UNCRY - UniCredit: Beat Across The Board

2023-05-04 04:49:32 ET

Summary

- Superior CET1 ratio even considering the 2022 share buyback.

- Record profit at €2.1 billion in the first quarter.

- Higher 2023 guidance supported by solid capital generation. Our buy rating is then confirmed.

UniCredit ([[UNCFF]], [[UNCRY]]) delivered a solid set of numbers. The Milanese group, led by CEO Andrea Orcel, closed the 2023 first quarter beating the analyst's consensus across the board and raising its yearly guidance. It was a good call to increase ' UniCredit Earnings Estimates Before Q1 ', and here at the Lab, we are not surprised to see a plus 5% at the stock price level.

UniCredit Financials in a Snap

{kind=link}

Q1 updates and our take

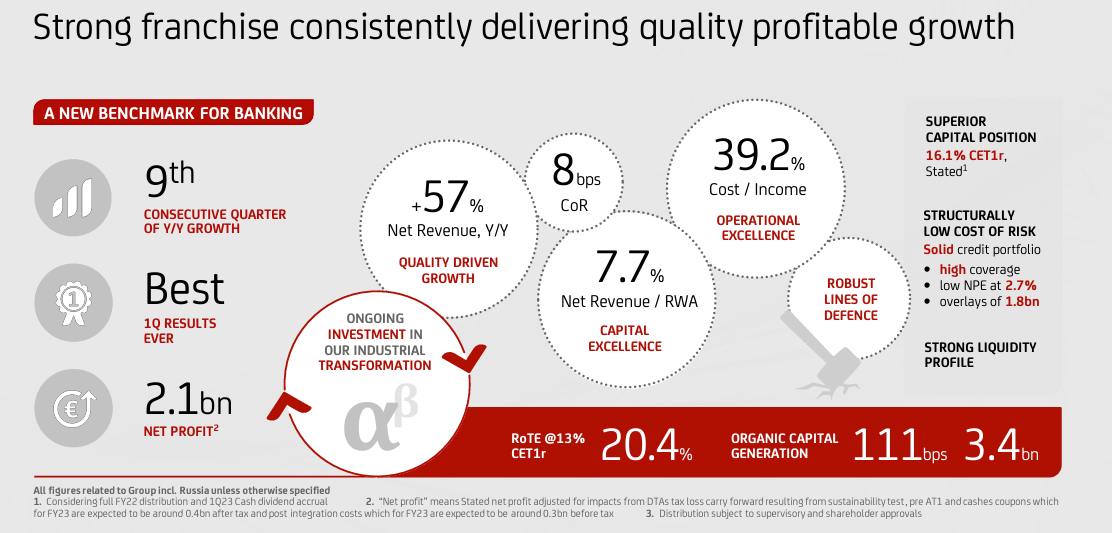

In Q1, the bank closed with revenues at €5.930 billion, up 18.3% on a yearly basis and above consensus expectations set at €5.292 billion. In detail, net interest income delivered €3.3 billion thanks to higher customer spread due to higher rates. There was pressure on loan volumes, but UniCredit sees NII estimates above €12.6 billion for the full year. Trading revenue increased by €500 million and a solid performance was also recorded in fee income thanks to higher volumes despite lower asset under management investment fee generation. In numbers, UniCredit reached €2 billion with a plus 11% on a quarterly basis.

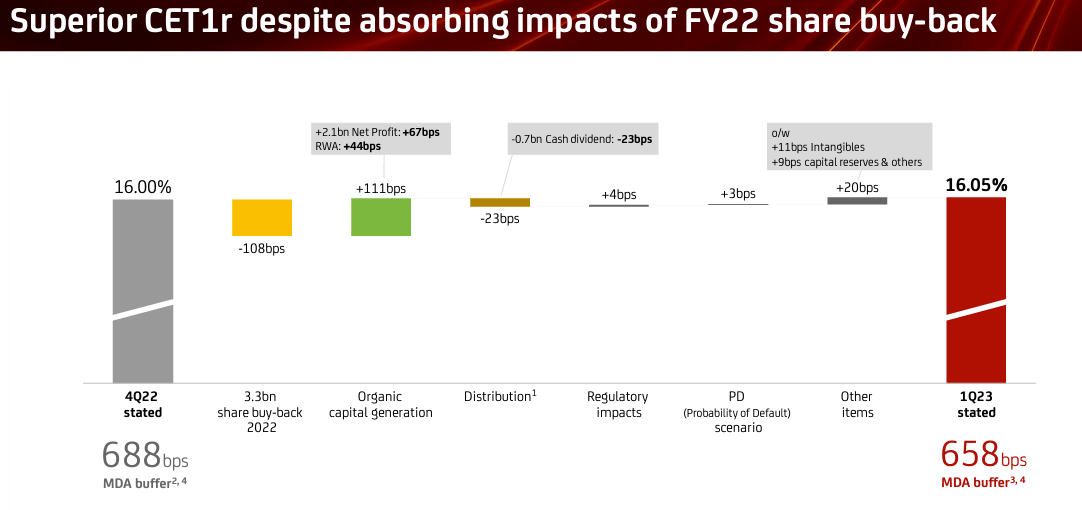

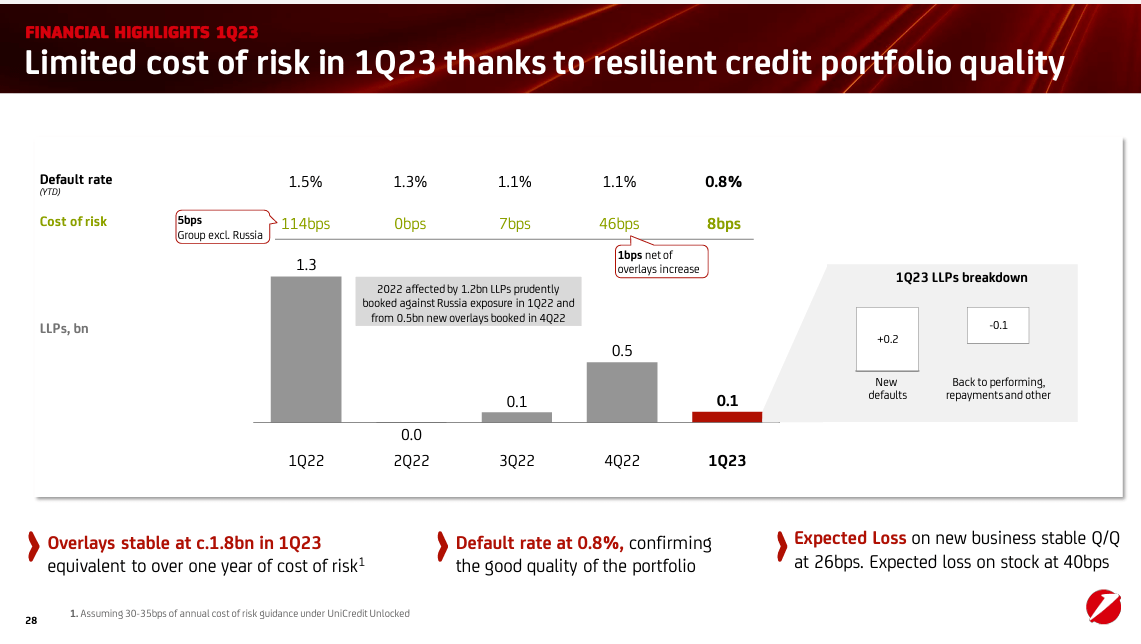

Operating costs fell to €2.32 billion and were down by 0.6%. This was driven by disciplined HR cost management and simplification. As a consequence, operating profit reached €3.6 billion (again a 24% beat). In addition, provision significantly fell and the cost/income ratio was down 7% at 39.2%, while net profit reached €2.06 billion and almost tenfold compared to the €274 million achieved a year ago when the group had to write down the Russian subsidiary. Moreover, with a cost of risk at just 8 basis points (Fig 1), in terms of capital solidity, the CET 1 ratio reached 16.05% in the quarter and in asb value was 2.1% higher than the 2022 end (expectations were set at 15.25%) - Fig below.

UniCredit CET 1 ratio evolution

{kind=link}

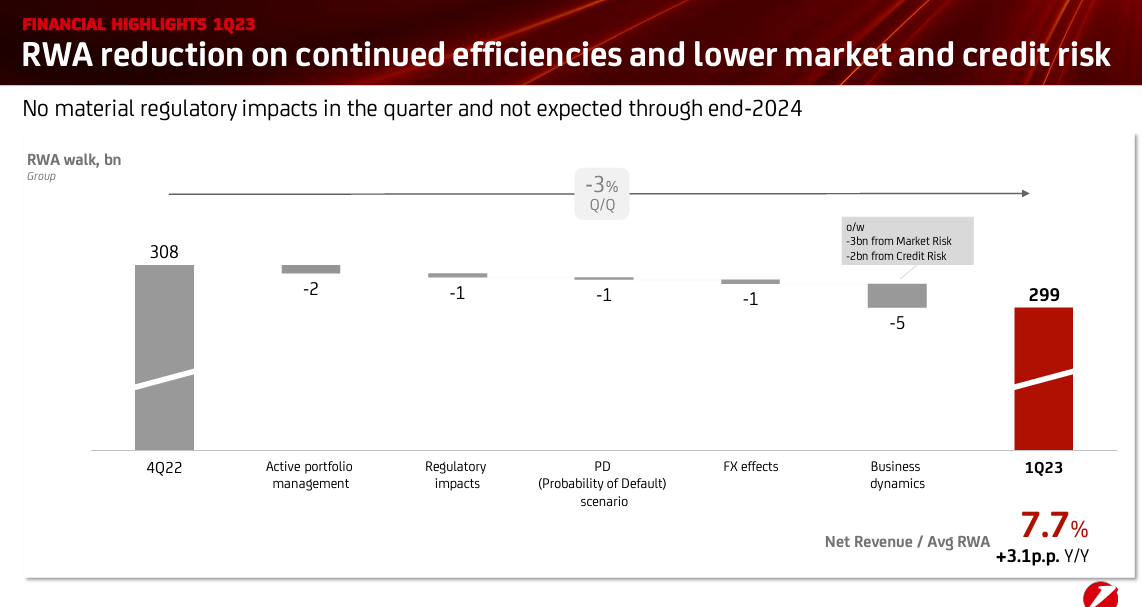

In detail, taking account of the company's share repurchase (€3.3 billion) in 2022 results, UniCredit's CET1 ratio closed at a record rate. Once again, the company was able to organically generate capital with income and RWA that adds 67 and 44 basis points respectively. RWA's active optimization continues to reward the company (Fig 2). We should also note the cash dividend accrual which detracted 23 basis points at CET 1 level. The CEO noted that there are no expectations for new regulatory impacts for the next two years. By 2023, we anticipated that RWA will further decline below €300 billion and will contribute 250 basis points of capital generation.

{kind=link}

Fig 1

{kind=link}

Fig 2

Despite the recent banking turmoil, the company deposits remained stable at almost €500 billion with a liquidity coverage ratio at a high of 163%. In addition, loan to deposit ratio is at 90%, and in line with the EU environment, almost 80% of deposits belong to SMEs and B2C clients with no particular risks of outflows.

Conclusion and Valuation

UniCredit posted more than €2 billion in net income with a 58% beat on Wall Street average consensus. Once again, the Italian bank over-delivered and unlocked its value . This is very much in line with our initial buy rating target called: ' UniCredit Could Return Its Entire Capitalisation In 4 Years' released in early June 2022. Core top-line sales are solid with an impressive cost-efficiency (cost income fell to 39%). The bank cost of risk was just at 8 basis points, CET 1 ratio was even stronger than anticipated and was the result of better capital generation.

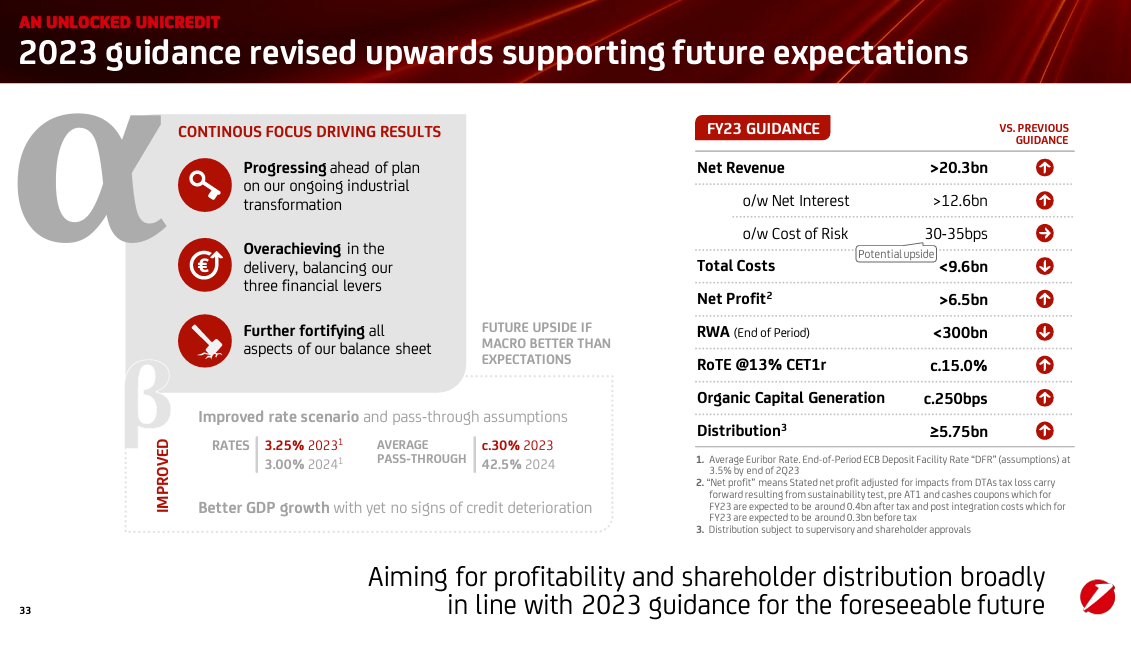

For the above reason, the group raised its 2023 guidance. In detail, revenues are set at €20.3 billion (versus the previous at €>18.5 billion), supported, as already mentioned, by higher NII generation (expected above €12.6bn versus the previous at >€11.3 billion). Costs are forecasted lower than initially anticipated and are now set below €9.6 billion (versus the previous at <€9.7 billion). Therefore, net profits are set above €6.5 billion (versus the previous at > €5.6 billion). This sets a new reference base for 2023 and beyond.

In line with CEO's latest guidance on the bank profitability target, RoTE is expected well above capital cost (15% vs 13% on target estimates).

UniCredit is one of the best banking stocks in Europe year-to-date, and we expect this outperformance to continue due to continued improvement in consensus estimates, rising return on capital, and a still subdued valuation. Capital distribution is now expected at or above €5.75 billion, last time we already increased our internal numbers, and so today, we confirm our buy rating target at €22 per share.

{kind=link}

For further details see:

UniCredit: Beat Across The Board