UNCRY - UniCredit Is Likely To Deliver Long-Term Return

2023-09-13 05:42:47 ET

Summary

- Despite inflation expectations, UniCredit plans to cut costs by about €500 million.

- UniCredit is now a transformed bank with an earnings growth trajectory and sustainable competitive advantages, given its cost structure.

- Best in class cost/income ratio with solid CET 1. Impressive results with an ongoing buyback and upside in shareholders' remuneration.

- The CEO's comment on the 2024 forecast results is another positive sign of our buy target.

Here at the Lab, ahead of Q2 results, it was an excellent call to confirm and increase our target price. Looking back, when we upgraded UniCredit with a buy (UNCFF) (UNCRY) thanks to a publication called the bank " Could Return Its Entire Capitalisation In 4 Years ," we were not expecting to achieve this performance in four quarters. In numbers, the Italian bank's stock price increased by 91.97% and, including its tasty dividend per share, returned its entire market cap.

{kind=link}

Starting with the negative news, the Italian legislature introduced an extraordinary tax to hit the banking extra profits. This is a differentiated tax treatment extended to all operators operating in the sector; nevertheless, this methodology carries out legally arbitrary discrimination. We are not legal experts, but the Italian legislator appears uncertain in outlining the object the government intends to target. As reported in our Crédit Agricole update , " if a government intends to tax the banks when rates go up, the question arises whether they will be willing to support them when rates start going down again, and we very much doubt that."

Still related to Italy, this extra profit could not translated into income. Why? Despite the ECB's intention to increase rates over the short-term horizon, expecting a rate normalization, banks might offset profit with higher provisions and funding costs. While the government is already willing to review this proposal, and we also believe it is incompatible with the Italian constitutional principles, the downside scenario is regulatory credibility. UniCredit is less exposed to the Italian GEO sales footprint than Intesa San Paolo. In numbers, with the proposal to tax the " 0.1% of the net assets ," according to our estimates, UniCredit could pay a maximum of €500 million in the worst-case scenario.

Why are we still positive?

- Having participated in the Azimut Q&A call (AZIHF) (AZIHY), we positively reported that the CEO announced that the companies entered the second phase of their strategic partnership. As a reminder, in 2022 end, they signed a collaboration to start marketing Azimut funds in Q1 2024 . This also involves the creation of new funds in Ireland that will place non-exclusively products to B2B and B2C Italian clients. Here at the Lab, we also commented on the Amundi downside risks of the new Italian partnership;

- We positively view UniCredit CEO's words not to pursue acquisitions and to prefer moving on with the current share repurchase. M&A should consider an earning accelerator; however, at the moment, there are neither the right conditions nor the correct terms;

- Reporting our latest comment on SocGen , the European Central Bank is concerned about UniCredit's presence in Russia but has not considered taking action. UniCredit avoided exiting the country, where it operates one of the largest foreign banks. Presidential approval is required to leave the market due to restrictions on asset sales. Reporting UniCredit CEO words, he continued with its emphasis on " No Gift For Russia ," and again in Q2, he said that UniCredit's " strategy does not change on Russia, and we continue to reduce exposure to the country, and we will continue with determination in this direction ," assuring that the reduction is " organic and orderly ." Currently, an asset sale is not an option, given the underlying value. In the worst scenario, with a bank nationalization of the UniCredit subsidiary, the impact on the CET1 ratio is limited to 40 basis points;

- Looking back to the H1 results, this was the best first half ever for the bank and signed the 10th consecutive quarter of growth in profitability. In numbers, the financial institute closed with a net accounting profit of €4.4 billion with a plus +91.5% vs. last year and a remarkable RoTE of 20.8%. In Q2 alone, profits amounted to €2.3 billion, with net income exceeding consensus expectations;

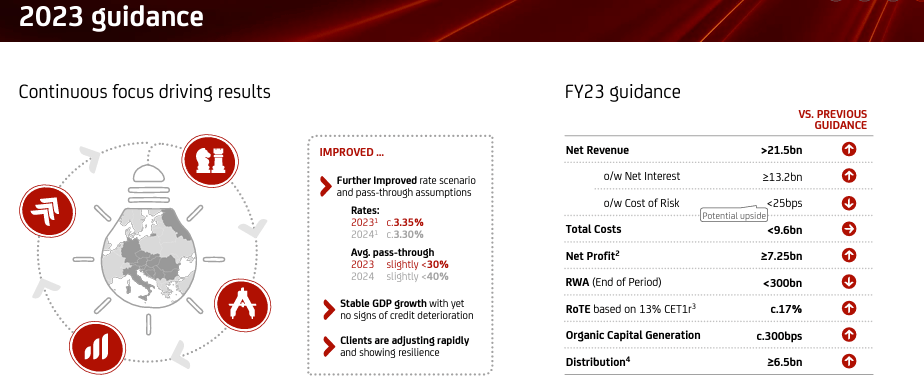

- Despite inflation, the bank surprised by the operating costs evolution. These were down 1.2% year-on-year to €2.3 billion with a low cost/income ratio of 39%. UniCredit intends to carry out a further cost cut of around €500 million, acting mainly on simplifying & automating business processes and improving outsourcing contracts conditions with an investment in digital resources;

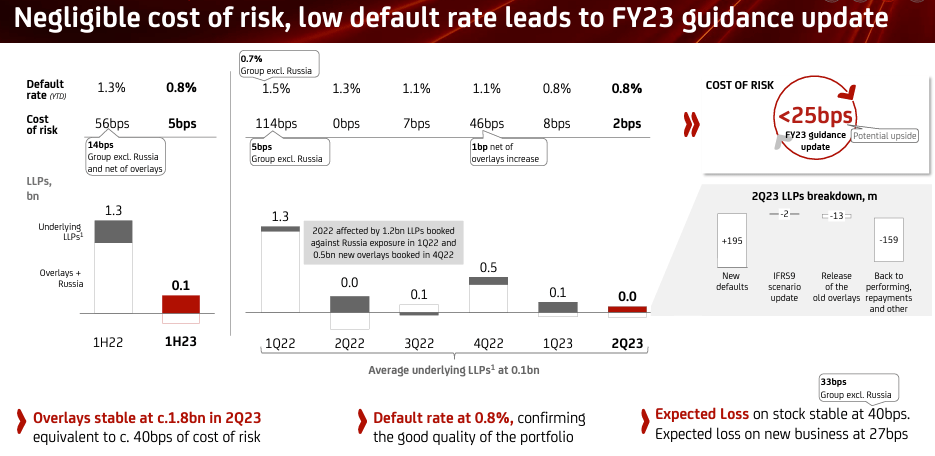

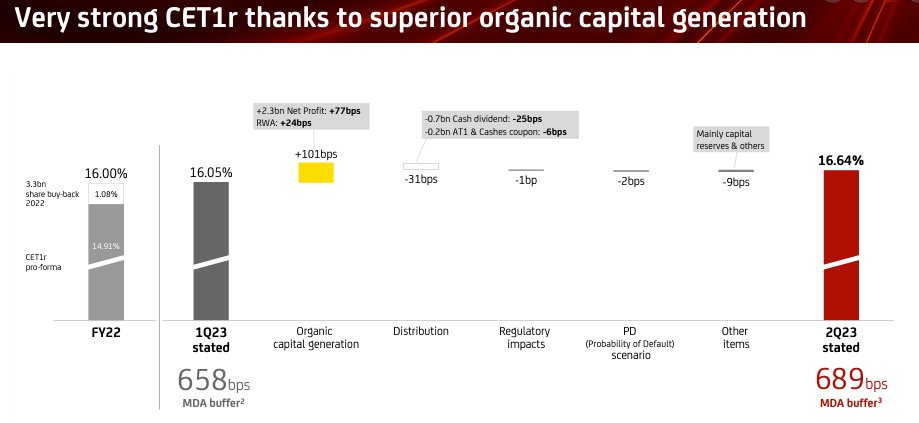

- In Q2, the company recorded a low cost of risk of 2 basis points. A robust assets portfolio supported this. The CET 1 capital ratio was one of the best in the sector at 16.64%, up by 58 points quarter on quarter and by 91 points every year. This was supported by € 6.5 billion in organic capital generation, considering €1.5 billion in dividends accrued. Still related to the cost of risk, UniCredit forecasts a ratio of less than 25 basis points for 2023, and we align with the company's internal estimates;

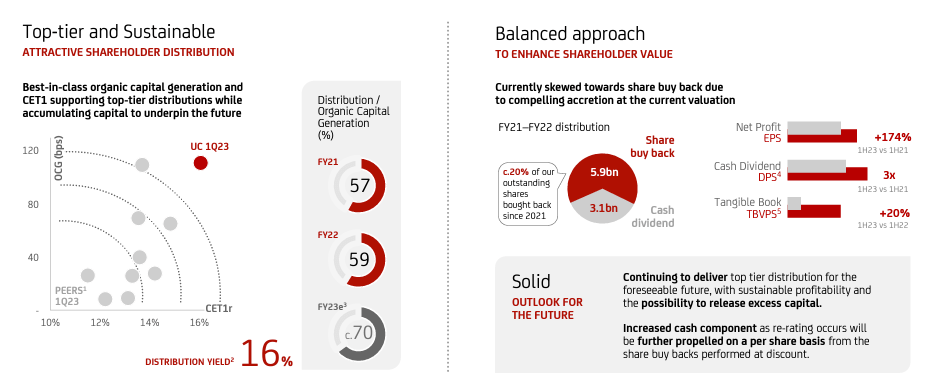

- UniCredit also reported the excellent progress of the 2022 share buyback program for €3.34 billion, equal to 6.5% of the capital;

- Looking to the future, according to the CEO, 2023 results serve as a reference basis for what UniCredit is confident to achieve next year.

UniCredit cost of risk development

{kind=link}

Fig 1

UniCredit CET1 ratio evolution

{kind=link}

Fig 2

UniCredit Dividend and Buyback

{kind=link}

Fig 3

{kind=link}

Fig 4

Conclusion and Valuation

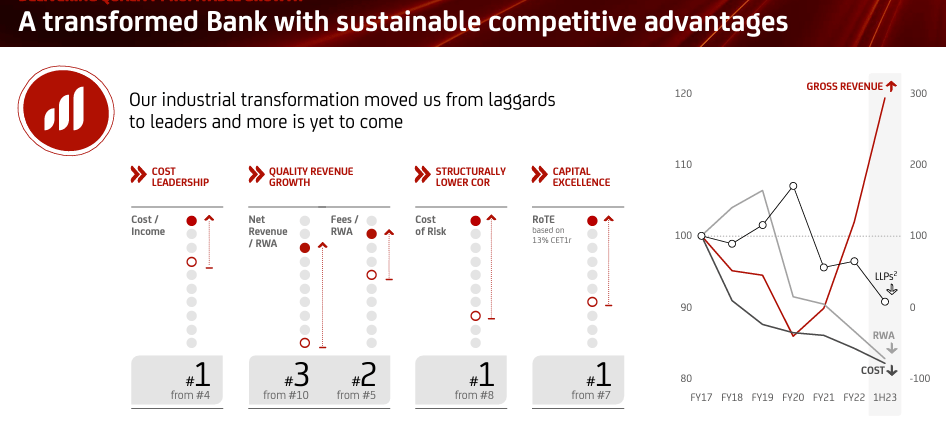

Here at the Lab, we positively view UniCredit's latest development, and even if there are downside risks in Russia and the extra profit tax, we still believe the company has a valuation upside. Q2 EPS reached €1.12, and the book's tangible value is now at €30.2 per share. Valuing the company with a TBV of 0.8x, we derived a target price of €24 per share, confirming our upside . What is more important to emphasize is that UniCredit can generate significant returns throughout the economic cycle. The company has transformed with clear competitive advantages in costs and lower risks. The slide below shows the considerable progress that UniCredit has achieved in the last year. Our buy rating is then fully confirmed.

{kind=link}

For further details see:

UniCredit Is Likely To Deliver Long-Term Return