ECCV - Undervalued And Unique High Yield Baby Bonds From Oxford Lane And Eagle Point Credit

2023-06-22 12:00:00 ET

Summary

- As far as I know, Oxford Lane and Eagle Point Credit are the only closed end funds which offer baby bonds making these baby bonds unique.

- I will show that the strict leverage limits on closed end funds plus preferred stock protection make these closed end funds virtually bankruptcy proof.

- While the baby bonds from OXLC and ECC are unrated, I would rate them “A-”, but the market mistakenly treats them as junk bonds.

- While I estimate fair yield-to-maturity (YTM) for these relatively short term baby bonds at around 6.0%, they can currently be had with 8.3% YTM (except overvalued ECCX).

- I consider these very undervalued baby bonds from OXLC and ECC to be “must own” core holdings and they are the largest position in my personal portfolio.

Eagle Point Credit and Oxford Lane Capital

Eagle Point Credit ( ECC ) and Oxford Lane Capital ( OXLC ) are closed end funds (CEFs) that trade on the stock exchange (public). Both hold a diversified portfolio of CLO (Collateralized Loan Obligation) equity tranches. While equity tranches are the riskiest tranches of CLOs, the yields on them are very high allowing these CEFs to pay very high dividend yields and their popularity has resulted in the CEFs generally trading at a premium to NAV (Net Asset Value).

ECC and OXLC not only purchase CLOs with their equity but both ECC and OXLC also sell preferred stock and baby bonds in order to raise money to invest in higher yielding CLOs. So they want to generate additional income off of the yield spread between the yield they are getting on CLOs and the yield they must pay on their preferred stocks and baby bonds.

While preferred stocks issued by CEFs are generally very highly rated, ECC and OXLC are the only CEFs that I know of that issue preferred stock and additionally bonds. This makes the bonds super protected because they are ahead of the preferred stock in the capital structure.

ECC and OXLC Baby Bonds

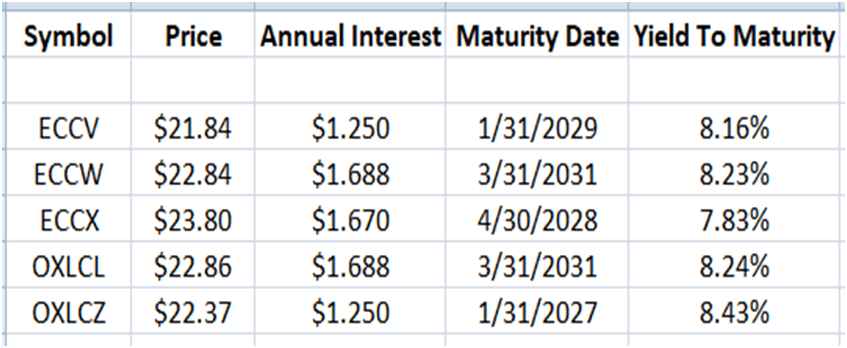

OXLC has 2 baby bonds with symbols OXLCL and OXLCZ. ECC has 3 baby bonds with the symbols ECCV, ECCW and ECCX. All mature at $25.00. Here is the relevant data:

{kind=link}

As you can see, the “Yield to Maturity” (YTM) is around 8.25% except for ECCX. Anyone owning ECCX would do well to swap it for one of the others as it is relatively overvalued and also has less upside should we see a rally in the sector.

For those who want somewhat less price volatility, a bit more safety given the shorter duration, and a YTM that surprisingly is better than the YTM on the longer term bonds from ECC and OXLC, OXLCZ is the best value. Personally, this is my largest holding here as the YTM looks very attractive for a quality bond with only about 3.5 years until maturity.

But, if after reading this article, you agree with me that these are excellent yielding bonds given the risk, you might like to lock in these yields for a longer time. I have done that as well with smaller positions in OXLCL, ECCW and ECCV and have created a ladder.

Why I Believe OXLC and ECC Baby Bonds Are So Undervalued

- No preferred stock issued by a CEF has ever gone bad, thus these baby bonds, which are higher in the capital structure than the preferred stocks issued by ECC and OXLC, are of extremely high quality.

- CEFs are only allowed leverage of up to 50%. Both ECC and OXLC operate well below that with leverage of 31% and 40% respectively. If the value of their CLO portfolio starts to fall such that they are at risk of violating the 50% leverage limit, they generally simply issue more shares of common stock to raise cash. They can also lower leverage by buying back debt or selling assets, but issuing additional common stock seems to be the method of choice for OXLC and ECC.

- If a company must keep leverage below 50%, it must always have a positive net asset value ((NAV)) and therefore cannot go bankrupt (outside of an asteroid striking the earth and crashing every investment overnight). This is why no CEF has ever gone bankrupt (or at least a large part of the reason).

- Legal leverage allowed on bonds issued by a CEF is only 25%, twice better than the leverage limits on CEF preferred stocks which have never gone bad. Thus, these baby bonds are extremely well protected. Currently the leverage on OXLC baby bonds is only 16% while ECC bonds are leveraged at only 20%. When a company is legally required to have assets that are at least 4 times the size of their debt, it doesn’t get much better than that. And their assets are marked to market so they won't have the problems that banks are currently facing.

A Closer Look At OXLC

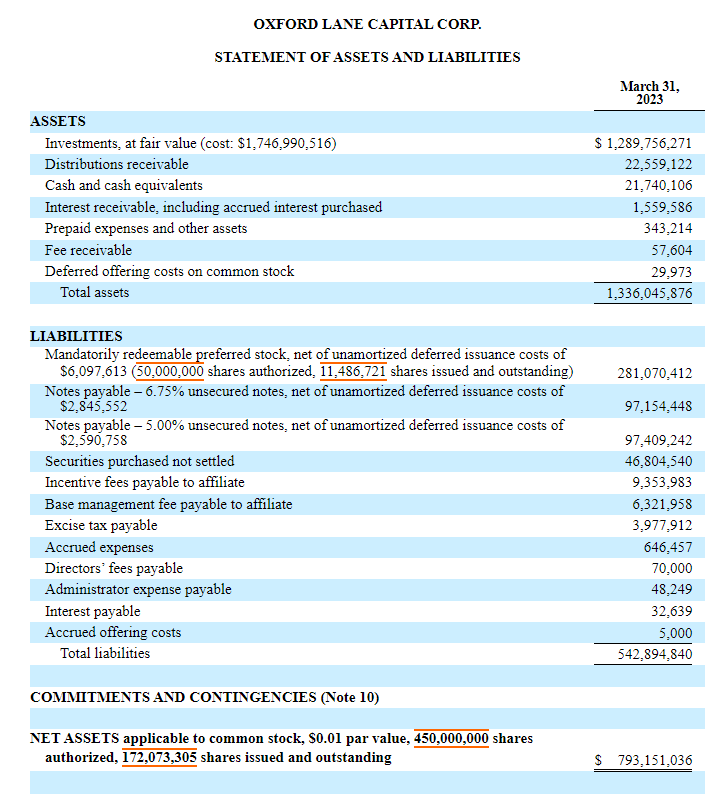

Basically the case for OXLC can be extrapolated to ECC as well. Here is the OXLC balance sheet.

{kind=link}

As you can see under “Liabilities”, OXLC has 2 baby bonds (notes payable) totaling $195 million. This is covered not only by $793 million of equity (Net Asset Value) but also by $281 million of preferred stock. Not only does OXLC have large common equity coverage but they also have 4 preferred stocks outstanding which provide protection for the 2 baby bonds.

Since the bonds are highest in the capital structure, you can also look at OXLC as having $1336 million in assets covering only $195 million of bonds (debt). So just super asset coverage.

In 2023, OXLC had $185 million in EBI (earnings before interest and preferred stock dividends). Since annual interest on their 2 baby bonds amount to only $11.5 million annually, interest on these baby bonds is covered a whopping 17 times.

Since leverage limits should always keep OXLC with a positive NAV, this really doesn’t matter, but if OXLC went to a large negative NAV of $250 million, only the preferred stocks would be hit. The baby bonds would still achieve a full recovery. Thus, I see these baby bonds as virtually bulletproof. That doesn’t mean the price of these baby bonds won’t fluctuate or can’t go lower in the short term, but that you will get your interest payments every 3 months and have your bonds redeemed at $25 on their maturity dates.

Fair Valuation of OLXC and ECC Baby Bonds

Preferred stocks of CEFs that have credit ratings are rated very highly, generally in the “A” range. This is because 1) they have diversity in their portfolios (although the portfolios may be all common stocks or all debt instruments that are often illiquid), but even more importantly because they have leverage limits which were instituted to protect the public from having CEFs take huge dives in price/NAV.

While it is true that CLO equity is considered risky, I don’t know how much riskier they really are versus common stocks. I can’t really find that information. But in looking at a CEF with the symbol OPP, I see that its preferred stocks are rated “A1”, but I also that it has 35% leverage, much more than the 16% leverage of OXLC baby bonds. I also see that they have large positions in small business loans, non-agency MBS and in high yield. I also see that OXLC and ECC have outperformed this CEF. So what should the bonds of OXLC/ECC be rated relative to the “A1” rated preferred stock of OPP. I would say that 2 notches lower at an “A3” rating would be fair given that we are comparing bonds with preferred stocks, and the leverage on these bonds are much lower than the leverage on the preferred stocks of OPP. This rating would put the preferred stocks of OXLC and ECC at a BBB rating, 4 notches below the preferred stocks of OPP. That seems very reasonable to me, though others may see it differently.

Given that bonds in the “A3” ratings category, with maturities similar to the OXLC and ECC baby bonds, have a YTM of around 5.5% to 6%, I would say that 6% would be a fair yield on these baby bonds. So their current 8.25% YTMs are just outstanding for such high quality baby bonds.

This is why baby bonds from OXLC and ECC hold the largest position in my personal investment portfolio. These are sleep very well at night bonds that also offer high yields with relatively short maturities. That is not easy to find.

Summary

As I laid out in the article, the baby bonds of ECC and OXLC (OXLCZ, OXLCO, ECCV and ECCW) are extraordinary values. If I were rating them, they would be strong investment grade and yet they have YTMs of around 8.25% versus 5.5% to 6.0% for similar quality bonds.

CEFs, like OXLC and ECC, are only allowed 25% leverage on their bonds. In other words, their assets must be at least 4 times their debt. This means that the NAVs of ECC and OXLC should never go negative and thus a bankruptcy is just not in the cards. These bonds are rock solid.

Because the bonds are not only at the top of the capital stack but are also quite small in value relative to the company’s assets, the coverage on these bonds is fantastic. In 2023, OXLC’s EBITDA covered the bond interest by 17 times and asset coverage is also enormous.

OXLC and ECC baby bonds are really special securities. They are unique in that they are bonds issued by CEFs. I am not aware of any other CEF that has issued bonds.

In my personal portfolio, OXLC and ECC bonds are my largest position. When you can find high yield combined with sleep very well at night quality, this is a big investment opportunity. When the market just doesn’t get it, and the mispricing is huge, these are the times when you can make some really concentrated investments.

For further details see:

Undervalued And Unique High Yield Baby Bonds From Oxford Lane And Eagle Point Credit