UBSFF - Ubisoft: Agreement With Microsoft Is A Very Positive One

2023-09-22 12:27:49 ET

Summary

- Ubisoft Entertainment SA has the potential to grow and become more valuable if the deal with Microsoft passes.

- Ubisoft Entertainment's potential exclusive cloud streaming rights from the Microsoft partnership position it well in the growing cloud gaming market.

- Ubisoft risks include deal failure and execution challenges.

Summary

I am recommending a buy rating for Ubisoft Entertainment SA (UBSFY), as I see huge potential for the business to grow and become much more valuable if the deal with Microsoft (MSFT) passes. That said, given that the agreement is contingent on the deal between MSFT and Activision Blizzard (ATVI) going through, I would recommend a small weight in the position just to be safe.

Business

Ubisoft Entertainment SA produces, edits, and distributes video games, as well as developing educational software. The company is known for many popular games around the world, such as Far Cry , Assassin's Creed , Silent Hill , etc. The majority of revenue is generated from the PlayStation game console (40% of FY23 revenue), with 31% from mobile, 18% from PC, and 11% from others. UBSFY has ridden the rising trend of gaming through the past decade, growing net bookings from EUR870 million in 2010 to EUR1.7 billion in FY23. Notably, across the same period, adj. EBIT went from EUR29 million to EUR408 million, indicating the operating leverage within the business. However, profitability got a big hit in FY23, dropping to -EUR500 million, and management is now aiming for a turnaround.

Valuation

{kind=link}

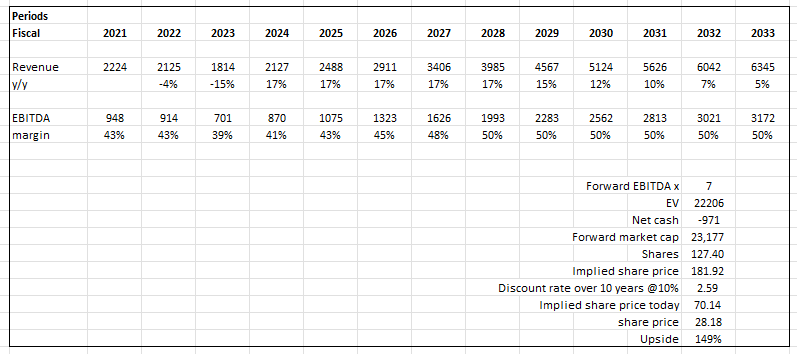

Based on my view of the business, if the agreement with Microsoft passes, UBSFY is worth much more than it is today. I used a 10-year discounted cash flow ("DCF") model to illustrate the potential worth of the business. The reason for 10Y is because the cloud industry is still in its nascent stages, so in order to capture that value, a longer time horizon is required. I used consensus FY24 revenue as a base and expect growth to maintain at the high-teen level (truth be told, growth could be higher , but I modeled high-teens to be conservative). As for EBITDA margins, I expect margins to step up gradually as the business has inherently operating leverage.

If UBSFY executes as I expected, its multiple should rerate upwards to where peers in developed countries are trading (such as Ncsoft Corp. and Krafton Inc.).

Comments

Touching a little on the recent quarter 1Q24 net bookings, it is true that it is one of the weakest quarters in the company's history; UBSFY Q1 2024 net bookings (EUR 268 million) were among the lowest. With no significant releases happening during the quarter, this was to be expected. The important thing to note is that net bookings came in better than guided, driven by stronger back-catalogue dynamics. Furthermore, management has reaffirmed its FY24 financial goals, which include robust revenue expansion and non-IFRS operating income of EUR400 million due to a strong release schedule. The problem with UBSFY is that its reputation has been damaged in recent years due to several guidance cuts caused by game delays and other factors. Thus, I think the market is very concerned about execution here, despite the robust future pipeline. This is probably also the main reason why UBSFY is trading at a significant discount to its competitors.

Coming to the primary focus of this post: the agreement with Microsoft . Upon closer examination, I believe that UBSFY has the potential to evolve into a considerably stronger company, warranting a revision in its current valuation metrics. Under the terms of the Microsoft partnership, UBSFY gains exclusive cloud streaming rights to the entire ATVI Blizzard library and all forthcoming titles for the next 15 years. This exclusivity encompasses global territories except for the European Economic Area, where it is non-exclusive.

In my view, this is an exceptionally favorable outcome for UBSFY. The company now has the option to leverage ATVI content to enhance its own subscription service or license streaming access to AVTI Blizzard content to other cloud gaming firms, service providers, and console manufacturers. Given UBSFY's relatively modest size, it poses no regulatory risk in the realm of cloud-based gaming and doesn't present a significant competitive challenge to Microsoft, making it the ideal recipient of this agreement. That said, its size also renders it a dependable partner in alleviating regulatory concerns.

Crucially, in recent years, UBSFY has built infrastructure such as Uplay+, Uplay multi-pass, and Ubisoft Connect, facilitating gameplay on a wide array of platforms including Luna, Microsoft, PC, and PlayStation. Additionally, it has demonstrated its proficiency in managing and monetizing intellectual property.

The cloud gaming market may be in its infancy, but there is undoubtedly a long-term opportunity that UBSFY can take advantage of. UBSFY would be in a strong position to license the streaming rights to the world's most valuable collection of titles to other players in the cloud gaming industry if it were able to acquire these rights. Therefore, if this deal materializes, I expect these licensing revenues to grow significantly in the future, particularly as cloud gaming continues to gain widespread adoption.

Risk & Conclusion

The risk to my investment thesis is that: (1) the deal might not go through and the upside from this agreement with MSFT will be worthless; and (2) UBSFY might continue to fail in executing well (games delay and what not), which will further reduce the creditability of management in the market, further weighing on the stock price.

In conclusion, I recommend a buy rating for Ubisoft Entertainment SA. The primary focus remains on the Microsoft agreement, which grants UBSFY exclusive cloud streaming rights to ATVI Blizzard content. This positions UBSFY to thrive in the evolving cloud gaming landscape. However, risks include the deal falling through and ongoing execution challenges, which have impacted market confidence. However, it's essential to exercise caution given the deal's reliance on the successful completion of the MSFT and ATVI transaction.

For further details see:

Ubisoft: Agreement With Microsoft Is A Very Positive One