rebound in the WFE market. Beyond the current slowdown, there is a broad consensus on a rebound starting as early as 2024.

Regarding valuation, TOELF trades at a TTM PE ratio of 35x, which isn't a bargain. However, our 'Buy' rating is grounded in TOELF's unique position. As one of the entities most impacted by the recent slump in memory chip demand, it is positioned for a stronger comeback as the market recovers.

In addition to its unique position in the memory market, TOELF, holding one of the industry's most diversified product portfolios, is well-positioned to capture the broader industry tailwinds in the logic semiconductor chips market fueled by an exponential demand for data processing.

Market's Current Condition and Future Forecast

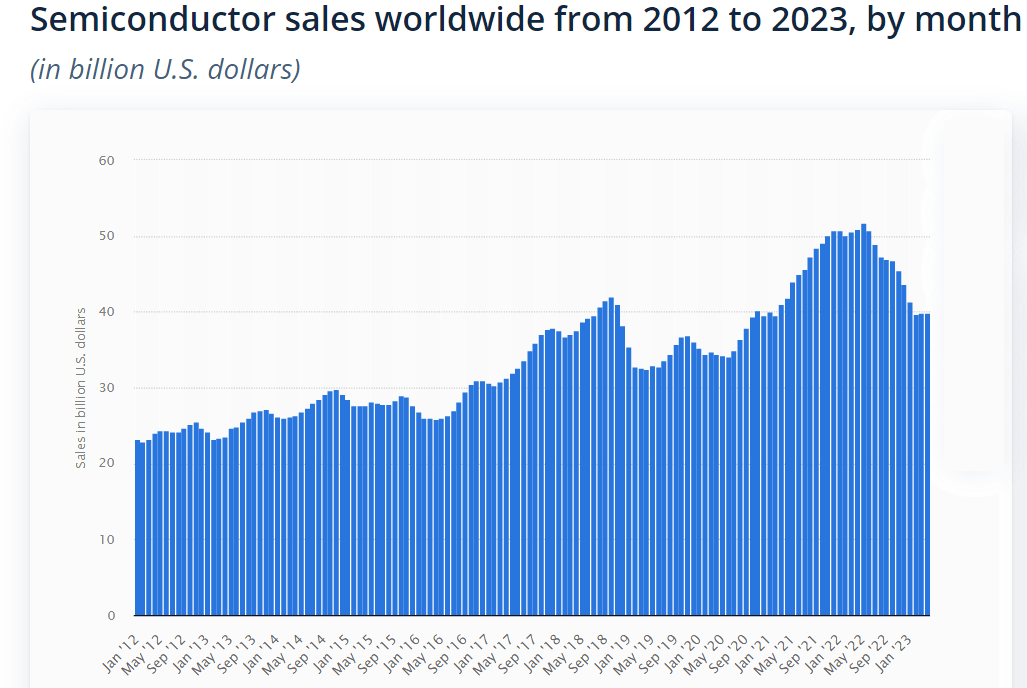

The Wafer Fabrication Equipment 'WFE' industry, which provides the machinery necessary for producing semiconductor devices, is currently experiencing a downturn. This year, the global semiconductor capex is estimated at $146 billion, 19% below 2022 levels.

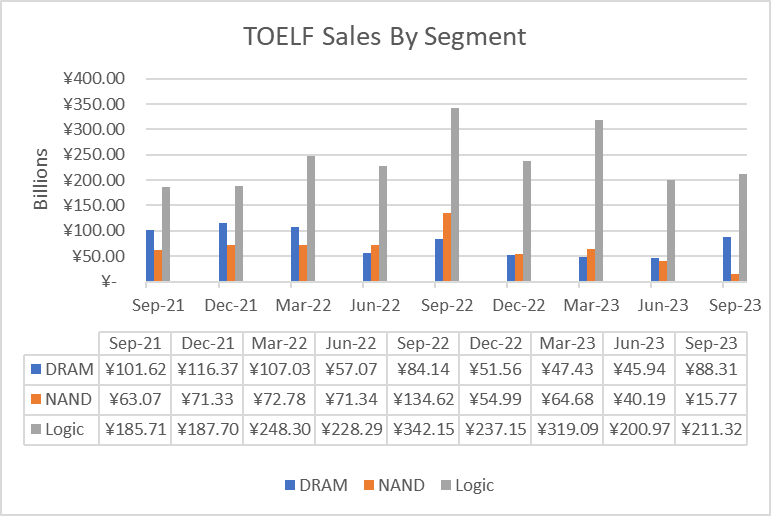

The downturn is primarily driven by reduced demand for semiconductor chips and overcapacity. The memory sector, encompassing DRAM and NAND markets, is particularly affected as it grapples with overcapacity and excess inventory, with demand expected to decline 35% this year. The DRAM and NAND markets are sensitive to consumer electronics demand impacted by high living costs and rising interest rates. TOELF , which had significant exposure to the memory market before the downturn, saw its sales decline significantly in the first half of FY 2024 (ended September 2023). The softening in demand for logic chips used in data processing hasn't helped. The September quarter's YoY comparison also comes after an exceptionally strong quarter last year.

{kind=link}

Still, we see some stability amid this challenging market. For example, TEOLF's logic segment sales remained stable compared to the June 2023 quarter, signaling the potential that the market has reached the bottom. DRAM sales show a strong rebound, too, signaling that the worst might be behind us now. Industry pundits seem optimistic for 2024. For example, Gartner expects the DRAM market to move from an oversupply to an undersupply from the December quarter. TOELF's customers are preparing for these dynamics, which are mirrored in the strong DRAM sales in the September quarter. The same is expected for NAND, starting in the second half of 2024.

{kind=link}

Statista

For these reasons, despite the double-digit sales decline, TOELF seems optimistic about the future. The company is expanding R&D to record highs, an account that signals a stronger future, as it mirrors collaboration initiatives with its customers to design and build new equipment. The company is also building new manufacturing facilities in anticipation of a strong recovery, including a $170 million production facility in Ozu and a $200 million development facility in Koshi.

{kind=link}

Tokyo Electron

Financial Performance and Outlook

Given that TOELF's fiscal year ends in March annually, the positive dynamics anticipated in 2024 are expected to influence the financial performance in fiscal year 2025.

This fiscal year, which ends March 2024, TOELF expects a 23% YoY decline as the slowdown deepens in the September quarter before rebounding in the second half of the fiscal year. The company reported a 30% sales decline in the September quarter.

Among its peers who already reported September quarter figures, Lam Research ( LRCX ) posted a 31% in sales, KLA saw a 12% fall, ASM, deviating from the patterns, registered revenue growth, aided by the acquisition of LPE, while Applied Materials ( AMAT ) management's sales projections of 5% YoY decline came better than many have anticipated.

Despite these quarterly variations, TOELF sales will realign with industry sale trends. There are no signs of market position changes, and the company is expecting a 200 billion yen R&D budget this fiscal year, the highest in its history, as it continues working with its clients to design and hone the semiconductor manufacturing process, a signal of anticipated rebound.

Revenue Drivers

Sales performance in multinational corporations is typically influenced by various factors such as competitive dynamics, product launches, market shifts, and regional economic trends. However, TOELF is an outlier, as its sales are predominantly driven by a single variable: the global semiconductor capital expenditure 'capex.' An astonishing 97% of TOELF's sales fluctuations can be attributed to changes in this metric.

TOELF's distinctive sales pattern is rooted in the peculiarities of the WFE industry. In this sector, a limited number of WFE providers cater to an equally small pool of semiconductor producers worldwide. This global orientation cushions the impact of regional economic fluctuations on TOELF's sales.

Furthermore, the leading WFE firms have each carved out a distinct market niche within the fabrication process. TOELF dominates with a complete market share in the EUV Coater/Developer market and a significant presence in the Bonder equipment (especially for AI chips), similar to how ASML ( ASML ) has secured its place in lithography, KLA Corp. ( KLAC ) in Metrology and Inspection - (its 295X Series is the industry benchmark). At the same time, ASM International ( ASMIY ) commands a 55% share of the Atomic Layer Deposition 'ALD' market. Lam Research has the dominant market share in NAND etching. However, TOEFL's breakthrough in the NAND etching market poses risks to the latter's dominance, an example of how breakthroughs can disrupt the relatively stable market of WFE, characterized by high barriers to entry, substantial R&D, and long-term customer relations.

Lately, TOELF's approach to working closely with clients on long-term initiatives to advance manufacturing processes minimizes the risks of strategic missteps that could erode market share. This starkly contrasts with the semiconductor design sector, where NVIDIA's strategic initiatives have led to its rise, while Intel ( INTC ) has suffered losses in market share due to strategic errors. Consequently, changes in WFE companies' market share are gradual.

With these market dynamics and semiconductor sales projections reaching $1 trillion by 2030, TOELF's medium-term outlook seems appealing, counterbalancing short-term demand/supply adjustments.

Buybacks and Dividends

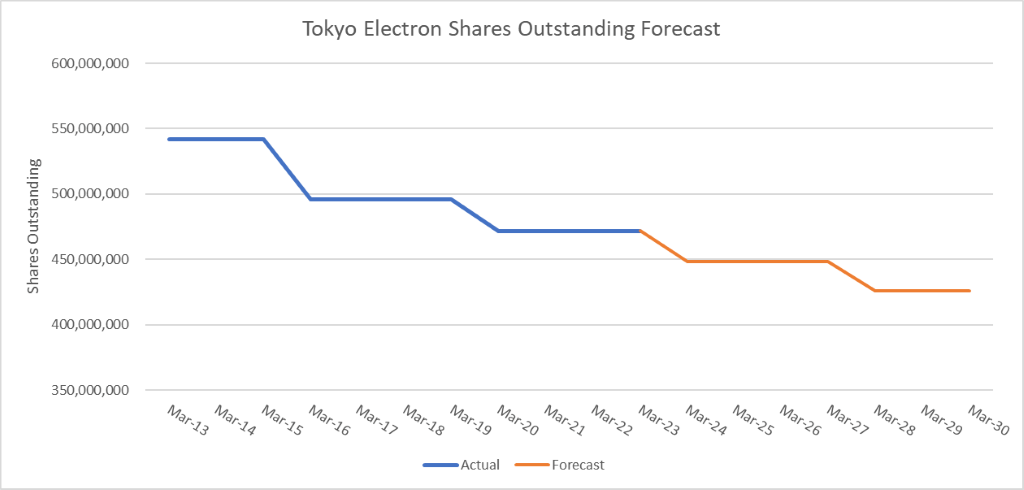

TOELF's share buyback program stands out in the WFE sector due to its structured approach. Unlike its competitors, who strategically adjust their buyback programs annually based on the market's conditions, TOELF adheres to a disciplined 4-year cycle. In its latest cycle in 2019, TOELF repurchased %5.5 of its shares outstanding.

In May 2023, management initiated a new buyback program to buy 10 million shares with a budget of 120 billion yen. However, since the announcement, the stock's significant price rise led to a different outcome. By September, TOELF had purchased fewer shares than planned, amounting to 5,899,200 for 119 billion yen, constituting 1.1% of the total shares outstanding.

TOELF's approach, including the swift execution of buybacks post-announcement, contrasts with US companies' more cautious, market-reactive strategies.

{kind=link}

Furthermore, TOELF's dividend policy is notably distinct. It pledges to return 50% of its income as dividends to shareholders, starkly contrasting the dividend growth approach of KLA and LAM, the stability-focused strategy of AMAT, and a more predictable scheme than ASM's erratic dividend pattern.

Valuation Risk

In the past decade, TOELF's Free Cash Flow ranged between $216 million and $2.1 billion, mirroring the challenges of evaluating a highly cyclical company. Still, I believe we are entering a new era of the WFE market, with AI, autonomous driving, and IoT significantly expanding.

A larger market translates to not only higher equipment sales, but also expands recurring revenue from spare parts, upgrades, and services. TOELF generated nearly a quarter of its revenue from services that depend on the installed base rather than new equipment sales, offering some cushion against cyclicality.

Tokyo Electron

Still, when assessing TOELF's valuation, it seems fairly priced and in line with peers. For example, assuming EPS rebound in 2024, reaching the 2022 and 2023 peaks of $7 per share, TOELF's FWD PE ratio would stand at 21x, compared to AMAT's 18x. These figures are high for a cyclical company, even on an absolute basis.

{kind=link}

Over the long term, management expects 3 trillion yen ($19 billion) of sales in 2027, translating to an 8% annual growth in line with the industry average. The recent breakthrough in 3D NAND etching could lead TOELF to gain market share from current market leader Lam Research.

Assuming a net income margin of 30%, the projected net income is $6 billion. This, along with a 5% decline in outstanding shares from 471.6 million to 447 million, translates to an EPS of $13 and a 2027 PE ratio of 11x. Considering the company's financial projections, our Buy rating is grounded on this long-term outlook.

Summary

Investing in TOELF offers distinct advantages for a diversified portfolio. The WFE industry is more stable compared to other segments of the semiconductor sector, marked by high barriers to entry and long-term customer relations centered around R&D initiatives aiming at enhancing the semiconductor chip manufacturing process. TOELF also adds a layer of geographical diversification, benefiting from the Tokyo Stock Exchange 'TSE's recent strong performance.

TOELF is also well aligned with the anticipated upswing in the memory semiconductor chip market. Most notably, TOELF's breakthrough in 3D NAND flash memory etching technology sets the stage for potential market share gains in a critical segment of the semiconductor industry.

This blend of market stability and leading industry position in a growing sector makes TOELF an appealing prospect for a semiconductor-focused investment strategy.

For further details see:

Tokyo Electron: Attractive Prospect In Anticipated WFE Market Rebound