V - Top 3 Dividend Growth Companies You Must Have In Your Portfolio

2024-01-11 08:00:00 ET

Summary

- Dividend investing should focus on companies with quality and growing free cash flow, rather than just high dividend yields.

- Alibaba, despite concerns and regulatory issues, is still a strong Chinese company with potential for dividend growth and capital gains.

- Evolution Gaming, a Swedish company in the gaming industry, has impressive financials and has been increasing its dividend at a high rate.

- Visa is a well-known company that has shown incredible growth in free cash flow and revenues.

The first thing that catches our eye when we look at a dividend company is its yield: the higher the better.

However, too high a dividend yield may hide pitfalls and is not the best way to create wealth over the long term. My impression is that the dividend is often seen as a separate entity from the company itself that issues it, which is absolutely wrong. If the profits of the company in question do not increase, forget about your dividend.

The crucial aspect of dividend investing lies in choosing companies with quality and growing free cash flow, because that is where future dividend growth will come from. By investing for a long time in such a company, over the course of 5-10 years the dividend on cost you will get may be surprising. Imagine after 20-30 years.

Just think that Warren Buffett, with his purchase of Coca-Cola in 1988, today gets a dividend yield on cost of 54%. Basically, every year he gets half of his initial investment in dividends.

3rd place: Alibaba

You have probably already closed my article after reading that I included Alibaba in third place. The pessimism found toward this company has peaked and many believe it is 'uninvestable' regardless of its fundamentals.

I do not doubt that investing in a Chinese company carries significant risks in terms of the political aspect, far greater than in a Western company. In any case, I don't think destroying Alibaba ( BABA ) pleases anyone, not even the CCP. After all, along with Tencent ( OTCPK:TCEHY ), these are two of the best Chinese companies and among the best in the world.

Contrary to what you might think, despite the fine and the freezing of Ant Group's IPO, Alibaba is by no means dead.

{kind=link}

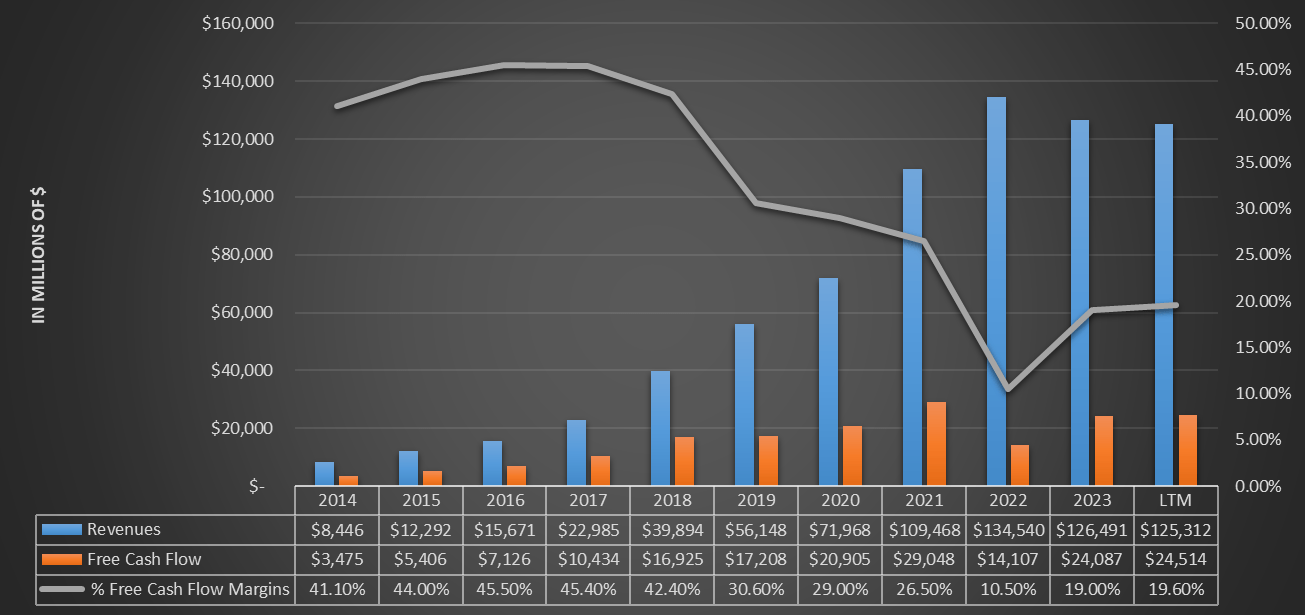

The golden period was FY2021, but what was achieved in subsequent years is not to be underestimated. In the past 12 months the company generated free cash flow of $24.51 billion, up from the disappointing FY2022 and FY2023. In addition to government-imposed restrictions, there was a pandemic in the middle and social norms in China have been very stringent until recently. Overall, Alibaba was resilient and came through a very complicated period without too much damage; today it is returning to growth.

The free cash flow margin was much higher in the past because Alibaba was not involved in as many projects as it is today. In any case, among management's goals is to sell the less profitable operating segments and focus more on those where there is a strong competitive advantage. The result is already evident, in fact the free cash flow margin has risen again in the last three years and is about to exceed 20%.

Now we come to dividends.

This month is the first time Alibaba has issued a dividend, so it is perhaps premature to talk about it as a dividend growth company. Anyway, the gap between free cash flow per share and dividend per share is huge, which is why I think Alibaba has a significant dividend growth margin. Suffice it to say that in the last 12 months the FCF per share has been $9.66, while the dividend per share is only $1. The current dividend yield is 1.41%.

I expect management to be able to increase the dividend per share considerably in the coming years, as it would incentivize even the most pessimistic people to invest in Alibaba. After all, dividend money is real and there's little to discuss, so this could help improve the company's reputation. China or no China, when your investment starts to pay off something is psychologically less stressful to keep it in the portfolio. Recovering the capital loss may take years, but in the meantime shareholders will get their first dividend. But there is more.

Beyond future earnings growth, one way to increase the dividend per share is logically to decrease the shares outstanding: this is exactly what Alibaba is doing.

The buyback has reached huge numbers and is not about to stop. Throughout 2023, Alibaba bought back $9.5 billion worth of shares. As of today, there is about $11.70 billion still available until March 2025. In short, management is serious about the buyback and this will bring a boost to both EPS and dividends per share.

Finally, the effectiveness of this buyback cannot be overlooked. At $72 per share Alibaba is severely undervalued in my view; its NTM levered free cash flow yield is 13.10%. By spending billions on the buyback now, the company will be able to buy a huge amount of outstanding shares.

As of December 31, Alibaba owned about 20 billion common shares, or 2.53 billion American depositary shares ADS (1 ADR is worth 8 common shares traded in Hong Kong). If the price per share remains around $70 for the next few months and all the remaining $11.70 billion of the buyback plan is used, the outstanding shares would become 2.36 billion, almost 7% less. This means that with the same amount of dividend paid out to shareholders, the dividend per share would increase to $1.072, about 7% more. If the company then decided to increase the amount of the dividend even slightly, the growth would almost certainly reach double digits. Personally, at least for the next few years, I expect the dividend to experience strong growth to attract as many investors as possible.

Be that as it may, in addition to the possibility of receiving an increasing dividend, the potential for capital gains with Alibaba is considerable given the current undervaluation.

2nd: Evolution Gaming

Evolution ( OTCPK:EVVTY ) is a Swedish company that I have covered several times on Seeking Alpha but I will briefly summarize what it is about since not everyone is familiar with it.

{kind=link}

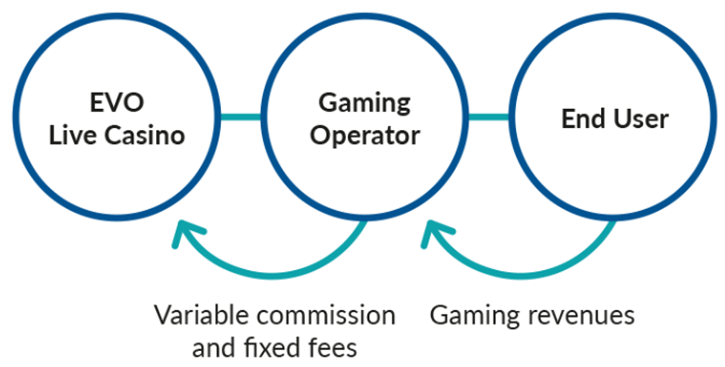

Evolution creates the live casino games used by major gaming operators around the world ( PokerStars, William Hill , and Sisal for example). Evolution's profit lies not in bets lost by bettors but in fixed and variable commissions from gaming operators. Although many of you are not familiar with Evolution, you have most likely heard of its main games: Crazy Time and Lightning Blackjack .

The financials of this company are impressive:

- Last 3-Yr Rev CAGR 58.5%

- Last 3-Yr EPS CAGR 67.2%

- Negative net debt

- Free cash flow margin 61.60%

Its games are able to keep bettors glued to the screen for hours and gaming operators around the world cannot avoid Evolution if they want to make their platforms competitive. Besides the cozy atmosphere, the secret of Evolution's games is to give a false control to the bettor because of the high RTP.

RTP stands for Return to Player and indicates how much a bettor expects to earn in a given casino game. In the case of land-based casinos, the RTP is between 70% and 90%, which means that out of $100 played the average bettor will receive between $70 and $90.

{kind=link}

In the case of Evolution, its games have an RTP often exceeding 99%, which makes the gaming experience quite long-lasting. The bettor may experience a series of wins and believe he/she has found a way to make money, but after hours of play he/she will lose it all. This diabolical mechanism fuels addiction and thus the coffers of Evolution.

It is clear that this company is part of the sin stocks group, so not everyone is willing to invest in it. The main risk concerns the regulation of gambling, an ongoing plague on our society.

{kind=link}

With such financial results, this company has increased the dividend at an insane rate: 5-Yr CAGR 50.86%. Obviously, this CAGR is not sustainable over the long term, so it will tend to fall over time; in fact, the first slowdown is already evident. Anyway, this does not mean that the company is no longer interested in increasing the dividend, on the contrary.

The board of Evolution Gaming Group AB has adopted a dividend policy whereby the company will distribute a minimum dividend of 50% of net income each year. This means that as EPS increases, an increase in dividend per share will necessarily follow. Obviously, in downturns in growth this could mean an unstable dividend, but in the long term I expect Evolution to be able to return to growth and with it the dividend. Its live casinos are still in high demand, and the company is becoming increasingly well-known internationally. It is also gradually entering new regulated markets such as the United States. The potential is high, but it will take a while since it will have to comply with each state's gambling regulations.

Finally, there will be no shortage of buybacks here either. As of November 27 to date, 1.39 million shares have been bought back; a total of 19.85 million shares can be bought back, about 10% of the outstanding shares.

Currently Evolution is not that expensive compared to its potential: the NTM Market Cap/Free Cash Flow is 19.49x. The dividend yield is 2.50%.

1st Place: Visa

Alibaba and Evolution, although dominant in their field, are two companies that have great potential but rather high risks. In the first case we have the Chinese government with the constant regulations, on the other we have an impressive company operating in a questionable market. In contrast, in the case of Visa ( V ) we have a flawless company operating in a market driven by a secular trend: the gradual transformation to a cashless world. I may be biased, but Visa in my opinion is one of the best companies in the world.

{kind=link}

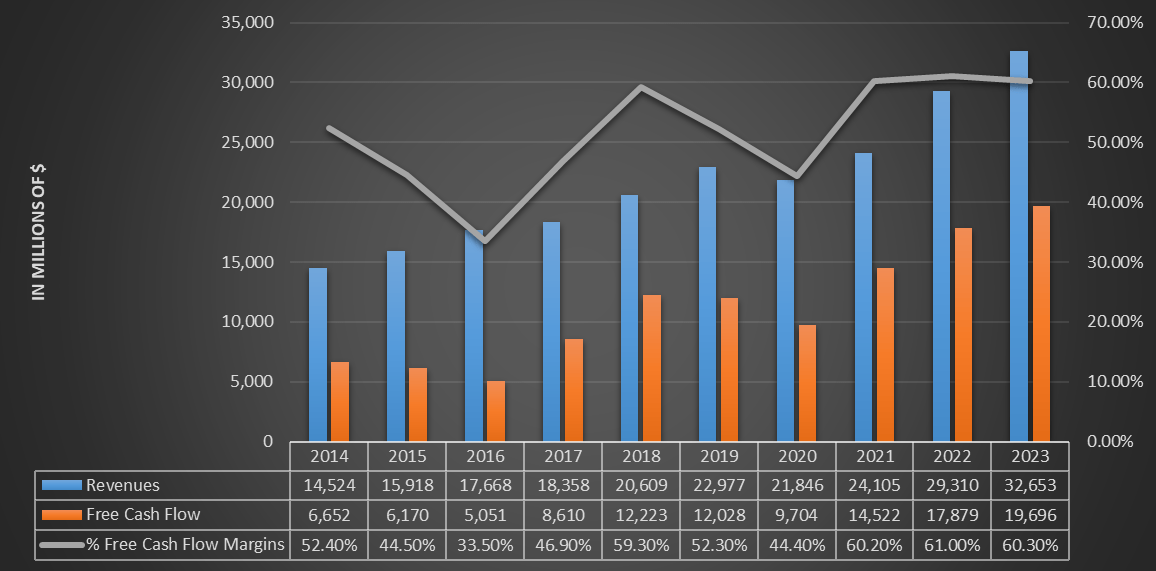

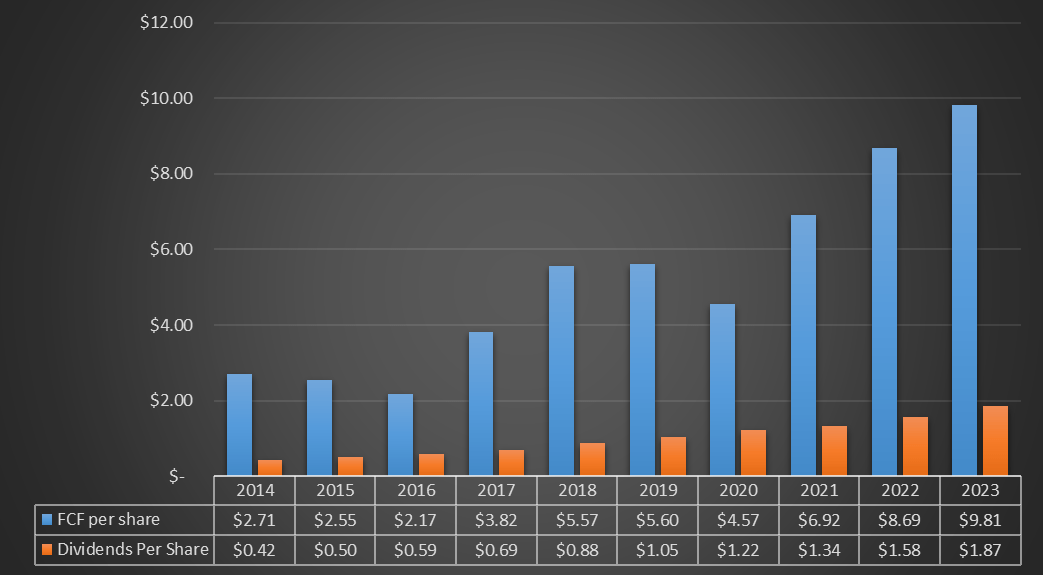

Steadily growing revenues, followed by equally growing free cash flow. The FCF margin was already huge in 2014, but management has managed to increase it even more and today it has reached 60.30%. Visa's structure based on fixed rather than variable costs allows it to scale its business exceptionally well. So, I would not rule out further improvement in the future.

{kind=link}

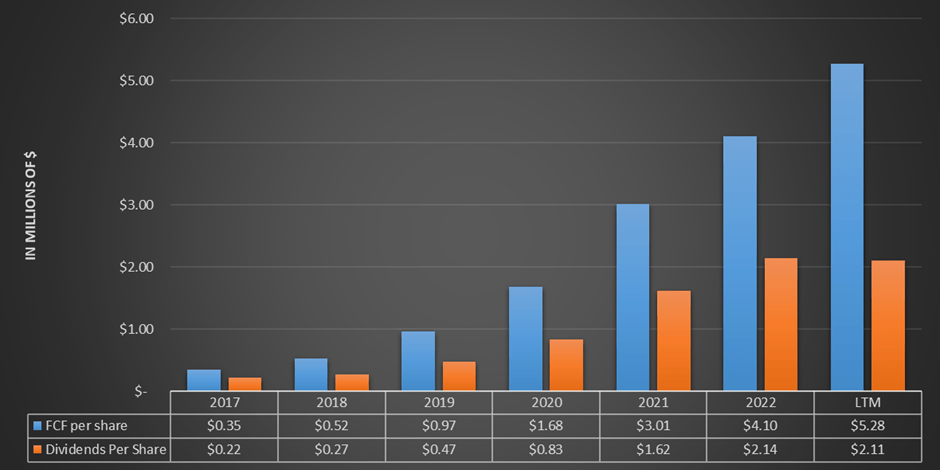

The growth in FCF per share has largely covered the growth in dividend per share. However, one shouldn't underestimate the latter.

{kind=link}

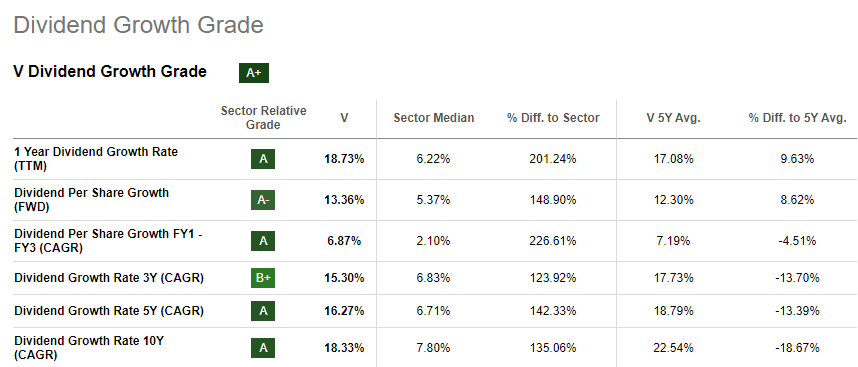

Dividends increased at a 10Y CAGR of 18.33%, which is well above the sector median. The current dividend yield is quite low, 0.71%, but if it maintains this growth rate, the future dividend yield on cost will be interesting. After all, even getting 3-4% per year will be a great result given Visa's low dividend riskiness.

In addition, Visa has a history of reducing its outstanding shares by a great deal over the years. Since September 2014, outstanding shares have decreased by 18.30%, about 2.22% per year.

Although the price per share has increased quite a bit in 2023, Visa remains in my opinion well-priced to invest in. The NTM Market Cap/Free Cash Flow is 26.06x, which is quite high but is justified in Visa's case: you have to pay a premium to have such a company in your portfolio. After all, Visa has never traded at low multiples and still performed excellently: +409.20% versus 280.40% for the S&P 500 ( SP500 ).

Conclusion

Alibaba, Evolution and Visa are three companies that I have in my portfolio and they have three key aspects in common:

- They have a significant competitive advantage in their market.

- They have increasing free cash flow over the long term and a high FCF margin.

- The dividend yield is not very high but has the potential to grow a lot.

Of the three, the one that gives me the most confidence is obviously Visa, both because of its history and prospects for growth in digital payments. Evolution was born in 2006 and is still in its infancy despite already capitalizing about $24 billion: it still has a lot to prove. Finally, Alibaba has the potential to generate huge capital gains but is still held back by widespread fear of new regulation.

For further details see:

Top 3 Dividend Growth Companies You Must Have In Your Portfolio