NSRGF - Unilever Hasn't Been This Cheap Since More Than A Decade

2023-12-20 06:16:04 ET

Summary

- Unilever's shares have underperformed the market for the past few years but may be at a turning point towards recovery.

- The company's valuation and normalized P/E ratio suggest that Unilever hasn't been this cheap for more than a decade, also compared to its peers.

- Commodity inflation has cooled down and UL's 2-year revenue growth has been in line with most of its peers.

- I believe Unilever is quite undervalued at the moment and is a potential turnaround story with Nelson Peltz on the board.

Household, personal care, and food producer Unilever ( UL ) has had a rough time. Although its shares did not crash, they have steadily underperformed the broad market for the last couple of years. At this moment, the company's valuation and its normalized PE ratio show that Unilever might be cheaper than ever. In this article, I will explain why I believe that it is likely that the company is situated at a turning point towards recovery at the moment, and why it is my favorite pick for 2024.

A brief look back at the past

Unilever has been one of the first stocks I invested in, and I have been holding the company's shares for more than a decade in my retirement account. Paying a decent dividend, it is a buy-and-hold stock for me, and I'm not intending to sell my shares at any time. But this doesn't mean that investing in this company has been a bed of roses.

I already wrote about Unilever a couple of times, though most of my articles are already quite old. I believe that, with recent developments surrounding the company and its recent (under)performance, my thesis urgently needs an update.

Of the writing that I still consider relevant, in this article, written in 2021, I wrote about 3 risks for Unilever in the short to mid term, namely commodity inflation, e-commerce, and store brands. After that, at the start of 2022, I tried to analyze the relative underperformance of Unilever compared to its peers, which you can find here . I reached the conclusion that it is likely that a large part of the underperformance could be explained by the large exposure of Unilever to commodity inflation, especially soybean and palm oil.

Underperformance

Unilever has probably not been the star of anyone's portfolio over the last couple of years. But there have been more companies in the consumer products business that have not performed well. Let us compare Unilever with some of its peers, namely Procter & Gamble ( PG ), Nestlé ( NSRGY ), Colgate-Palmolive ( CL ) and Mondelez ( MDLZ ). As a reference, I will also list the performance of the S&P 500 ( SPY ) in the graph:

I chose the last three years as time period, but I might as well have chosen 1, 5 or 10 years: in any of these time periods, Unilever underperformed its peers. Of course, compared to the benchmark of the S&P 500, more consumer conglomerates did not perform well, but Unilever has been the worst performer of this selection.

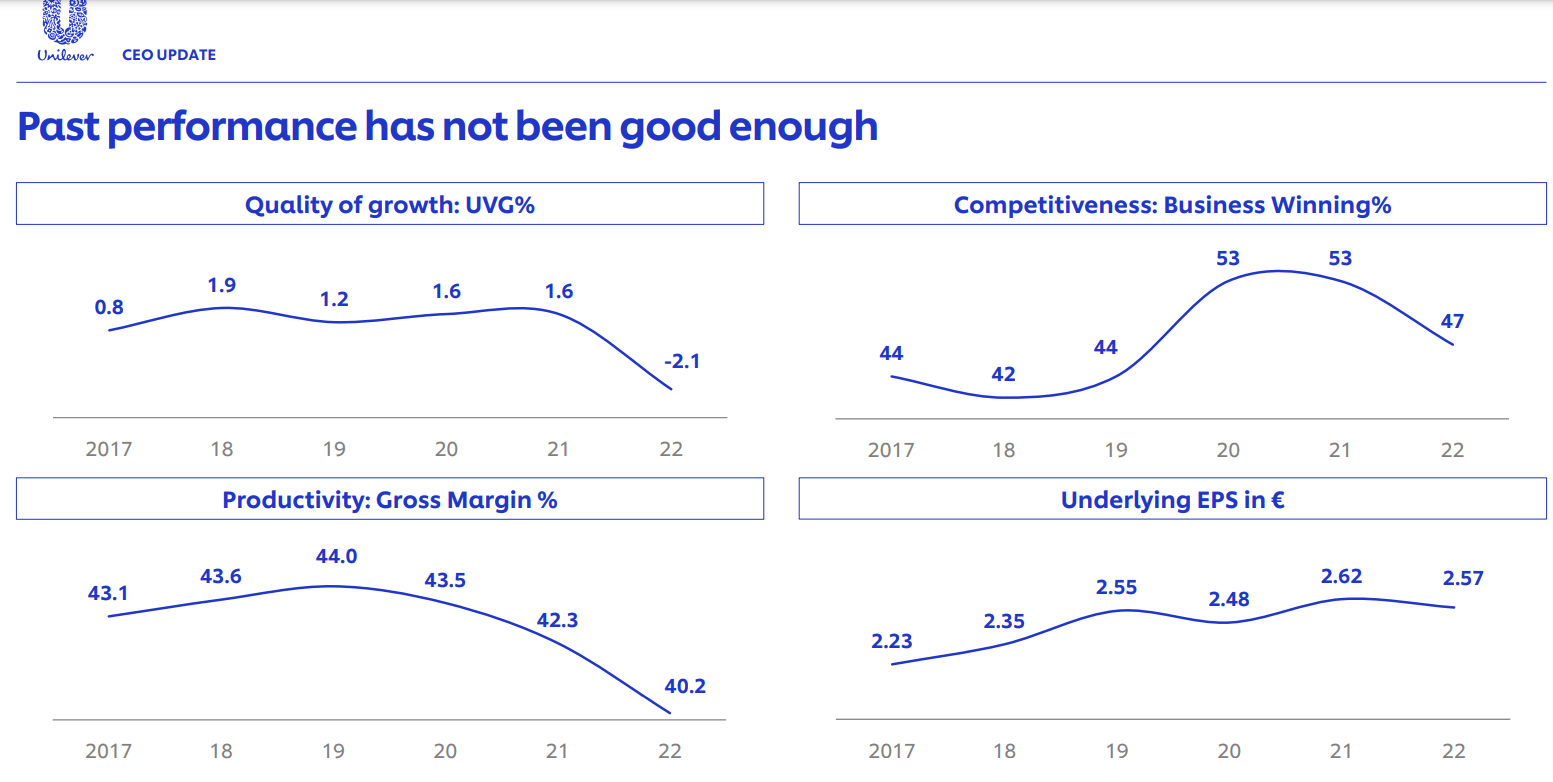

Unilever itself also acknowledges that its past performance has not been good enough. As the CEO Hein Schumacher mentioned in the Q3 2023 CEO Update, there have been multiple areas in which the company wants to improve.

Unilever past performance (Q3 2023 Trading Statement & CEO Update)

{kind=link}

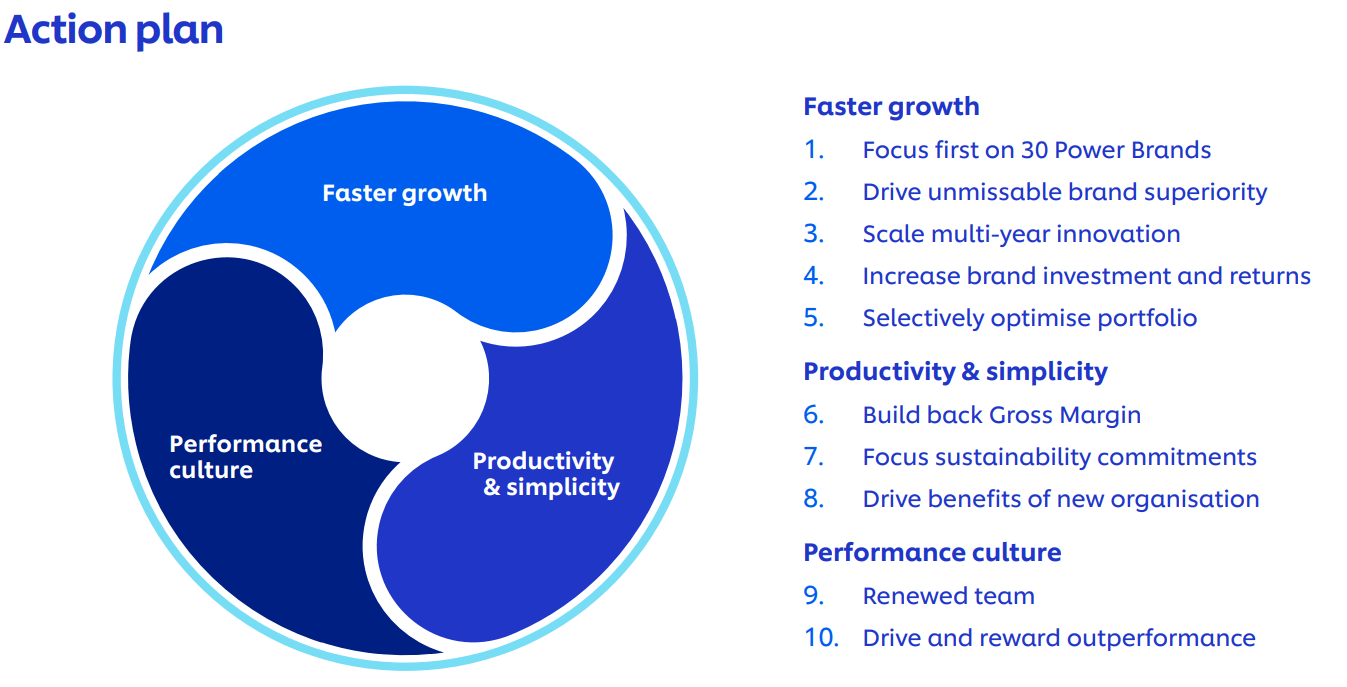

To tackle these issues, Unilever has developed an action plan that focuses on three key areas, which I pasted below:

Action plan (Q3 2023 Trading Statement & CEO Update)

{kind=link}

In the Q3 presentation, these topics are further detailed and explained. Most important seems to be the focus on the 30 most important 'Power Brands'. I agree that with these brands, there seems to be scope for improvement for Unilever. Revenue growth and margin improvement are noble targets to pursue, but in my opinion, it remains to be seen if this plan is a big enough change from the 'business as usual' approach to truly make an impact for Unilever.

On the bright side, with Nelson Peltz on the Unilever board since last year , this might be the first kick-off of an eventual transformation of the company like he pulled off at Procter & Gamble. At Procter & Gamble, focusing on the winning brands and cutting out the losers paid off handsomely, so this strategy should not be underestimated.

Known causes of underperformance

In a previous article, I wrote about two of the main reasons for Unilever's underperformance: the company is much more exposed to inflation in soybean oil and palm oil than its competitors, and it showed a much worse revenue growth.

Let us investigate whether these two issues have deteriorated or improved. First, commodity inflation:

In this graph I took the Malaysia Palm Oil Futures Price, the development of which is comparable to the world palm oil futures. Since my previous article, which was written at the start of 2022, palm and soybean oil prices have stabilized (in the case of palm oil) and sharply dropped (in the case of soybean oil). This is a good sign.

Of course Unilever is dependent on more commodity prices than only these two, but palm and soybean oil have an enlarged impact on the supply chain, and as such might be able to explain differences in performance between Unilever and its peers.

Let us take a brief look at revenue growth of Unilever compared with its peers:

As we can see, for 2023 Unilever is all the way down in the graph, but differences between it and most of its peers are relatively small, with the exception of Mondelez. Also, in 2022 Unilever's revenue growth was relatively high. Of course, from 2019 to 2021, Unilever's growth rate was negative. But when we look at the past 2 years, revenue growth of Unilever has been more or less in line with most of its peers. And at least it did not drop anymore like during the years before 2022.

It is mostly out of scope for Unilever to directly influence global commodity prices, but with regard to their revenue growth, the company does have more direct power. Partly, Unilever tries to address their lackluster revenue growth in their action plan mentioned in the Q3 financial update. At this moment, it looks like Unilever is not underperforming their peers anymore with regard to revenue growth.

Valuation

Let us take a look at the normalized PE ratio of Unilever over the last 12 years This is the longest time period I can generate for this metric on YCharts:

I first wanted to title this article 'Unilever might be cheaper than ever' because I was not able to find any reliable proof of a lower normalized PE ratio for Unilever anywhere in the past. But since the company is already very old, it is very likely that its shares traded for a cheaper multiple in the past, but we know for sure that this moment was at least more than a decade ago.

But is this an industry-wide phenomenon or is Unilever just cheap as a company? Let us again look at Unilever's peers:

For this chart I took the forward PE ratio because the normalized PE ratio showed distorted data for some of the peers. What is clear about this graph is that since 2022, PE ratios for consumer products giants have slowly but steadily decreased. This was likely influenced by increased interest rates which can behave like a competitor for the all-weather dividend-paying companies in this industry.

We can also conclude that Unilever is the cheapest of my selection of peers. And not only that, the discount for Unilever shares has actually increased during the last couple of months. During the last three years, Unilever has always been one of the cheapest companies (in 2021 together with Mondelez), but during the last 2 years this difference has become larger, not smaller.

Risks

One of the most attractive things about an investment in Unilever is that I believe risks are relatively limited at this moment:

- The company is trading for a low multiple, compared with both its own past and its peers.

- Commodity inflation has cooled off and seems to be heading towards more normal territories, which decreases pricing pressure for Unilever and could improve margins.

- The action plan and Nelson Peltz's involvement could lead to company transformation.

- Unilever pays a decent dividend with a yield of almost 4%

- The company, being active in consumer products and having a healthy balance sheet, is quite immune to 'higher for longer' interest rate environments. It looks like interest rates will go down again in 2024, but even if they stay elevated, Unilever is likely to continue to deliver.

Some risks for Unilever during the next year are:

- The transformation might not bear fruit or might go horribly wrong. But thinking back at previous big changes at Unilever, I believe the company is prudent and mature enough as to create a margin of safety so that failure will not turn out to be disastrous.

- Commodity inflation could return with a vengeance. Although it does not look like this will happen soon, strong commodity inflation is probably one of the most impactful risks for Unilever, as it impacts the company most compared with its peers.

- Revenue fails to grow and might even drop. If this happens, especially if it happens alongside margin deterioration, Unilever fully deserves its low multiple and might drop more. But I do not expect a crash in this case.

Takeaway

Unilever has become cheaper over the last couple of years, also when comparing the company to its competitors. Yes, Unilever has had a very bad revenue growth rate, but over the last 2 years this has recovered to a level that is in line with its peers. Also, commodity inflation might still be an issue, but prices of soybean and palm oil show that the severity of this factor has likely greatly diminished. Furthermore, Unilever's profit margin remained relatively solid compared with its peers, although it dropped recently. And last but not least, with Nelson Peltz on the board since last year the company might have the potential to create a P&G-like turnaround in the future. I feel the market has not started to price in this possibility.

So, the valuation difference between Unilever and its peers has increased, even though most of the reasons why the company was undervalued in the first place have become much less important. I believe that Unilever deserves a valuation slightly below its European peer Nestlé. A forward PE ratio of about 19 would be fair in the short term. This would mean that Unilever has room to rise 13%, from a current share price of $46.67 to around $53. With an additional safety margin of a dividend yield of almost 4%, this would mean a return of 17% if my price target is hit.

I am giving Unilever a buy rating. This company is at the sweet spot between being a plausible recovery story and an all-weather investment and is my favorite pick for 2024.

Please take note that I might be biased in my analysis, having been a shareholder in Unilever for over a decade. But this doesn't mean that my analysis is useless. In fact, I invite others who have not known the company for such a long period to share their insights in the comment section. By all means, tell me if I'm wrong and if I missed something important.

Even though I believe this is a very attractive opportunity, I will not buy additional shares of Unilever for my investment accounts, simply because I already own a full position. But for investors who are looking for an all-weather stock with a decent dividend and recovery potential with a Nelson Peltz kicker, Unilever might just be the one.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Unilever Hasn't Been This Cheap Since More Than A Decade