CSAN - Ultrapar's Impressive Q3 Performance Raises Valuation Concerns

2023-11-28 17:33:43 ET

Summary

- Ultrapar reported robust Q3 results, capitalizing on an oversupply of fuels and increased Russian diesel imports, leading to lower acquisition costs and significant year-over-year bottom line improvements.

- Despite a strong Q3, Ultrapar foresees inventory losses in Q4 due to an 11% premium on fuel prices in Brazil compared to international parity, signaling a more cautious outlook.

- Ultrapar's shares surged triple digits in 2023, raising valuation concerns. A discounted cash flow model implies a potential 28% downside, prompting a neutral stance.

In my initial article about Ultrapar ( UGP ), the Brazilian company operating in the fuel distribution sector through Ipiranga and Ultragaz, I maintained a neutral stance towards the significant price appreciation in the year's first half. Given the fuel scenario in Brazil, characterized by an oversupply of fuel and increased imports of Russian diesel, the sector experienced atypical conditions.

Consequently, I viewed Ultrapar's medium to short-term performance as somewhat speculative, making it vulnerable to fuel price and demand trends on Brazilian soil.

However, staying on the fence has its consequences. Since then, Ultrapar's shares have continued to rise, showing no signs of pausing in the face of a third quarter marked by solid results and an impressive margin expansion trend within its sector. This trend reflects lower acquisition costs due to the fuel oversupply.

Ultrapar anticipates a significant influx of imported fuel into Brazil by the end of the year and is contemplating adjusting fuel prices downward to maintain competitiveness.

However, when assessing Ultrapar's valuation using my discounted cash flow model, the substantial appreciation of the company's share price throughout the year suggests it is trading at an implied value approximately 28% below the current share price.

Therefore, despite Q3 showcasing the company with the most attractive margins in fuel distribution and presenting good potential for future growth, particularly with Ultragaz in LPG, I am maintaining my neutral recommendation due to the potentially stretched valuation.

Ultrapar's 3Q23 Financial Results

In the third quarter of 2023, Ultrapar reported a net income of R$891.2 million, representing a substantial increase of 978.9% compared to the R$82.6 million reported in 2022.

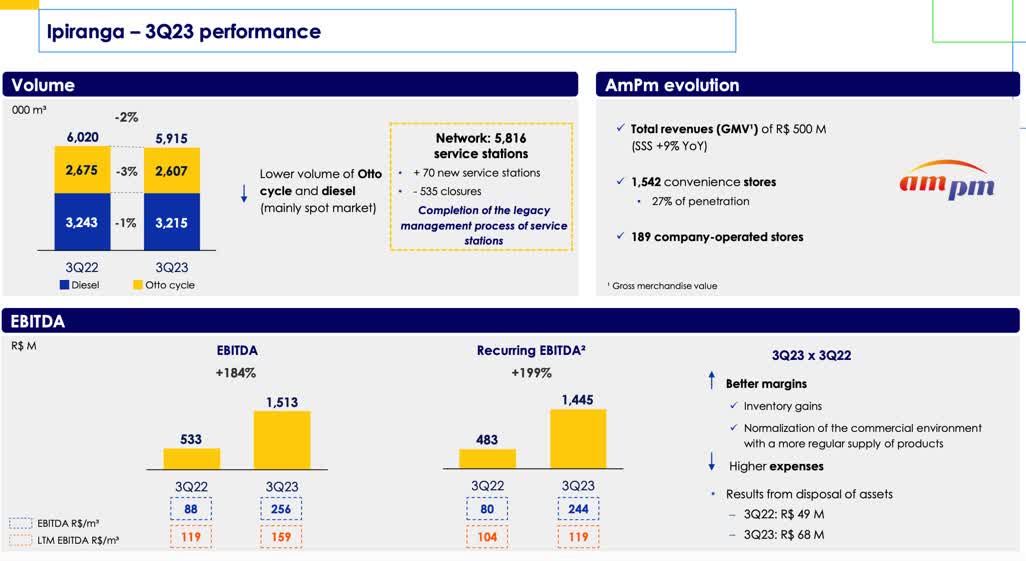

The adjusted EBITDA for 3Q23 reached R$2 billion, indicating a noteworthy surge of 139% compared to the results in 3Q22. The company attributes these improved results to the enhanced performance of all operations, particularly emphasizing the Ipiranga network, its most crucial business segment.

Total net revenue for the third quarter of 2023 amounted to R$32.5 billion, reflecting an 18% decrease compared to the same period in 2022. Net revenue from Ipiranga alone was R$29.5 billion, representing an 18% decline from the previous year's third quarter. The results report explains that this decline results from reduced fuel costs and decreased sales volume.

Despite a 2% decrease in volumes sold, Ipiranga's EBITDA increased by 184% compared to the previous year's third quarter. The higher EBITDA was mainly due to inventory gains caused by increased fuel costs throughout the quarter and a more regular product supply in the market. The company is focused on further enhancing its position in the market and aims to achieve a return on investment of about 20% in the fuel distribution sector.

{kind=link}

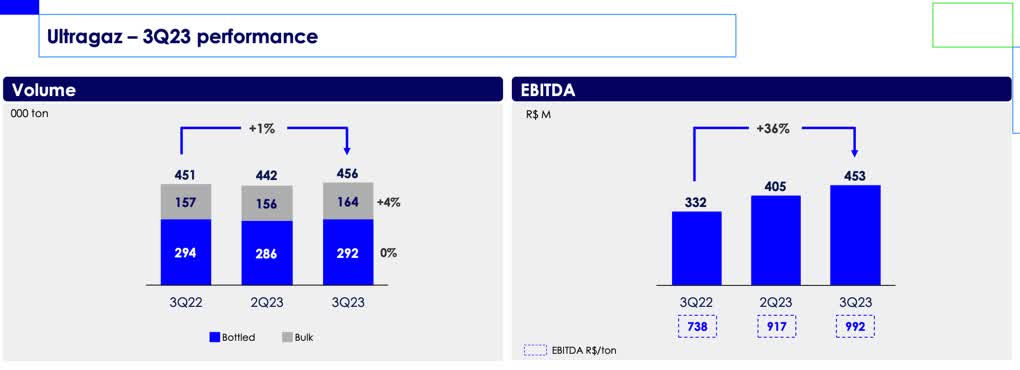

Regarding Ultragaz, the volume of LPG sold in this third quarter was 1% higher year-over-year, driven by a 4% increase in the bulk segment due to higher sales to industries. Ultragaz SG&A in this third quarter was 15% higher than that of the third quarter of 2022 due to two manufacturers' expenses with freight due to higher sales volume and higher expenses with personnel.

Ultragaz's EBITDA totaled R$453 million, marking a 36% increase year-over-year. This growth is primarily explained by efficiency and productivity initiatives implemented in the last quarters, a better sales mix, and inflation pass-through despite higher expenses.

{kind=link}

Conversely, the overall adjusted EBITDA experienced a remarkable increase of 199%, reaching R$1.4 billion. This surge is attributed to improved margins and a normalization of the commercial environment.

Ultrapar's net financial result was negative at R$301 million in the third quarter of 2023, indicating an 8% increase in economic losses compared to the same period in 2022.

The company's net debt stood at R$7 billion, reflecting a decrease of 4.9% compared to the same period in 2022. The financial leverage indicator, measured by net debt/adjusted EBITDA, was 1.4 times in September 2023, indicating a 0.5 percentage point decrease compared to the same period in 2022.

Enhanced Profit Margins in Fuel Distribution

In the third quarter of 2023 (3Q23), a more favorable commercial environment and inventory gains improved profit margins for fuel distribution companies. The market dynamics in the year's first half, characterized by product oversupply and increased imports of Russian diesel, created atypical conditions in the sector. Russia emerged as the primary fuel supplier to Brazil in 2023, surpassing the USA. This resulted in significant outperformance by distribution companies such as Ultrapar, Vibra Energia ( PETRY ), and Raízen, a Cosan ( CSAN ) subsidiary, in Brazil, exceeding market expectations and causing notable changes in their balance sheets compared to the previous year.

During Ultrapar's third-quarter conference call , the anticipation of inventory losses for 4Q23 was highlighted. This is attributed to fuel prices in Brazil currently exceeding international parity. Since the beginning of the year, under Petrobras' ( PBR ) new management, the company abandoned international oil parity (IPP) and set its prices. In August, the price lag reached 45%, prompting a surge in fuel prices in the country.

Ultrapar anticipates a substantial influx of imported fuel into Brazil by year-end and is contemplating adjusting fuel prices downward to remain competitive. The company notes that the current fuel price in Brazil, as of November, carries a significant premium of 11.3% compared to international prices, potentially leading to increased product imports.

CEO Marcos Lutz emphasizes the expected loss of inventory value for 4Q23 and the likelihood of reduced fuel prices, potentially causing increased market volatility. The CEO also expressed concerns about specific companies in the sector operating outside established rules, making the business environment highly risky.

For the second half of 2023, Ultrapar's primary focus remains on strengthening its balance sheet and improving operations, particularly in response to the volatile fuel prices, which are notably impacting Ipiranga. The ongoing restructuring of Ipiranga encompasses four strategic pillars: pricing, logistics, negotiation, and network engagement. The management of Ultrapar underscores a comprehensive overhaul of the pricing area, with increased efforts expected in the commercial pillar through AmPm convenience stores.

Valuations

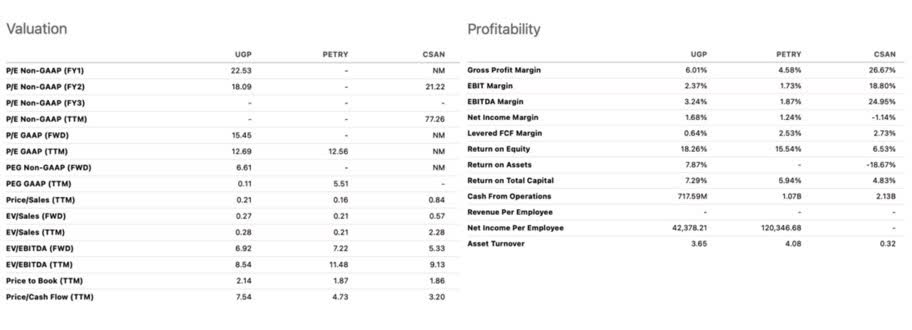

In the Brazilian gas station landscape, the primary distributors, namely Ipiranga (Ultrapar), Petrobras Distribuidora (Vibra Energia), and Shell (Raízen, a subsidiary of Cosan), present distinct valuation dynamics. Ultrapar trades at a discount in valuation multiples when comparing EV/EBITDA but at a substantial premium when evaluating price/cash flow. Notably, in a comparison between Ultrapar and Vibra Energia, both companies exhibit similar margins, with Ultrapar holding a slight advantage.

{kind=link}

Considering that Ultrapar shares have surged by 127% throughout 2023 until the end of November, aligning with a fuel scenario in Brazil that was much less dire than anticipated, the company is now trading at a multiple that, in my view, is considerably more stretched than justified.

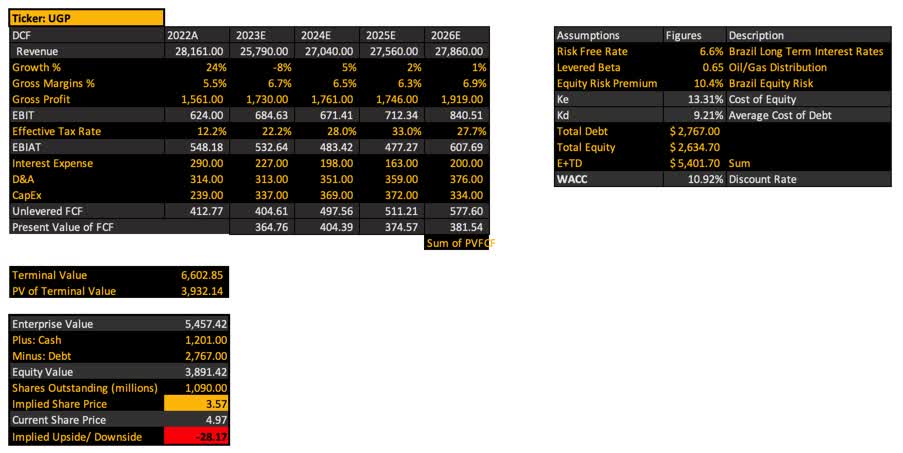

According to my discounted cash flow ((DCF)) model, which relies on estimates from S&P Global Intelligence and employs a weighted average cost of capital ((WACC)) of 10.9%, the implied value of Ultrapar should be $3.57 per share. This suggests a current downside of 28% from the share price on November 28, which stood at $4.97.

S&P Global Intelligence, Company's filings, table compiled by the author.

{kind=link}

The Bottom Line

Ultrapar reported a robust performance in the third quarter, benefiting from an oversupply of fuels in Brazil and increased imports of Russian diesel, resulting in lower acquisition costs for fuel resale. This led Ultrapar to significantly surpass market expectations and achieve substantial year-over-year improvements in its bottom line.

However, expectations for the next quarter are more cautious, with the company itself forecasting inventory losses for Q4 (a reflection of the oversupply of fuels). This anticipation is attributed to Brazil's current 11% premium on fuel prices compared to the international parity price.

In light of these factors, I believe that while the worst may be clearly behind Ultrapar, the potential for further significant gains may be limited, especially considering its triple-digit rise in share price this year. In my assessment, this surge positions the company at a premium valuation. Therefore, I will maintain my Neutral rating on Ultrapar stock for Q4 as well.

For further details see:

Ultrapar's Impressive Q3 Performance Raises Valuation Concerns