UNCRY - UniCredit: Top-Rated And Undervalued

2023-07-18 18:28:11 ET

Summary

- UniCredit S.p.A. is a $45-billion market cap commercial bank based in Milan, Italy.

- The bank reported strong financial results for Q1 2023, driven by favorable interest rates, well-managed deposit rates, and robust commercial performance.

- Despite the successful implementation of the management plan and its ongoing progress, the market undervalues UNCRY's growth potential, in my view.

- The fair value of the stock, in my opinion, is at the level of 7 times next year's earnings, which equates to about $16.38/sh. on available consensus EPS data.

The Company

UniCredit S.p.A. ( UNCRY ) is a $45-billion market cap commercial bank based in Milan, Italy. It provides retail and corporate banking services, including payments, trade finance, and capital market solutions. The bank also offers sustainable finance, project finance, and advisory services. UniCredit is actually a group of companies that operate in multiple regions and serve a wide range of clients, including corporations, financial institutions, and individual customers.

UniCredit reported strong financial results for Q1 2023 , driven by favorable interest rates, well-managed deposit rates, and robust commercial performance. The group achieved exceptional revenue growth, with net revenues totaling €5.9 billion, representing a significant 18.3% increase compared to the previous year. This growth was supported by solid net interest income of €3.3 billion [+43.6% YoY] and fees of €2.0 billion [-2% YoY] while operating costs amounted to €2.3 billion [-0.6% YoY] and loan loss provisions stood at <€0.1 billion [way lower than in Q1 FY22].

{kind=link}

The bank demonstrated its commitment to managing risk effectively - UniCredit's credit portfolio quality remained resilient, with high coverage and a structurally low Cost of Risk (CoR) of 8 basis points in Q1 2023. The management maintained its CoR guidance of 30-35 basis points for the full year, with the potential for even lower levels.

The bank's capital efficiency in Q1 FY2023 was also strong, with organic capital generation of 111 basis points in the quarter, resulting in a CET1 ratio of 16.05% - over 200 b.p. higher on a YoY basis:

{kind=link}

Despite the difficulties in keeping deposits on the balance sheets of some banks due to rising market interest rates for money market instruments, UniCredit recorded a 4.4% year-on-year increase in assets on its balance sheet in 1Q FY2023 due to the growth of loans to banks [+57.3% YoY]. At the same time, the value of net bad loans decreased by 44.1% YoY. The group consolidated ~€188.7 billion of total liquid cash by the end of the quarter, an increase of ~7.1% compared with the previous quarter (in Q4 FY22). UniCredit is one of the strongest banks in terms of balance sheet health I've seen for the past few months.

The management has not yet announced a specific date for the bank's exit from Russian assets. However, the bank previously stated that it is "committed to disengaging from Russia in an orderly and decisive fashion." This suggests that the exit process could take several months or even years to complete. But it is already apparent that the bank is no longer expanding its credit base in Russia, thereby shifting its focus to other regions and, against this backdrop, it seems less risky in terms of geopolitical risks.

UniCredit's data book

{kind=link}

During the latest earnings call , CEO Andrea Orcel shed some light on the company's corporate development strategy, which can be divided into 2 phases.

The 1st phase, which is already underway, is aimed at reducing UniCredit's cost base by €1.5 billion by 2024. The bank is achieving this by cutting jobs, reducing IT costs, and streamlining its operations. The bank is also focusing on improving its profitability by increasing its revenues and by managing its risks more effectively.

The 2nd phase, which was expected to begin someday this year, is focused on growth and innovation. The bank is targeting €5 billion in new revenue growth by 2025. This growth will be driven by expansion into new markets, such as Asia, and by the development of new products and services. The bank is also investing in digital transformation and data analytics to improve its customer service and make its operations more efficient.

As far as I can tell, UniCredit is probably one of the most reliable banks I have seen in recent times. The first phase of development that management is talking about is already showing its fruits in the latest financial reports. The second phase of development should only accelerate the bank's modernization and provide additional marginality benefits [read - "higher EPS"].

Therefore, in my opinion, investors should consider the bank as a potential investment. Provided, of course, that one does not have to pay too much for this investment. Let us just take a look at it.

The Valuation Is Too Tempting To Pass By

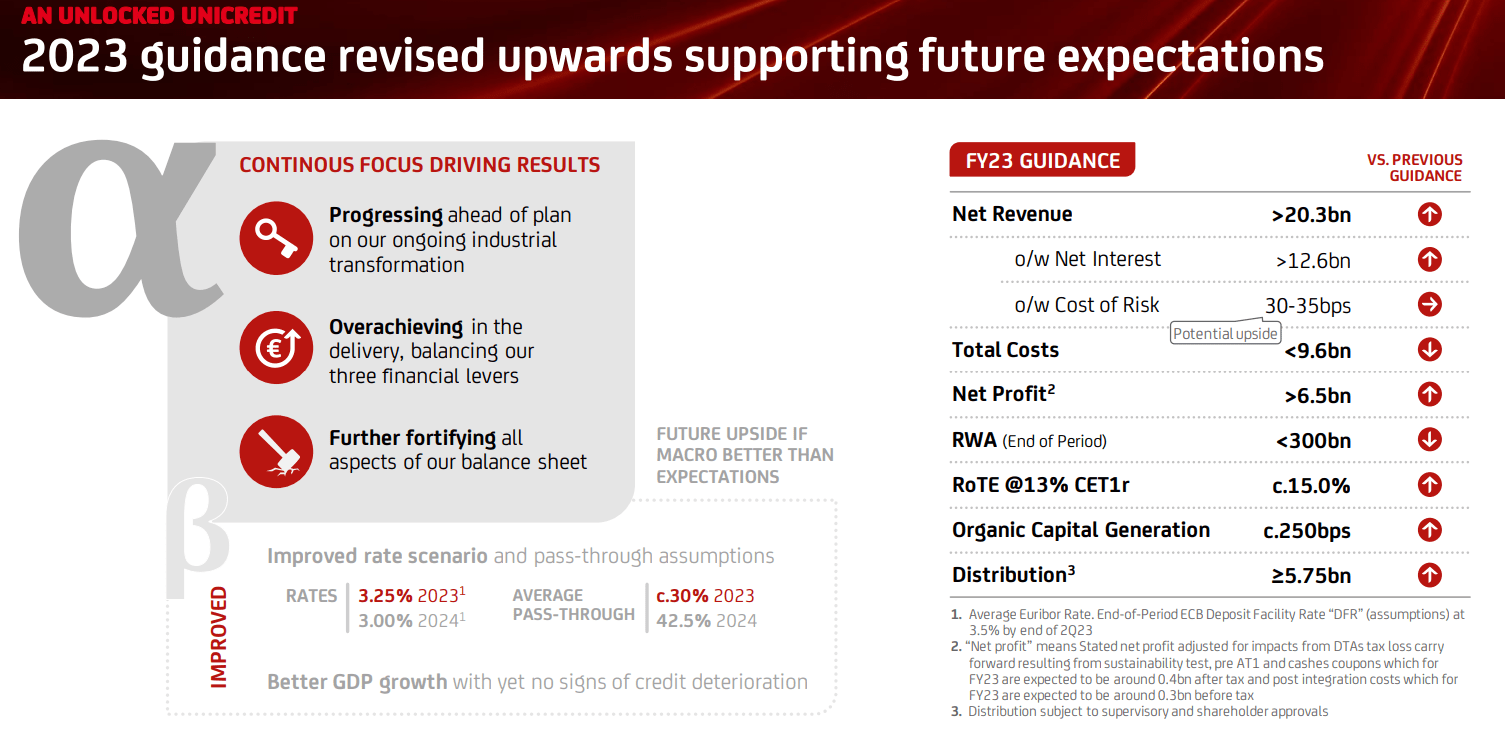

Based on its positive financial performance and the supportive interest rate environment, UniCredit revised its financial guidance for FY2023. The bank now expects net interest income to exceed €12.6 billion, net revenues to surpass €20.3 billion, and net profit to exceed €6.5 billion. UniCredit also increased its shareholder distribution intention for FY2023 to at least €5.75 billion, reinforcing its commitment to delivering shareholder value.

{kind=link}

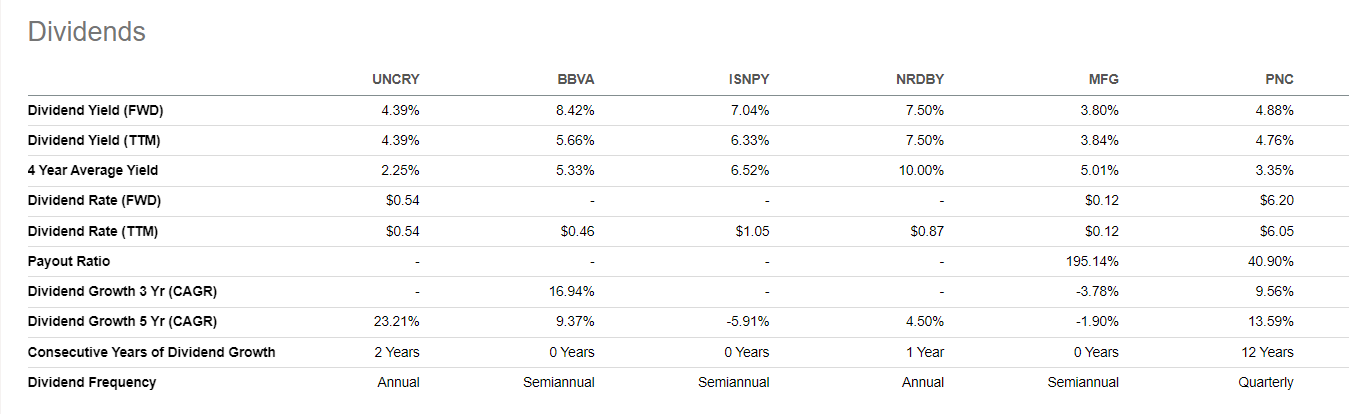

Is it a lot for UNCRY - €5.75 billion in distributions? According to my calculations, this is ~11.5% of total return (distributions on market capitalization), which is very significant for such a large bank as UNCRY. This fact should compensate for the bank's relatively low dividend yield compared with other peers of the same size:

{kind=link}

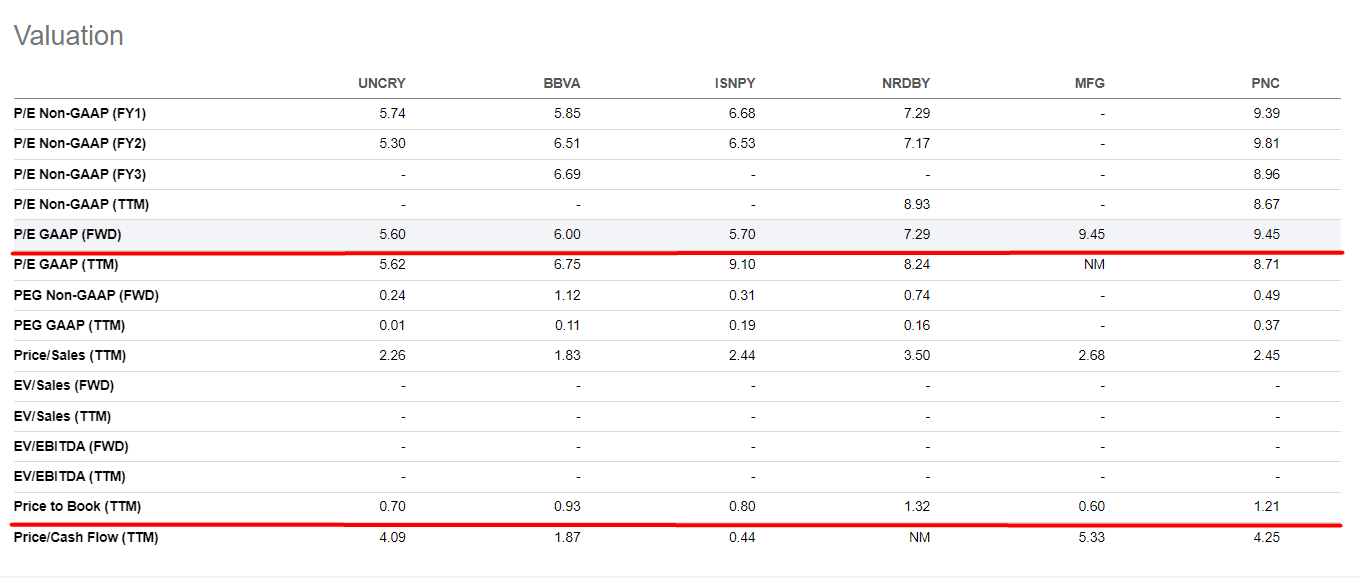

Even in absolute terms, I think UNCRY's valuation multiples are heavily discounted. Paying 5.6 times next year's net income for a company that returns about 11.5% of total compensation to shareholders sounds like a steal to me.

{kind=link}

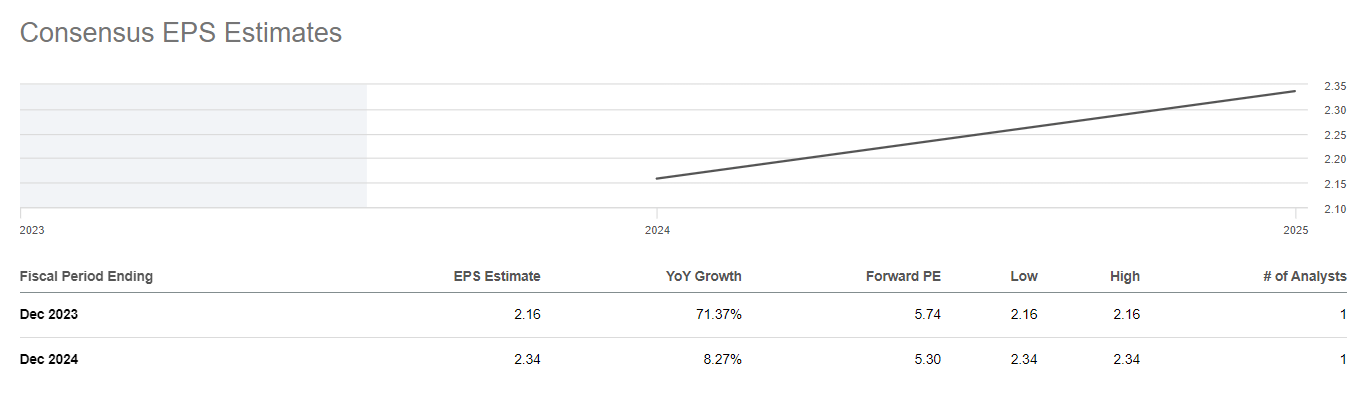

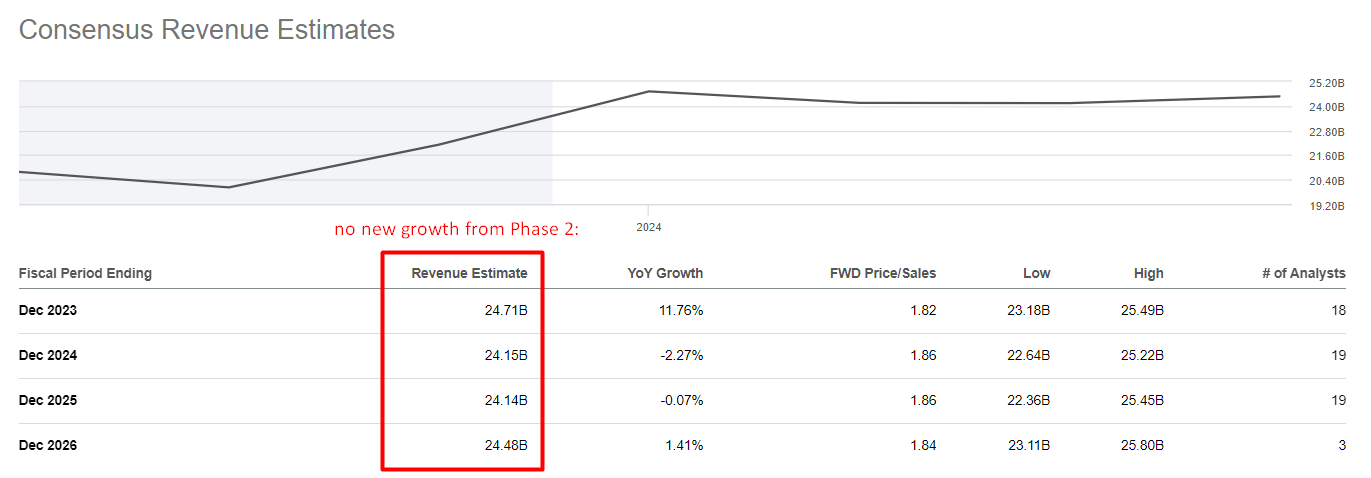

And the most interesting thing is that Wall Street is still not taking into account management's plans to expand the revenue base by €5 billion by FY2025:

{kind=link}

{kind=link}

I suspect that the market expects a cyclical downward movement in the bank's ROE, as was the case in 2020 - hence the low P/E multiples:

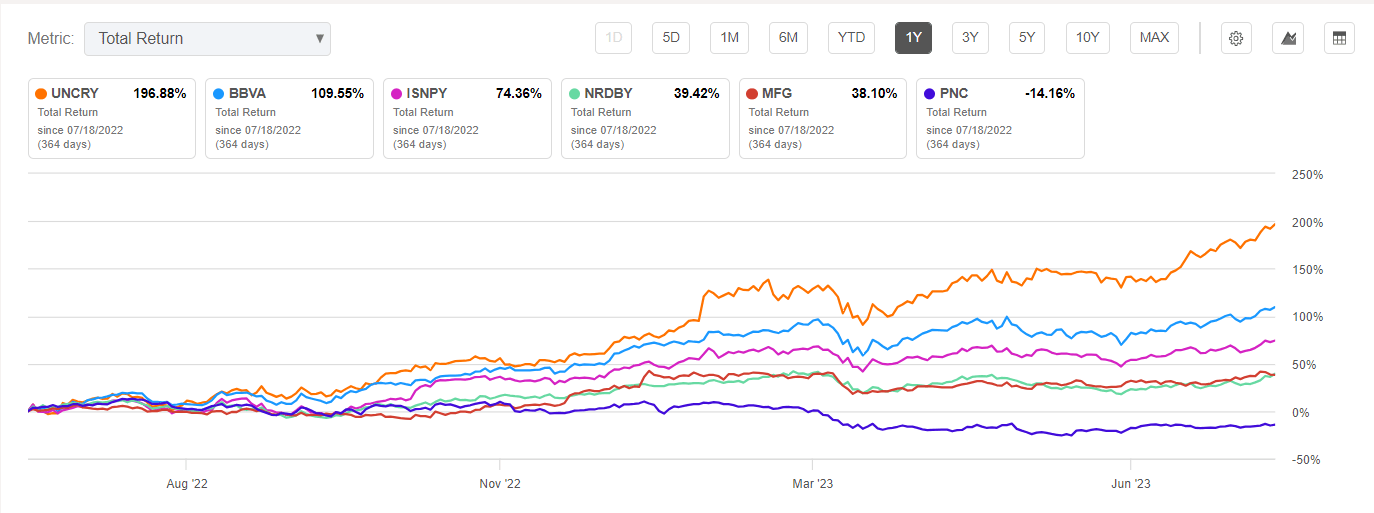

However, I see no fundamental reasons for such a turnaround now. Yes, central bank interest rates should start falling soon - the management seems to be already fully prepared for this. The strategic development plan itself does not depend much on what the head of the ECB will say at the next meeting. Structurally, the bank is solid and planning for growth rather than decline over the next year, while trading at a deep discount - this is the reality that UNCRY multiples stubbornly ignore. At the same time, the lack of multiple expansion does not stop the stock from actively soaring:

{kind=link}

The Bottom Line

Of course, UniCredit faces various risk factors that could negatively impact its business and financial performance. Geopolitical risks, including war, terrorism, and political instability, pose a threat due to the bank's global operations in over 17 countries. Economic risks, such as recessions, financial crises, and interest rate fluctuations, also pose challenges. The complex regulatory environment exposes UniCredit to regulatory risks, and changes in regulations could have adverse effects. Operational risks, including fraud, cyberattacks, and IT failures, further add to the risk profile. Additionally, credit risks associated with the lending business and market risks, such as interest rate changes and stock market volatility, could affect UniCredit's financial stability and stock price performance.

Despite these risks, I still tend to be optimistic about the UNCRY stock. Given that management has proven the viability and effectiveness of the new business development strategy in practice, and that this strategy is still far from being fully realized in terms of the initial idea itself, I believe that UNCRY stock still represents great value for investors seeking stable income and total shareholder return in the coming years.

The fair value of the stock, in my opinion, is at the level of 7 times next year's earnings, which equates to about $16.38/sh. on available consensus EPS data. The upside potential is thus about 32.3% of the price at the last trading day close.

Thank you for reading!

For further details see:

UniCredit: Top-Rated And Undervalued