VRAI - Turbulent Year Ends With Records

2023-12-31 09:00:00 ET

Summary

- U.S. equity markets extended a spirited year-end rally with a ninth-straight week of gains - concluding a once-gloomy year with record-highs across the major benchmarks.

- The dramatic shift in fortunes beginning in late October coincided with a slate of inflation data showing a definitive easing of inflationary pressures and a long-awaited Fed acknowledgment of this disinflation.

- Finishing the year within 1% of fresh record-highs, the S&P 500 posted gains of another 0.4% on the week, extending its winning streak to its longest since 2004.

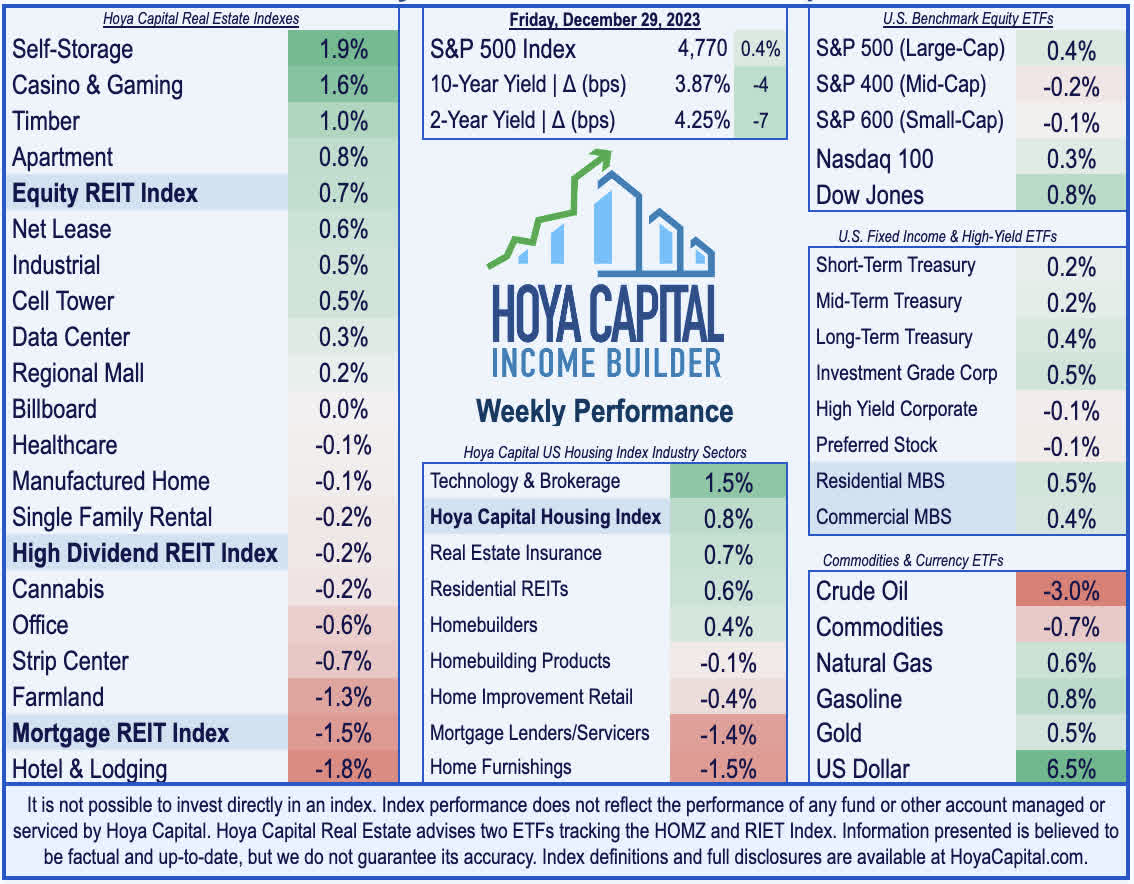

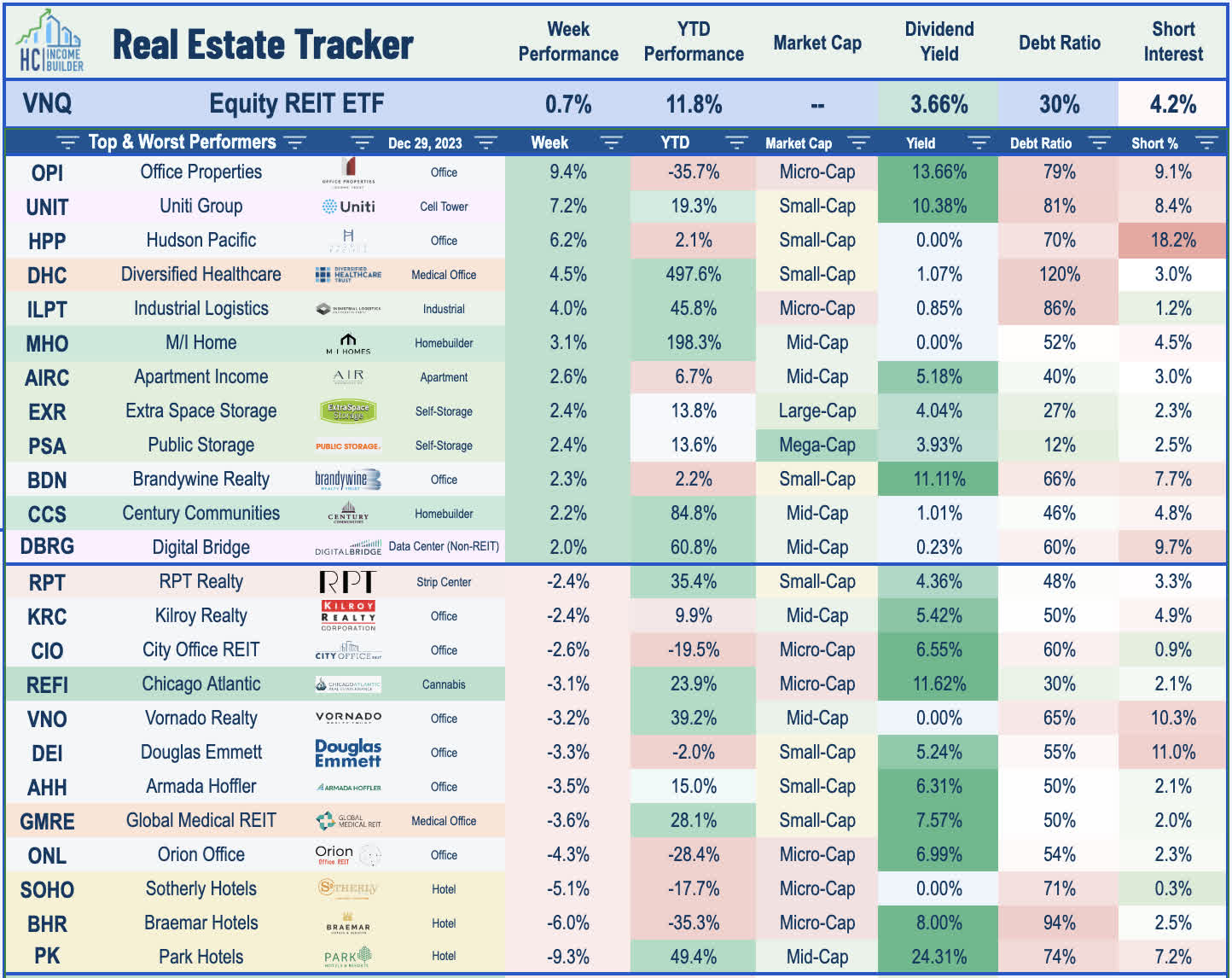

- Real estate equities - which were the "punching bag" of the Fed's aggressive tightening cycle and the most "unloved" sector in mainstream financial narrative - continued their dramatic year-end rebound. The Equity REIT Index gained 0.7% this week, posting total returns of around 12% this year.

- On an otherwise slow week of economic data and corporate newsflow, credit card processor Mastercard released its annual SpendingPulse retail sales report, which showed relatively lukewarm spending trends during the critical holiday season.

Real Estate Weekly Outlook

U.S. equity markets extended a spirited year-end rally with a ninth-straight week of gains - concluding a once-gloomy year with record-highs across the major benchmarks - amid a continued reversal in benchmark interest rates on solidified expectations of easing monetary policy conditions in 2024. The dramatic shift in fortunes beginning in late October coincided with a slate of inflation data showing a definitive easing of inflationary pressures and a long-awaited acknowledgment of this disinflation by central bank officials, while economic data and commentary thereafter did little to challenge the renewed optimism that the U.S. economy is indeed on course for a "soft landing."

{kind=link}

Finishing the year within 1% of fresh record-highs, the S&P 500 posted gains of another 0.4% on the week, extending its winning streak to a ninth-straight week, its longest since 2004. The tech-heavy Nasdaq 100 notched another series of record highs this week and posted its best year of returns since 1999. The Mid-Cap 400 and Small-Cap 600 finished marginally lower on the week after outperforming their large-cap peers in six of the prior eight weeks. Real estate equities - which were the "punching bag" of the Federal Reserve's aggressive eighteen-month tightening cycle and the most "unloved" sector in mainstream financial narrative - continued their dramatic year-end rebound. Extending their nine-week rebound to over 25%, the Equity REIT Index gained 0.7% this week, with 9-of-18 property sectors in positive territory, while the Mortgage REIT Index slipped 0.7%. Homebuilders and the broader Hoya Capital Housing Index were also among the leaders once again this week as mortgage rates continued their sharp retreat from three-decade highs, setting the stage for a revival in housing market activity in 2024.

{kind=link}

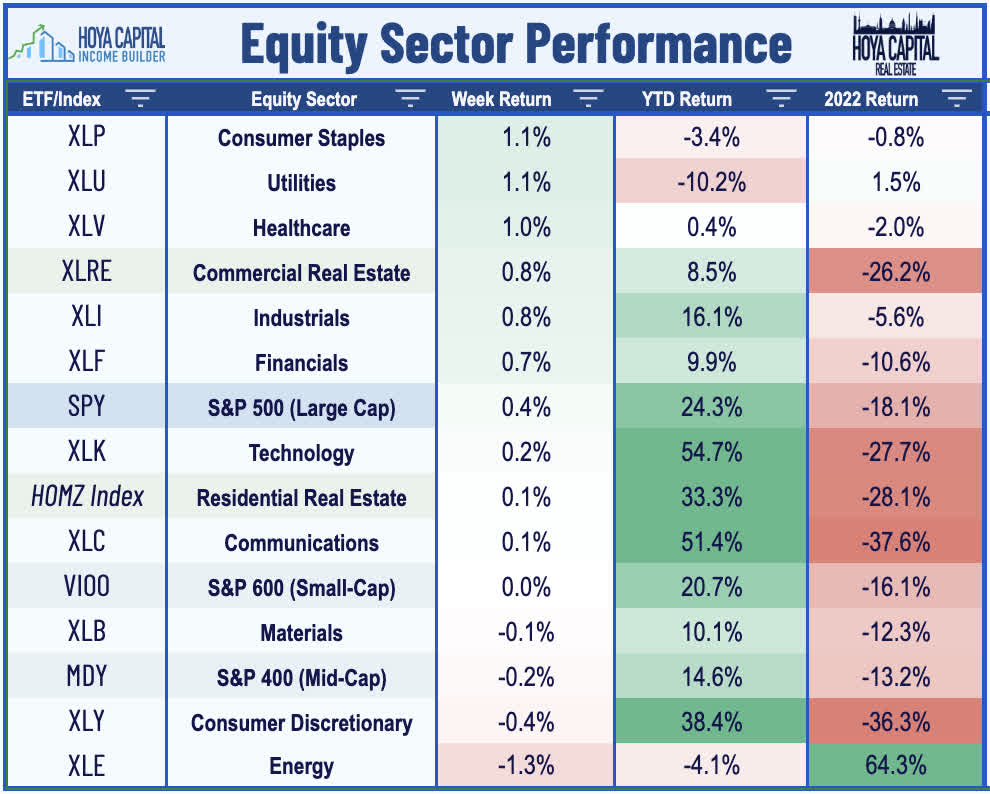

Bond markets continued their emphatic year-end rally as well this week as benchmark interest rates took a fresh leg lower following a series of successful Treasury auctions indicating strong demand for newly-issued government debt, indicating that investors are seeking to lock-in current yields on expectations of rate cuts ahead. The 10-Year Treasury Yield dipped another four basis points to 3.87% - its lowest weekly close since mid-July - while the policy-sensitive 2-Year Treasury Yield also dipped by seven basis point to 4.25%, its lowest close since mid-May. Swap contracts now imply an 86% probability the Federal Reserve initiates its first rate cut in March - and implies a year-end Fed Funds rate of 3.95%, which equates to six quarter-point rate cuts. Erasing its gains from last week, WTI Crude Oil traded lower by 3% this week after Danish shipping company Maersk announced that it will resume travel via the Suez Canal following a temporary halt after attacks by Iran-backed militia, easing concerns over supply chain bottlenecks through the critical Red Sea shipping lanes. The key "swing" inflation input, oil prices are now 4% above their December 12th low, but still 25% below their September 27th high. Nine of the eleven GICS equity sectors finished higher on the week, led on the upside by Consumer Staples ( XLP ), while Energy ( XLE ) stocks lagged.

{kind=link}

2023 Performance Recap

For the year, the Equity REIT Index finished with total returns of 11.8%, while the Mortgage REIT Index posted total returns of 14.9%. At the bottom in late October, both indexes were lower by over 10% on a year-to-date basis and trading at their lowest-level since the depths of the pandemic in May 2020. This compares with the 26.2% gain on the S&P 500 , the 16.1% gain for the S&P Mid-Cap 400 , and the 16.2% gain for the S&P Small-Cap 600. Within the real estate sector, 15 of the 18 property sectors finished the year in positive territory, led by Data Center, Regional Malls, and Hotel REITs, while Cell Tower, Net Lease and Farmland REITs lagged on the downside. The 10-Year Treasury Yield ended the year lower by 1 basis point - up from its 2023 intra-day lows of 3.26% in April, but down sharply from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index posted total returns of 5.5%. WTI Crude Oil prices declined by 5% this year, while Natural Gas prices dipped 64%.

{kind=link}

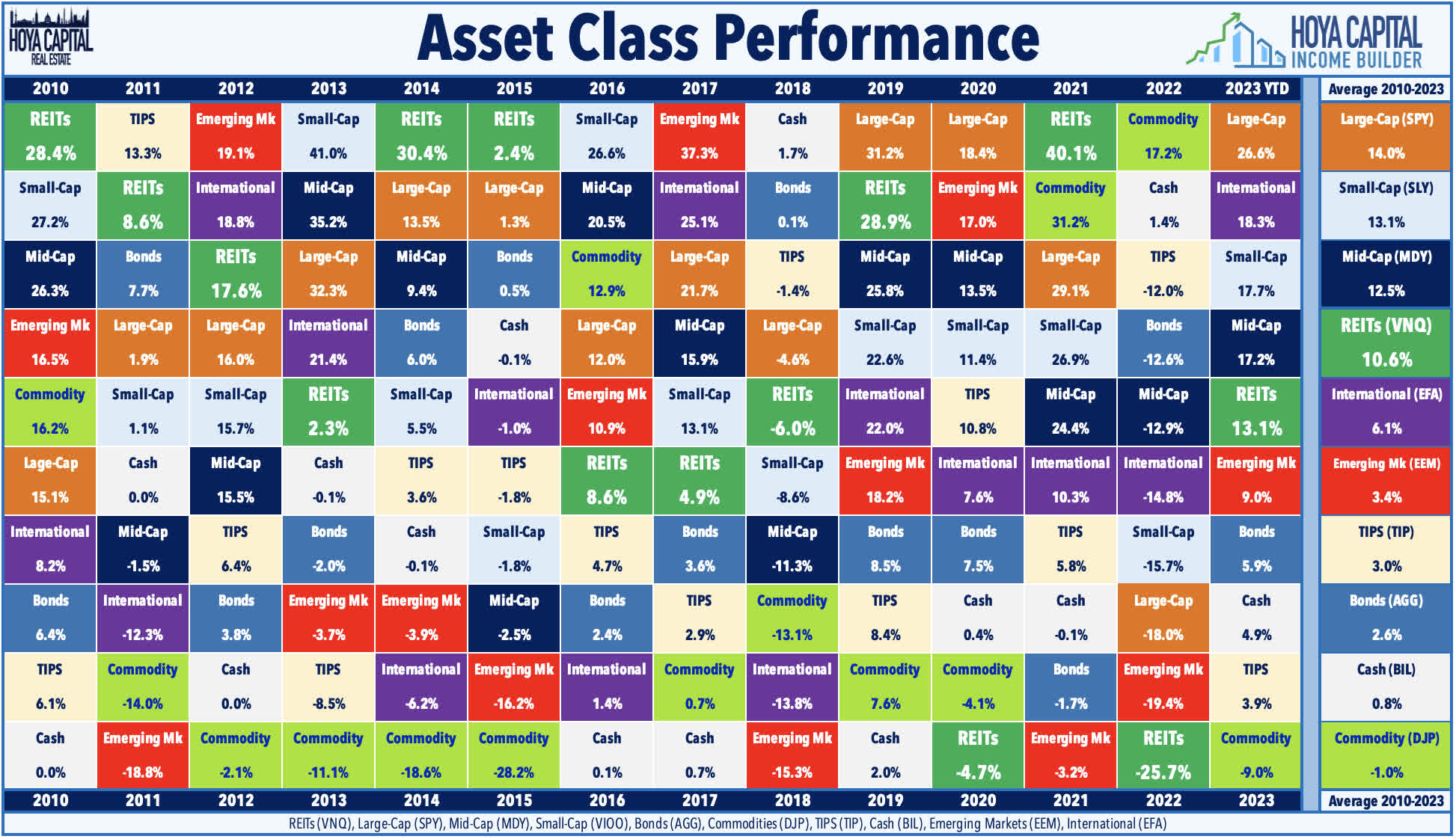

Until the late-year rebound, there were few places to hide across financial markets from late 2021 through late 2023 in a historically brutal two-year period for investors, which had wiped out nearly a fifth of global financial wealth. Pressured by the historically aggressive Fed tightening cycle, the typically steady US bond market delivered its worst year in history in 2022 with a loss of 13.01% on the Bloomberg US Aggregate Bond Index , which was over 4x larger than the previous worst year back in 1994 (-2.9%). Among the ten major asset classes, Commodities was the only segment to see positive inflation-adjusted returns in 2022, but was the weakest-performing asset class in 2023. After lagging for much of the year in the basement of the performance tables among the ten major asset classes, REITs ultimately concluded 2023 year as the fifth-best performing asset class. The performance dispersion between U.S. Large-Cap and Small-Cap Equities was unusually large for much of the year, peaking at nearly 20 percentage points in October before tightening in the final two months to around 10 percentage points.

{kind=link}

Real Estate Economic Data

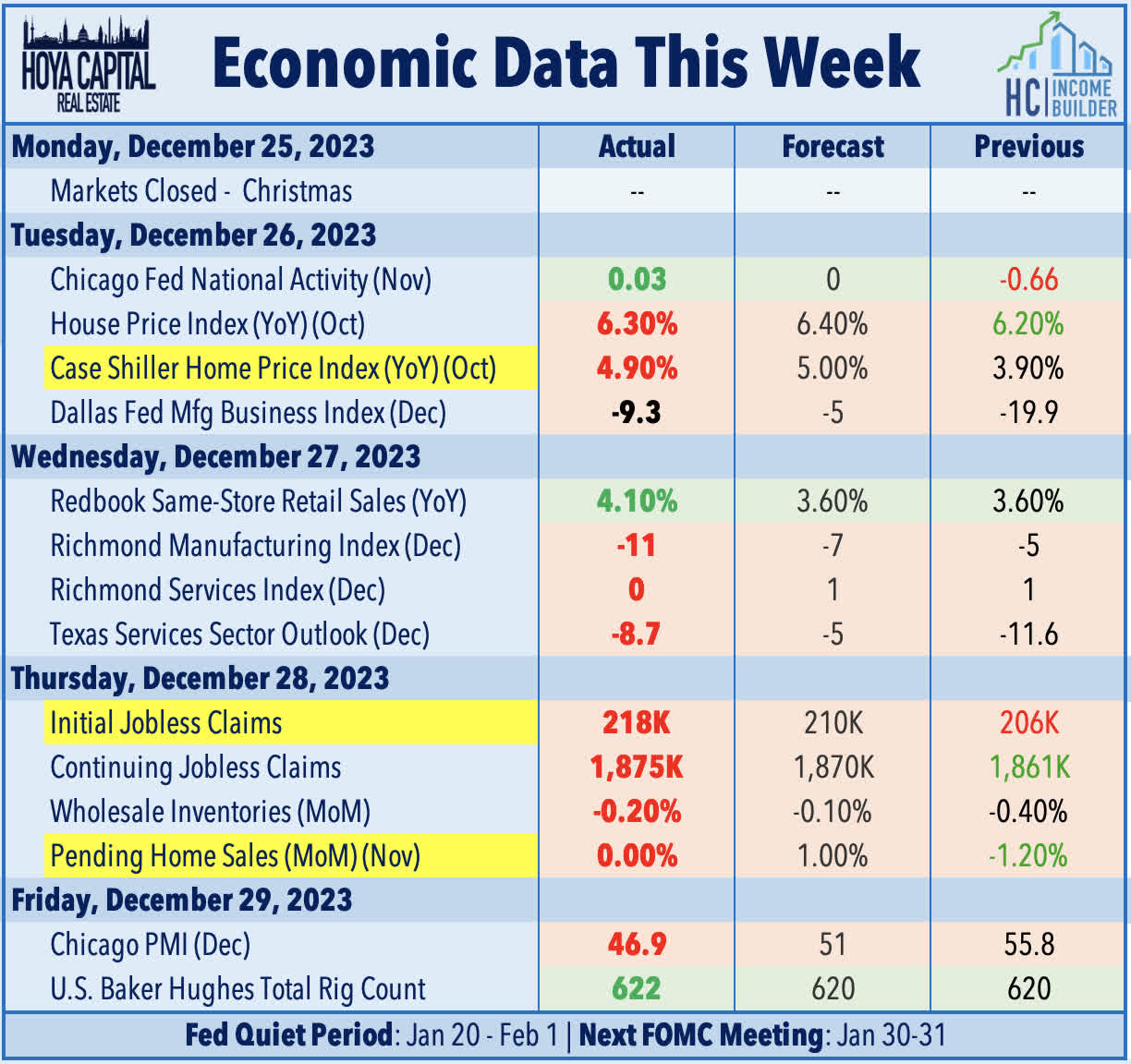

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

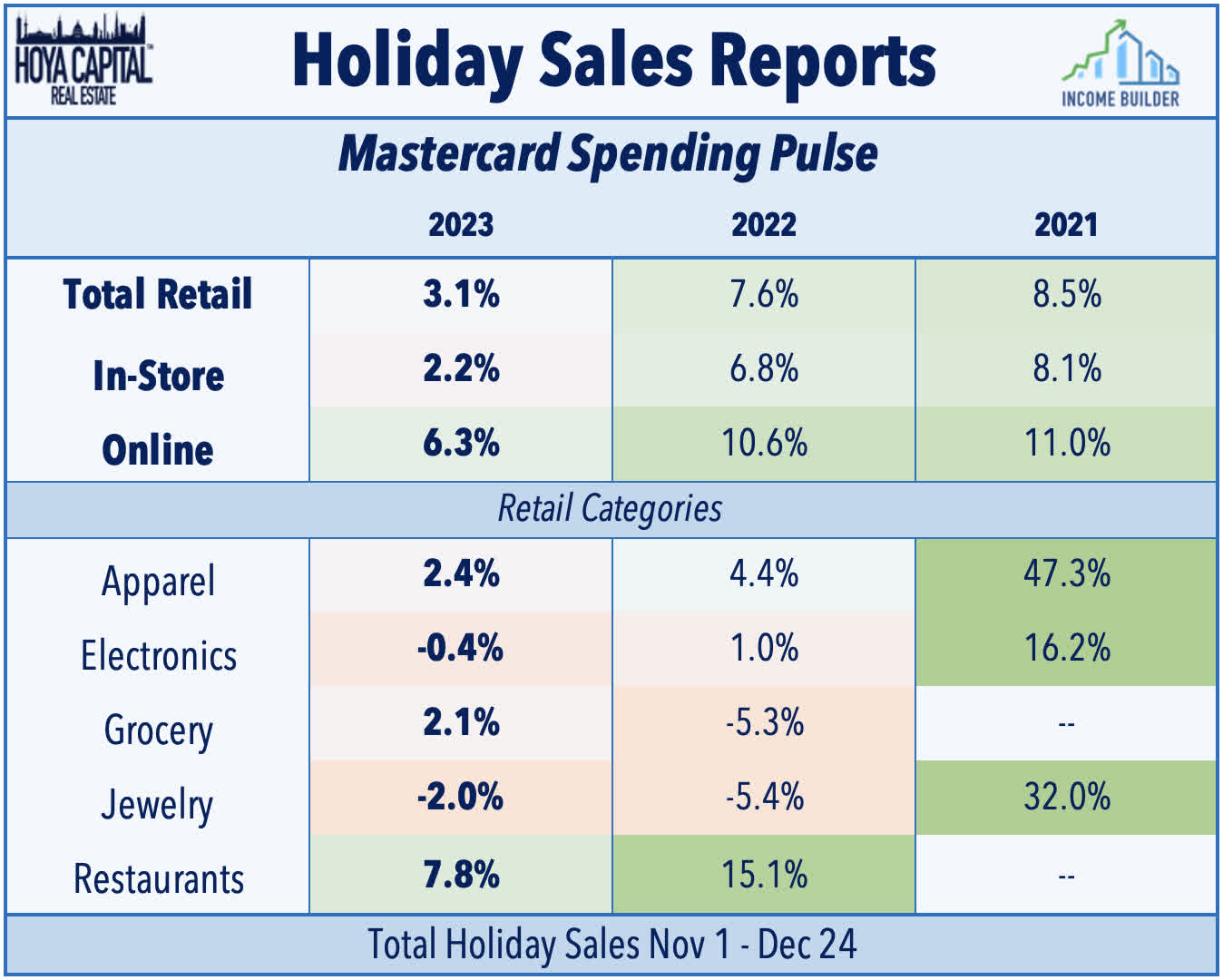

Credit card processor Mastercard released its annual SpendingPulse retail sales report this week, w hich showed relatively lukewarm spending trends during the critical holiday season. Total retail sales rose 3.1% for the period from November 1 through December 24th compared to a year earlier - roughly matching expectations, but down from the roughly 8% nominal growth reported in 2022 and 2021. The report was generally consistent with the BLS report released earlier this month, which showed that retail sales rose 3.3% year-over-year in November. On an inflation-adjusted basis - using the CPI Price Index - "real" consumer spending was effectively flat this holiday season after rising less than 1% on a "real" basis in the prior year. Mastercard reported that online retail sales rose 6.3%, outpacing the in-store sales increase of 2.2%. At the category-level, restaurants were the top-performing category, jumping 7.8% from a year earlier, while grocery store sales were also relatively solid with a 2.1% increase. Apparel sales were strong for a second-straight year, rising 2.4% from last year after an increase of 4.4%% in 2022, but electronics and jewelry sales were soft for a second-straight year.

{kind=link}

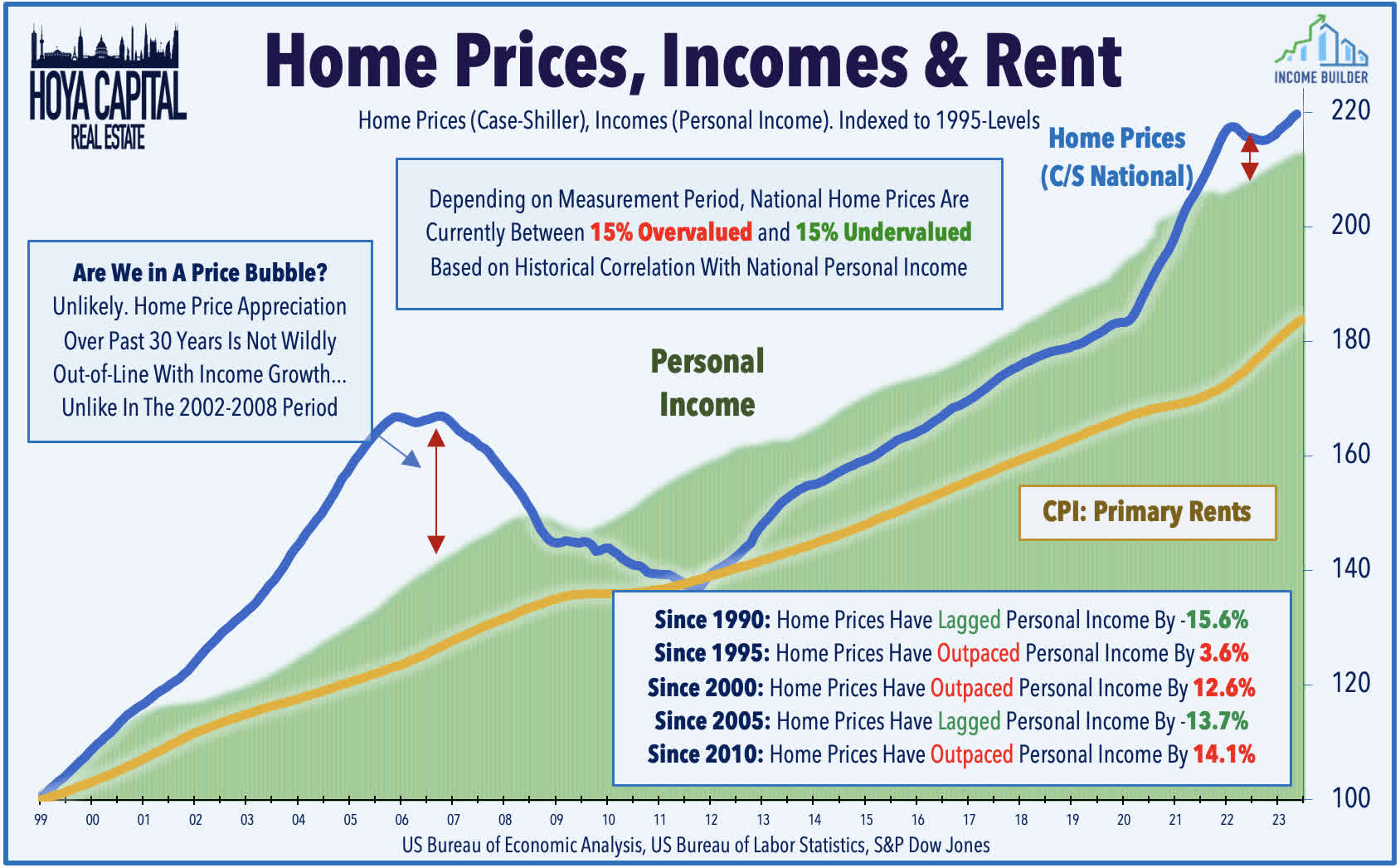

Elsewhere on the economic slate, S&P released its monthly CoreLogic Case-Shiller Home Price Index this week, which showed a reacceleration in home price appreciation in October, even as mortgage rates peaked at three-decade highs. Historically low inventory levels - a function of a decade-long period of under-building of single-family homes immediately following the Great Financial Crisis - outweighed the headwinds on valuations from soaring mortgage rates. National home prices rose 4.8% year-over-year in October, marking the ninth-straight month of increases since posting monthly declines in seven-straight months from late 2022 through early 2023. On a seasonally adjusted basis, prices increased in 19 of the 20 cities on a month-to-month basis. (Portland was the lone decliner in October). Despite the rebound, several major metros remain notably "underwater" relative to their recent peaks, including San Francisco (down 8.1% from the peak), Seattle (-6.5%), Portland (-4.3%), Las Vegas (-4.2%) and Phoenix (-3.9%.) Despite the double-digit surge in home values from 2020-2022, home prices are still roughly in-line with their "warranted" levels based on Personal Income.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

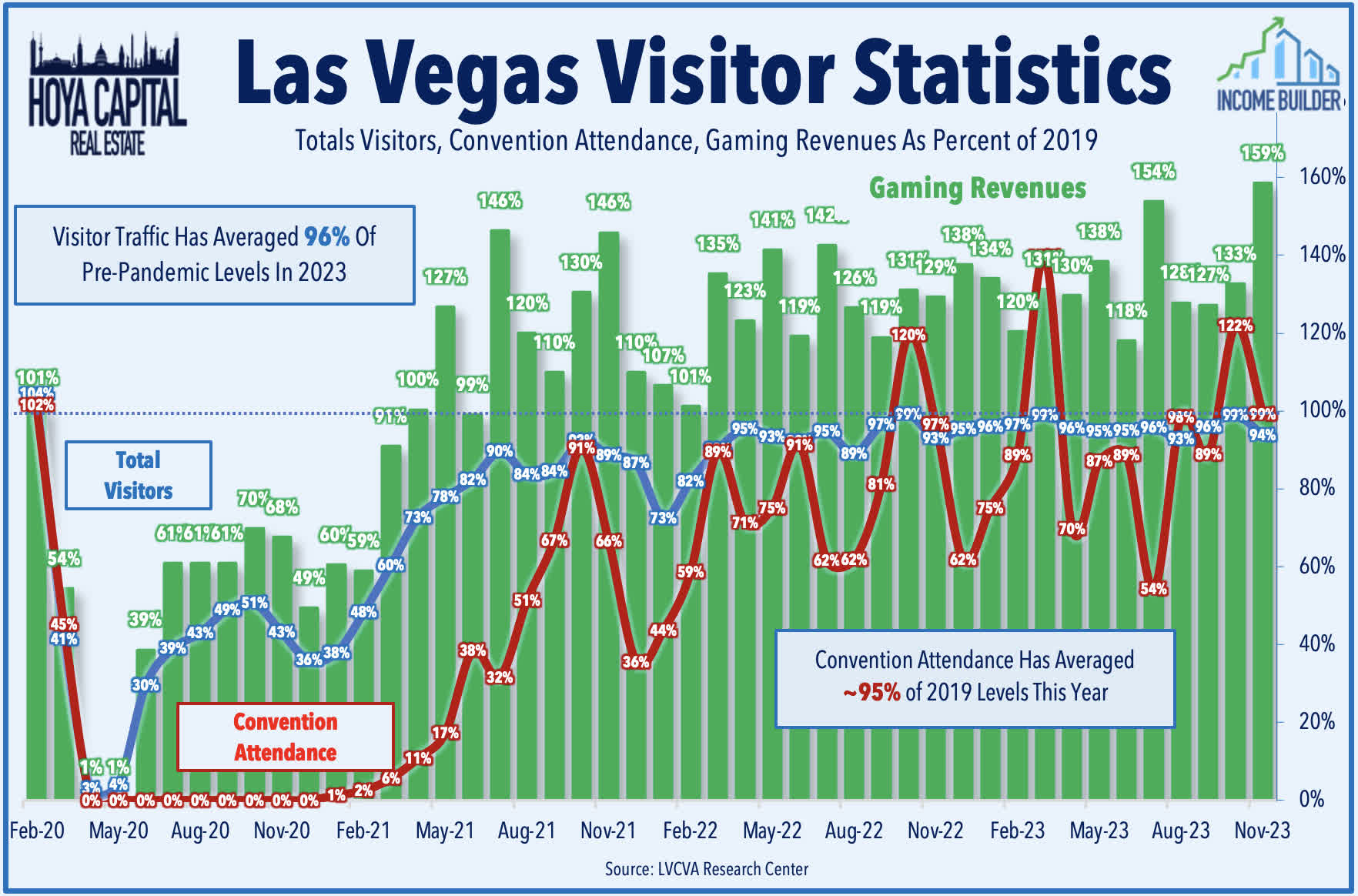

Hotel : Apple Hospitality ( APLE ) - which we own in the Focused Income Portfolio - was active on the M&A-front this week on an otherwise slow week of REIT-related newsflow, announcing the $75M acquisition of a Las Vegas hotel adjacent to the Strip. The 299-room SpringHill Suites by Marriott - which opened in October 2009 and is adjacent to the Las Vegas Convention Center - was acquired for $251k per key and a 10.7x multiple on trailing twelve-month Hotel EBITDA. Las Vegas has remained one of the strongest hotel markets since the start of the pandemic, benefiting in part from the relative weakness of other West Coast markets. According to the LVCVA Research Center , visitor traffic and convention attendance has hovered within 5% of the record-setting 2019 season throughout 2023, while total hotel and gaming revenues are more than 50% above pre-pandemic levels. Of note, the average room rate for a Las Vegas hotel was more than 80% higher in November 2023 compared to November 2019. Taking a step back and looking at national trends, the TSA reported this week that domestic throughput through TSA checkpoints has averaged about 105% of 2019-levels during December, a relatively strong showing for the holiday season amid concern of waning consumer confidence.

{kind=link}

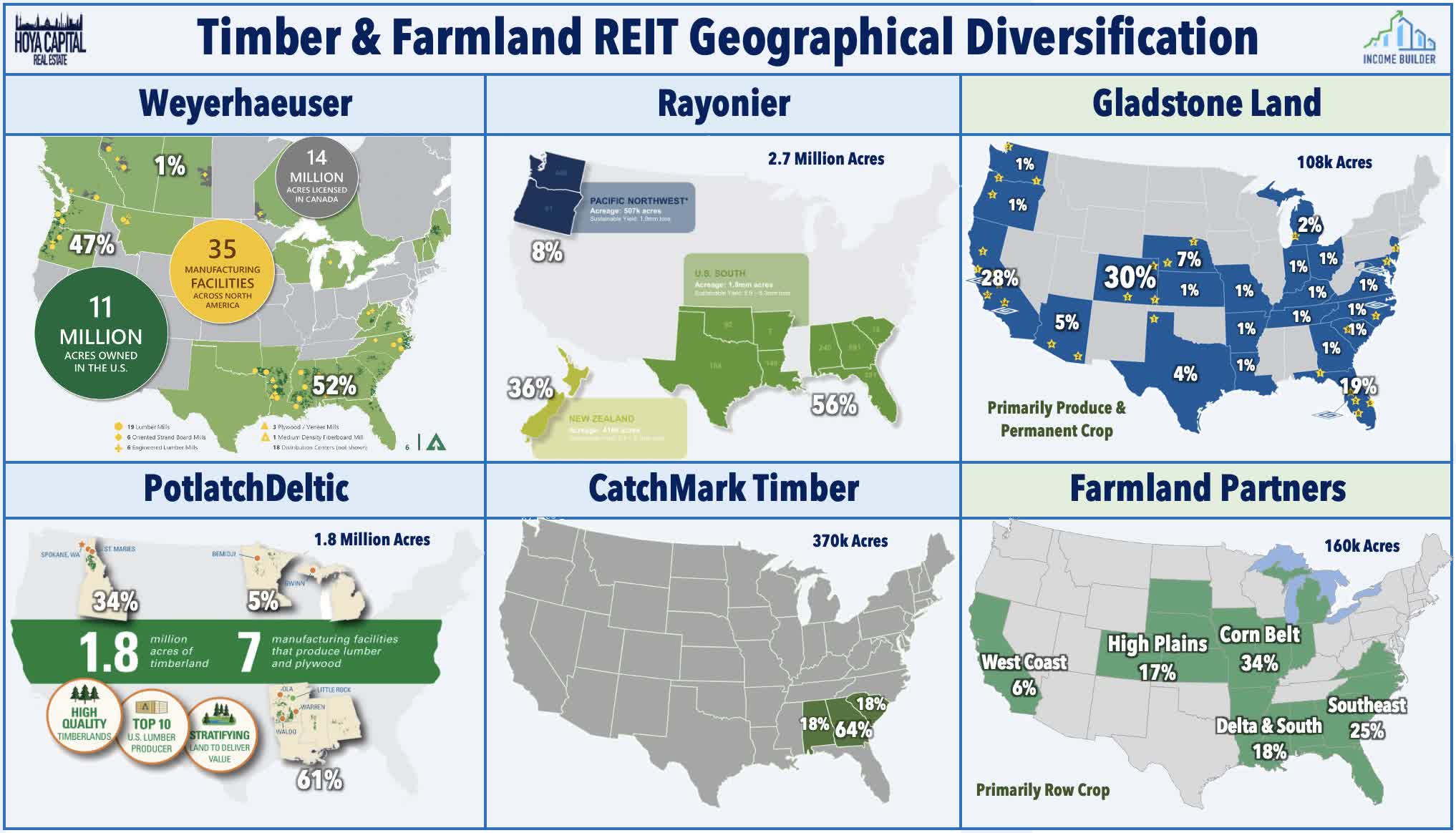

Timber : Weyerhaeuser ( WY ) - the largest timber REIT and the largest private landowner in North America - was among the leaders this week after it announced the sale of its first batch of carbon offsets, its first move into the potentially lucrative voluntary carbon market in which companies with ESG mandates buy and sell carbon credits that represent certified removals or reductions of greenhouse gases. Weyerhaeuser sold roughly 32,000 of these environmental credits backed by its timberland in the North Maine Woods to an undisclosed buyer for $29 each, generating total proceeds of more than $900,000. The credits each represent a metric ton of carbon dioxide sequestered in standing trees. WY - which owns roughly 11 million acres of timberlands in the U.S. which remove about 14 million metric tons of carbon dioxide from the atmosphere each year - has highlighted its push into the carbon offset business in recent quarters, and expects this new unit dedicated to carbon offsets to generate $100 million a year in profit by the end of 2025. While the concept and effectiveness of carbon offset markets has faced some criticism - and has raised questions over whether self-imposed ESG mandates are consistent with a company's fiduciary duty to shareholders - the effectiveness of trees in atmospheric carbon removal is well-established. According to the USDA, a mature tree will absorb 48 pounds of CO2 per year.

{kind=link}

Office : West Coast-focused office REIT Hudson Pacific ( HPP ) rallied another 6% this week - extending its frenetic nine-week rally to over 100% - after it closed on an amendment to its unsecured revolving credit line. The deal refined certain definitions and adjust certain covenant calculations, while reducing the aggregate commitments from the lenders by $100 million, to $900 million of total commitments, with the maturity date remaining December 2026 (including extension options). HPP commented that the deal "underscores our strong banking relationships and provides us with the flexibility to continue operating successfully in the current market environment and beyond." Office REITs have rebounded by an average of 40% since the lows in late October, led by gains of over 70% from a trio of the most heavily-beaten down names including the aforementioned Hudson Pacific, City Office ( CIO ), and Office Properties Income ( OPI ). Last week, we reported that Fitch Ratings published a note outlining a downbeat outlook on credit trends in commercial real estate, forecasting that the overall U.S. CMBS loan delinquencies will double from 2.25% today to 4.5% in 2024 and 4.9% in 2025, driven primarily by a "deterioration" in office properties. Context is important, however, and office delinquency rates had been trending to historic lows below 2% over the prior decade from nearly 8% in 2012.

{kind=link}

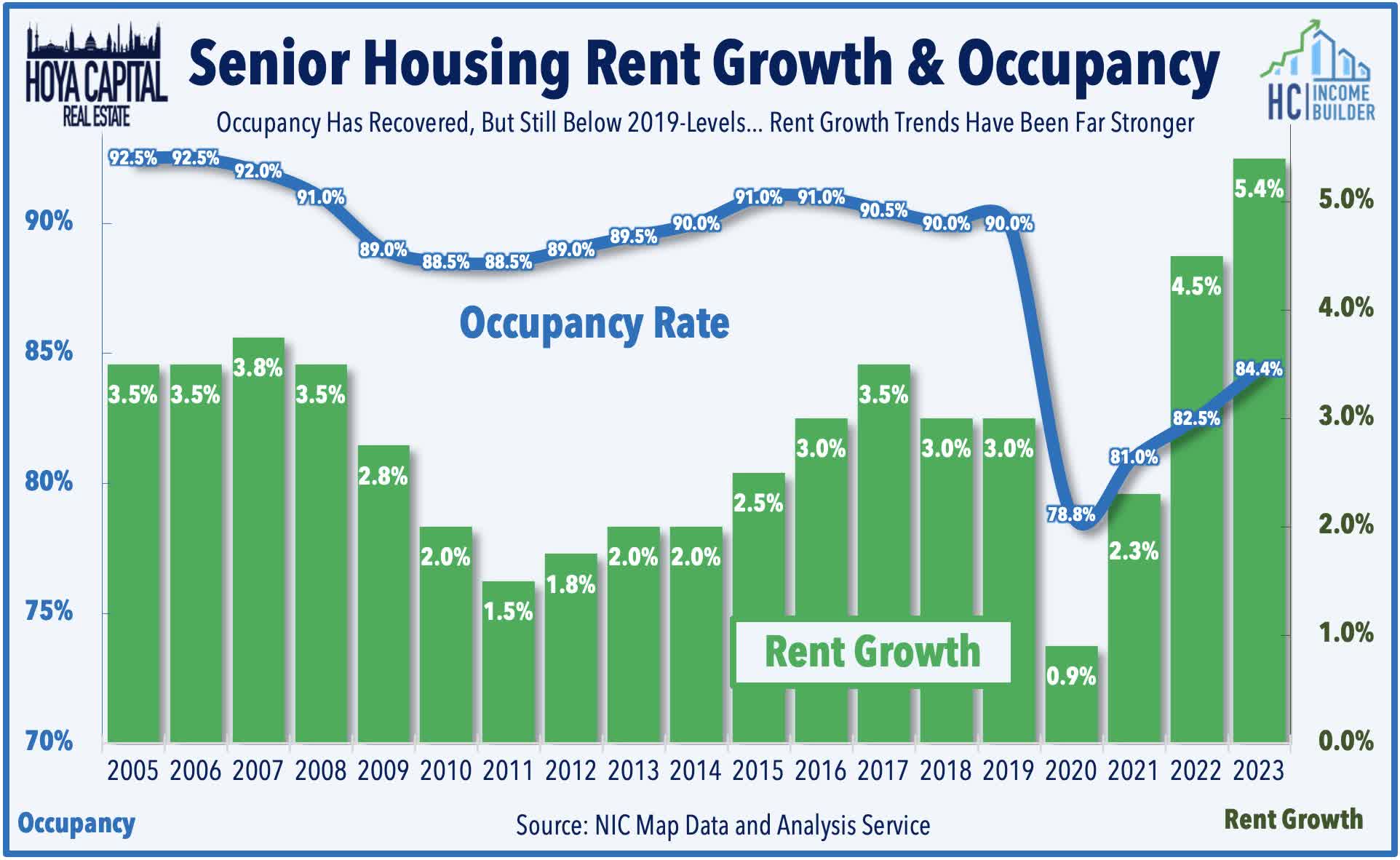

Healthcare : Diversified Healthcare Trust ( DHC ) - which notched the strongest gains of any REIT in 2023 after plunging in 2022 on solvency concerns - rallied another 4% this week after it provided an operating update showing a continued recovery in its Senior Housing Operating ("SHOP") portfolio. DHC noted that its occupancy rate in November climbed above 80% for the first time since the start of the pandemic. At 80.1%, this rate was more than 10 percentage points above the lows below 70% in Q1 of 2021, but still about 5 percentage points below the pre-pandemic level of around 85% from 2019. These trends were largely consistent with data from NIC last month, which also showed that record-setting rent growth over the past two years has helped to offset the drag from lower occupancy rates. Driven in part by the nearly 9% increase in Social Security benefits this past year due to the Cost of Living Adjustment ("COLA"), senior housing rental rents have been climbing at roughly double their pre-pandemic pace, increasing by nearly 6% this year.

{kind=link}

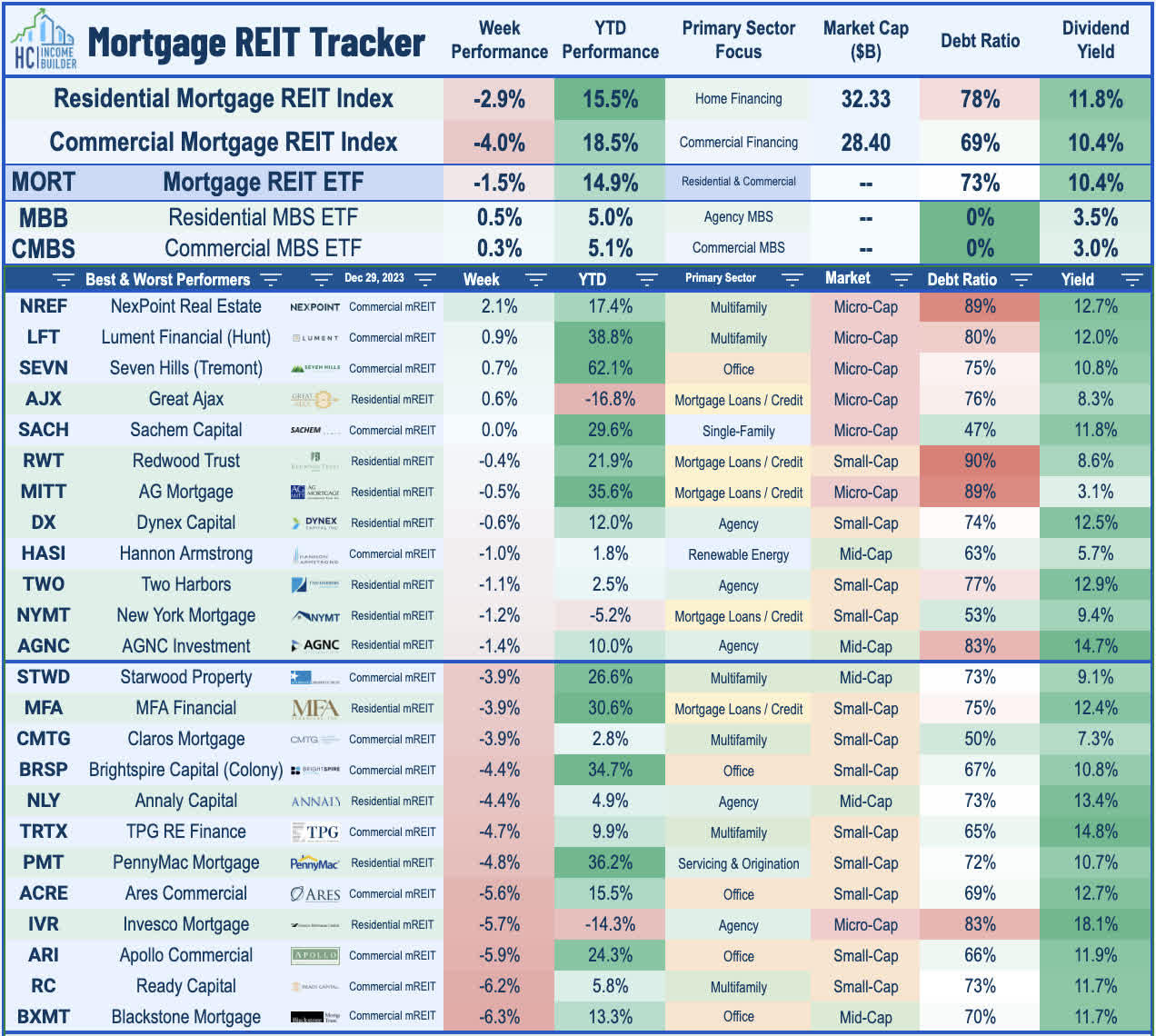

Mortgage REIT Week In Review

Giving back some of their gains following a 30% surge over the prior eight weeks, mortgage REITs were under some pressure this week, with the iShares Mortgage REIT ETF ( REM ) slipping 1.5% to wrap-up the year with total returns of roughly 15%. On a clearly slow week of newsflow, the sector took a hit late in the week after a Bloomberg reported on a bankruptcy court filing from a little-known private REIT called JER Investors Trust , which had last filed a public shareholder report in 2012. A puzzling report that linked to the firm's website which had not been updated in over a decade, the article extrapolate that the filing is the "latest sign of distress in commercial real estate." Perhaps a better commentary on the state of financial media and the amplification resulting from AI-generated content than as a commentary on the state of the real estate industry, the Bloomberg report on the "pink sheet" company with a market capitalization of below $2M was picked up by a handful of other outlets with one commenting , "the world will be watching closely, keenly aware of the implications this case could have for the commercial real estate sector and the broader financial market."

{kind=link}

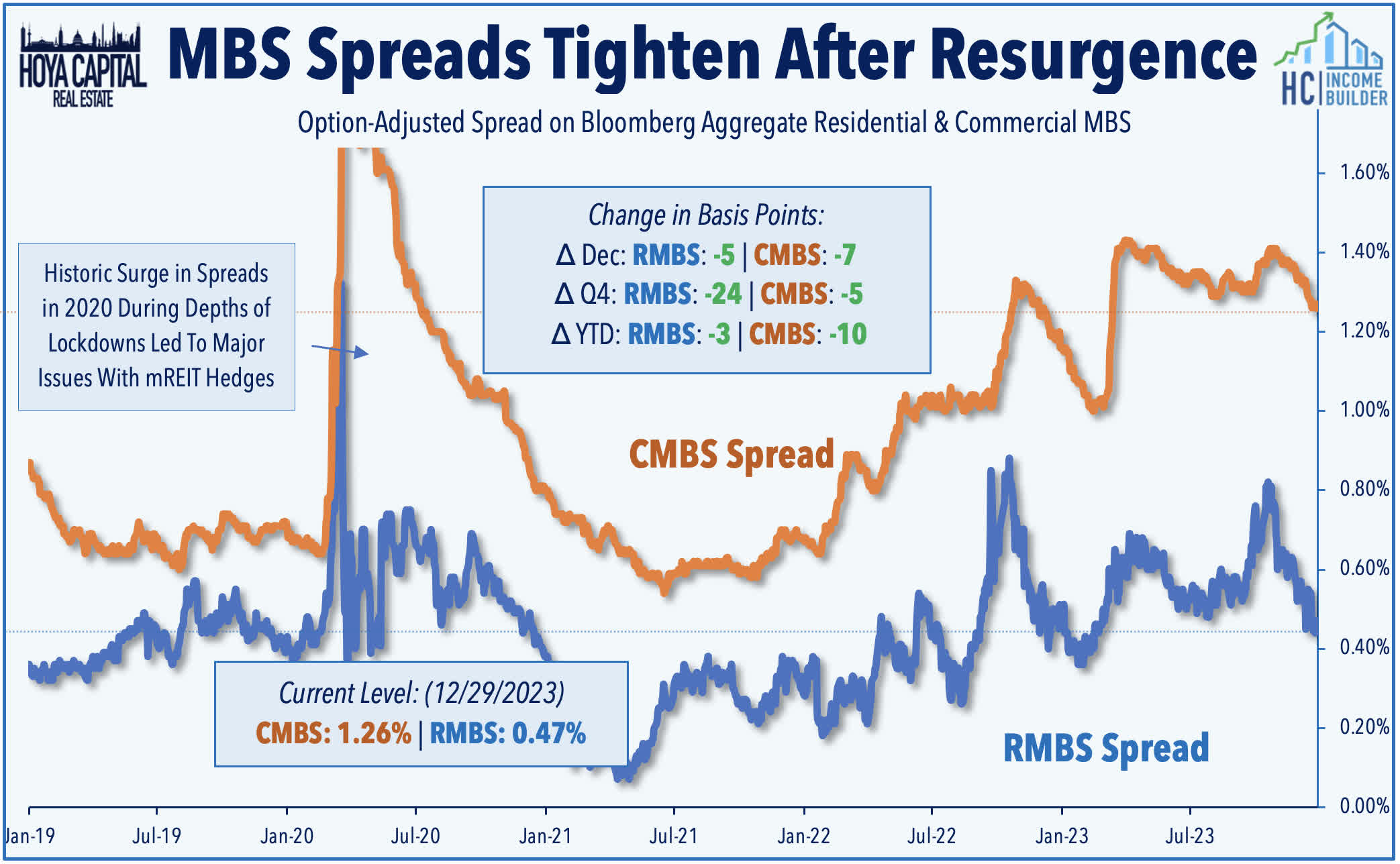

Elsewhere this week, Ellington Financial ( EFC ) - which closed on its acquisition of fellow mortgage REIT Arlington Investment earlier this month - traded lower by about 2% this week after it announced that its estimated Book Value Per Share ("BVPS") was $14.06 as of Nov 30, which is down about 2% from the end of September. Perhaps aside from EFC, mortgage REITs are likely to report a significant increase in Book Values in the fourth quarter given the double tailwinds from lower benchmark interest rates and tighter spreads, the two primary input into valuation models. Since the start of the fourth quarter, the benchmark 2-Year Treasury Yield has plunged 80 basis points from 5.05% to 4.25%. Providing an added boost, spreads on Residential Mortgage Backed Securities ("MBS") have tightened by 24 basis points during Q4, while spreads on Commercial MBS ("CMBS") have tightened by 5 basis points. In a year dominated by headlines of CRE loan distress, RMBS spreads actually tightened 3 bps while CMBS spreads tightened by 10 bps.

{kind=link}

To estimate changes in mortgage REIT Book Values, it's helpful to look at the un-levered performance of the underlying mortgage-backed securities. The iShares Residential MBS ETF ( MBB ) - which tracks the un-levered performance of RMBS - posted total returns of 7.3% in Q4 - one of its strongest quarters on record. The iShares Commercial MBS ETF ( CMBS ) - which tracks the un-levered performance of RMBS - posted gains of 5.0% in Q4, also one of its strongest quarterly gains on record. Based on recent correlations between these indexes and mREIT book values -and incorporating an estimate for hedging-related impacts - we estimate that the average residential mREIT will report an increase in BVPS of between 10-15% in Q4, while the average commercial mREIT will report an increase between 5-10%.

Hoya Capital

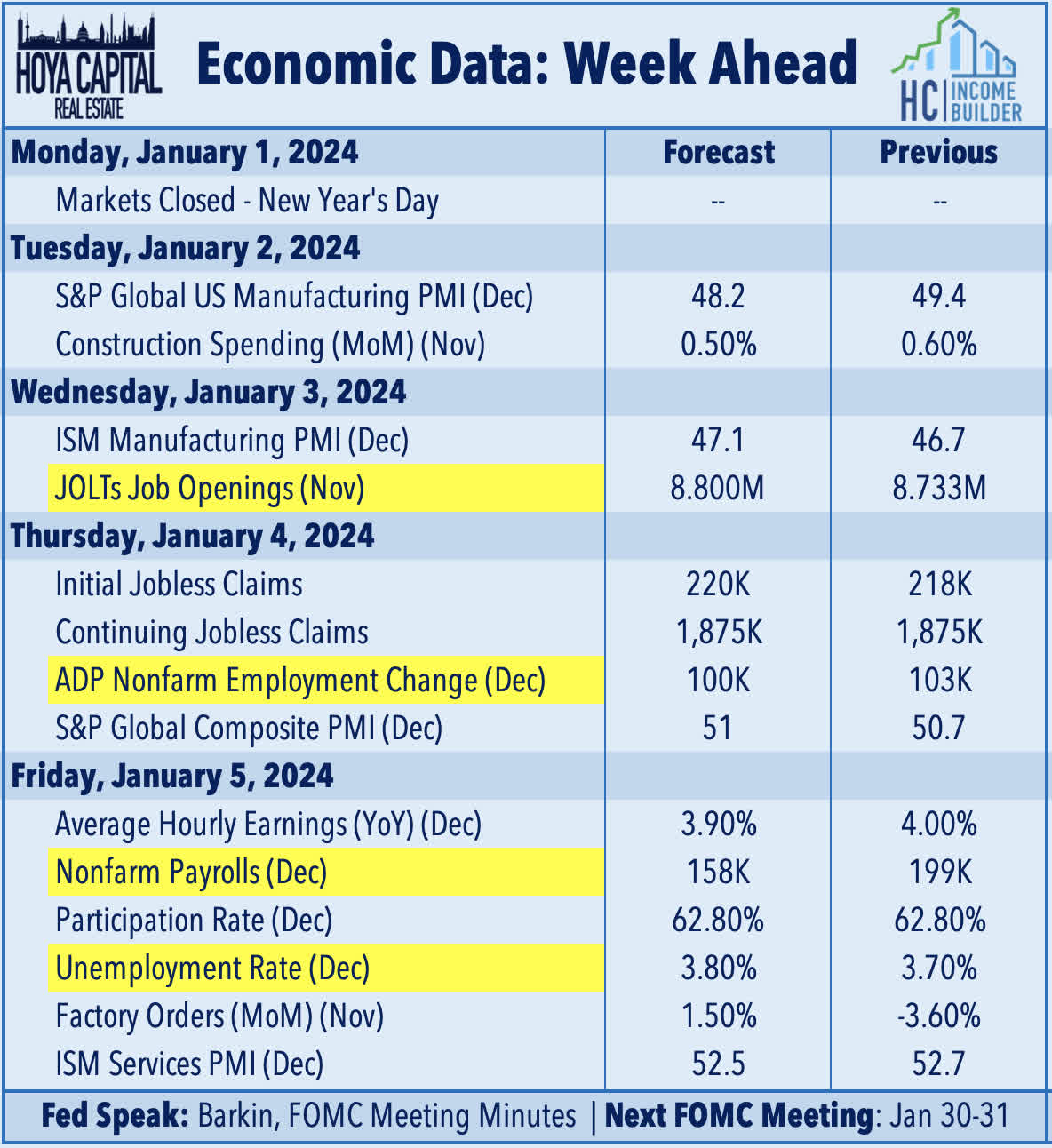

Economic Calendar In The Week Ahead

The economic calendar heats-up once again in the first week of the new year after markets re-open on Tuesday following the New Year holiday on Monday. Employment data highlights the critical week of economic data, headlined by the JOLTS report on Wednesday, ADP Payrolls and Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 158k in December, which follows a relatively solid report in November in which the economy added 199k jobs. Last month, the BLS report was the strongest of the four major reports and followed particularly soft JOLTS data showing that job openings in October dipped to the lowest level since March 2021 at 8.73 million - the lowest since the "reopening" of the US economy in early 2021 - and down roughly 30% from the peak of the labor market shortages seen in early 2022. The Average Hourly Earnings series within the BLS payrolls report - which is the first major inflation print for December - will also be closely-watched, and is expected to show a cooldown in wage growth to 3.9%. 'Good news is bad news' will likely remain the theme of these reports as Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on cooling labor markets. Happy New Year from Hoya Capital and the team!

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Turbulent Year Ends With Records