ATVI - Ubisoft: Agreement With Activision To Drive Further Value

2023-08-24 07:00:00 ET

Summary

- Ubisoft recently announced that it had acquired the cloud gaming rights to Call of Duty and all other Activision Blizzard games released over the next 15 years.

- The cloud gaming industry has the scope to replace the traditional model, with forecasting suggesting a growth rate of >40%. With this acquisition, Ubisoft is positioned as a leader.

- Downside continues to be protected by the strategic quality of Ubisoft and its low valuation (4.4x NTM EBITDA), making it a highly attractive takeover target.

- Underpinning this recent announcement is continued positive development. The highly anticipated "Skull and Bones" is going into beta and is on track to release as expected.

- Further, the company comfortably beat expectations and is forecasting operating profits of €400m for FY24.

Current and prior thesis

We last covered Ubisoft in Apr-23, rating the stock a buy. Our thesis at the time was:

- Increasing recurring revenue should create greater income stability and improve margins.

- Its leading franchises will allow revenue to grow at a similar rate to what has been achieved historically.

- Ubisoft is cheap at its current valuation and represents a potential takeover target, significantly reducing the risk to current investors.

We believe these points are still valid and the development we expected (such as margin progression and growth) is on track. We have the following additions:

- The agreement with Activision Blizzard will position Ubisoft as one of the largest players in the cloud gaming space. Although the outlook of the industry remains uncertain, we expect material value to be generated from this transaction.

- Skull and Bones looks to be developing well, with this game having the scope to transform the growth potential of Ubisoft in the coming years.

We thus reiterate our buy rating.

Company description

Ubisoft Entertainment SA ([[UBSFY]], [[UBSFF]]) is a company that creates, publishes, and distributes video games for various platforms worldwide, including consoles, PCs, smartphones, and tablets.

Ubisoft is responsible for a range of titles, including Assassin's Creed, Far Cry, The Crew, Tom Clancy's, Prince of Persia, Watch Dogs, and 2048, among others.

Share price

Ubisoft's share price performance since Mar-23 has been fantastic, gaining almost 50%. As the trajectory illustrates, this has not been purely driven by the recent agreement but by a broad improvement in investor sentiment.

Activision Blizzard x Ubisoft Agreement

Ubisoft recently announced that it had acquired the cloud gaming rights to Call of Duty and all other Activision Blizzard ( ATVI ) games released over the next 15 years in perpetuity , once (/if) the Activision/Microsoft ( MSFT ) transaction closes.

Cloud gaming is a method of playing games using remote servers in data centers provided by gaming companies. There's no need to download and install games on a PC, reducing the financial cost to the end user.

This will allow Ubisoft direct access to offer these games, but also to license streaming access to Activision Blizzard's catalog of games to other gaming companies. The company will essentially have full control over the cloud gaming experience of these titles.

Activision Blizzard's titles include Call of Duty, Spyro, Sekiro, Tony Hawk, Candy Crush, WoW, and Diablo, among others. Taken in conjunction with Ubisoft's current portfolio, its cloud gaming offering will substantially increase.

This agreement is almost certainly to placate the UK regulator ((CMA)), who is now the biggest challenge to Microsoft's ability to close this deal. With this deal, Ubisoft will control the streaming rights to Activision Blizzard games outside of the EU and license titles back to Microsoft to be included in Xbox Cloud Gaming . The CMA raised concerns about Microsoft's control over the cloud gaming industry, implying it could grow to the point of replacing the existing way games are played.

Our view is that Ubisoft has hit the jackpot with this transaction, regardless of how the cloud gaming landscape develops in the coming years. Firstly, the Activision Blizzard IP it has gained is extremely valuable, particularly due to the volume of games released by the outfit. Activision Blizzard has an LTM Revenue of $8.7bn and is one of the most valuable gaming companies in the world.

Fortune Business Insight estimates that the global cloud gaming industry will grow at a CAGR of 47% into 2030, anticipating it to be the future of gaming. The development of the industry has been somewhat restricted thus far, as there is a need for high-speed internet (5G) globally to accommodate low latency and significant upfront investment in data centers/GPUs. The industry is in a "chicken-or-the-egg" situation, as consumers will only show interest if the infrastructure is in place but companies are reluctant to make the investment without certainty over future returns.

Despite these concerns, it feels inevitable that the industry will be given an opportunity to succeed. We believe this because if consumers could be convinced to move over, we see unit economics improving.

The cloud gaming segment represents the potential for incredible value as it reduces installation and download times, while not requiring the equivalent level of hardware. This should contribute to a significant increase in the number of gamers accessing the industry, particularly because it brings handhelds and other portable devices into the fold.

Further, Many of the cloud gaming platforms are positioning their offering as a subscription-based services, a natural development given the streaming concept. Subscription revenue is always preferable, as it creates greater certainty over future earnings and a higher lifetime value.

Additionally, this will propel Ubisoft in line with, if not ahead of, the other major gaming companies, including Electronic Arts ( EA ) and Take-Two Interactive ( TTWO ). From this point, Ubisoft could look to expand its library further, partnering with smaller studios to acquire their cloud gaming rights, and creating one of the largest cloud gaming offerings to consumers.

Equally, cloud gaming could be a failure. It arguably already is given the numerous attempts with little success. The primary roadblocks are:

- Latency - As discussed, the availability globally of sufficiently fast internet is critical.

- Thermodynamics - Although hardware requirements are less than running a AAA title directly on-device, there are still some technological limitations, namely keeping devices cool

- Reliability - In conjunction with the first and second points, the ability to provide a robust gaming experience is key. That means not being disrupted by internet dropouts, a device overheating, the battery running out if portable, and the potential for a subpar experience relative to direct ownership.

Finally, some have questioned whether the market is even large enough. The risk is that most "gamers" will still own powerful devices and so will prefer to own games. Further, console makers will continue to fight for their segment of the gaming industry. This leaves the casuals, many of whom are happy with the offering provided by the Apple (AAPL) / Android ( GOOG ) app stores.

Realistically, I believe the industry will land in the middle. Cloud gaming will move toward the mainstream but the idea of it becoming the primary conduit for gaming, at least in the next 15 years, feels unlikely.

We will be interested to see how this strategically develops in the medium term. With such power given to Ubisoft+, Microsoft is unlikely to allow Ubisoft to mismanage its IP, especially if it looks like cloud gaming is going to be the future. This could mean some form of partnership or collaboration between Ubisoft+ and Xbox's Game Pass, further enhancing the value for Ubisoft.

Finally, to add a little more food for thought. This agreement, as mentioned several times already, suddenly makes Ubisoft incredibly powerful and inherently tied to Microsoft. At an EV of c.€4.6bn, this begins to look like a lucrative strategic acquisition. By whom? Microsoft? (Round 2 vs. the CMA - maybe not given the size of the transaction), Sony? (far more interesting and more realistic), or Take-Two after it releases GTA 6?

Other matters to consider

Skull and Bones

Ubisoft's much anticipated Skull and Bones game goes into closed beta, opening to the public with (interestingly) no NDA. This game has been in development for a decade, with numerous delays and growing hype.

The game is an MMO, with a large amount of content and explorable regions (developing over time with additional content). The expectation for this game is to garner a big player base who continue to play for an extended period. There is no current release date, although rumors suggest " 2023-2024 ".

With the lack of NDA and beta availability to the public (Even I have an invite), Ubisoft is clearly extremely confident this game will go down well with consumers. The success of such games has the potential to materially improve the trajectory of the business, and we are quietly confident.

Q1 results

{kind=link}

Bookings (Ubisoft)

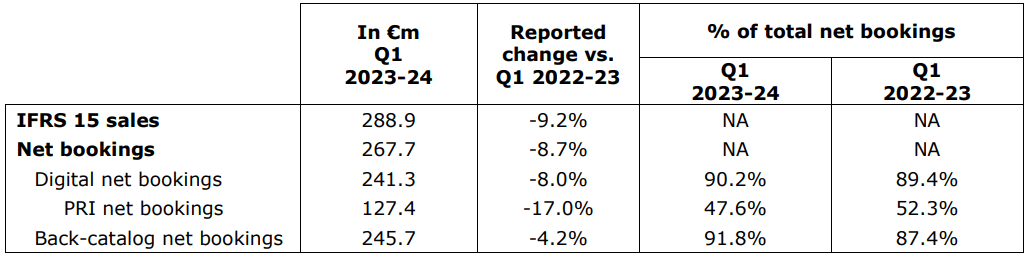

Ubisoft announced net bookings of €267.7m in Q1, a decline of (9)% compared to the prior year, but importantly, ahead of expectations by 16%.

Management was broadly positive on the quarter, seeing improved customer engagement and sentiment (importantly, for its upcoming free-to-play games), as well as good development toward new releases. Further, another Assassin's Creed mobile game was announced, a segment we are highly bullish on.

Finally, the board has nominated two additional independent directors, both of whom have extensive experience within the industry and should support further operational improvement toward financial enhancement.

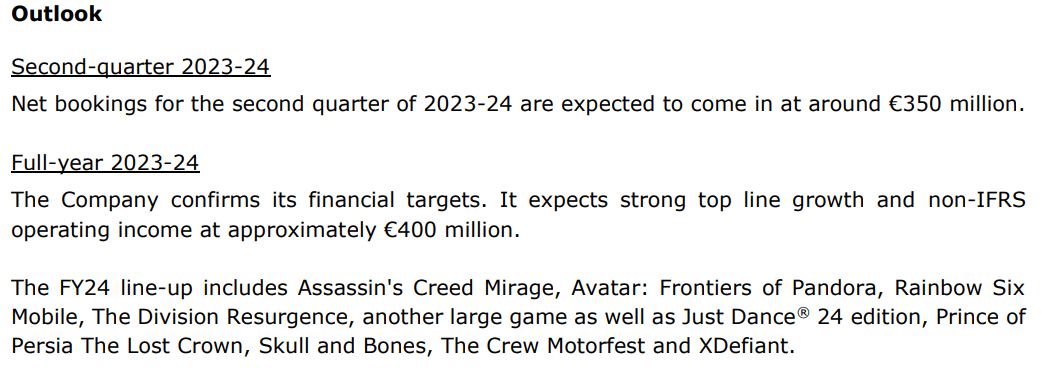

Management's outlook for FY24 is positive, with further gains in Q2, culminating in a substantial improvement in margins. With the improvement already observed thus far, and the current lineup yet to be released, we broadly consider this assessment reasonable.

{kind=link}

Outlook (Ubisoft)

Valuation

Ubisoft is currently trading at 4.4x NTM EBITDA, significantly below the larger peers we identified previously. To quote our prior analysis "At 3.8x EBITDA, you have to ask yourself what are you buying, and the answer is a business with the capacity to generate a 40% EBITDA-M". Our view has not changed.

Conclusion

We consider the gaming industry to be incredibly attractive due to the stickiness of demand and the development of a highly lucrative business model. Cloud gaming presents the opportunity to extend this further, as the uncertainty of box/in-game sales is eliminated via a subscription model.

The Activision agreement cannot be described as a once-in-a-lifetime opportunity because no logical market participant would ever agree to this. Ubisoft has been given an incredible opportunity and must exploit this by doing its part in developing the cloud gaming industry.

Even if this does not play out, we believe the company is developing well and should see renewed investor interest as its financial performance improves.

For further details see:

Ubisoft: Agreement With Activision To Drive Further Value