UNCRY - UniCredit: One Of The Best European Bank Stocks Heavily Discounted

2023-09-18 09:25:34 ET

Summary

- The political nonsense to levy a windfall tax on banks' profits still creeps around. However, Italian banking stocks have been resilient to such noise and represent an excellent investment opportunity.

- UniCredit is among the best European banks. Last quarter's results prove that statement: growing CET1, a declining cost-to-income ratio, and improving RoTE.

- UniCredit stock is deeply undervalued based on Excess Return Valuation and the company's book value.

- I give UniCredit a strong buy rating due to the improving balance sheet quality, growing profitability, and regular dividends.

Thesis

UniCredit (UNCRY) is among the best European banks. Last quarter's results prove that statement: growing CET1, a declining cost-to-income ratio, and improving RoTE. On top of that, the bank pays adequate dividends. Compared to Excess Return valuation and the bank`s book value, the current market price offers a significant margin of safety. The persistent political risk in the face of windfall taxes is still too tangible. That said, despite the political risk, I give a strong buy rating due to the bank's qualities and excellent price.

Company Overview

UniCredit S.p.A., a commercial bank, provides retail and business banking services. It additionally provides services for retail, business, and corporate customers. The bank also offers solutions for capital markets, specialty loans, risk management, transactions and payments, and advisory services. It also provides services connected to assets, funds, life insurance, brokerage, and portfolio management.

UniCredit has evolved into one of the best-performing banks in Europe under Andrea Orcel's direction. The last report confirms that a 39% cost-to-income ratio, 16.6% CET1r, and 90 % loan-to-deposit ratios are all present. These are unquestionably impressive numbers.

Below is a comparison against other large European banks to illustrate my point:

- Dutch ING Groep ( ING ): Cost/Income of 54%, CET1 14.9%, and RoTE 17.3%.

- French BNP Paribas ( OTCQX:BNPQF ): Cost/Income ratio of 64%, CET1 13.6%, and RoTE was around 10%.

- Intesa Sanpaolo ( OTCPK:ISNPY ): Cost/Income ratio of 42%, CET1 13.7%, and RoTE was around 11.2%.

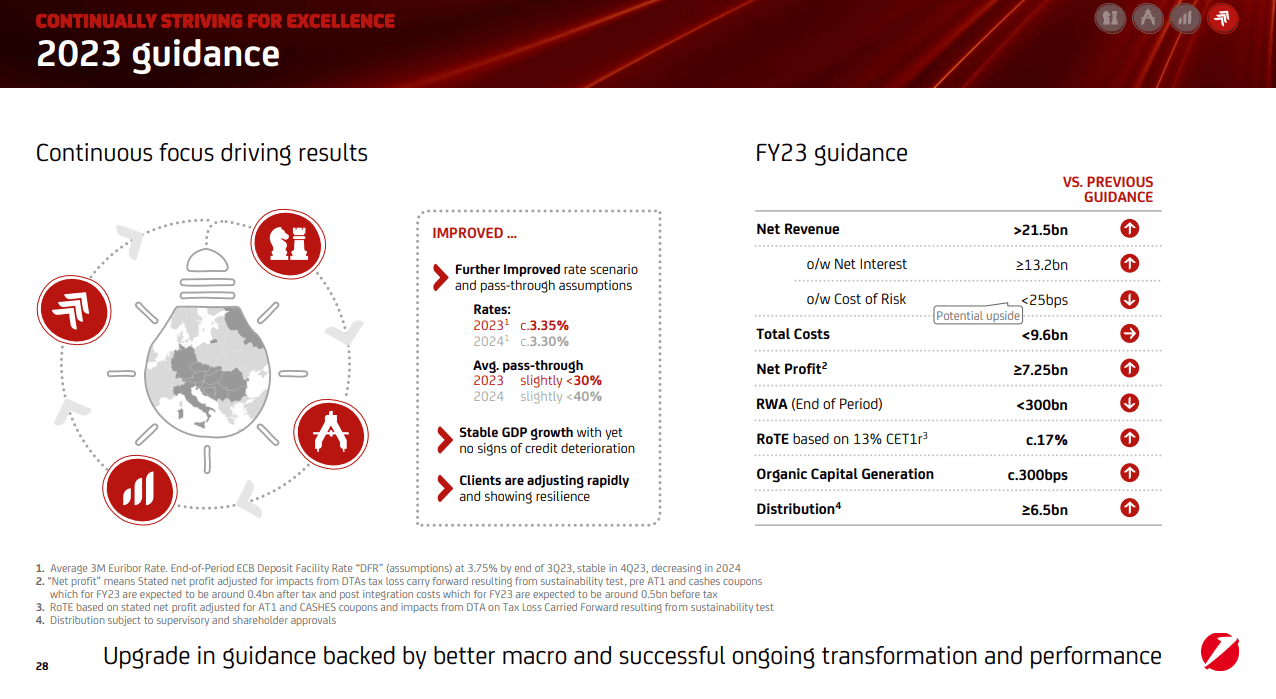

Below are UniCredit guidelines from the last company presentation . The bank exceeded its guidelines.

{kind=link}

Singular growth in revenues and income while improving balance sheet composition is an outstanding achievement. In the chapter below, I will dig deeper into the bank's finances and argue why UniCredit is an excellent bank.

Company Financials

Italian banks are notorious for poor-quality balance sheets. However, that is not valid anymore, and UniCredit has proven it. The table below shows some metrics I use to estimate banks' health. The data is from the last bank`s financial report .

| Asset ratios: assets structure |

| Cash/Total Assets |

| 9.0 % |

| Loans to banks/Total Assets |

| 7.9 % |

| Loans to customers/Total Assets |

| 53 % |

| Bonds/Total Assets |

| 17.7 % |

| Liability ratios: capital structure |

| Deposits/ Total Liabilities |

| 78 % |

| Other liabilities/ Total Liabilities |

| 35 % |

| Company bonds/ Total Liabilities |

| 11.2 % |

| Equity/ Total Liabilities + Equity |

| 7.3 % |

| Solvency ratios: |

| Bank loans /Deposits |

| 10 % |

| Customer loans /Deposits |

| 73 % |

| Cash/Deposits |

| 12.4 % |

| Borrowings (inc. bonds)/ Total Assets |

| 10.9 % |

There are a couple of things I want to point out. First is the adequate level of cash to deposits. This is every bank's first line of defense in case of a bank run. UniCredit has 1.2 euros in cash reserves for every ten deposited euros. The company-issued bonds consist of 10.9 % of total assets. Hence, the bank funding is not too dependent on bondholders.

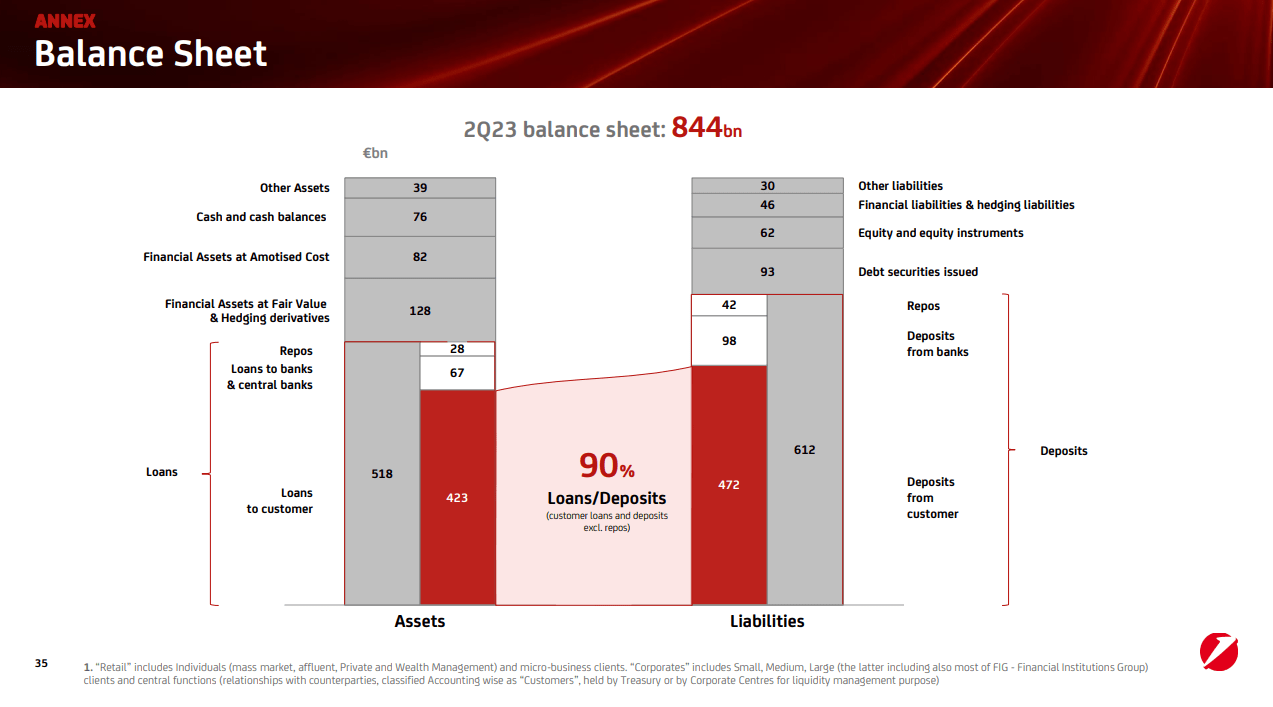

Let's go into detail and analyze loans and deposit composition. The image below represents the bank`s balance sheet at a glance.

{kind=link}

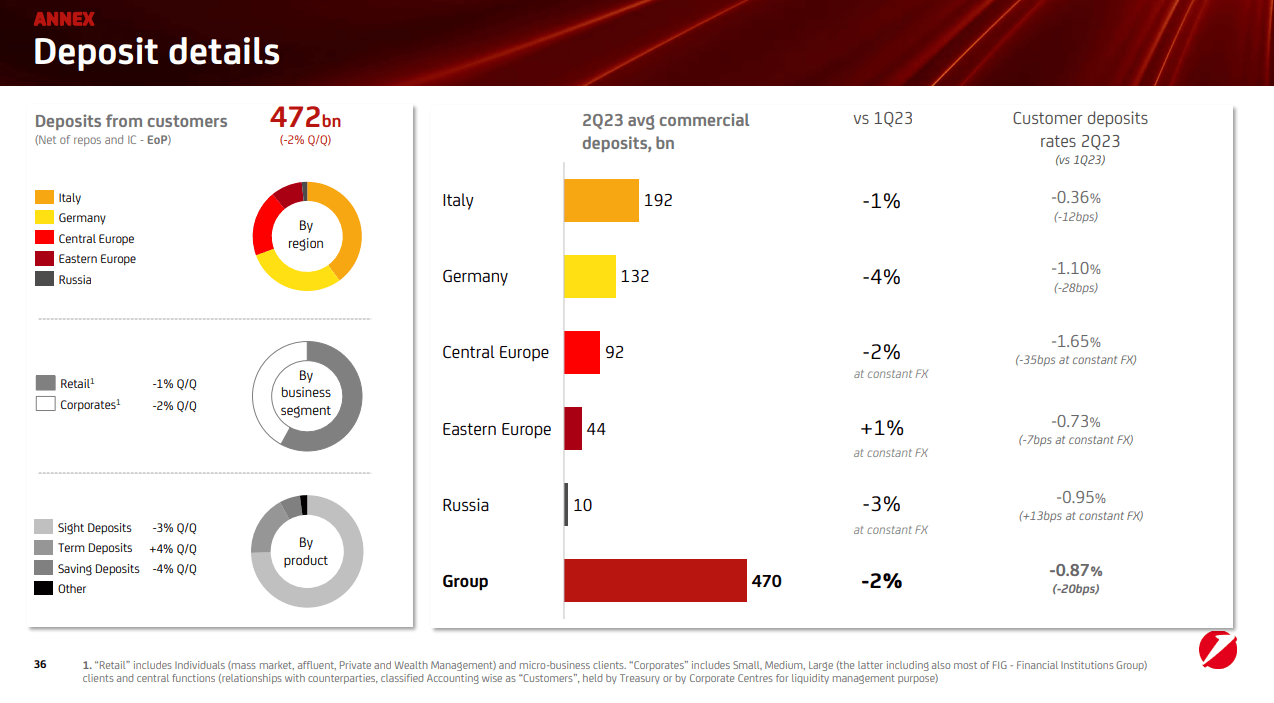

Loans to deposits ratio is 90 %. That means the bank is not overloaded with loans, thus risking its liquidity standing. Loans and deposits are proportionally distributed between banks and retail customers. The image below shows the deposit's composition.

{kind=link}

Geographically, they are well diversified across EU states, with Germany and Italy contributing more than two-thirds of the deposits. Most of the deposits are sight, i.e., checking accounts. That is not the best structure due to the lack of a lock period for those funds. Hence, a critical mass of depositors might withdraw funds without notice and cause a liquidity crunch. Preferably, time deposits, savings accounts, and checking accounts must be balanced; thus, maturity transformation will remain unaffected, and the bank`s liquidity risk will notably improve.

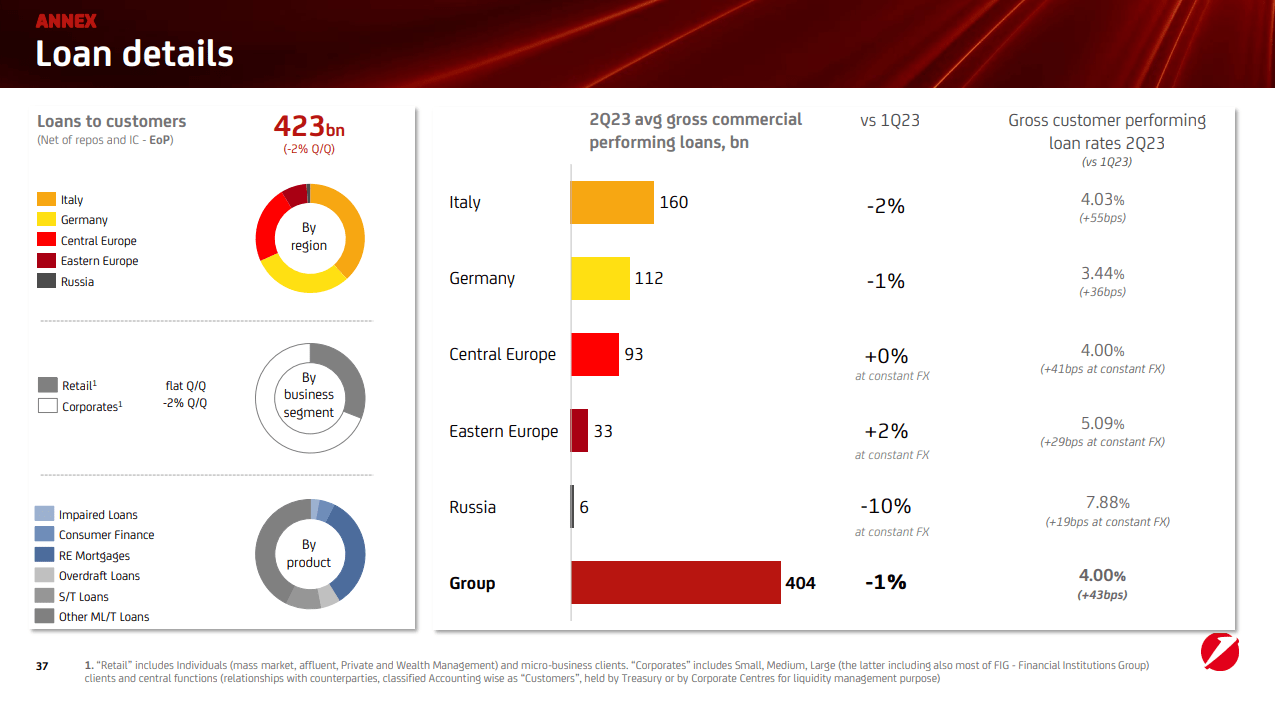

The right side of the balance sheet is illustrated below. The loans are distributed similarly by country; Italy and Germany lead the pack.

{kind=link}

Compared to deposits, the composition loans portfolio is well diversified. Mortgages represent one-third, and the remaining is scattered among consumer finance, overdrafts, corporate midterm, and short-term loans. Non-performing loans (NPL) have declined for the last quarters and reached 1.4 %. This is considerably lower than the Italian average of 3.1 %.

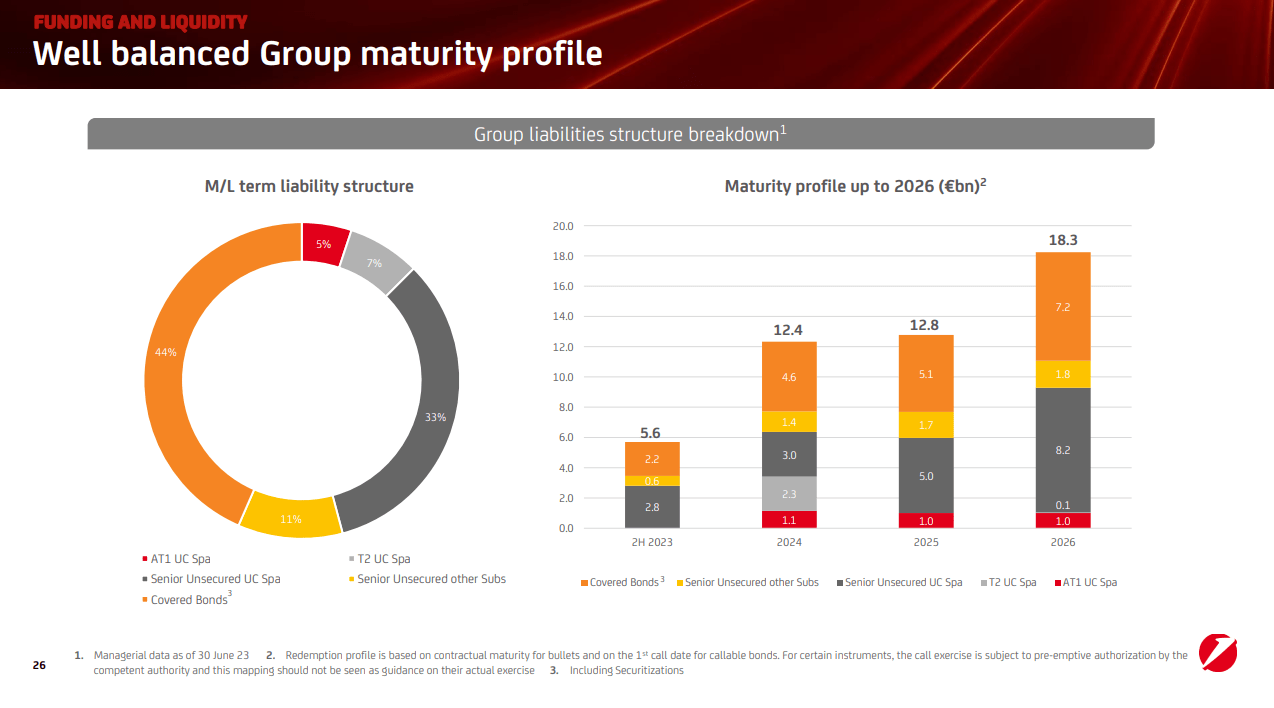

UniCredit-issued bonds have BBB ratings by S&P and Fitch for their long-term and short-term issues. Bond maturity is safely distributed in the next few years. The image below illustrates the UniCredit debt structure. The data is from fixed-income investors' presentations.

{kind=link}

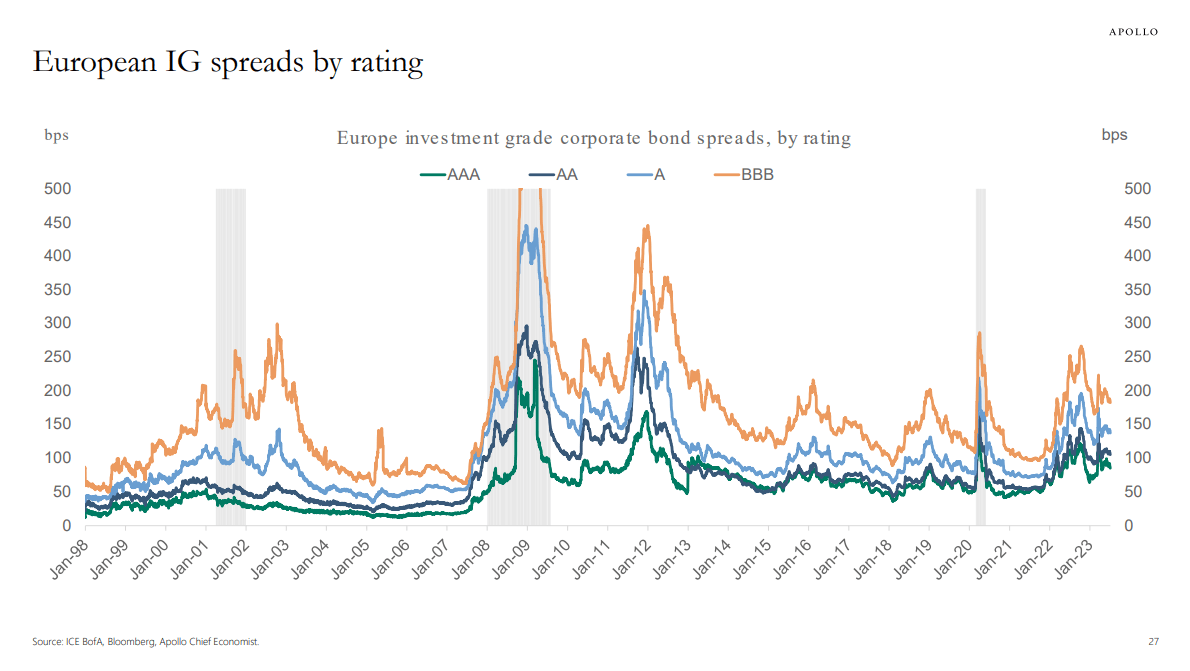

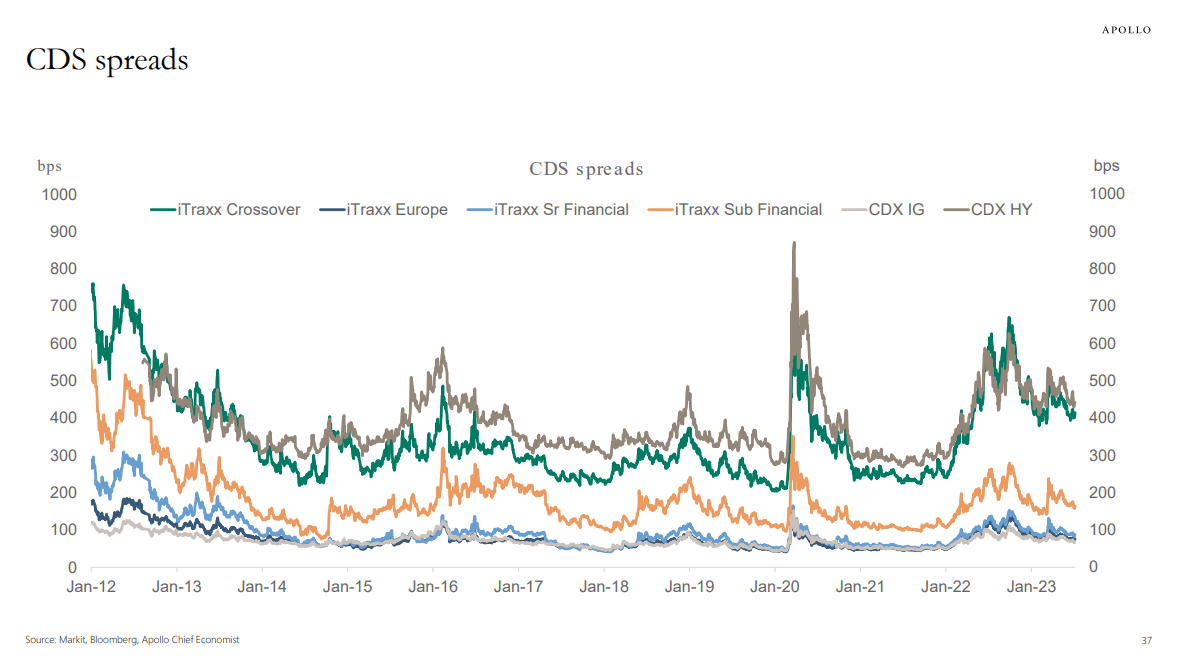

The bank has to repay its 50 billion euro of debt in three years. Given its strong performance and available liquidity, I am confident the debts will be covered. Talking about fixed income, it is worth mentioning the big picture. In two charts from Apollo Global, I will show where are European IG bonds.

The first shows IG spreads by rating. As seen below, the spreads are declining and far from their peak even in March 2023, during SVB turmoil and the European debt crisis 2013.

{kind=link}

The second chart is more interesting. It shows credit default swaps (CDS) spreads. CDX IG is dropping along with IG spreads.

{kind=link}

That said, the lending conditions in Europe have improved. Henceforth, all European banks carry less liquidity risk by issuing new bonds, at least in the short term.

Last but not least is to estimate UniCredit's performance against Basel III metrics. The table below shows the bank`s solvency and liquidity ratios. The data is from the previous financial report, Q2 2023 .

| Capital (in billions of euros): |

| Regulatory Capital |

| 63.5 |

| Tier 1 capital |

| 54.7 |

| Common equity tier 1 (CET1) |

| 48.9 |

| Risk-Weighted Assets |

| 295.7 |

| Basel III Ratios: |

| Regulatory capital ratio (Capital adequacy ratio) |

| 21.5 % |

| Tier 1 ratio |

| 18.5 % |

| CET1 ratio |

| 16.6 % |

| LCR |

| 140 % |

| NSFR |

| 130 % |

UniCredit excels on all parameters due to improved balance sheet composition. The primary driver behind that is the improving assets' quality, thus significantly reducing RWA.

Rising interest rates made all banks more profitable due to increased net interest margins. UniCredit is not an exception. Last quarter, the bank reported solid results reflected in its bottom line. The table below shows profitability metrics I use to asses bank's efficiency.

| ROE |

| 15.1 % |

| RoTE |

| 17.0 % |

| RoCET 1 |

| 19.5 % |

| ROA |

| 1.0 % |

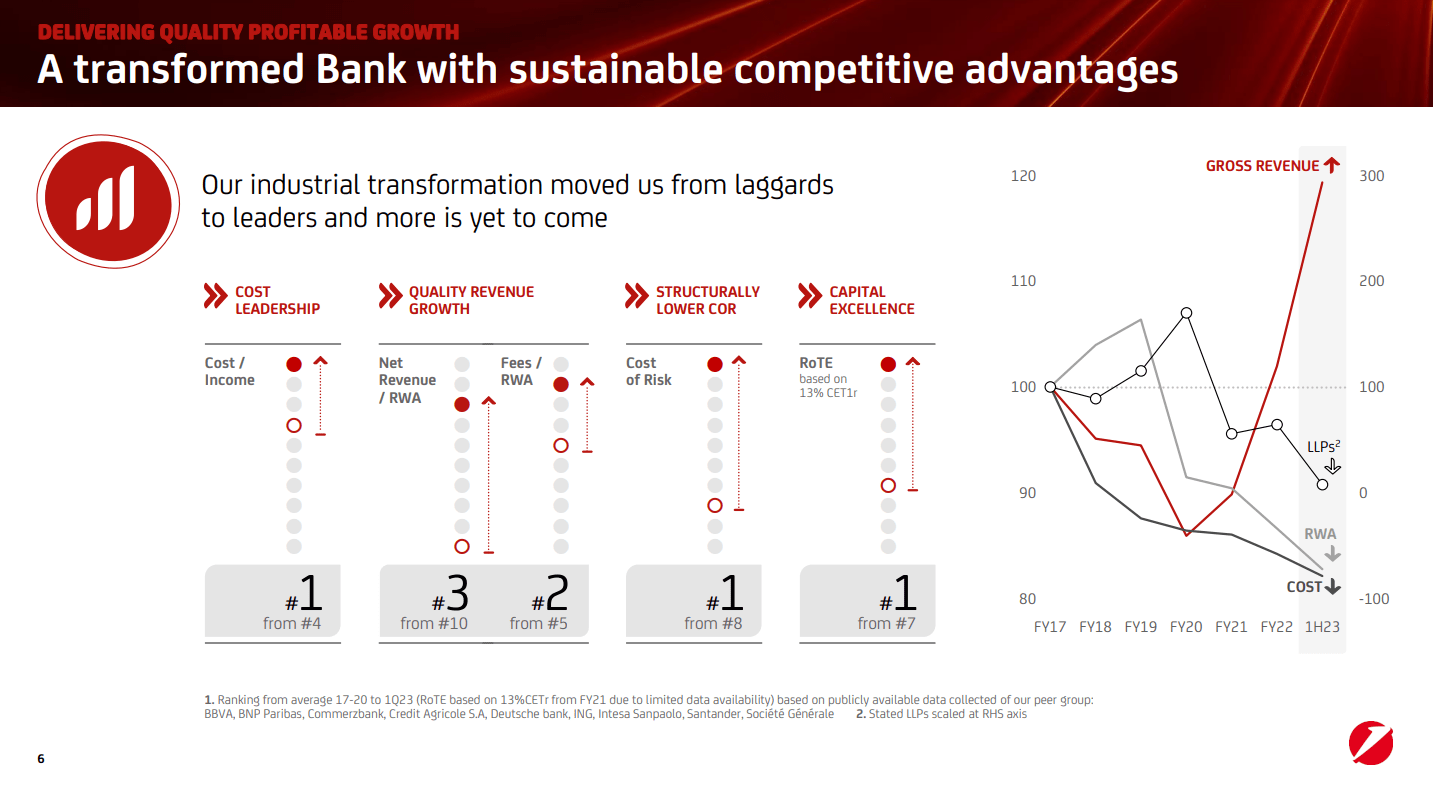

The bank improved its costs, profitability, and capital structure, as seen in the image below.

{kind=link}

I would like to point out the cost-to-income ratio and cost of risk. The former is the most basic metric in banking; however, it predetermines banks' long-term efficiency. In the Q2 report, UniCredit cost to income is 39 %. In other words, to earn 1 euro, the bank must invest 0.39 euro. Cost of risk is another foundational metric in banking. It measures the ratio of provisions (annualized) to the average volume of banks` loan portfolios. The cost of risk has dropped from 110 bps to just 2 for the last 18 months.

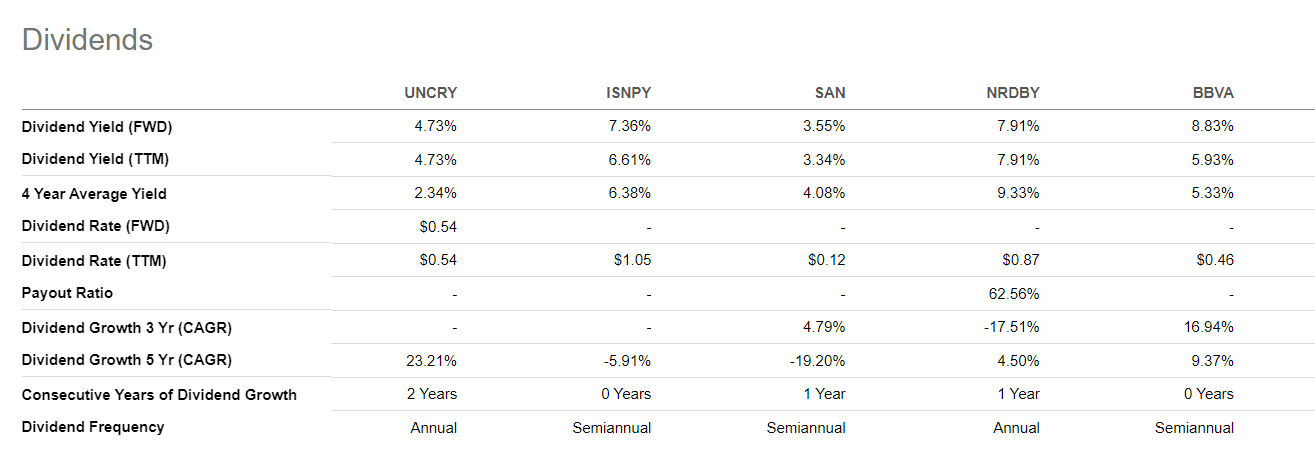

UniCredit pays adequate dividends, however, lower than Intesa Sanpaolo ( OTCPK:ISNPY ), Nordea Bank ( OTCPK:NRDBY ), and Banco Bilbao Vizcaya Argentaria ( BBVA )

{kind=link}

With improving profitability, I expect UniCredit to increase its dividends, thus becoming more luring for income-minded investors.

Company Valuation

For the valuation of UniCredit, I use the Excess Return Model. I do follow Professor Damodaran's framework and its database.

Assumptions and inputs:

- Risk-free rate equals the 5Y average of USA long-term Government bond Rate, 2.2%.

- Growth rate, g, equals the 5Y average of the USA long-term Government bond Rate, 2.2%.

- Italy's equity risk premium is 8.33 %.

- UNCRY's book value per share is $ 37.18 (Sept 17, 2023).

- UNCRY' unlevered Beta 1.12

- UNCRY Debt/Equity ratio 201 %.

- Italy's effective tax rate is 24 %.

- UNCRY ROE ((TTM)) 13.62 %

1. Calculate Levered Beta with the formula below:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E).

2. Calculate the discount rate (discount rate as the cost of equity) using the resulting value for leveraged beta. The formula I use is:

Cost of Equity = Risk-Free Rate + (Levered Beta * Equity Risk Premium).

3. Calculate Excess Returns using GGAL's ROE, Book Value, and Cost of Equity:

Excess equity return = (Stable Return on equity - Cost of equity) x (Book Value of Equity per share).

4. Calculate Excess Returns Terminal Value assuming perpetual constant growth and stable cost of equity:

Excess Returns Terminal Value = = Excess Returns / (Cost of Equity - Expected Growth Rate).

6. Calculate the Value of Equity.

Value of Equity = Book Value per share + Terminal Value of Excess Returns.

For UNCRY, I get the following results:

Terminal Value of Excess Returns Per Share = $ 8.33

Intrinsic value per share = $ 45.51

Current market price = $ 11.49 (Sept 17, 2023)

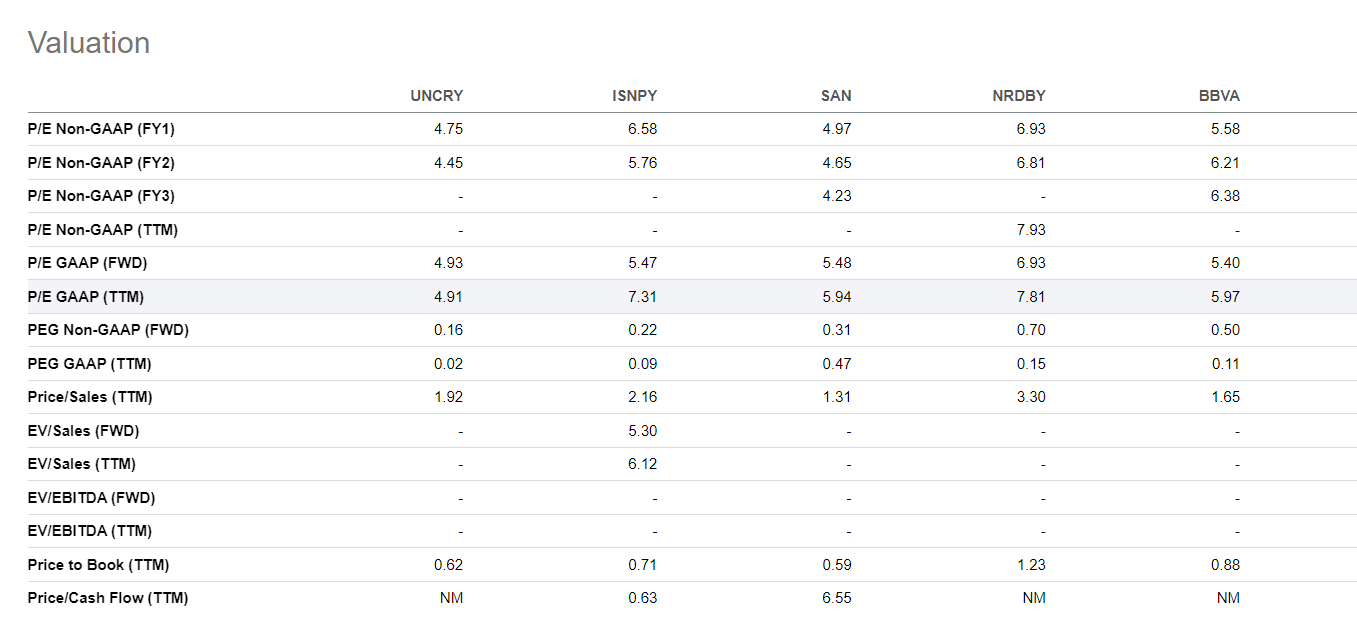

I compare UNCRY with other large EU banks.

{kind=link}

Using price to book Unicredit is deeply undervalued. The same is true for price to sales. The relative valuation confirms my conclusion based on the Excess Return Model. Unicredit is for sale at a significant discount.

Risks

All banks share the same risks (credit, liquidity, market, and operational); however, one more risk arises during good times—hungry government officials implementing windfall taxes, i.e., short-term PR moves with long-term high costs. As discussed in my report for ISNPY , the risk for windfall taxes is still very tangible. Italian PM Meloni opposes ECB guidelines to avoid such measures, and the windfall tax scenario is not out of the equation.

Despite that, UniCredit manages the remaining risks well. Its loan portfolio is effectively distributed, thus mitigating the credit risk from the bank`s borrowers’ issues. The same is valid for deposit structure and cash reserves. As I pointed out earlier, the deposit composition could be better with equal distribution between deposit terms. Based on Basel III ratios, LCR and NSFR UniCredit perform more than adequately. The same can be said for solvency ratios, too.

Conclusion

UniCredit is another excellent European bank to bet on banking industry growth. The bank has a healthy balance sheet, growing revenues and income, and regularly distributes dividends. The bank is profoundly undervalued based on the company`s book value and excess return valuation. Due to the reasons mentioned above, UniCredit deserves a strong buy rating.

For further details see:

UniCredit: One Of The Best European Bank Stocks, Heavily Discounted