XHB - United Homes Group: Weak Performance Takes Away From Improving Outlook

2023-12-18 04:58:03 ET

Summary

- House builder United Homes Group has seen its stock fall by 31% since July as its performance stays weak.

- The Company's revenues have declined by 15.8% for the first nine months of 2023, with gross profits and operating margins also sliding.

- Despite weak performance, UHG continues to expand through acquisitions and has a stable balance sheet, but its market multiples suggest it could drop further.

Since I wrote about the US-based house builder United Homes Group ( UHG ) in July, it has fallen by 31%. This was expected considering its weakening financials in a slowing housing market at the time. However, its performance is in stark contrast with the homebuilders in general. The SPDR S&P Homebuilders ETF ( XHB ) has actually seen a 55% increase. This raises the question as to whether UHG is due an uptick as well.

{kind=link}

A look back

Before I get into the latest on UHG, a quick look back at where it was at when I last checked. The company's first quarter (Q1 2023) results were out then, which showed a 12.5% year-on-year (YoY) revenue decline and a softening in both gross and operating margins. Macro factors like high inflation, rising interest rates, and a potential slowdown in the US economy all contributed to a drag on housing demand.

The picture going forward, however, looked less daunting even though there were signs of future stress too, in the following ways:

- As of May 2023, new single-family sales were up by 20% YoY, which is significant for the company which specialises in the category. However, it remained to be seen whether the increase could continue. Goldman Sachs had predicted a 22% fall in new home sales in 2023.

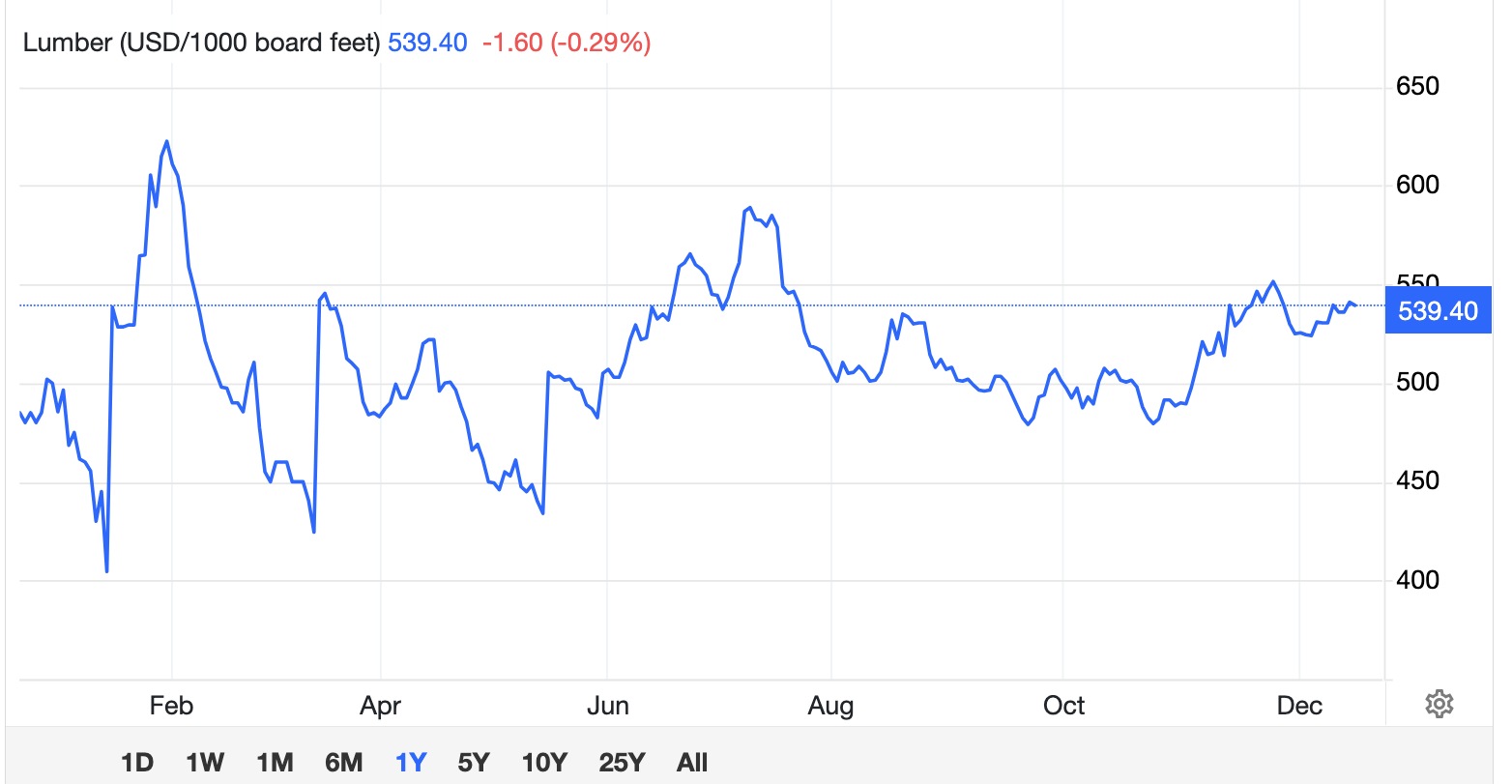

- Lumber futures had cooled significantly after spiking in 2022, which meant that the company's costs could be controlled and improve margins.

Recent performance

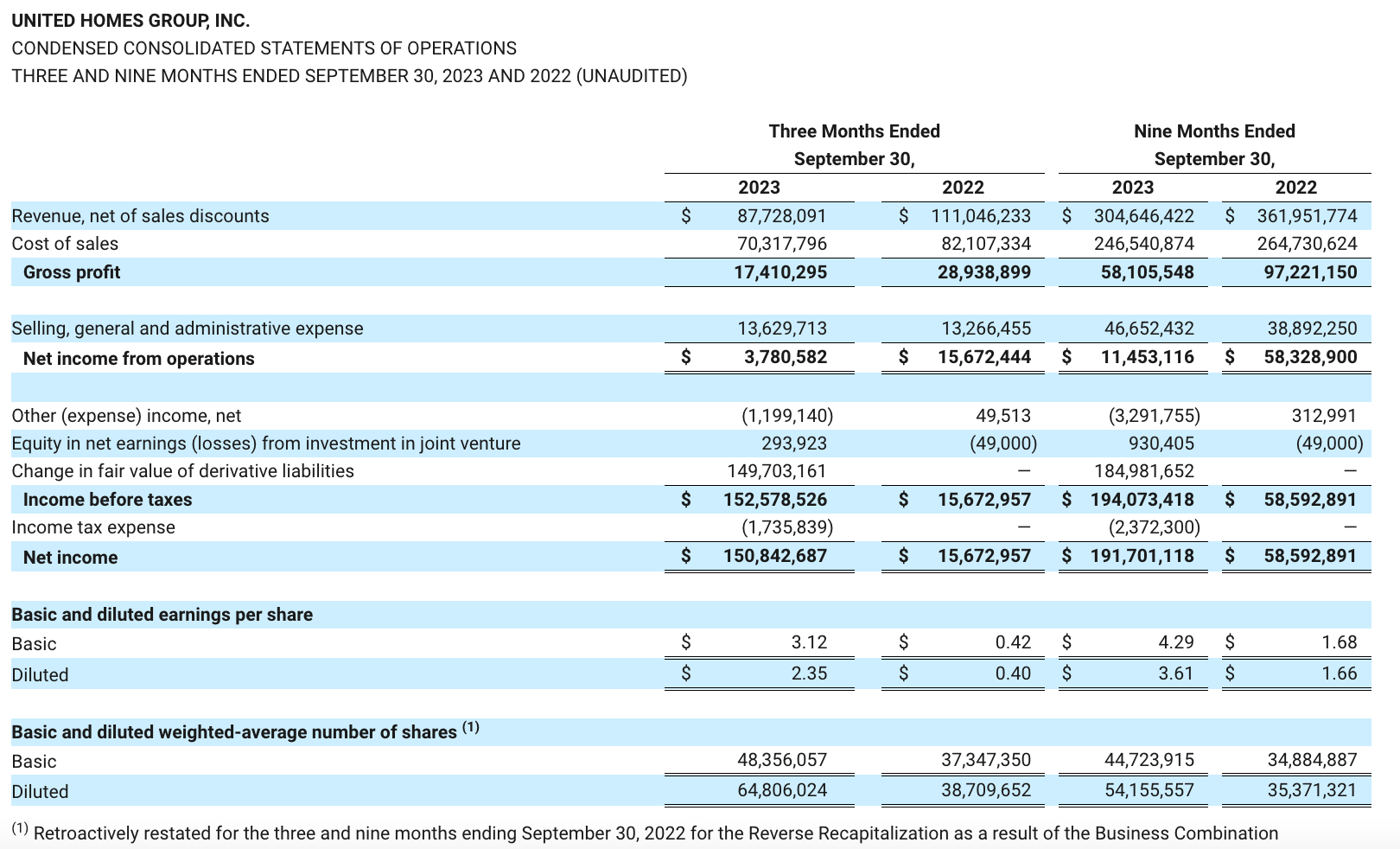

So far this year, though, the company's performance continues to be weak. For the first nine months of 2023 (9M 2023), its revenues have declined by 15.8% as both its home closings and new orders have contracted from 9M in 2022.

{kind=link}

While the cost of sales has declined too, it's by a much smaller 6.9% and gross profits continued to slide. The gross profit margin is now down too, to 19.1% (9M 2022: 26.9%), on account of sales incentives and the sale of inventory that was developed when lumber costs were higher, in a trend that continues from the first quarter. The operating margin also declined to a much smaller 3.8% (9M 2022: 16%) on fast-rising SG and A expenses.

Interestingly though, the net profit margin is up to 62.9% (9M 2022: 16.2%) as stock price measurement during the period changed the fair value of derivative liabilities. It is for exactly this reason that the company actually reported a net loss during Q1 2023. Instead of reflecting on the company's health, however, the basis of profit and loss at the net level indicates that it isn't a reliable indicator of the company's actual performance right now.

Expansion underway

The company continues to expand despite the current state of the market, however. In August, it acquired Herring Homes, which gives it entry into the North Carolina market, in addition to its existing portfolio in Georgia and South Carolina. The acquisition was made with a cash payout of USD 2.2 million.

It also acquired Rosewood Communities in October for USD 13 million in cash and also paid off USD 10 million of its liabilities. It's also expected to pay 25% of the EBITDA attributable to Rosewood's business up to the end of 2025. The acquisition further expands UHG's footprint in South Carolina.

The company's liquidity position however stays comfortable with a working capital ratio of 2.8x as per the September 2023. Also, considering there's no debt acquired in the process, its debt-to-assets ratio stays at an alright 51%.

Improved Outlook

The outlook however is improved from the last I checked. For one, while sequentially the single-family new home sales are slowing down , in October 2023 they are still up by 17.7% YoY, a far better performance than the decline expected by forecasters earlier in the year. It's worth noting that the trend in new home sales continues from the last I checked, which may well spill over into UHG's properties going forward.

With inflation coming off and an expected decline in mortgage rates next year as the Fed ends its rate hike cycle and potentially starts cutting rates in 2024, demand for homes can increase. In any case, the outlook for the housing market in general is healthy for next year, with the expectation of a small uptick in house prices.

Lumber prices too have stayed largely steady this year (see chart below), which should continue to bode well for its costs and margins.

{kind=link}

The market multiples

Despite a decline in UHG's share price over the past months, however, it is still highly valued compared to peers. I looked at its two other peers with a market capitalisation of under USD 1 billion and that is profitable. The first is Beazer Homes ( BZH ), which builds homes across US states, including the ones that UHG is present in. The second is Legacy Housing Corporation ( LEGH ), which provides manufactured homes as well as tiny and mobile homes.

Compared to UHG's trailing twelve months [TTM] EV/EBIT at 12.9x, BZH trades at 9x while LEGH is at 8x, indicating that on average UHG can drop another 25%. While UHG does trade favourably in terms of TTM P/S at 0.1x compared to 0.4x for BZH and 2.6 for LEGH, it's declining revenues indicate that the ratio does risk rising going forward.

What next?

There are arguments on both sides for UHG right now. Its performance undoubtedly continues to remain weak. While it has now reported a net profit after falling into a loss in Q1 2023, this is entirely due to a change in the fair value of derivative liabilities, which makes the metric an unreliable indicator of performance right now.

Nevertheless, it continues to expand with two acquisitions made in the past month, including one that increases its footprint across more states. Its balance sheet also looks stable despite the acquisitions. The improved outlook for both lumber prices and the housing market as such is encouraging too.

However, its key market multiple of EV/EBIT doesn't compare well with peers. At a time of weak performance, it's best to keep UHG on Hold until it shows signs of improvement. It is looking far more interesting as a potential investment than it was in July, though.

For further details see:

United Homes Group: Weak Performance Takes Away From Improving Outlook