UL - Unilever: New CEO Making Changes

2023-12-04 12:53:49 ET

Summary

- Unilever is undergoing a management change and starting fresh with a new approach, showing potential for a turnaround.

- The valuation gap between Unilever and its competitor Procter & Gamble is widening, suggesting undervaluation of Unilever.

- Unilever has a number of key strengths, including its strong position in emerging markets and a well-diversified and innovative product portfolio.

Unilever is one of the biggest consumer packaged goods companies in the world amongst the likes of Nestlé ( NSRGY ), Procter & Gamble ( PG ), and Kraft Heinz ( KHC ). Despite Unilever being a global powerhouse in the FMCG sector, the company's stock price has underperformed its competitors in the last five years and its valuation is relatively low compared to its peer group trading at 15 FWD P/E.

I believe that Unilever is still a world-class business able to compete with the likes of Nestlé and Procter & Gamble. If the new CEO manages to turn it around, there is potential to unlock a lot of value. Compared to its peer group, Unilever trades at a relatively cheap valuation which provides a potential buying opportunity for value investors.

Over the past five years, the stock performance has been less than stellar, the stock is down about 10% while its main competitor Procter & Gamble is up 70% over the past five years. Unilever's shareholders are unhappy and they have called for management to step up its game and rightly so. As a form of backlash, bonuses have been scrapped and the new CEO's salary is capped.

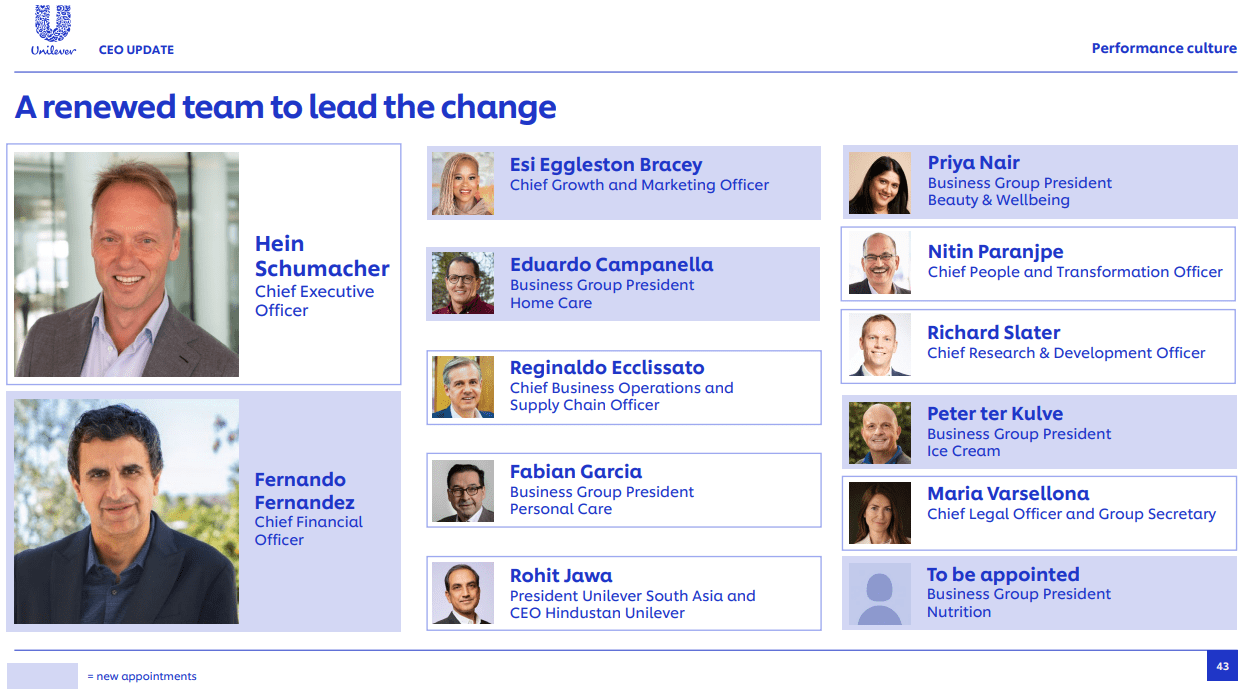

The company is now going through a transition phase with a big management change involving a new CEO. He is making a big sweep across existing positions and starting with a clean sheet. Activist investor Nelson Peltz has also been on the board since last year, aiming to ignite a turnaround improve the company's performance on the stock market. With a new strategy, the goal is to improve performance by building back gross margins and focusing on more organic growth.

New CEO and Strategy Changes

Unilever recently got a new CEO, Hein Schumacher. He is willing to make some changes involving toning down Unilever's ESG ambitions and purpose marketing, in favor of financial performance and shareholder returns. The market has responded somewhat negatively to the management change due to uncertainty, but I see this mostly as a positive change. I am of the view that Unilever made a string of bad decisions under the previous CEO Alan Jope, involving the failed takeover attempt of GSK 's ( GSK ) consumer health business for $50 billion that was almost half the market cap of Unilever itself. This was a case of, what I think, a minnow trying to swallow a whale; the size of the takeover was much too large and Unilever's share price was punished by investors (rightly so). Moreover, the fit between GSK's consumer health products and Unilever's business was very unclear. Investors were unhappy with management because of this takeover attempt (among other reasons) and bonuses have been scrapped; 60% of the shareholders voted against the remuneration policy at the 2022 AGM. Moreover, key management positions of underperforming divisions have been replaced , new people are now leading divisions like nutrition and ice cream. Now, new management will take over the wheel and try to turn it around.

{kind=link}

Management changes (Unilever, 2023)

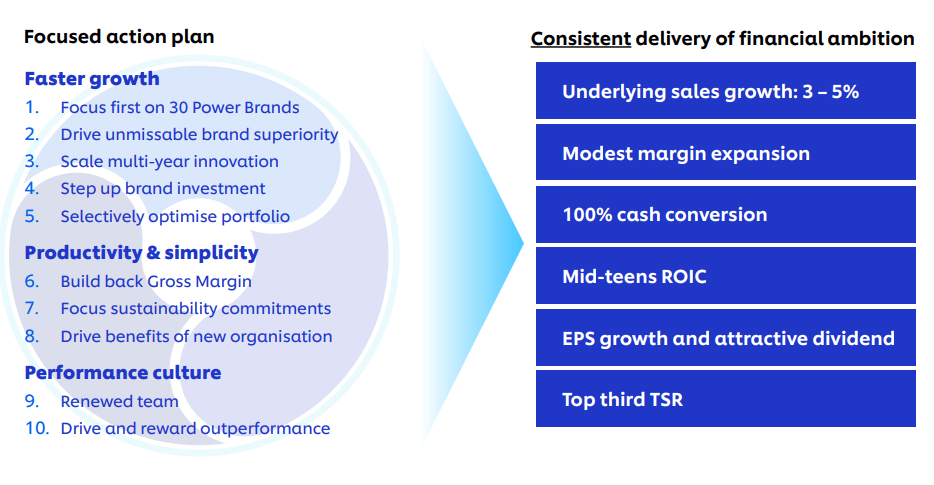

The CEO introduced himself during the latest earnings call and presented his new strategy to improve the company's performance. However, the latest Q3 earnings call was not well received by the market, and the stock dropped three percent after the earnings call. The CEO was very self-critical during the earnings call and pointed out several things for improvement, which was negatively received by the market because it might be seen a sign of weakness. Personally, however, I found it very positive because I would rather have a CEO that is self-critical and aims to improve things, than someone who says everything is going great irrespective of reality. In particular, I liked his strategy to focus on higher organic growth instead of doing major acquisitions, and he shared several cost-cutting initiatives that will help the bottom line.

{kind=link}

Unilever Outlook (Unilever Q3, 2023)

There were some one-off impacts that impacted Q3 earnings but these are not structural issues in my opinion. More specifically, there was an 8% impact of FX and bad weather conditions have impacted ice cream sales negatively.

Company Overview: Well Diversified Portfolio

Unilever is a juggernaut and one of the largest consumer packaged goods in the world . Their product portfolio is well diversified across different segments, entrenched with big brands and household names such as Dove, Ben & Jerry's, Magnum, Omo, Knorr etcetera. It's a wide moat business with a lot of market power. While most investors might know Unilever from their nutrition- and ice cream brands, these make up less than 50% of total sales. Next to food products, their also sell home care items like laundry detergent (e.g., Omo), personal care (e.g., Axe aka Lynx in UK) and beauty products (e.g., Dove). These high-quality branded products are consumer favorites and remain in high demand, allowing Unilever to charge premium prices with pricing power.

Revenue Split (Own research, 2023)

Main Competitors and the Valuation Gap

Unilever's main competitor is Procter & Gamble, the valuation gap is widening between PG and UL even though the gap in profits is shrinking. This valuation gap should therefore be closed. P&G is currently valued 3 times as much as Unilever, but it only makes less than twice as many net profits. So based on this simple relative comparison, it seems that UL already has substantial upside potential to close this valuation gap to its US competitor.

Another important competitor is Nestlé. Here again, the valuation of Nestlé is three times that of Unilever, but the amount of net profits are relatively similar and the profit gap is closing. Unilever's increased its profits recently while Nestlé's profits have decreased. This suggests that the valuation gap between Nestlé and Unilever should become smaller than it is now.

Competition from Store-Branded Products

Next to P&G and Nestlé, Unilever competes against private label brands sold by retailers. During times of high inflation, the dynamic is that consumers are trading down to cheaper private label products (i.e., store brand). However, academic marketing research has shown that this dynamic is cyclical. Competition between private label and premium label products has been going on since the 1900s and the dynamics have stayed the same. The proportion of people using private label or branded products remains relatively stable over time, but fluctuates depending on the business cycle. During bad economic times, some consumers cut back and buy private label, and during good times people spend more on branded products. In the current economic downturn, some consumers are again "trading down" to cheaper private label brands.

In the long run, however, branded products will most likely remain popular and both Unilever and P&G are able to charge higher prices than generic store brands. This brand equity earns them substantially higher profit margins compared to retailers such as Walmart ( WMT ) and Costco ( COST ). Additionally, Unilever is investing in direct-to-consumer marketing channels that circumvent retailers. Examples of this DTC strategy are Unilever's own subscription services and websites for particular brands. While competition with private label products will remain a constant factor and consumers might trade down in the short-term during economic downturns, CPG companies will most likely do fine in the long-term. The fact of the matter is that large CPG companies have more market power than retailers and they possess a strong moat because their premium and branded products remain in high demand.

Financial results for Q3 FY2023

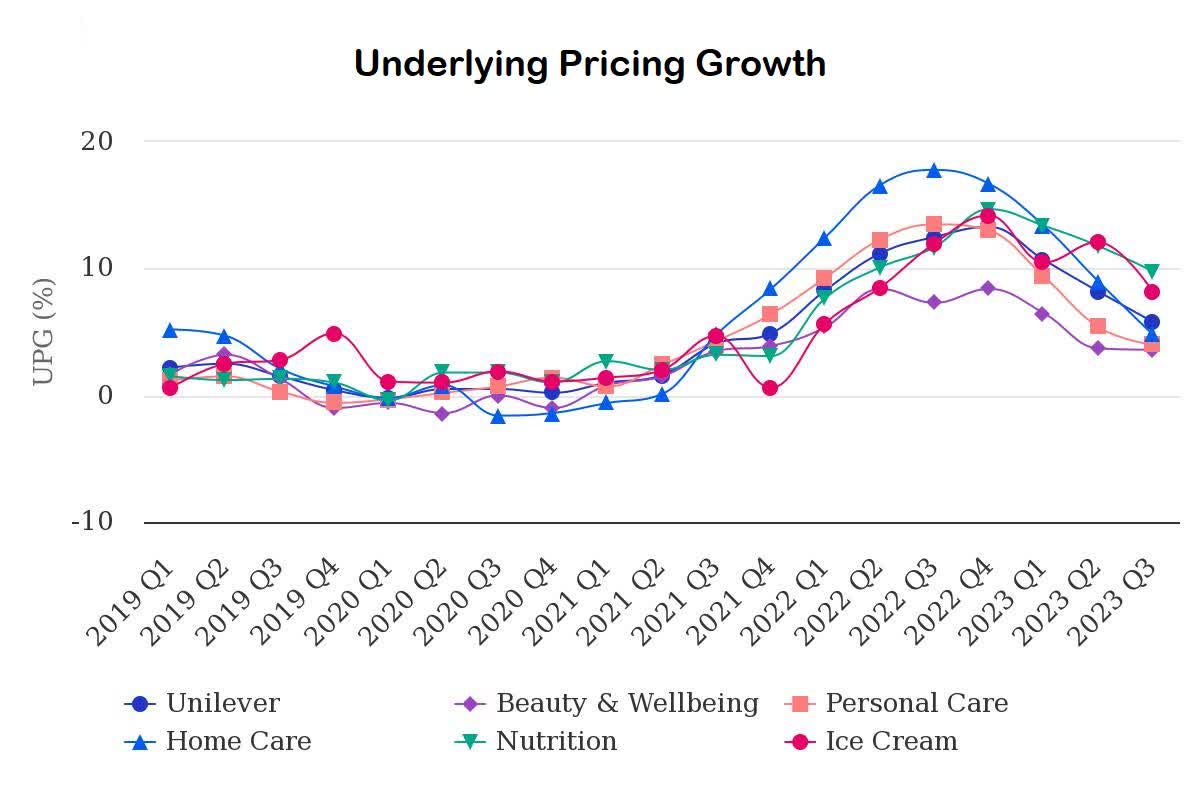

Unilever has raised its prices over the past year to deal with rising input costs. Compared to FY2021, Unilever's prices have increased about 20% on average. In FY2022 there was a big rise in pricing of about 13% and in FY2023 price growth has slowed down to about 5%. Consumers have taken these increases surprisingly well, volumes have decreased slightly (1-2%) but have remained on the same level pretty much for most segments. This shows that Unilever has a lot of pricing power because of its strong brands with low price-elasticities of demand.

{kind=link}

Pricing Growth (Unilever, Q3 2023)

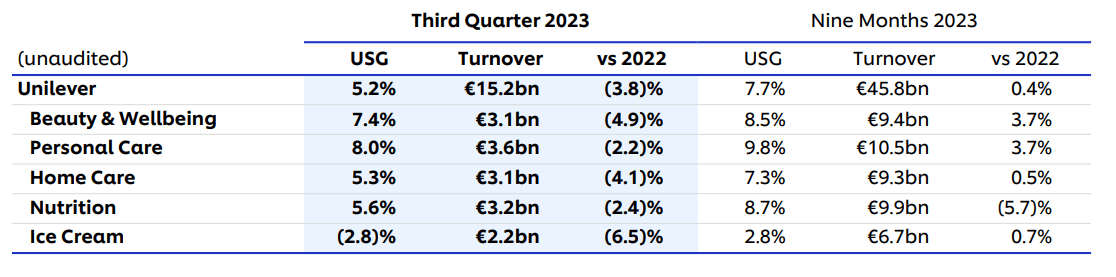

Q3 was a relatively bad quarter mostly due to currency headwinds (-8%) and poor performance of the ice cream segment, these were caused by some factors outside the management's control such as exchange rates and bad weather. People generally ate less ice cream depending on the weather, but this is not a long-term issue for the company. The currency headwinds impact their revenues more severely because they get ~60% of their revenue from emerging markets such as India. Compared to P&G, this is a key difference.

{kind=link}

Revenue per segment (Unilever, Q3 2023)

That being said, the company noted that some consumers are "trading down" to store owned brands to get more value-for-money deals. Especially in Europe, performance was bad with volumes decreasing by over 10%. This was compensated by 13% price growth for 1.7% USG, but this is not great long-term because there is an upper limit to price growth. In the long-term, Unilever needs to balance this by growing volumes as well as price. Overall, the company is doing fine long-term. They might have reached the limit of price growth for the ice cream segment, with consumer trading down to private label brands. Moreover, the recent surge in inflation and the energy crisis have stretched consumer's budgets more in Europe than in America.

Revenue per region (Unilever, Q3 2023)

Revenue per region (Unilever, Q3 2023)

Their strong presence in emerging markets is a strategic long-term advantage, albeit the cost of some currency headwinds from time to time. This year that was a big headwind of 8% to push Unilever's Q3 group level revenue in Euros down by 3% despite 5.8% UPG. Despite a small decrease in revenue because of these FX headwinds, Unilever raised the dividend yield approaching 4%.

Strong Strategic Position in Emerging Markets

While Unilever also has a strong position in developed markets such as Europe and the USA with some of the leading brands alongside P&G, they also have a strong focus on emerging markets that is a strategic bet and helps drive future growth. Recent quarters have shown double digit sales growth in Asia Pacific, Africa, and Latin America. Unilever now gets a lot of their sales from emerging markets while P&G is more focused on the USA. About 60% of Unilever's sales come from emerging markets such as India, Indonesia , and China , which have rapidly growing populations and an emerging middle class with more discretionary income. In the long term, this is a big advantage for Unilever.

Revenue per region (Unilever, Q3 2023)

Unilever reports its activities in India under a separately listed subsidiary company named Hindustan Unilever (HUL), but Unilever still owns over 60% of the shares. HUL has a very dominant position in India and it grows at over 8% per year benefiting from the development of one of the strongest emerging economies in the world. Similarly, its activities in Indonesia are also separately listed as PT Unilever Indonesia Tbk (ULI), with the parent company Unilever still owning 85% of the shares. Both of these companies and Unilever's activities in China have shown considerable growth due to the general economic development and population growth of these countries.

Especially India, which is now the most populous country in the world , provides a lot of potential for future growth. At time of writing, the current market valuation of this Indian subsidiary is 65.5 billion Euros, so Unilever's 60% stake in this business should be worth 40 billion Euros which is already over 30% of Unilever's total market cap at this time (115 billion).

Investing in Beauty and Wellbeing Trends

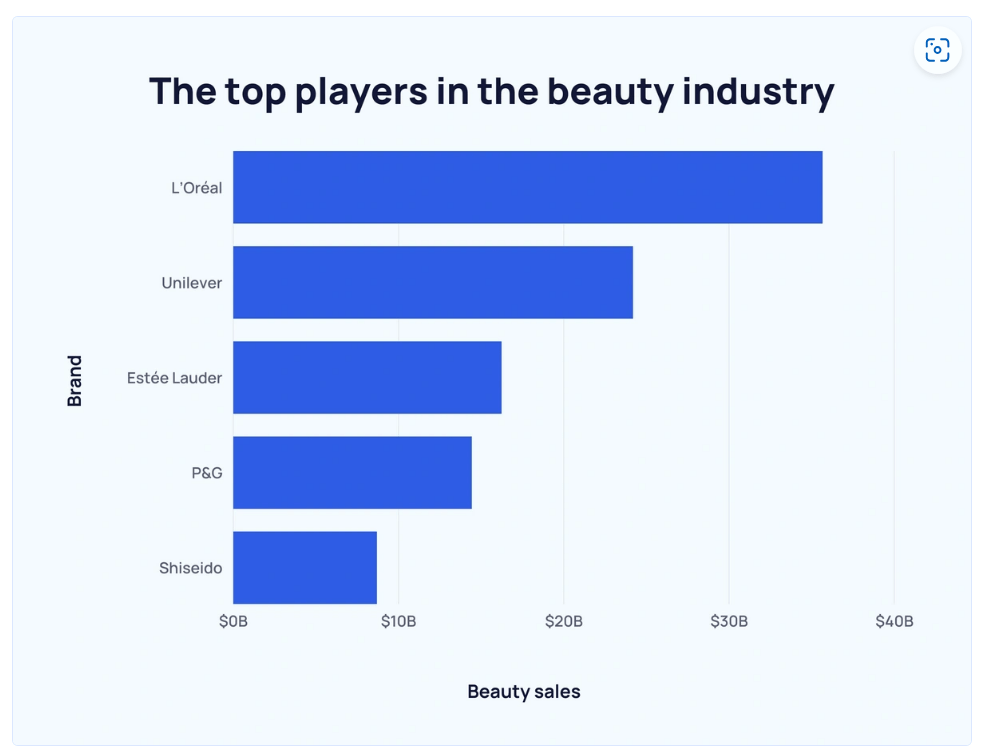

Next to emerging markets, they have invested heavily in the beauty and wellbeing segment which has shown good returns. This segment is very attractive because it has higher margins than the other segments. Unilever is now actually one of the biggest beauty players in the world by sales, even bigger than Estée Lauder ( EL ) who is a pure play in beauty products behind L'Oreal ( LRLCF ). Their " beauty and wellbeing " and " personal care " divisions includes brands like Dove, Sunsilk, Axe, Rexona, and Vaseline. Together, the beauty- and personal care segments now make up almost 50% of total group revenue. This segment also shows higher growth compared to other segments such as nutrition.

{kind=link}

Unilever is #2 largest beauty player in the world (Statista, 2023)

This strong performance is shown by growing revenues from these segments as shown below in volume- and price growth.

{kind=link}

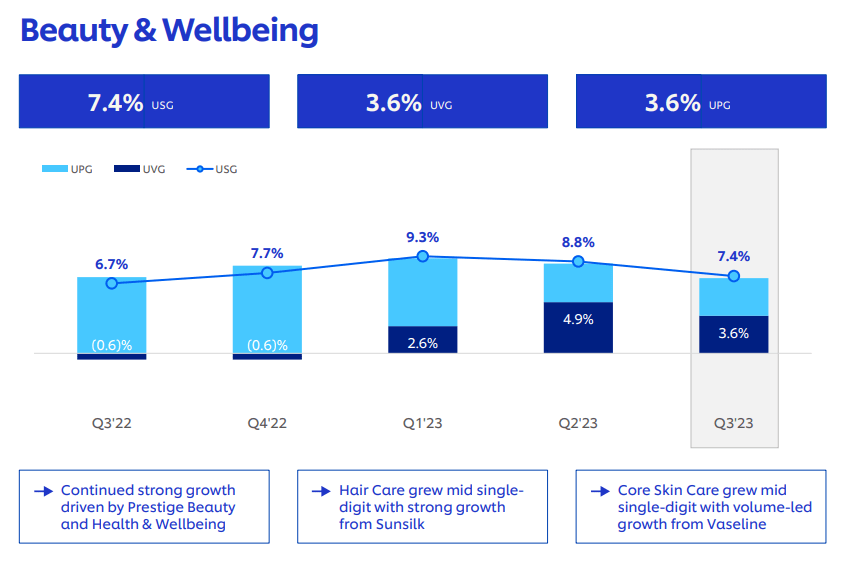

Beauty and Wellbeing segment is growing (Unilever Q3 2023)

This beauty & wellbeing segment is showing positive volume growth as well as positive price growth, growing at about 8% this year. Very nice growth.

{kind=link}

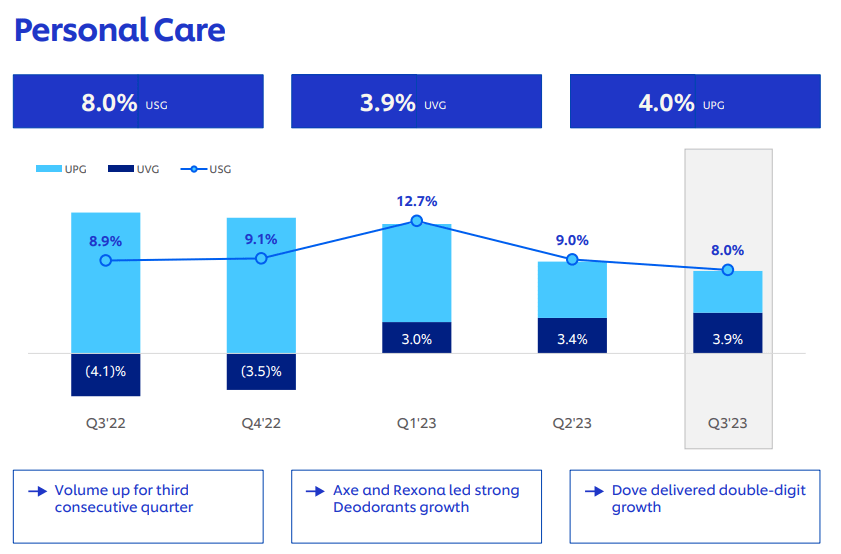

Personal care segment is growing (Unilever, Q3 2023)

Similarly, the personal care segment is also growing at 8%. Together these segments account for about 40% of the portfolio, but they could grow to 50% of the portfolio in the near future if they keep up this strong performance.

Innovation and Growth with Structural Trends

These beauty and wellbeing brands include supplements and "superfoods" such as Olly, whose products claim to improve things like sleep, mood, and sex drive. Unilever claims to have a competitive advantage for these products with their large R&D spending on biotechnology and so on. The health claims are not evaluated by the FDA, so that could be a risk factor. That being said, Unilever has over 20,000 patents to protect their innovations. Unilever's long-term investments in research and development, can lead to innovative products that can capture new market segments and meet consumer needs.

For example, their Liquid IV product leverages this R&D spend to claim product benefits and superior performance. These innovative products are supported by growing trends towards more sustainable and healthy food options. They also acquired the Vegetarian Butcher that offers meat replacements, which benefits from regulation and growing trends towards less traditional meat consumption. It seems like they have a strong position to benefit from these trends with their superior R&D and innovative product offerings supported by patents to defend their competitive edge in growing market segments.

Relatively Cheap Valuation

Putting it all together, Unilever shares look attractive and relatively cheap. Compared to its peer group with P&G ( PG ) and Nestlé ( NSRGY ), Unilever trades at a much lower market multiple as shown below. While P&G and Nestlé trade north of 20 times earnings, Unilever is substantially cheaper at less than 15 times earnings. This low valuation shows that analysts are quite negative about Unilever citing factors such as inflation and stretched consumer budgets even though P&G and Nestlé are exposed to much of the same challenges.

Given the large difference in valuation between Unilever and its peer group, I believe that there is an opportunity to beat low expectations and close this valuation gap. In my bull case, I am estimating a multiple expansion for Unilever. Considering the valuations in the peer group, a fair market multiple for Unilever should be closer to 20x P/E instead of 15x P/E where it sits now. This multiple expansion represents a significant 33% potential upside.

Using the high end of Unilever's outlook, namely 5% USG combined with a margin expansion, I think we could be approaching double-digit EPS growth with buybacks. When meeting these higher growth assumptions, you're getting a reasonable margin on safety on a world-class wide moat business that has diversified operations across the globe.

In a bear case with slower growth, you're getting it for around fair value with limited downside risk because it is a very stable company. Moreover, a growing dividend policy with a yield close to 4% provides additional income. Compared to its peer group competitors, Unilever trades at a relatively cheap valuation.

Conclusion

Our rating on Unilever shares is a " B uy ", because of the positive management change, the relatively cheap valuation, and the quality and size of Unilever's operations. I believe that Unilever can catch up to competitors, leveraging its strong existing position with good profitability. Unilever enjoys positive long-term tailwinds due to its strong presence in emerging markets as well as its strategically positioned portfolio of brands focused on health and wellbeing.

The risks for Unilever are relatively limited because it is a stable business that is not going anywhere anytime soon. The current valuation represents a fair price for a wonderful business with limited downside risk. The new CEO seems like a rational manager who is willing to make important changes and upset some people, which is good because the company needs to wake up.

For further details see:

Unilever: New CEO Making Changes