UNCRY - UniCredit: Solid Q3 Results Shares Attractively Valued

2023-10-24 23:28:05 ET

Summary

- Higher interest rates and benign NPL formation are still supporting outsized profitability at UniCredit, with Q3 another strong quarter for the bank.

- Earnings have likely peaked at this point, but management guidance still points to a mid-teens return on tangible equity even with lower net interest income and higher provisioning costs.

- These shares look cheap below tangible book value and with a prospective shareholder yield of around 16%.

For a long time, Italian banks like UniCredit ( UNCRY ) were struggling under the weight of chronically low interest rates and a very high stock of non-performing loans. Well, what a difference a year or two can make. Higher rates in the Eurozone have been a nice tonic for previously squeezed net interest margins ("NIM"), while good historical work on bad debt and a supportive macro environment is paying off in the form of benign NPL formation and low cost of risk. As a result, UniCredit and Italian peers like Intesa Sanpaolo ( ISNPY )( IITSF ) are now among the most profitable banks in Europe having previously been laggards.

UniCredit recently released Q3 2023 figures. Although net interest income is reaching its cycle peak, numbers on the whole were impressive. Revenue and credit quality both remain strong, and the bank's profitability remains stellar. While UniCredit is definitely over-earning right now in a still-supportive macro environment, that doesn't necessarily make these shares expensive. Indeed, trading below tangible book value they remain cheap.

Record Profitability

"From laggards to leaders in all key metrics" is how management describes UniCredit's recent performance, and while often those kinds of comments should be taken with a pinch of salt, in this case, it is a fair reflection of the transformation that has taken place. UniCredit generated an annualized return on tangible equity ("ROTE") of 18.4% in Q3 – around double what the bank was averaging in the low rate, pre-COVID 2015-2019 era. Year-to-date ROTE (~21.4%, albeit based on a 13% CET1 ratio) was a record according to management.

Net interest income ("NII") and strong asset quality continue to support profitability. Q3 NII was €3.6 billion, up a little under 3% sequentially and 45% year-on-year. Higher rates are a boon for UniCredit as it has allowed bank to unlock a lot of value from its deposit franchise, with deposit beta still only at around 25% as of Q3. Performance in its core Italian home market (~50% of pre-provision earnings) will be even better, as Italy accounts for the vast majority of its sticky retail and SME (small and medium-sized enterprises) deposits. Sight deposits (i.e. instant access) amount to around €340 billion – a level that has been relatively consistent throughout the hiking cycle – funding around 40% of the bank's assets.

The benefit of the above gets lost in a very low interest rate environment but is a massive boon when rates rise. Although UniCredit's loan balances aren't growing (indeed balances have fallen for several straight quarters), higher rates have led to around 80bps of NIM expansion since the ECB began hiking in mid-2022 (Fig 1). Operating costs have remained flat-to-down in that time, leading to a surge in pre-provision earnings (Fig 2).

Fig 1. (Data Source: UniCredit Quarterly Results Releases) Fig 2. (Data Source: UniCredit Quarterly Results Releases) Fig 3. (Data Source: UniCredit Quarterly Results Releases)

At the same time, asset quality metrics have remained robust. Q3 was another very strong quarter, with stage 3 loans again coming in flat at around 2.7% and NPL formation remaining at record lows (Fig 3). As a result, cost of risk ("CoR") was again low in Q3 at just 12bps – and this is helping to drive record profitability right now.

With regards to risks, UniCredit's loan book does skew to corporate and SME lending (~75% of loans) as opposed to retail, and I have my concerns as to how that would hold up in a sharp downturn. I would note that the bank's Stage 2 loan ratio (~17.5%) is rather high, albeit there is a subjective element to this (i.e. management could be adopting an overly cautious view of things). On the flip side, UniCredit's most recent stress test result was strong, with its CET1 still seen above 12.5% even in an adverse scenario.

Earnings Have Peaked, But Shares Not Necessarily Expensive

Q2 and Q3 are likely to mark the high points for UniCredit's earnings. We are at or very near the top in terms of the hiking cycle, with NII pressure still coming from higher funding costs and muted loan growth.

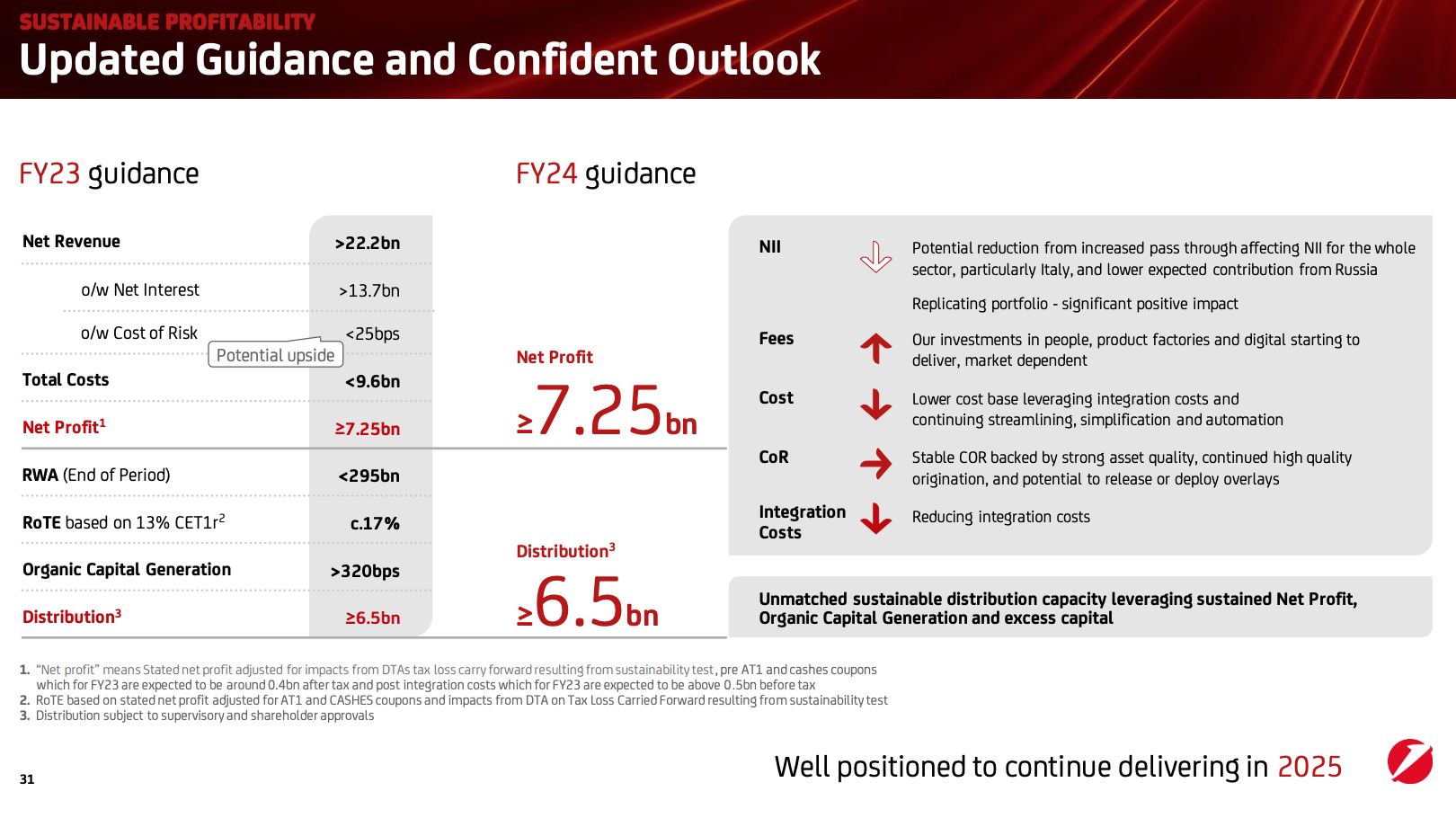

FY2023 NII guidance was actually raised following Q3 results (to at least €13.7 billion), implying around €3.3 billion in Q4 NII. NII is likely to carry on falling into FY2024, albeit relative to the pre-2023 low interest rate era it is still going to be high. At the same time, normalizing CoR is also going to eat into earnings as provisioning is currently at unsustainably low levels.

While the above amounts to a headwind to earnings, we need to put it into the context of UniCredit's current share price and profitability. The stock trades for €23.00 per share in Milan trading (~$12.20 for the ADSs; ticker "UNCRY"), which is only equal to around 0.85x tangible book value per share ("TBVPS"). That looks like a very steep discount given the bank just earned a high-teens ROTE last quarter. What's more, management is guiding for around €7.25 billion in FY2024 net profit, which would map to a ROTE of around 15%. As a rough guide, that would mean CoR increasing to around 35bps and NII falling by around €1 billion or so, with fee income and operating costs roughly flat.

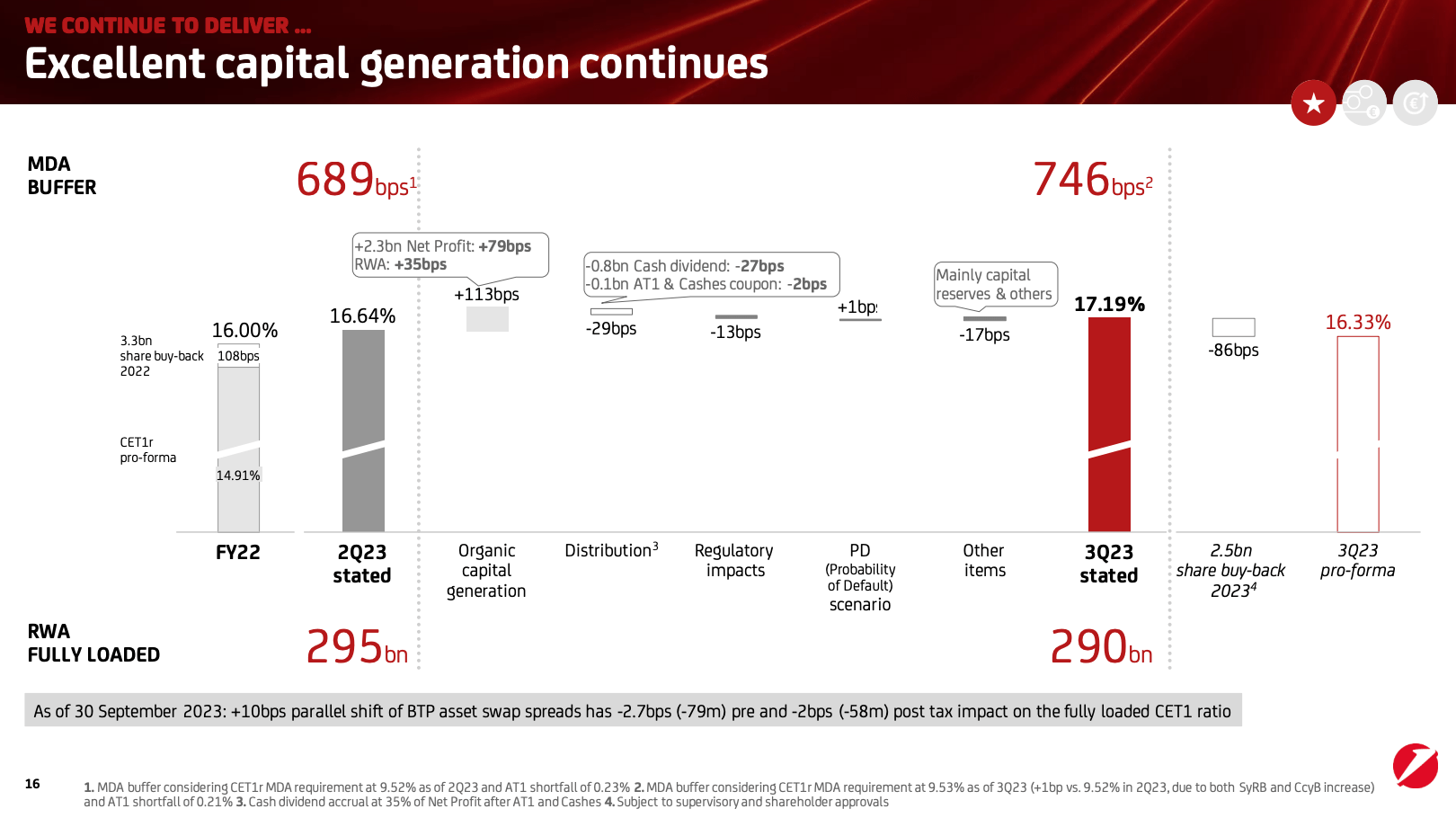

Moreover, management plans to pay out at least €6.5 billion to shareholders in FY2024 (in line with FY2023). That equates to a circa 16% implied shareholder yield based on a current €40 billion market cap (Fig 4). Alongside capital generation, the bank is sitting on a lot of surplus capital (CET1 was 17.2% in Q3)(Fig 5), further lending support to its capital return plans.

Fig 4. (Source: UniCredit Q3 2023 Results Presentation) Fig 5. (Source: UniCredit Q3 2023 Results Presentation)

{kind=link}

{kind=link}

For UniCredit to be fair value right now, I think you would have to be assuming that its through-the-cycle ROTE would fall back to around the 9% area. That, in turn, would require a return to chronically low interest rates alongside a significant uptick in CoR. While I don't discount that happening, it is already in the share price. Even an 11-12% through-the-cycle ROTE could drive around 30% upside to 1x TBVPS. In the meantime, attractive capital returns will continue to provide support to these shares. Buy.

For further details see:

UniCredit: Solid Q3 Results, Shares Attractively Valued