DHCNL - Top Insider Picks June 2023

2023-07-13 08:30:00 ET

Summary

- June 2023 saw significant insider purchases in Lucid Group, Diversified Healthcare Trust, Akoya Biosciences, and Axon Enterprise. The Public Investment Fund bought $1.8 billion worth of shares in Lucid Group, increasing its ownership to 74.95%.

- Diversified Healthcare Trust's proposed merger with Office Properties Income Trust is facing opposition from major investor Flat Footed LLC, which argues the deal undervalues DHC and benefits RMR Group Inc unfairly.

- In this article, we discuss the most interesting insider purchases by value. In addition, we will take a look into 2 companies more in-depth, which we found particularly interesting.

- We will delve more deeply into DHC and AKYA as they were two share purchases that caught our attention.

Introduction

June was an interesting month for insider purchases as multiple companies had some major insider action. In this series, we will take a look at some of the biggest insider purchases over the last month and we will discuss one or 2 of the biggest purchases in more detail.

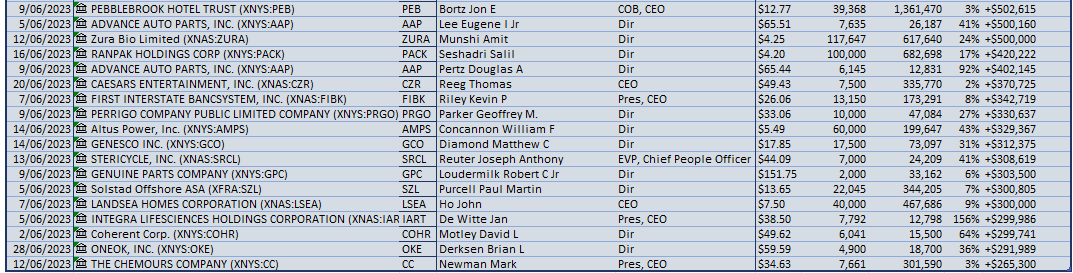

Top Insider Buys June 2023

Below you can find a list of the most valuable insider purchases for June.

{kind=link}

{kind=link}

Now let's take a look at 4 of the biggest insider purchases of June 2023.

Lucid Group ( LCID ) , saw a big insider purchase by the "Public Investment Fund", which bought $1.8 billion worth of shares. This increased his ownership in the company by over 24%, with the Public Investment Fund now holding 74.95% of all the shares. Recently the stock has been on a tear, increasing 34% just this month, as EV companies and high-beta stocks and general have been hot.

Director Adam Portnoy of Diversified Healthcare Trust ( DHC ) recently added 17,545,359 shares for a combined price of $42,464,050, which increased his ownership in the company by over 195%.

DHC is a real estate investment trust ((REIT)) primarily focusing on investing in healthcare-related properties. It was formerly known as Senior Housing Properties Trust (SNH) and changed its name to Diversified Healthcare Trust in 2020 to reflect its expanded investment strategy beyond senior housing.

Akoya Biosciences ( AKYA ) promotes itself as "The Spatial Biology Company". Akoya tries to allow scientists to see how human cells function inside the space of a human body. Recently director Thomas A. Raffin bought $10.10 million worth of shares, increasing his stake in the company by 14%. Currently, the stock has a $335.00 million market cap, this unprofitable biotech company still has lots to prove and is certainly a risky investment.

Axon Enterprise ( AXON ) previously named Taser International is a technology company that focuses on providing law enforcement agencies with innovative solutions to enhance public safety. They are known for their development and provision of advanced hardware, software, and services specifically designed for law enforcement and public safety professionals. Recently director Hadi Partovi bought an additional 25k shares or close to $4.78M worth of shares, which increased his position by 6%. Axon is a quality company, but currently trading at quite a hefty valuation.

Top Insider Purchases: DHC and AKYA

Diversified Healthcare Trust ((DHC))

Diversified Healthcare Trust ((DHC)) is a real estate investment trust ((REIT)) primarily focusing on investing in healthcare-related properties. It was formerly known as Senior Housing Properties Trust (SNH) and changed its name to Diversified Healthcare Trust in 2020 to reflect its expanded investment strategy beyond senior housing.

Today, DHC's portfolio includes diverse healthcare real estate assets, such as medical office buildings, hospitals, skilled nursing- and life science facilities, as well as other properties. The company aims to generate rental income and capital appreciation by leasing these properties to healthcare operators and providers.

As a REIT, DHC must pay a significant portion of its taxable income to shareholders as dividends, which is where this stock gets its attractiveness. In addition, DHC has gathered attention from recent news of a merger with Office Properties Income Trust ( OPI ). The merger has not been well received by DHC's shareholders, which has caused the stock to fluctuate strongly throughout the year.

For instance, Flat Footed LLC, a major investor in DHC, is against the planned OPI merger. The investor, which owns 7.4% of DHC, claims that the deal greatly underrates DHC by about 90%. Flat Footed wrote a letter to DHC's board of trustees, saying that the merger is a "take-under" for DHC shareholders. They argued it would be a poor business decision to merge with a company that manages office properties when working from home is common nowadays. Flat Footed advised the board to look for other strategic options and intends to vote no to the merger at the special meeting.

The merger of OPI and DHC was initially revealed in April to create a more substantial company ready for growth. The deal states that DHC shareholders would get 0.147 shares of OPI common stock for each DHC share, which means a value of $1.70 per common share on the day of the reveal. However, Flat Footed LLC argued that DHC's portfolio should be worth $5 billion, with the stock price ranging from $9 to $10 per share. DHC's stock ended trading at $1.05 on the day in April, showing a 15% drop as the merger was revealed.

Flat Footed's letter also slammed OPI, calling it a troubled REIT made up of failing single-tenant commercial office properties. They expressed worry that the newly merged company would favor RMR Group Inc, which would keep managing the assets. Flat Footed stated that RMR Group would get unfair benefits from the merger by having the chance to increase its fees.

DHC still needs to answer the issues brought up by Flat Footed LLC. The outcome of the merger and the next steps will depend on the views of other investors and the actions taken by DHC's board of trustees. Investors should be wary of this conflict between DHC and other major shareholders before starting a new position.

Looking at DHC's financials gives an idea why Flat footed believes the initial offer from OPI does not meet their expectations. Despite DHC's poor gross margins, they have maintained revenues relatively constant since 2016. The attractiveness, however, lies in the extensive portfolio DHC possesses, which, unfortunately, has not been able to generate a positive cash flow since 2020. This is most likely due to the challenging economic climate for the past year and a half. The sheer size of the insider purchases could signal a strong belief that the profitability of DHC will turn positive soon.

{kind=link}

Historically, DHC has generated positive free cash flow while maintaining an operating margin of close to 30%. Investors would want to see the poor free cash flow the company has had for the past three years begin to improve. In addition, the operating income has remained negative for some time, and a turn to positive numbers is warranted.

{kind=link}

With that said, should DHC find a merger deal that would bring the stock price to the $9 - $10 level, it would mean an almost 500% upside relative to the stock's current price. It seems very unlikely that such a deal would materialize; however, as mentioned earlier, Flat Footed LLC believes it is feasible. This remains to be seen as negotiations with OPI and others continue.

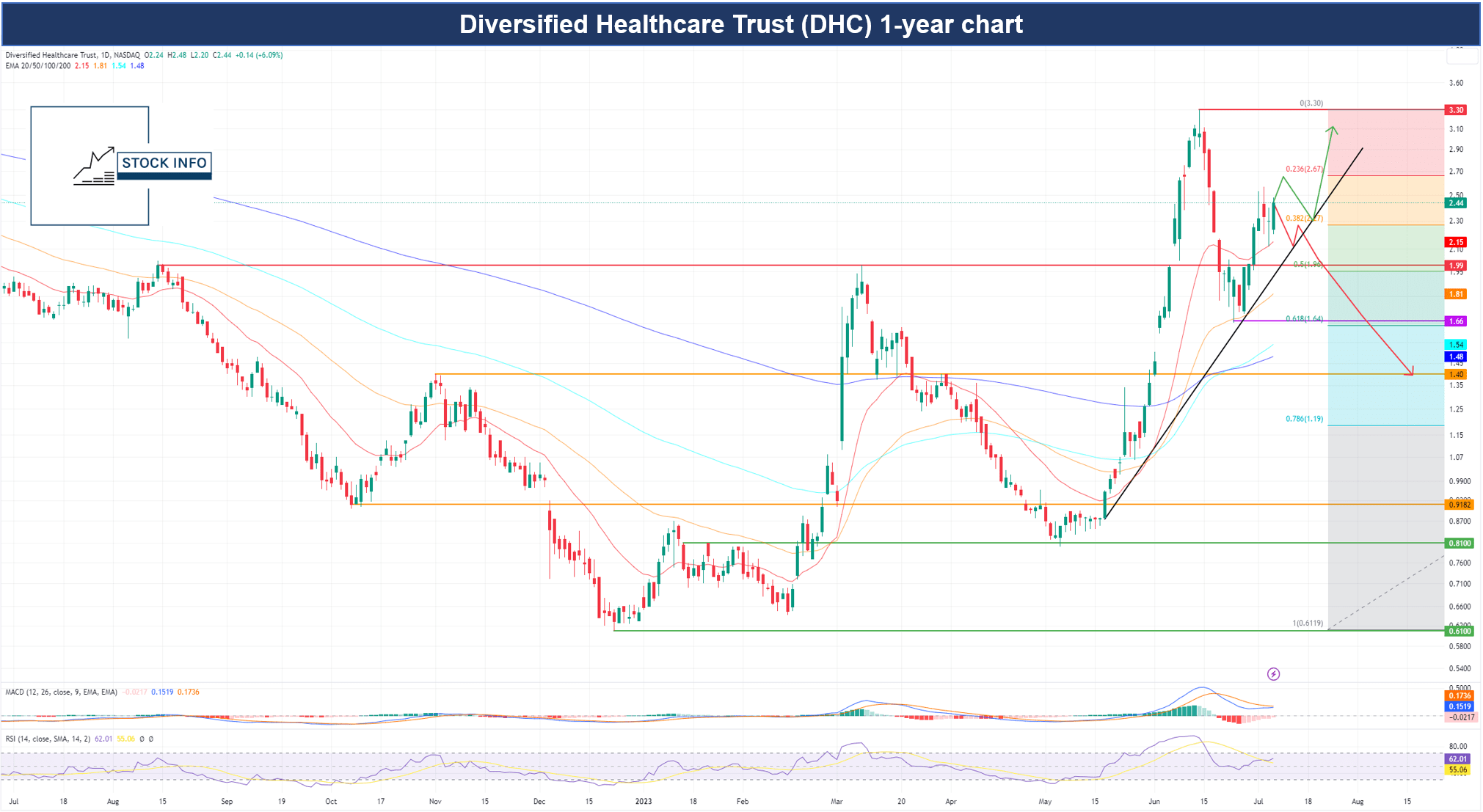

DHC Technicals

As can be seen in the graph below, the stock has had major down- and upswings in the past year.

The blistering move to the upside in mid-May torpedoed the stock above all major EMAs, where it has been sitting comfortably ever since.

Most recently, the stock bounced off the 50 EMA at $1.66 and then through a critical resistance at $1.99. The stock currently trades along a steep trendline, which it will need to hold to continue up towards the $9 level as Flat Footed LLC believes it should be valued at in a potential merger.

Most importantly, if the stock continues to move to the upside, it will need to break $3.30, which is a significant local high - there are potentially many sellers waiting at this price.

If the stock breaks the trendline to the downside, the stock price could likely slide as it did in March and April of this year. In this case, we would most likely see an eventual retest of $1.40. However, the sizeable inside purchases suggest that their director believes a move to the downside will not be the case.

An important indicator is the MACD, which is on the verge of printing a cross to the upside, signaling bullish momentum for the stock. We saw the opposite cross happen back in mid-March, resulting in a major move to the downside.

We advise investors to be aware of which print we get on the MACD in the following days, as this can have big implications for which direction the stock moves. The RSI sits in slightly oversold territory; however, historically, this stock can make big moves to the upside even in this RSI territory.

{kind=link}

Akoya Biosciences, Inc. ((AKYA))

Akoya Biosciences, Inc. ((AKYA)) is a company that provides spatial biology solutions for life science research and clinical diagnostics. Their goal is to enable the development of more precise therapies for immuno-oncology and other drug development applications.

The company offers platforms and reagents that will allow researchers to study the spatial relationships of biomolecules in cells and tissues. AKYA's product line includes CODEX, Phenoptics, Vectra Polaris systems, and other consumable drugs and software. Their primary customers are academic institutions, pharmaceutical companies, and other contract research companies.

AKYA had an inspiring start to 2023, as on January 6, the company announced a partnership with Agilent Technologies ( A ), a global leader in life sciences and diagnostics.

The partnership will combine Agilent's Dako Omnis, an autostaining instrument, with Akoya's PhenoImager HT, a high-throughput multiplex immunofluorescence imaging system. The resulting product offers bioscience researchers a complete solution for single-cell multiplex tissue analysis, including reagents, staining, imaging, and research.

Akoya Biosciences will also distribute and resell Dako Omnis, an Agilent product, under a Value-Added Reseller agreement. This will, in turn, expand AKYA's reach to Agilent's extensive and diverse customer base in 110 countries.

Agilent could be an ideal partner for AKYA, as it already has a strong presence and reputation and could help bring AKYA's product to the forefront of the market. Despite the partnership, the stock is down approximately 27% YTD.

Looking at AKYA's financials, it appears to be a relatively healthy business based on its topline. They have had steady revenue growth for the past five years.

However, their gross margin has slightly dipped in the past year and TTM. Their revenue has grown at a 5-CAGR rate of 13.5% from 2019 to the TTM period, which is nothing to shy away from - it is very satisfactory.

{kind=link}

While their top line has grown, their free cash flow and operations have significantly dipped. AKYA is still a relatively young company, so, naturally, they would have periods with worsening bottom lines.

Their FCF, as well as operating income, has especially suffered since 2019. The reasoning behind the insider purchases could therefore be a sign that the financials are starting to turn the other way. The inside purchases had their filing day on June 12th, and the stock soared the following days.

{kind=link}

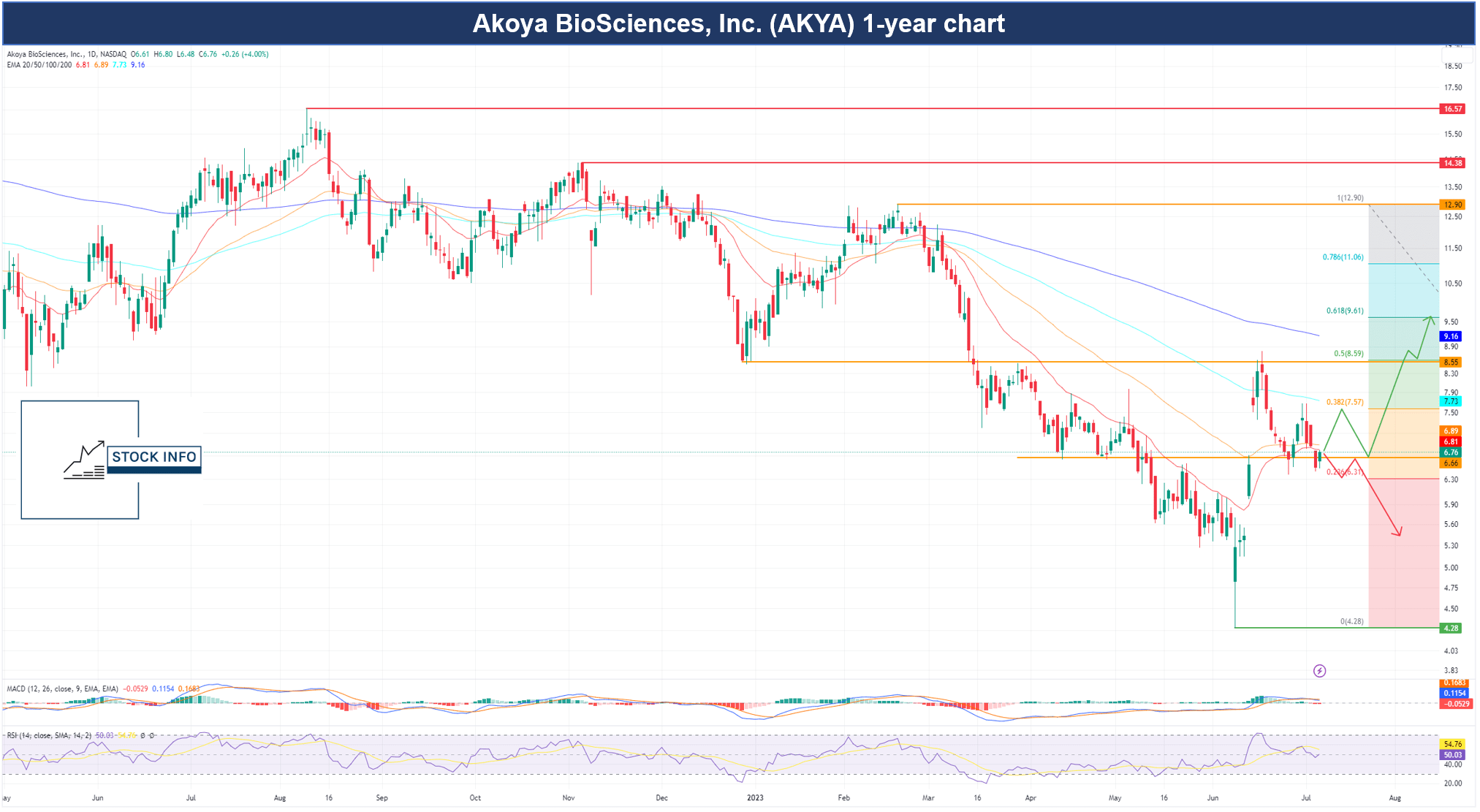

AKYA Technicals

Looking at the technicals of AKYA's stock price, it shows a significant jump in price following the insider purchases in the middle of June. The stock broke through the $6.66 mark, which was a level of support in April, but was eventually lost in May - this level was then revisited following the insider purchases and broke through it.

The December 2022 lows then became the next resistance level at $8.55. The stock has since then touched the $6.66 level twice in the past couple of weeks, which could be a set-off point for the stock.

It is worth noting that the 20 EMA is close to crossing the 50 EMA, which could signal momentum to the upside. The stock is still, however, sitting well below both the 100 EMA and the 200 EMA - two critical levels the stock needs to break through to establish a solid uptrend.

In addition, the MACD has not fully shown a downward crossing on the daily chart, and thus the following days of trading will be pivotal for whether or not it entirely crosses to the downside. The RSI is currently close to 50, indicating a neutral relative price for the stock.

As we see it, there are two possibilities for AKYA. If the stock cannot break through and hold $6.66, it could mean a sizable swing to the downside, most likely testing $4.28 again. The stock would likely test the 0.382 fib number at $7.57 if it can hold.

As indicated in the graph below, the stock could bounce from here or break through and test the 100 EMA. Either way, we believe now is a crucial time to pay attention to AKYA. The director most likely thinks the stock will move to the upside based on the inside purchases.

{kind=link}

Conclusion

In conclusion, the planned merger between OPI and DHC is facing opposition from Flat Footed LLC, a major investor in DHC. Flat Footed argues that the deal undervalues DHC significantly and criticizes OPI's troubled REIT status. They express concern about potential unfair benefits for RMR Group Inc.

The outcome of the merger and the resolution of these issues depend on the actions taken by DHC's board of trustees and the views of other investors.

Meanwhile, DHC's financials show poor gross margins and a lack of positive cash flow, but significant insider purchases suggest a belief in future profitability. Investors should consider the ongoing conflict before making investment decisions.

Shifting focus to Akoya Biosciences, the company has experienced revenue growth over the past five years and recently announced a partnership with Agilent Technologies.

Despite this, AKYA's stock is down approximately 27% YTD. While their financials show steady revenue growth, their free cash flow and operations have dipped, possibly prompting insider purchases as a sign of turning financials.

Technical analysis suggests the stock is currently at an inflection point, where the price movement in the coming days can indicate a longer-term trend for the stock.

Overall, both DHC and AKYA present investment considerations, with the merger's outcome and each company's financial performance being important catalysts to monitor.

For further details see:

Top Insider Picks June 2023