HTGC - Trinity Capital: This 14.1% Yielding BDC Is Underrated

2023-10-18 12:34:44 ET

Summary

- Trinity Capital Inc. is a well-managed business development company that provides financial solutions to growth companies.

- The BDC has expertise in financing capital needs across industries and has a well-diversified investment portfolio.

- Trinity Capital offers a 14.1% dividend yield and is selling at a small premium to net asset value, making it an underrated choice for passive income investors.

Trinity Capital Inc. (TRIN) is a well-managed business development company that focuses on providing financial solutions to growth companies.

Furthermore, Trinity Capital has developed an expertise in financing capital needs of companies across the industry spectrum. The BDC is well-diversified in its investment portfolio, has NII upside in a rising-rate environment and has delivered substantial dividend growth since 2020 which is the reason why I think that Trinity Capital is a promising bet for passive income investors.

With Trinity Capital's stock selling only at a small premium to net asset value, I think the 14.1% dividend yield that TRIN offers is underrated.

Portfolio Overview And Business Direction

Trinity Capital is an internally-managed specialty lending company that is regulated as a BDC under the Investment Company Act of 1940. This means the BDC is required to distribute 90% of its income to the BDC's owners which makes an investment in Trinity Capital particularly to those investors that want to create a long term stream of income.

Trinity Capital is a rather small BDC with a market value just shy of $600 million. Nonetheless, the addition of Trinity Capital could make a difference for passive income investors since the BDC is growing its base dividend fast and the portfolio is well-diversified.

The majority of Trinity Capital's investments are made in the foundational secured loan business which accounted for 74.5% of investments and the percentage has been growing over time.

The second business is Equipment Financing which helps companies finance the acquisition of capital goods and it helps Trinity Capital in diversifying its cash flows. Equipment Financing accounted for 21.3% of assets while Equity/Warrant positions accounted for 4.2% at the end of the second quarter.

There is a slight tendency in Trinity Capital growing its loan portfolio at the expense of its Equipment Financing and Equity/Warrant investments. If this trend continues, Trinity Capital might become more dependent on its loan originations moving forward than in the past.

Portfolio By Investment Type (Trinity Capital)

A Kicker For NII Growth: Higher Rates

Like most BDCs, Trinity Capital has positioned itself for a cyclical increase in interest rates by investing 72.1% of its debt portfolio into floating-rate loans.

As a result, the BDC has built considerable interest-rate sensitivity into its portfolio which could continue to pay off for Trinity Capital as long as the central bank pushes rates up. The recent inflation report, saying that consumer prices rose 3.7% YoY , is likely to result in a rate hike next month. A 100-basis point rise in interest rates is expected to boost Trinity Capital's net investment income by $0.15 per share.

My personal view is that inflation will continue to go up in the short-term, suggesting that the BDC will continue to profit from its interest-rate sensitive debt portfolio. A cyclical decline in interest rates would be a negative from a NII growth perspective, but it may help boost Trinity Capital's origination business. Either way, I think that Trinity Capital is well-positioned to participate in the growth of the credit industry moving forward.

Annualized Interest Rate Sensitivity (Trinity Capital)

Dividend Coverage And Growth

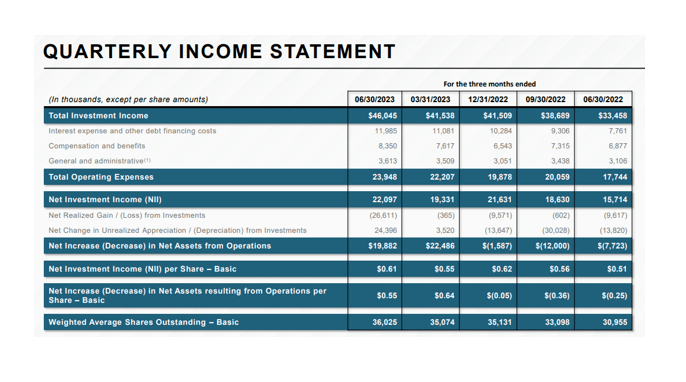

Trinity Capital earned a total $2.34 per share in NII in the last four quarters which translates to average NII of $0.59 per share per quarter. Floating-rate exposure primarily has helped Trinity Capital produce NII growth.

In 1Q-23, Trinity Capital had 117% dividend coverage (excluding supplemental dividends) and 127% in 2Q-23. In the last four quarters, Trinity Capital had a dividend coverage ratio of 126%. The base dividend, thus, is comfortably covered by NII. In a rising-rate environment, it could even improve further.

Quarterly Income Statement (Trinity Capital)

{kind=link}

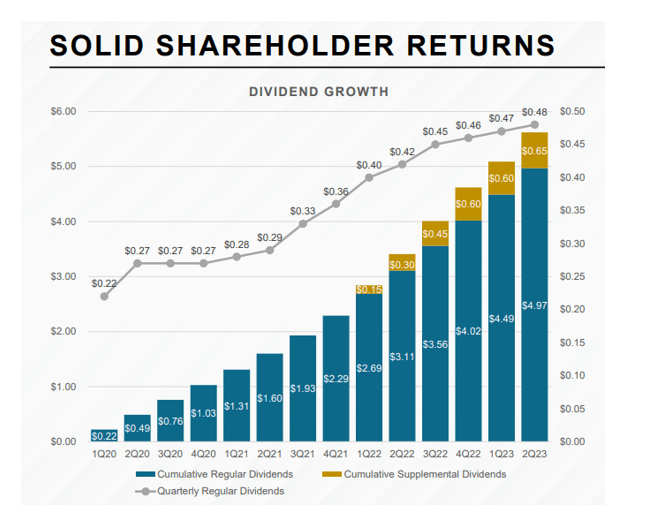

Since 2022, Trinity Capital is paying a substantial amount of hard-to-plan supplemental dividends that are effectively boosting passive income investors' earnings potential.

Trinity Capital is also growing its base dividend which has risen from just $0.22 per share in 1Q-20 to $0.49 per share in 3Q-23, reflecting total growth of 123%. Again, this figure doesn't include the growth in total dividends which has been driven in part by the payment of supplemental dividends.

Dividend Growth (Trinity Capital)

{kind=link}

Trinity Capital Is Selling At 1.07x NAV

Trinity Capital sells at a premium of 7% to net asset value which I think is deserved considering that the BDC is not only seeing strong NII and growing its regular dividend, but also paying supplemental dividends.

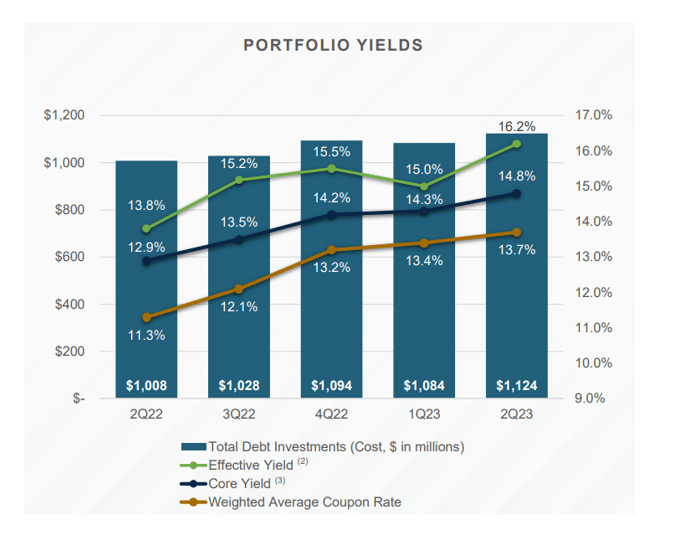

Trinity Capital has seen a strong expansion in yields as well in the last year with effective debt yields ticking up to 14.8%. Good credit quality, growing investment yields, growth in NII and excess dividend coverage justify a premium NAV multiple, in my view.

{kind=link}

Other BDCs are selling at small discounts or premiums to book value as well, like Oaktree Specialty Lending Corp. (OCSL) or Blue Owl Capital Inc. (OBDC) .

On the other end of this spectrum is Hercules Capital Inc. (HTGC) which sells for a premium to net asset value of 48% right now. The premium for Trinity Capital is due, in my view, due to the BDC's excellent dividend coverage and demonstrated growth.

Given the relatively small size of Trinity Capital (it has a market value of less than $600 Million), I think the BDC has not made it onto the radar-screen of many passive income investors yet.

Taking into account Trinity Capital's high excess dividend coverage, I would not be surprised to see TRIN trade at a 15-20% discount to net asset value moving forward.

Why Trinity Capital Could See A Higher/Lower NAV Multiple

The direction of interest rates could be an influencing factor determining to what extent Trinity Capital sells at a premium or discount to net asset value.

Trinity Capital had 72% exposure in its debt portfolio to floating-rates, implying that the BDC's NII trajectory will continue to be dependent on the central bank's interest rate policy moving forward.

Inflation ticked up again in September, on a YoY basis, so the central bank does appear to have an incentive to hike again next month. An end to the present rate-hiking cycle would probably be a negative for Trinity Capital, from an NII growth point of view.

Trinity Capital, however, may miss out on NII upside if the central bank pushes ahead with rate hikes in 2024. Golub Capital, for instance, is 100% invested in floating-rate debt, meaning the BDC could do better than Trinity Capital if rates continue to go up.

In a sense, Trinity Capital's high diversification (inclusion of Equipment Financing business) and lower degree of floating-rate exposure offers protection in a lower-rate environment, but it could limit Trinity Capital's NII growth in a rising-rate environment.

My Conclusion

Trinity Capital is an underrated, well-managed and promising BDC that passive income investors might want to put on their investing radars.

Trinity Capital has produced 123% growth in its base dividend rate since the beginning of 2022 and the BDC is increasingly distributing excess portfolio income through supplemental dividends which boosts the earnings potential of passive income investors.

The BDC's stock is selling at a relatively moderate 7% premium to net asset value, given the degree of excess dividend coverage, and I am getting a 14.1% NII-covered dividend yield on my last buy.

For further details see:

Trinity Capital: This 14.1% Yielding BDC Is Underrated