COOK - Traeger: The Picture Is Warming Up

2024-01-05 16:54:26 ET

Summary

- Traeger, a company that produces grills and cooking appliances, has experienced a drop in price while the S&P 500 has risen.

- The company has seen improvements in its net loss and gross profit margin, but revenue has continued to decline until very recently.

- Despite some positive signs, the company is still facing risks and it is not yet a favorable investment opportunity.

- But if the picture continues to improve, this situation could change.

As far as food goes, there is very little in this world that beats a good piece of meat cooked over a hot, steaming grill. If you have ever wondered which companies produce these appliances, look no further. One business dedicated to producing these, particularly ones that use natural hardwoods and even electricity for the purpose of grilling, smoking, and cooking in other ways, whatever pleases your palette, is Traeger ( COOK ). Back in August of 2022, I found myself revisiting Traeger after previously rating it a ‘hold’. While I had hoped that the company might be worth buying into, I found that it was dealing with fundamental deterioration. Even though shares were looking fairly attractively priced, that deterioration was enough to offset any potential upside the company might offer. This led me to keep the company rated a ‘hold’.

But even that, unfortunately, ended up being too bullish. Since the publication of that article, shares have dropped 12.5% at a time when the S&P 500 has jumped 13.6%. Fast forward to today, and we are starting to see some major improvements on both the top and bottom line. But until the company truly recovers and can grow out of some of its issues, I believe that it is still too risky to warrant any significant degree of optimism.

The picture is improving at last

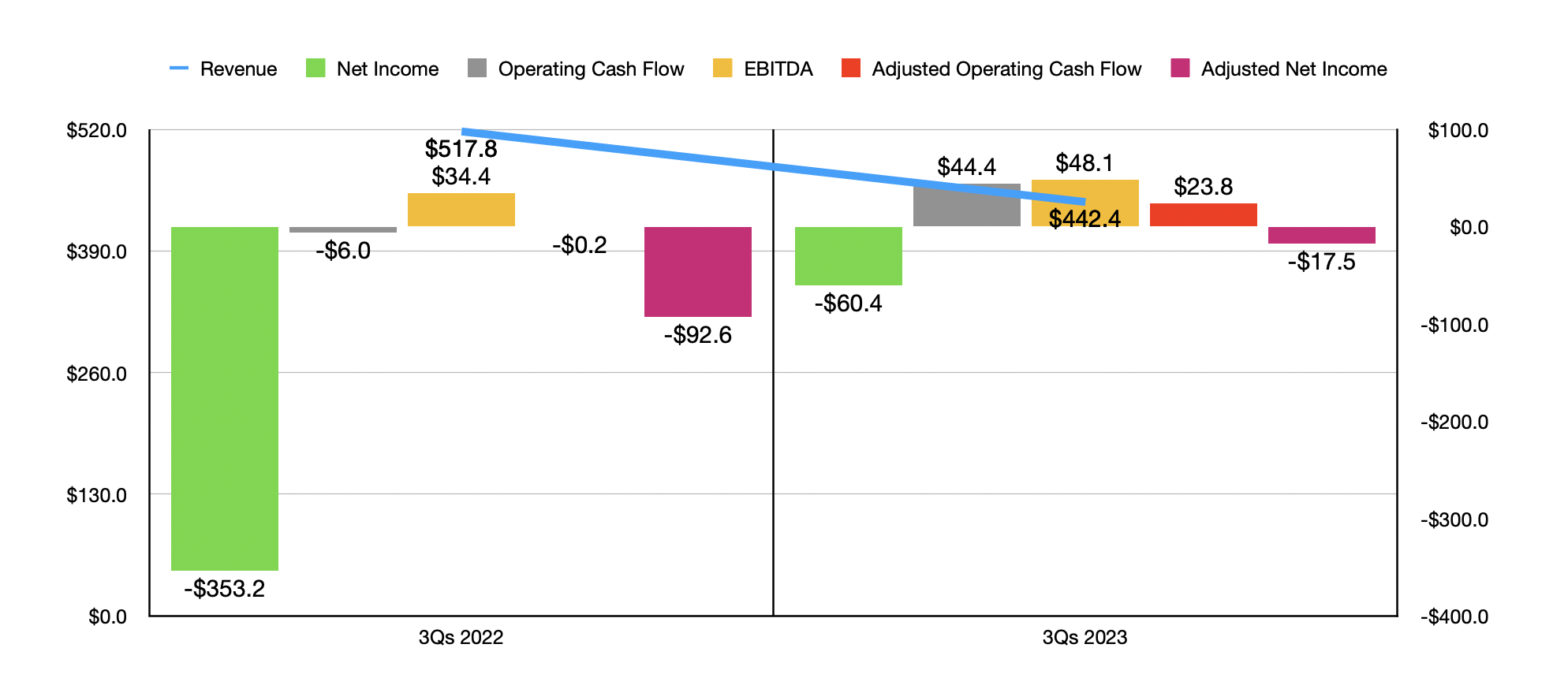

When analyzing a company, it's important to look at it through the lens of multiple points in time. It's only by doing this that you start to see how the picture is changing. For instance, if you look at the first nine months of the 2023 fiscal year compared to the first nine months of 2022, you would see that revenue for Traeger has continued to take a hit. Sales of $442.4 million came in 14.6% lower than the $517.8 million the company reported the same time one year earlier. Even though accessories revenue for the company rose 8.5% year over year, grill related revenue plunged 22%, while consumables sales dropped 15.5%. For the grills, the drop in sales was driven largely by a mid-double-digit percentage plunge in unit volume, even as the company dealt with a high single digit percentage decline in average selling price. Consumables revenue, meanwhile, dropped because of the same magnitude of decline in unit volume and a low single digit percentage reduction in average selling price.

{kind=link}

Author - SEC EDGAR Data

Even though the revenue picture for the company took a hit, there were some positive signs. The company’s net loss, for instance, went from $353.2 million in 2022 to $60.4 million last year. Most of this improvement was driven by a reduction in impairment charges. However, the firm also reported some meaningful margin improvement. Gross profit margin rose from 35% to 36.9%, thanks largely to reduced costs associated with freight, foreign currency fluctuations, and a reduction in restructuring expenses. Sales and marketing costs, meanwhile, went from 19.8% of sales to 17.2%. Management chalked this up to a drop in advertising costs, commissions, and other employee related expenses. Travel costs and professional fees also declined by an unspecified amount. And lastly, general and administrative costs dropped from 27.5% of revenue to 23.5%. This was thanks mostly to a $33.4 million drop in stock-based compensation because of a large chunk of compensation that was accelerated last year.

This improvement in profits brought with it an improvement in other profitability metrics. The company went from generating operating cash flow of negative $6 million to a positive of $44.4 million. On an adjusted basis that ignores changes in working capital, we would see an improvement from negative $0.2 million to positive $23.8 million. The company's adjusted net loss went from $92.6 million to $17.5 million. And lastly, EBITDA increased from $34.4 million to $48.1 million.

{kind=link}

Author - SEC EDGAR Data

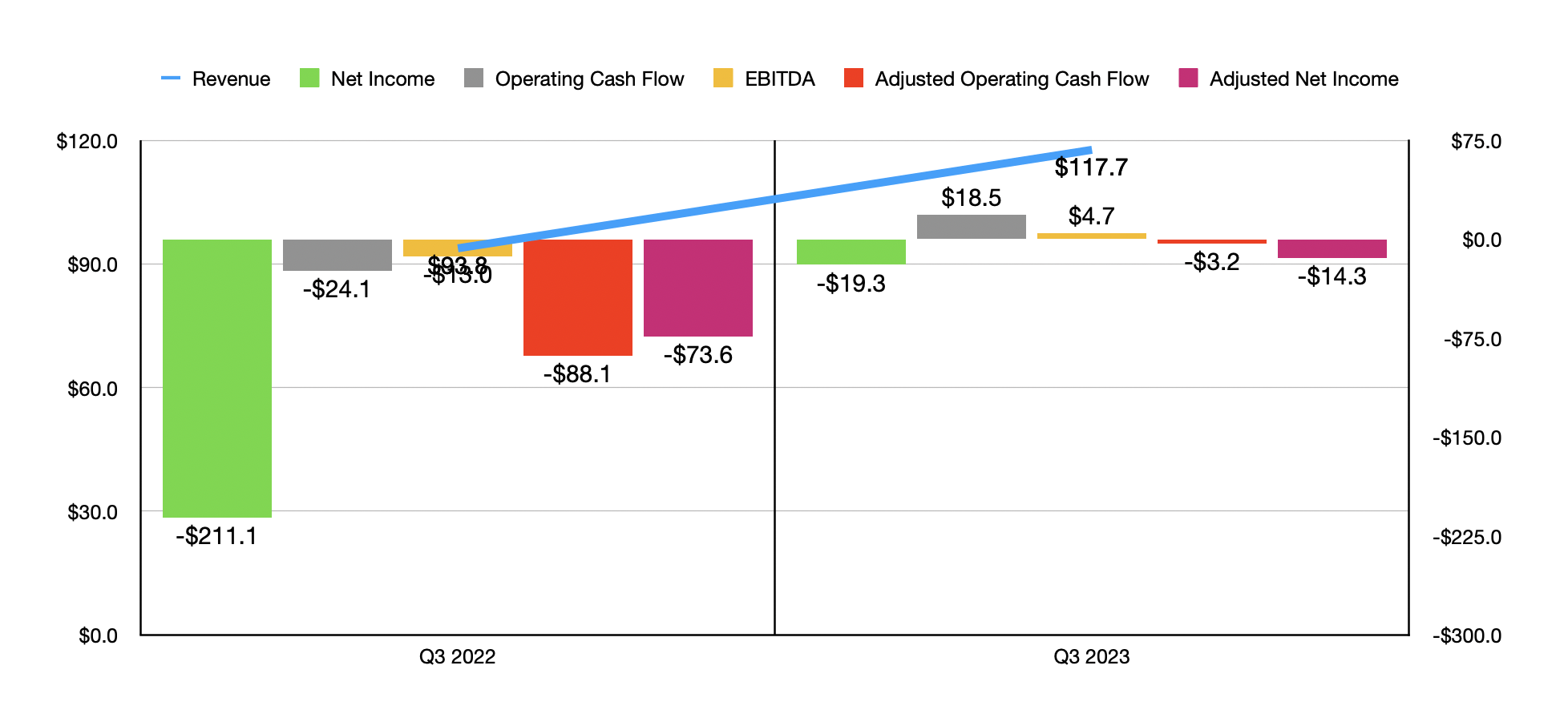

As you can see in the chart above, those same types of margin improvements played a role in the much-improved bottom line for the third quarter of 2023 on its own relative to the same quarter one year earlier. But what really shows an improvement for the company outside of this is revenue. During the third quarter, revenue totaled $117.7 million. That's 25.5% higher than the $93.8 million reported one year earlier. Although consumables revenue inched up only modestly by $0.9 million, accessories revenue jumped 20.7%. The big winner, however, was grill related revenue. Sales of $56.6 million came in 45.1% higher than the $39 million reported the same time of 2022. A boost in sales associated with grills and the company’s MEATER smart thermometers helped tremendously. Digging deeper, we find that the firm benefited to the tune of a more than 60% rise in unit volumes as inventory destocking of its customers back in 2022, combined with the introduction of new products and price cuts, led to a shortage of the product with the firm’s customers.

{kind=link}

Author - SEC EDGAR Data

More likely than not, this is a trend that will continue to some extent. I say this because, at the start of this year, management forecasted revenue for 2023 of between $560 million and $590 million. That's down from the $655.9 million reported one year earlier. The most recent guidance offered up by management now calls for revenue for 2023 of between $590 million and $600 million. And it's not just the top line that's improving. The bottom line should continue to improve as well. As an example, EBITDA is now forecasted to be between $57 million and $59 million. That's up from prior guidance of between $45 million and $55 million. And it also compares favorably to the $41.5 million reported for 2022.

{kind=link}

Author - SEC EDGAR Data

Unfortunately, no estimates were provided for other profitability metrics. Sadly, operating cash flow will probably come in low. And that's because of a rise in interest expense for the business. I forecast a reading of about $27.1 million for the year. If we use my same modified estimate for 2022, that year would get us a reading of $13.6 million. In the chart above, you can see how this all prices the company for both 2022 and 2023. On a forward basis, shares are starting to look a bit attractive. However, when you consider that revenue should still be lower year over year and that profits and some cash flow estimates are still in negative territory, it's difficult to get terribly excited. Add on top of this the fact that even achieving midpoint guidance for 2023 would result in a net leverage ratio of 7.28, and shares are not yet cheap enough for me to consider it a great prospect.

Takeaway

Fundamentally speaking, there is no denying that Traeger is showing some great signs when it comes to improving. The company has successfully cut costs, in large part thanks to a 14% reduction in headcount. It has also taken other initiatives to reduce unnecessary expenditures, such as suspending certain operations. The stock finally looks reasonably priced, though that would only be the case for a healthy operator. If shares were trading at multiples around half of what they currently are, I would consider this an appealing opportunity. But until the picture changes further, I plan to sit on the sideline and keep the business rated a ‘hold’.

For further details see:

Traeger: The Picture Is Warming Up