PNTG - U.S. Physical Therapy Remains Overpriced (Rating Downgrade)

2023-10-16 13:25:25 ET

Summary

- U.S. Physical Therapy's stock has underperformed the S&P 500 since I rated it a 'hold' in November 2022.

- The company's financial performance has been mixed, with a decline in net income and operating cash flow.

- The stock is pricey compared to similar firms and therefore I am downgrading it from a 'hold' to a 'sell' due to recent weakness and valuation concerns.

Just like when it comes to chess or any other activity, part of becoming better at what you do involves learning from your weaknesses and improving on them. When it comes to investing, one of the weaknesses that I have is that I tend to give too much leeway in companies that look pricey when those companies are high quality operators in their space. In short, I overemphasize the significance of the quality of the business relative to the price at which shares are trading. Sometimes, this can lead to a lot of pain. Other times, it can just result in some suboptimal performance.

A great example of this can be seen by looking at U.S. Physical Therapy ( USPH ). Those who follow the company you know that the firm operates physical therapy clinics that provide both pre and post operative care for orthopedic related disorders, sports related injuries, neurological injuries, and more. Back in November of last year, I wrote about the company , rating it a ‘hold’ because of its continued growth. However, I've said that shares looked more or less fairly valued at that time. And that assessment was based on the quality of the operation. Normally when I rate a company a ‘hold’, my belief is that shares should generate upside or downside that should more or less match the broader market for the foreseeable future. But since the publication of that article, shares have generated upside for investors of only 3.2% compared to the 12.1% seen by the S&P 500.

Fast forward to today, and my overall valuation of the company is still the same. After learning from my past mistake and comparing the company's valuation to similar firms, I have decided to downgrade it slightly from a ‘hold’ to a ‘sell’. Although I don't think that the company is awful by any means, shares are pricey relative to similar enterprises and some of its recent financial performance has been mixed. In the event that fundamentals change from this point on, and those changes are for the better, I could change my assessment of the company again. But for now, I think a more bearish stance on it makes sense.

Growth continues, but there are weaknesses

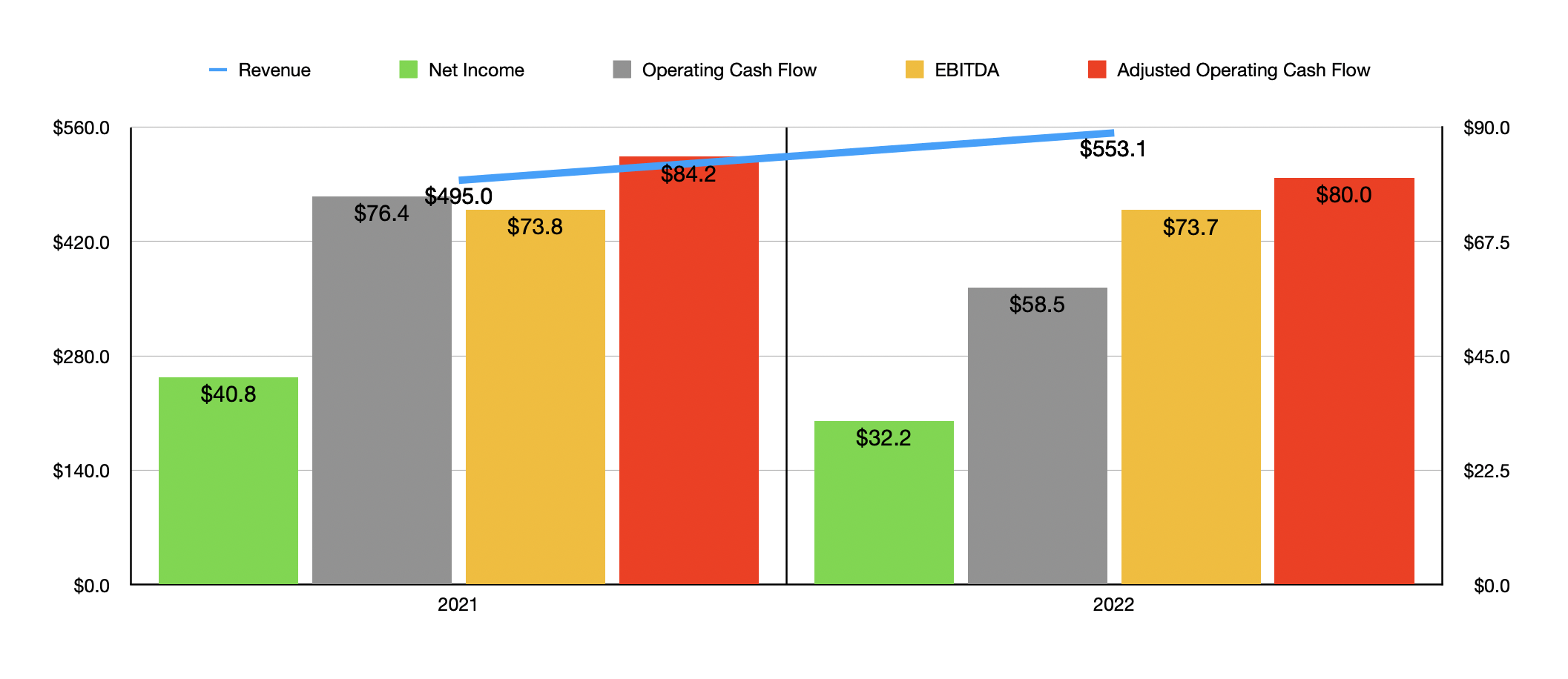

Several quarters now, the financial performance achieved by U.S. Physical Therapy has been undoubtedly mixed. Consider how the company ended its 2022 fiscal year . Revenue came in at $553.1 million. That's 11.7% above the $495 million reported one year earlier. But on the bottom line, the picture was worse across the board. Net income dropped from $40.8 million to $32.2 million. Operating cash flow declined from $76.4 million to $58.5 million. Even if we adjust for changes in working capital, we would have seen a drop from $84.2 million to $80 million. And finally, EBITDA for the company dipped ever so slightly from $73.8 million to $73.7 million.

{kind=link}

Author - SEC EDGAR Data

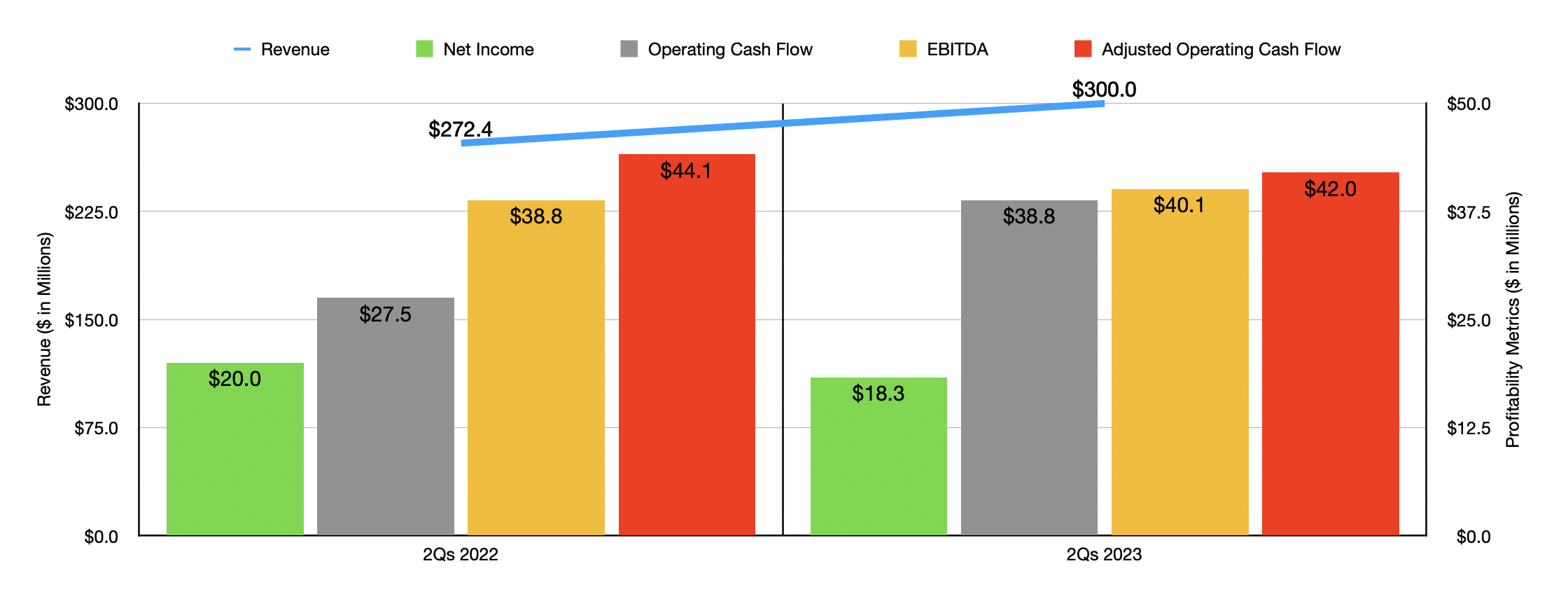

When we look at the more recent data provided, which covers the first half of 2023 relative to the same time last year, we see a very similar trend continue. Revenue of $300 million beat out the $272.4 million reported the same time last year. This increase was driven by continued growth in the number of clinics that the company has. At the end of the second quarter of last year, the firm had 600 clinics in operation. Today, that number is 656. But while the addition of clinics has helped the company's top line, mature clinics have also been a contributor to its expansion. Revenue associated with clinics that were added prior to 2022 grew 3.6% from $221.2 million to $229.1 million. This was driven entirely by a 4.2% increase in the number of visits at the mature clinics that the company has, with some of that increase offset by a modest drop in the net rate per patient visit from $103.09 to $102.56. And that was mostly because of a reduction in the net rate associated with Medicare visits due to a 2% Medicare rate reduction that began in January of this year as well as a discontinuation of sequestration relief on Medicare visits starting in July of 2022.

{kind=link}

Author - SEC EDGAR Data

The drop in revenue brought with it a decline in profits from $20 million to $18.3 million. Obviously, the new clinics hurt the company to some extent. However, mature clinics also saw a 3.3% rise in costs. The company was negatively affected by an increase in salary and related expenses from 56.9% of sales to 57.6%. Though this may not sound like much, when applied to the revenue generated in the first half of 2023, the bottom line was hit from this alone to the tune of $2.1 million. That accounts for more than 100% of the decline in net profits. Other profitability metrics were all over the place. Operating cash flow jumped from $27.5 million to $38.8 million. But if we adjust for changes in working capital, we get a decline from $44.1 million to $42 million. At the same time, however, EBITDA for the company grew from $38.8 million to $40.1 million.

{kind=link}

Author - SEC EDGAR Data

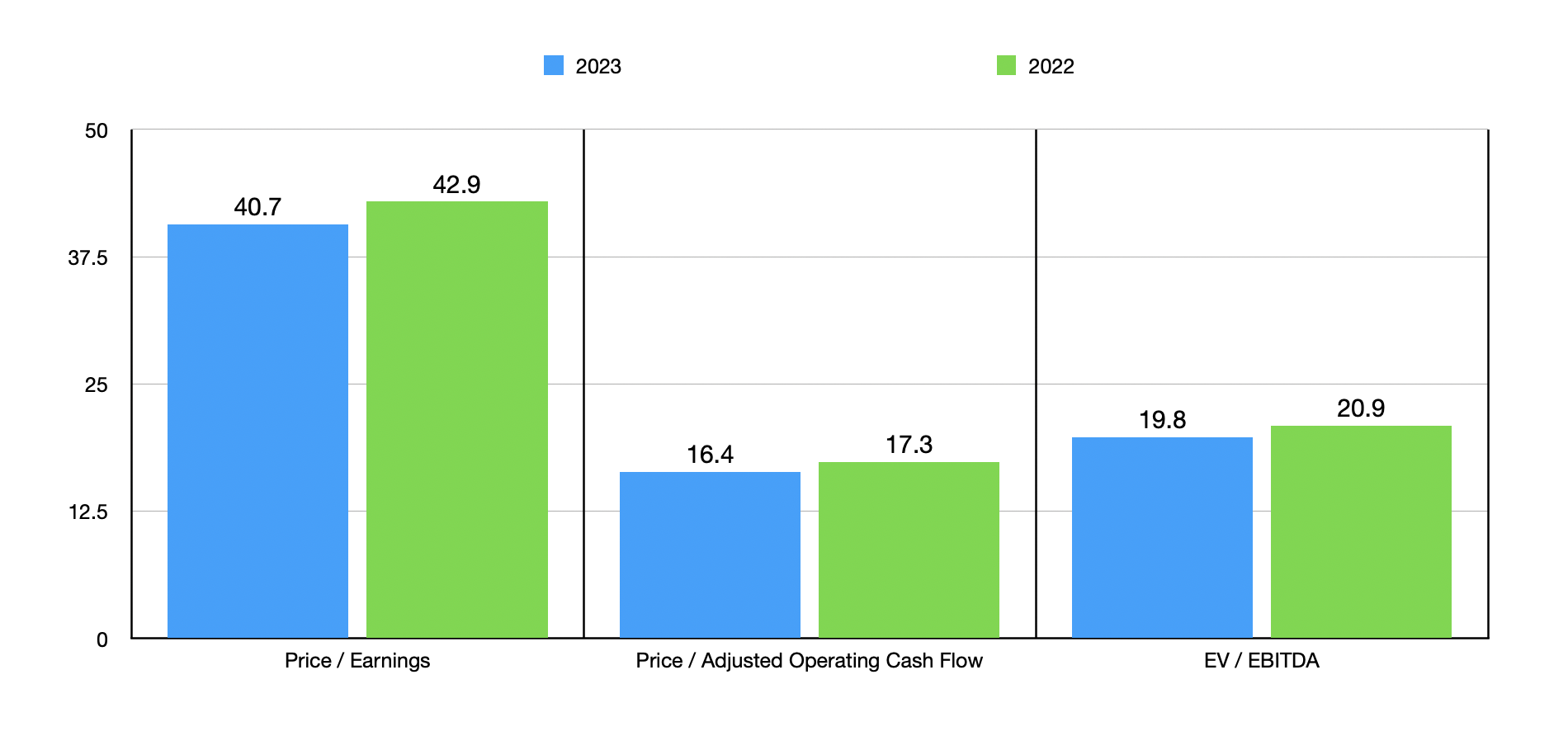

Management has not provided guidance for the rest of 2023. But if we annualize results experienced so far, we would expect net profits of $33.9 million, adjusted operating cash flow of $84.1 million, and EBITDA of $77.5 million. Using these figures, you can see how I priced the company as shown in the chart above. Even though the company does look cheaper across the board compared to what we would get using data from 2022, it is still quite pricey, especially when it comes to the price to earnings multiple. But it's not just this and the weakening in results that caused me to downgrade the business. In the table below, I also compared it to five similar firms. Using both the price to earnings approach and the EV to EBITDA approach, I found that our prospect was the most expensive of the group. And when it comes to the price to operating cash flow approach, three of the four companies that had positive results were cheaper than it is.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| U.S. Physical Therapy |

| 40.7 |

| 16.4 |

| 19.8 |

| Select Medical Holdings ( SEM ) |

| 15.1 |

| 7.5 |

| 9.5 |

| Encompass Health ( EHC ) |

| 21.1 |

| 9.8 |

| 10.1 |

| Pennant Group ( PNTG ) |

| 25.6 |

| 16.9 |

| 13.8 |

| Community Health Systems ( CYH ) |

| 1.3 |

| 1.5 |

| 7.0 |

| The Oncology Institute ( TOI ) |

| N/A |

| N/A |

| 7.0 |

Even though I have downgraded the company for now, this does not mean that I believe it's a bad prospect in the long run. The company has a fairly solid balance sheet, with cash exceeding debt by $9.7 million. This gives it a fairly solid balance sheet. The firm also operates in a rather sizable market with great upside potential. The US rehabilitation market, for instance, is a more than $30 billion market opportunity. By 2025, that market is expected to grow to more than $40 billion. And no single company has a market share exceeding 10%. This means that the industry is very fragmented and fragmentation can lead to opportunities for attractive growth by means of acquisition. And the company has not shied away from those types of opportunities since 2005, the firm has completed more than fifty different acquisitions, with some as small as three clinics and the largest at 52. There are also some attractive markets that U.S. Physical Therapy can grow into if it so desires. Even though it operates in 41 states, it has no clinics located in California or New York. Those immediately come to mind as attractive prospects given their size and population density.

Takeaway

All things considered, U.S. Physical Therapy it's still an interesting company and I do believe in its long-term potential. But with how shares are priced, both on an absolute basis and relative to similar firms, and with recent weakness on the bottom line, I do not have a great deal of optimism that the future will look much different than the past until something changes. I don't believe it's likely that investors who own the stock will have a high chance of losing money. But I do think that the risk of underperformance at this point is material. And it's because of that and other aforementioned factors that I have decided to downgrade the stock from a ‘hold’ to a ‘sell’.

For further details see:

U.S. Physical Therapy Remains Overpriced (Rating Downgrade)