UNCRY - UniCredit: Cheap Valuation And Hefty Capital Returns

2023-07-19 13:24:59 ET

Summary

- We believe this is an opportunity to accumulate shares in a geographically diversified commercial bank trading at compelling multiples.

- The stock trades at a discount to peers in terms of both P/E and P/TBV despite returns on tangible book value being in line and shareholder remuneration being higher.

- 27% of the market cap will be distributed to shareholders over FY23-24.

We present our Long thesis on UniCredit ( UNCRY ) while exploring the company’s improving fundamentals, robust trends, and announced targets. We believe this is an opportunity to accumulate shares in a geographically diversified commercial bank trading at compelling multiples.

Company Overview and History

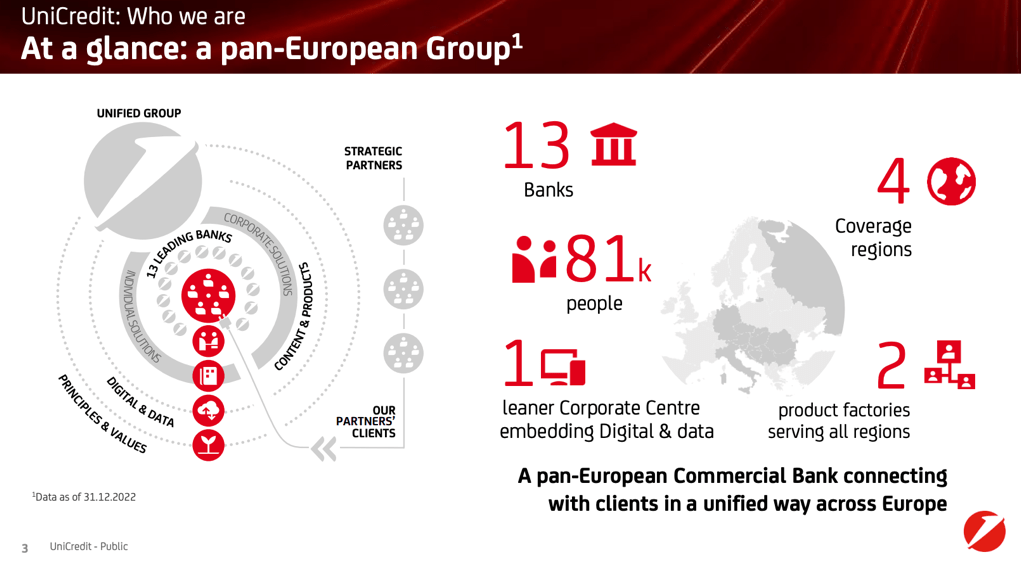

UniCredit is a pan-European commercial bank with an offering in Italy, Germany, and Central and Eastern Europe, serving over 15 million customers worldwide. UniCredit Group contains 13 banks. 46% of revenue is generated in Italy, 26% in Germany, 18% in Central Europe, and 10% in Eastern Europe. UniCredit ranks #2 in Italy in terms of total assets, after Intesa Sanpaolo (ISNPY). UniCredit holds leading positions in Bulgaria, Bosnia, and Croatia, and is among the top 5 in Czechia, Slovenia, Slovakia, and Serbia. Over the last decade, profound changes were made including the disposal of the stake in the Polish Bank Pekao, the disposal of the stake in Pioneer Asset Management, the disposal of the stake in Mediobanca, the disposal of the stake in Fineco, the disposal of the stake in Turkish bank Yapi Kredi, the disposal of €17.7 billion of NPLs at the end of 2016, and a large capital increase in the following quarter. In April 2021, renowned investment banker Andrea Orcel was appointed CEO. In July 2022 he was also appointed Head of Italy. In December 2021 the new business plan was introduced. We will explore it in the UniCredit Unlocked section.

UniCredit Investor Presentation

{kind=link}

Recent Performance

UniCredit has delivered a strong start to the year with solid Q1 numbers. Net Interest Income came in at €3.3 billion and benefited from a wider spread as a result of rising interest rates with little trickle-through to deposits. In addition, fee income was also satisfactory and came in at €2.0 billion with 10% like-for-like growth. Total revenue was €5.8 billion increasing 58% YoY. Asset quality trends were also impressive with no deterioration, an 8 basis points Cost of Risk provision, and a stable NPE ratio. Capital ratio development was also positive as CET1 rose to above 16%. The set of results in Q1 triggered a guidance revision for FY 2023. NII guidance was raised from >€11.3 billion to >€12.6 billion and net revenue guidance stands at >€20.3 billion vs a previous target of >€18.5 billion. Shareholder distribution targets were increased by €500 million to >€5.75 billion, or around 13% of the current market capitalization. The company aims to have profitability and shareholder returns around the same levels as 2023 in the following years despite a likely fall in interest rates. This could be achieved through higher fee income, lower deposit betas, and lower operational costs.

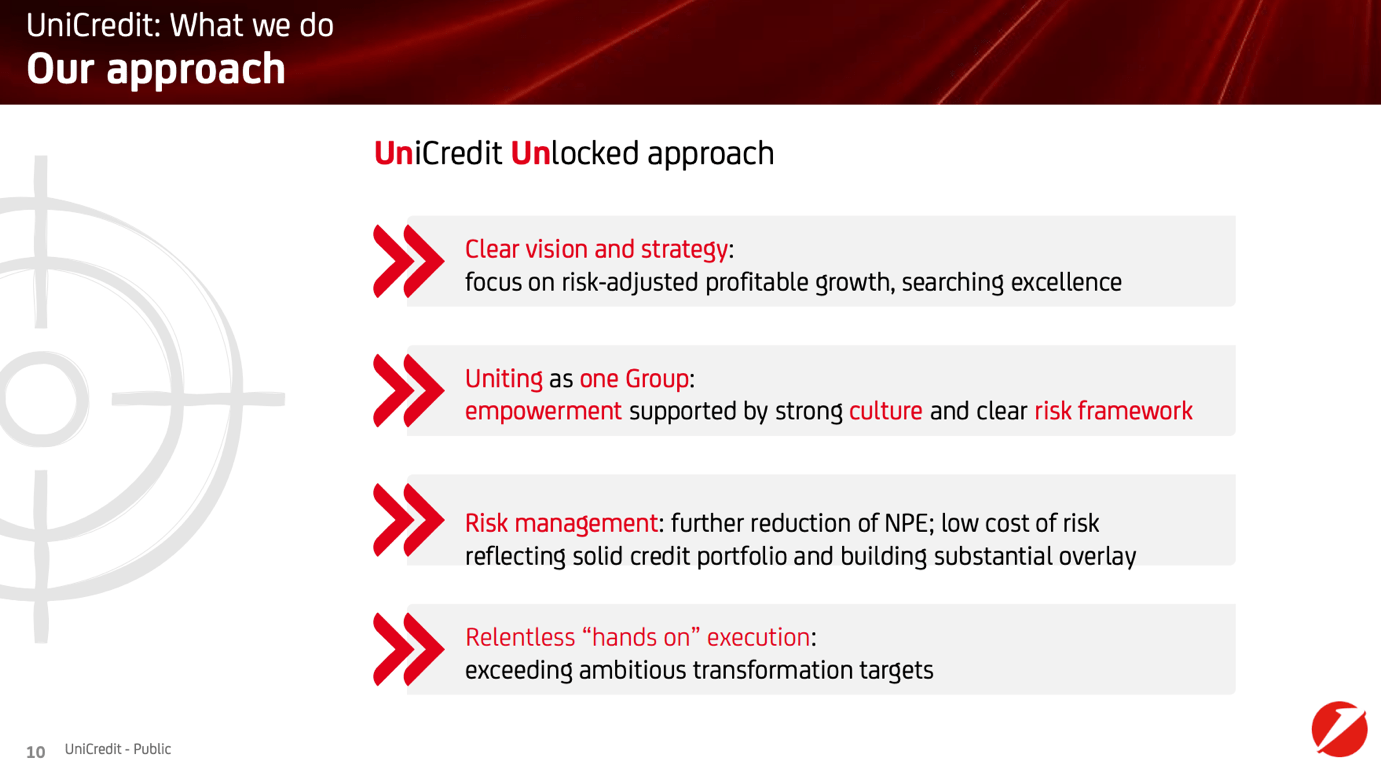

UniCredit Unlocked

UniCredit Unlocked aims to achieve quality growth, grow the capital-light business, focus on value-added offerings for clients, and unite all 13 banks in an integrated group. The plan will conclude the restructuring phase of the bank. The plan aims for 2024 Net Revenue to be higher than €17 billion, 2024 NII higher than €4 billion (a target that has already been surpassed), and cumulative shareholder returns of over €16 billion between the years 2021 and 2024 included.

UniCredit Investor Presentation

{kind=link}

Valuation and Investment Thesis

Our thesis on UniCredit revolves around rising profits, a strong capital position, high CoR visibility, considerable shareholder returns, exposure to growing economies in CEE, and an appealing valuation. The stock trades at a discount to peers in terms of both P/E and P/TBV despite returns on tangible book value being in line and shareholder remuneration being higher.

UniCredit is outperforming expectations consecutively every quarter, supported by rising rates, and finally enjoying the benefits of restructuring plans, cost optimization, and prudent risk management. The tailwinds from product factories are yet to materialize. We see additional scope for guidance revisions this year. We expect total revenue of €22.0 billion and net profit of €7.0 billion in 2024.

On the Cost of Risk side, we would like to point out the €1.8 billion of overlays that can be used in case a scenario of macroeconomic deterioration materializes or can be used to enhance earnings in case of more a benign macro environment.

We are impressed with the 110 basis points of capital generation in Q1 2023, and we believe this puts UniCredit on the path for at least 200+ basis points of capital generation in total surpassing the initial target by at least 50 bps. We believe this will be an important factor in determining shareholder returns over the following years.

Shareholder remunerations are an important catalyst for UniCredit. €5.75 billion will be distributed in 2023, with €1 billion of share buybacks remaining to be executed by year-end; and at least an additional €5.75 billion (at least) will be distributed in 2024. That is equivalent to 27% of the market cap in shareholder distributions over FY23-24. This is the highest in Europe, so far.

We value UniCredit using a blended P/TBV and P/E multiples analysis. We value UniCredit at 8x earnings 2024e, arriving at a valuation of €56 billion for the group, or a share price of €29 or $32.5, implying a 31% upside. We would like to note that the average PE since 2007 has been around 9x.

We forecast a tangible book value of €34.7 and 11.8% ROTBV in FY24. The current valuation implies 0.64x P/TBV’24e, which is excessively low given the ROTBV. This P/TBV multiple implies a 18.5% cost of equity. As UniCredit prints good quarters and reiterates/upgrades its guidance we believe it should rerate to 0.8x+ P/TBV’24e, implying at least a 25% upside, or a share price of €27.60 or $31. Our blended target price is €28.30 or $31.80.

Risks

Risks include but are not limited to deteriorating macroeconomic conditions, no rate hikes or slower rate hikes, increase in cost of funding, additional pressure from Russian operations / a full write-down, adverse changes in regulation e.g., higher than expected capital requirements, decline in asset quality and a worsening of the capital position, higher competition from traditional players and neobanks / fintech, and inability to go forward with shareholder remuneration plans.

Conclusion

Based on the strong underlying fundamentals, compelling valuation, and shareholder distribution catalyst, we recommend building a long position in UniCredit shares.

For further details see:

UniCredit: Cheap Valuation And Hefty Capital Returns