UNCRY - UniCredit: Racing To Deliver A ~16% Yield In 2024

2023-10-24 08:33:56 ET

Summary

- UniCredit's Q3 2023 report exceeded expectations, with a 23% YoY growth in revenues and a 36% YoY growth in net profits.

- The company's strong earnings and CET1 ratio of 17.1% prompted management to guide for a 2024 shareholder distribution of "at least" €6.5 billion.

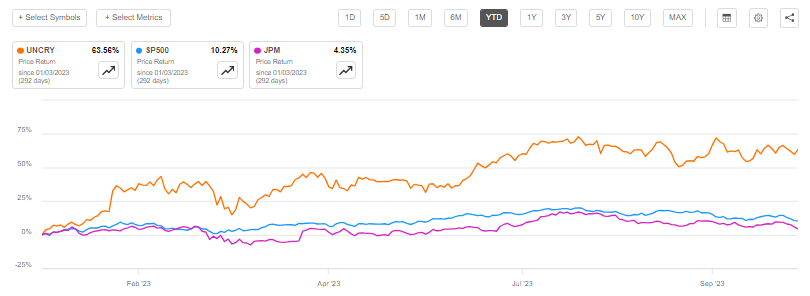

- UniCredit stock has outperformed the market, with a YTD gain of 63%, compared to 10.3% for the S&P 500 and 4% for JPMorgan.

- UniCredit's equity yield for 2024 is expected to be 16%.

- I think a 10% equity distribution yield should be enough for UniCredit investors, and accordingly, UniCredit may be 60% undervalued.

UniCredit delivered a bumper Q3 2023 report, crushing consensus on already strong expectations regarding both topline and earnings. During the September quarter, UniCredit recorded a 23% and 36% YoY growth in revenues and net profits, respectively. For the trailing nine months, the group's net profit now stands at €6.7 billion, suggesting an eye-watering €8.9 billion in profits on an annualized ROTE of 21.7%. For reference, this compares to a market capitalization of slightly below €40 billion.

Strong earnings power, combined with an industry leading 17.1% CET1 ratio, prompted UniCredit management to guide for 2024 shareholder distribution of "at least" €6.5 billion. Investors may thus consider Unicredit's one year forward equity yield, including share repurchases and dividends, quite safely above 16% -- crushing the yield of even the most popular dividend stocks. I am upgrading Unicredit stock to a "Strong Buy".

For context, Unicredit stock has strongly outperformed the market YTD. Since January 2023, Unicredit stock is up about 63%, compared to a gain of 10.3% for the S&P 500 (SP500), and a gain of 4% for banking industry leader JPMorgan (JPM).

{kind=link}

UniCredit's Strong Q3 Report

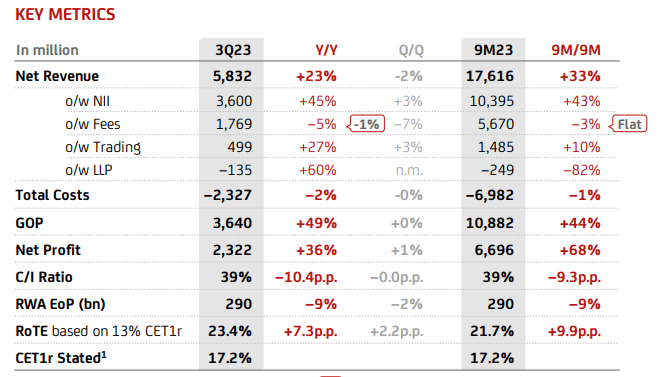

In the third quarter of 2023 , UniCredit highlighted its ability to leverage the positive effects of a favorable interest rate environment: During the period spanning from June to September, the largest bank in Italy generated approximately €5.8 billion in total revenues, indicating a robust 23% year-on-year growth compared to the same period in the previous year. On a nine month basis, revenues are up 33%, at €17.6 billion. It's worth noting that in Q3 UniCredit's revenues exceeded analyst expectations by nearly €100 million, as per Refinitiv's collected estimates.

In terms of profitability, UniCredit reported a quarterly post-profit of €2.3 billion, surpassing analyst consensus by approximately €400 million (estimated at €1.93 billion). This represented a substantial year-on-year growth of nearly 36% when compared to the third quarter of 2022. On a nine-month basis profit growth is up 68% YoY. Referencing profit numbers, UniCredit reported a quarterly post-tax return on tangible shareholders' equity of around 23.4%, which significantly surpassed the industry median of 11-12%. For reference, JP Morgan's ROTE is trending around 22%. Additionally, the bank maintained a cost-to-income ratio of 39%, down 1,040 basis points compared to the same period one year earlier. UniCredit's Common Equity Tier 1 (CET1) ratio jumped to 17.19%, supported by organic capital generation of €9.9 billion in the first 9 months of 2023.

{kind=link}

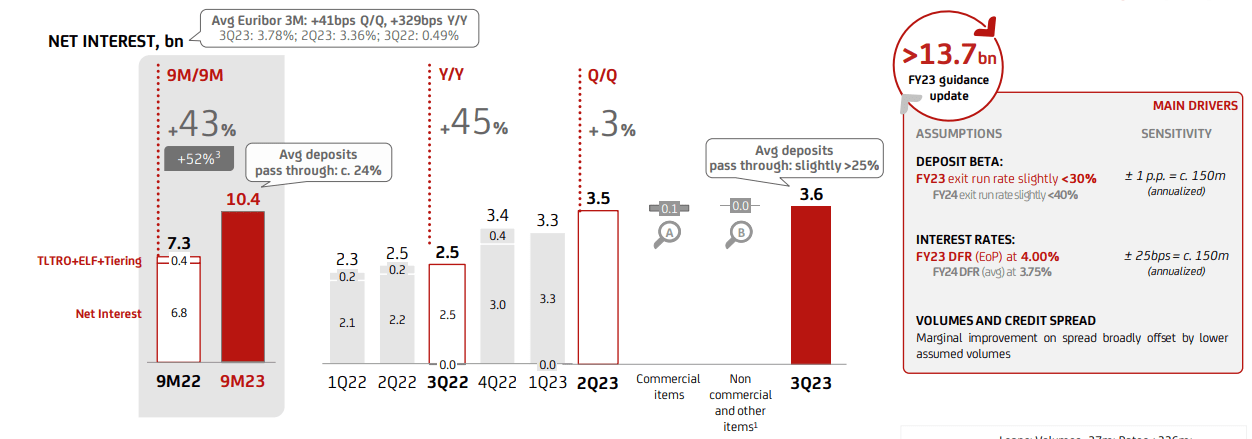

UniCredit's bumper Q3 2023 was mainly driven by a supportive rates backdrop, with the ECB' benchmark lending rate above 4%. This pushed net interest income for the trailing nine months to €10.4 billion, up 43%. But the strong quarterly result was also aided by other tailwinds: Most notably, UniCredit continues to manage the deposit beta quite well, with an average nine-month rates benefit pass through of only 24%. In addition, UniCredit reported asset write downs below expectations, as asset quality remained strong, with a cost of risk at 12 basis points.

{kind=link}

Anchored on a favorable rates, deposit beta, and credit environment, UniCredit completed the €3.34 billion share buyback announced in 2022 and proposed to front-load the €2.5 billion tranche expected for the 2H of 2023. With this decision, UniCredit is now comfortably on track to reach a 16% distribution yield in 2023.

Now, looking beyond 2023, UniCredit expects to defend the 16% yield. For 2024, the company guidance for a net profit of "at least €7.25 billion" and suggested a shareholder distribution of "at least €6.5 billion" (close to 90% payout!).

Downside Looks Very Manageable

I believe that bank investments are more secure than what the market indicates, but there's still a heightened tail-risk that, under extremely severe financial distress circumstances, could materially pressure UniCredit financials -- just think of the great financial crisis 2008-2009.

For banks, is crucial to acknowledge that fundamentals are sensitive to economic downturns and fluctuations in interest rates. Furthermore, challenges related to credit and loan risks and operational issues, such as compliance, could act as catalysts and reveal vulnerabilities that may only become apparent in a recessionary economic environment. Although as of the third quarter, I haven't identified any specific, notable risks, it's prudent for investors to remain mindful of the intricate dynamics in the macro backdrop.

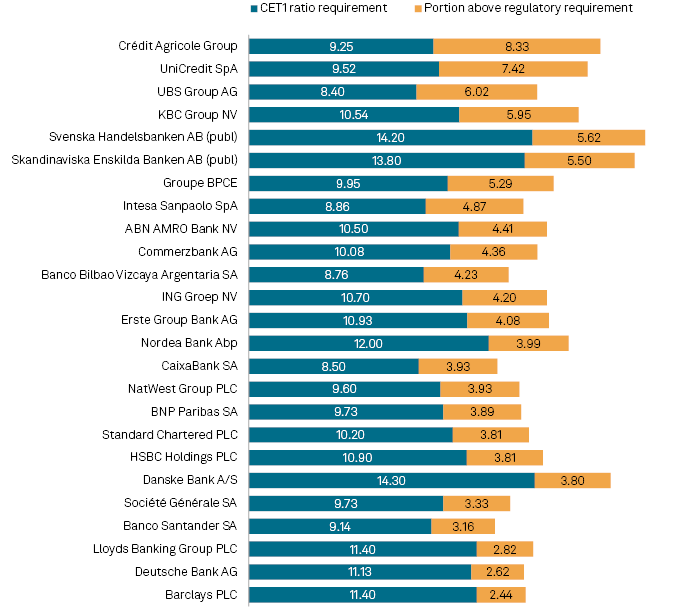

That said, UniCredit's robust 17.2% Common Equity Tier 1 ratio provides a significant safeguard for the company's balance sheet, even considering in most high-stress scenarios. In that context, I would point out that UniCredit's CET1 ratio is well-above regulatory requirements, even in light of the Basel III adjustments.

{kind=link}

Investor Takeaway

UniCredit's Q3 2023 report exceeded expectations, beating consensus on both topline and earnings. During the September quarter, UniCredit scored a notable performance, with revenues up by 23% YoY and net profits by 36% YoY. The nine-month net profit of €6.7 billion implies an annualized ROTE of 21.7%. Supported by a robust 17.1% CET1 ratio, UniCredit anticipates a 2024 shareholder distribution of "at least" €6.5 billion, against a market capitalization of under €40 billion, offering a forward equity yield well above 16%.

While bank investments generally carry some tail-risk, UniCredit's strong balance sheet, with a CET1 ratio of 17.2%, provides significant protection. And as such, I think investors are materially undervaluing UniCredit's 16% equity distribution yield. In my opinion, a yield of 10% would be more than attractive to offset the implied, idiosyncratic risk skew of the financial services industry. Aligned with this, in my opinion, UniCredit may be 60% undervalued. I upgrade to "Strong Buy".

For further details see:

UniCredit: Racing To Deliver A ~16% Yield In 2024