TPVG - Trinity Capital's Outperformance Is Likely To Continue In 2024 Against TriplePoint And S&P 500 (Rating Downgrade)

2024-01-11 07:44:34 ET

Summary

- Trinity Capital is well-positioned to offer healthy returns to shareholders in 2024 due to its diversified portfolio and high asset quality.

- TriplePoint's high accruals and declining portfolio value may hinder its performance.

- The private credit market is expected to rebound significantly in 2024, benefiting BDCs like Trinity Capital.

In my article in late 2022, I suggested investors prefer Trinity Capital (TRIN) over TriplePoint Venture Growth (TPVG) for higher returns. TRIN's 60% total return in 2023 vindicated my opinion. For 2024, I believe Trinity is well-positioned to offer healthy returns to shareholders. TRIN's performance in 2024 is likely to be supported by its diversified portfolio and high asset quality. Additionally, the robust private credit market growth outlook will improve its portfolio activity, helping offset the rate cut impact.

Private Market Growth Support BDCs Upside

Despite the risk of recession and defaults from regional banks, BDCs performed exceptionally in 2023. Their earnings marked new highs because floating-rate portfolios benefited from high rates. However, rating agencies are showing concerns about credit deterioration and earnings growth in 2024.

It's true that BDCs benefited significantly from rate hikes in the past two years and that cuts in 2024 would impact their portfolio yields and margins. However, at the same time, I believe rate cuts would also enhance business confidence and portfolio activity, allowing BDCs to offset the impact of rate cuts with higher portfolio value. In particular, the private credit market, which accounts for nearly 66% of the BDCs' loan portfolio, is likely to rebound significantly in 2024. The private credit market grew sharply in the last decade and doubled in market share since 2020 on the back of low-interest rate policies. Indeed, the market performed exceptionally well even in a high-rate environment and deteriorating market conditions. The sustainable growth trend indicates that borrowers are interested in obtaining loans from the private credit market relative to selling equity at a discount. Moreover, tightening policies from traditional lenders has been adding to the shift. In fact, recent developments highlight that mainstream acceptance of the private credit market has been increasing as well-established companies, which were previously clients of banks, have started taking loans from the private market. For instance, Hyland Software was engaged with Credit Suisse for years to achieve its cash requirements, but it recently shifted to the private market for $3.4 billion from BDCs, such as Golub Capital, and others.

The private credit market share of $1.6 trillion surpassed the junk-rated corporate bond market in the US in 2023. In addition, the estimates suggest private credit is likely to expand its market share to $2.3 trillion by 2027. Besides higher demand, attractive returns for investors are yet another reason for robust private credit growth. The State Street Private Equity Index estimated that private debt funds surpassed buyout funds in terms of investor return in most of the quarters since 2022. Overall, it appears that private markets are on a secular growth trend and BDCs are likely to benefit from a stronger private credit market.

Trinity Capital is Likely to Outperform

Trinity Capital Total Returns Vs S&P 500 (Seeking Alpha)

After generating a 60% total return for shareholders in 2023, Trinity Capital is well-positioned to generate healthy returns in 2024. There are many reasons to anticipate solid returns in 2023, including robust demand for venture debt, strong asset quality and low accruals (asset quality and accruals are discussed later in the article).

Its portfolio value has soared nearly $500 million since 2020, supported by strong venture debt demand in both low and high-rate environments. In the third quarter, it funded around $149 million in new and existing companies. The stability in interest rates would support its portfolio investment activity in 2024. Although the venture capital market is likely to stabilize in 2024 after marking a 38% decline in 2023, the potential equity down rounds would add to venture debt demand. Additionally, its portfolio diversification across 19 different industries lowers the risk factor. Recently, the company took another strong step to enhance its liquidity and returns for shareholders by starting off-balance sheet growth drivers, such as a joint venture and RIA.

Financial Performance, Outlook and Returns

Trinity Capital's third- quarter investment income grew by 20% year over year to $46.6 million. In addition to investments across 19 different industries, the company's strategy of focusing on more than one revenue source lowers the risk factor. The company earns income from three streams, including loans, equipment financing, and accelerated OID plus fees. Loans account for 75% of its total income, while equipment financing and an accelerated OID plus fee make up 16% and 8%, respectively.

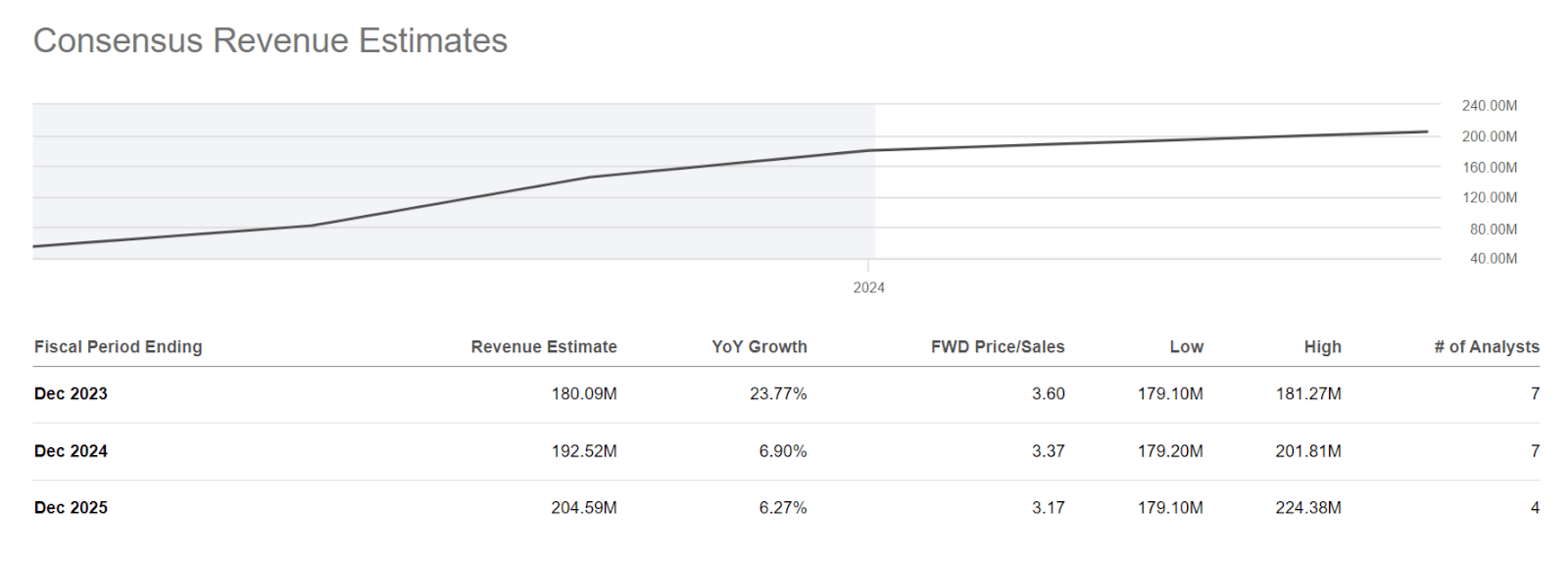

Revenue Estimate (Seeking Alpha)

{kind=link}

Wall Street estimates indicate that Trinity's investment income is expected to increase by 24% year over year in 2023 to $180 million and by 7% in 2025. Although rate cuts and a higher number of outstanding shares may negatively impact its earnings growth potential, expectations for earnings around $2.20 per share in the following years appear to be sufficient for dividend growth. Currently, its dividend coverage ratio is around 120% of its net investment income. As earnings are expected to hover around $2.20 per share in 2024, there is still room for more dividend increases.

Furthermore, in terms of asset quality, 97% of its portfolio is performing in line with expectations. At the end of the third quarter, it had only four portfolio companies on non-accrual, representing 2.6% of the total debt portfolio. Another way to look at the strength of Trinity's portfolio companies is their ability to raise funds. Between January and September 2023, 45 of its portfolio companies raised more than $2.4 billion for growth activities. Trinity's cash potential is also strong enough to capitalize on the opportunities in the venture debt market. The company had $257 million in liquidity as of the end of third quarter. It also recently raised $13 million through its ATM programme and has $134 million in assets under management in the joint venture.

Where Does TriplePoint Venture Growth Stand?

TriplePoint's Total Returns Vs S&P 500 and Trinity Capital (Seeking Alpha)

TriplePoint Venture Growth underperformed in 2023 despite offering one of the highest dividend yields in the industry. Its shares underperformed throughout the year because of concerns over high accruals and a notable decline in portfolio value. Its portfolio value of $870 million as of the end of the third quarter was down significantly from $962 million in the previous year's quarter. Higher accruals and low investments in new opportunities impacted its portfolio in the past few quarters. The company funded only $12 million in debt investments in the third quarter, representing a steep decline from $101 million in the year-ago period. The company's non-accrual was at 5% of the portfolio at the end of the third quarter, and three of its portfolio companies gained the lowest internal credit rating. Wall Street expects TriplePoint to generate earnings of $1.70 per share in 2024, representing a steep decline of 18% from expected earnings of $2.07 per share in 2023. Overall, it appears that TPVG carries a high risk heading into 2024.

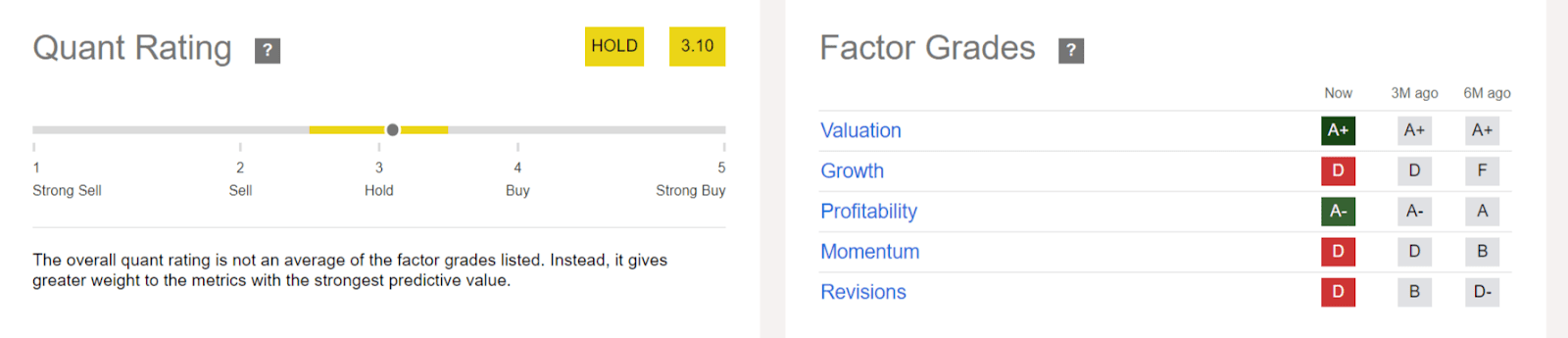

TriplePoint Quant Rating (Seeking Alpha)

{kind=link}

TriplePoint Venture Growth earned a hold rating with a quant score of 3.10. Its stock looks undervalued based on valuation. However, low growth, poor momentum, and downside revisions negatively impacted its overall ratings. A negative C on growth means the company is struggling to generate revenue and earnings growth compared to peers, while a negative D score on revision means analysts are lowering their earnings targets for the company. On the other hand, Trinity received high quant grades on valuation, growth, and profitability.

In Conclusion

Challenges for TriplePoint are mainly due to its underwriting policies, which don't reflect the performance of the entire industry. Based on SA's quant rating, it is ranked 49 out of 93 in its industry. There are dozens of other BDCs that are performing exceptionally well and are poised to generate robust returns with a low risk of non-accruals. Trinity Capital is among the well-positioned BDCs, supported by its strong balance sheet, increasing portfolio value, low non-accruals, and diversified portfolio.

For further details see:

Trinity Capital's Outperformance Is Likely To Continue In 2024 Against TriplePoint And S&P 500 (Rating Downgrade)