USFD - United Natural Foods: An Unappetizing Downgrade

2023-09-27 14:15:53 ET

Summary

- United Natural Foods' shares plunged 27.4% after disappointing financial results and guidance for 2024.

- The company's revenue increased by 2% but profits fell significantly, leading to a net loss of $68 million.

- Management expects margin pressures to persist in 2024, with negative earnings per share and total profits.

- And yet, shares could offer investors with a bit of upside from this point.

Sept. 26 ended up being a very painful day for shareholders of the food distribution company United Natural Foods ( UNFI ). After management announced financial results for the final quarter of the company's 2023 fiscal year and gave guidance for 2024, shares plunged, closing down 27.4%. We did see a partial rebound as of midday on Sept. 27, with the stock up around 6% as of this writing. But that still puts it far below what it was just two days earlier. Looking into the data, it appears as though the financial position of the company is deteriorating rapidly because of a change in inflationary pressures. Next year should be particularly painful, though we have no idea what the year after that might look like. Based on the change in financial performance and management's own guidance, I have decided to downgrade the company from a 'strong buy' to a soft "buy" at this time.

The picture has looked better

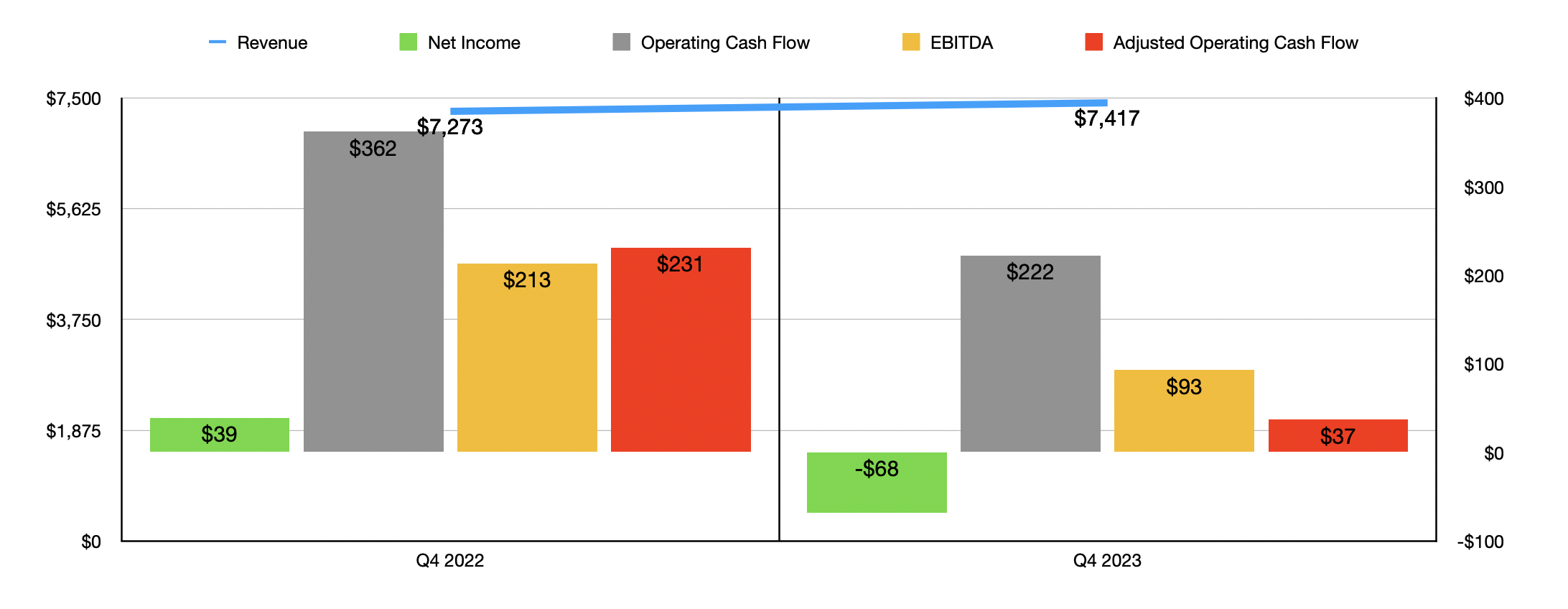

Before the market opened on Sept. 26, the management team at United Natural Foods announced financial results covering the final quarter of the company's 2023 fiscal year. On the top line, revenue came in at $7.42 billion. While this represents an increase of 2% over the $7.27 billion reported one year earlier, it fell short of analyst expectations to the tune of $51.5 million. A combination of inflationary pressures that the company was able to push on to its customers, and new business coming from the company selling new or expanded categories to existing customers and also adding new customers, was responsible for the year-over-year increase. This was, unfortunately, somewhat offset by a decline in the volume of goods that the company shipped.

{kind=link}

On the bottom line, the picture was far worse. The company actually reported a loss per share of $1.15. That's significantly lower than the $0.63 per share reported the same time last year. This brought total profits for the year down from $4.07 per share last year to $0.40 per share this year. In addition to falling significantly year over year, the earnings per share that the company reported came in at $0.18 per share lower than what analysts thought it would be . Put another way, the company went from generating a net profit of $39 million to generating a net loss of $68 million. Even though revenue for the enterprise rose, profits fell in large part because of a decline in the company's gross profit margin from 14.5% to 13%. Excluding a non-cash charge the same time last year, and a smaller one this year, the decline would have been from 15.2% to 13.5%. This drop, management said, was mostly driven by lower levels of procurement gains, higher shrinkage (which is largely associated with theft), and less of an ability for the company to push on inflationary pressures to its customers.

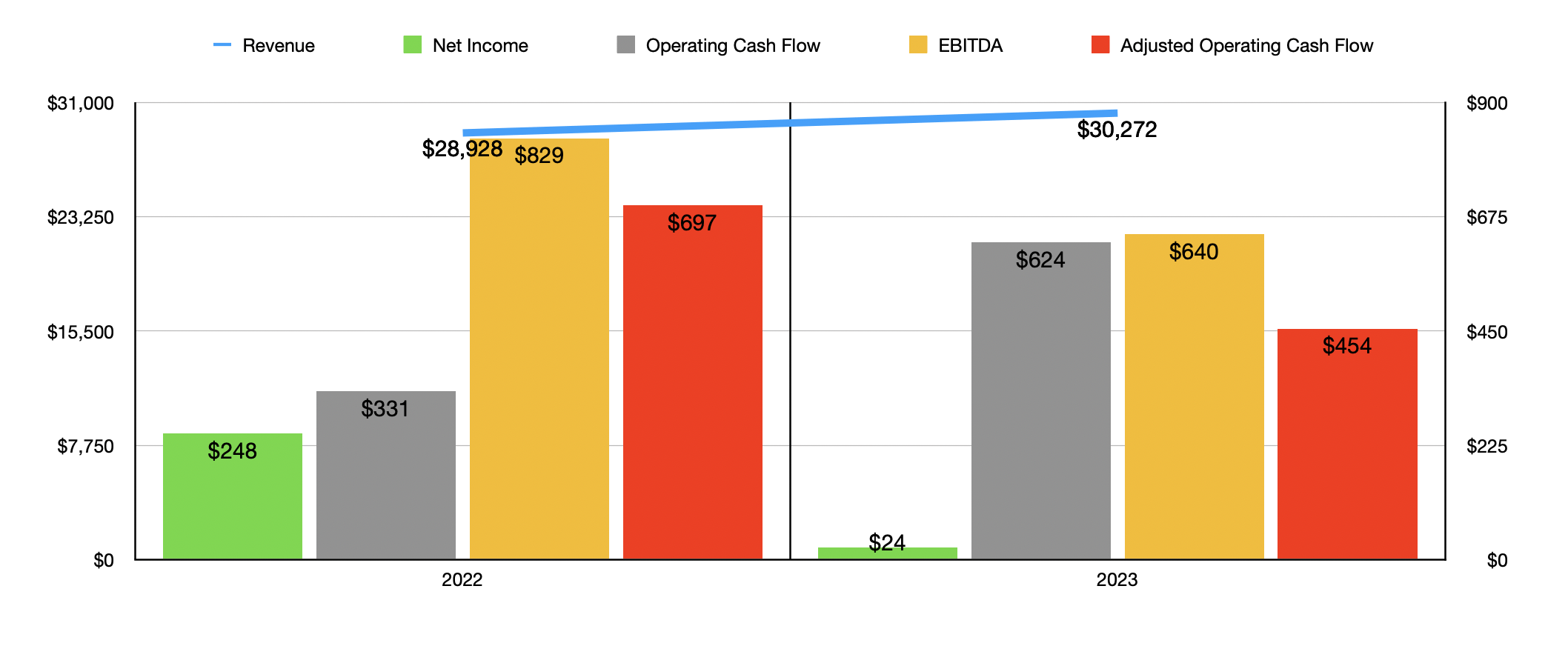

Other profitability metrics also took a hit. Operating cash flow, for starters, went from $362 million to $222 million. If we adjust for changes in working capital, the decline would have been worse, from $231 million to $37 million. Meanwhile, EBITDA for the business fell from $213 million to $93 million. In the chart below, you also can see results for 2023 in its entirety relative to 2022. When you look at the picture through that lens, you can see the final quarter of the year as being a microcosm of the year as a whole. Revenue increased, but profits and cash flows both fell compared to the same time last year. The one exception was operating cash flow. But on an adjusted basis, which is the most important variant of the two, it managed to still decline.

{kind=link}

Frankly, I found some of the results reported by management to be rather surprising. After all, inflation still has not vanished. The most recent data provided by the USDA estimated that, in August of this year, prices were 3% higher than they were the same time last year. Although some food categories reported year-over-year declines, most reported increases. The retail egg category posted the largest drop, with prices down 18.2% year over year and down 38%, compared to January 2023. Fresh fruits were down 0.4% compared to August last year, while fresh vegetables were down 0.1%.

Driven in part by continued inflation, management expects revenue next year to come in at between $30.9 billion and $31.5 billion. This compares to the $31 billion that analysts had forecasted. This on its own is not awful. However, they expect margin pressures to persist, with a forecast for earnings per share of between negative $0.38 and negative $0.88. That compares to the $2.28 per share that analysts were expecting. Total profits should come in negative to between $36 million and $110 million, with adjusted profits ranging between negative $52 million and positive $22 million. The only other profitability estimate provided by management involved EBITDA. The forecast for it is between $450 million and $550 million. If we use the midpoint for that guidance and look at the other revenue and cost items forecasted by management, we would expect operating cash flow of around $313 million on an adjusted basis.

{kind=link}

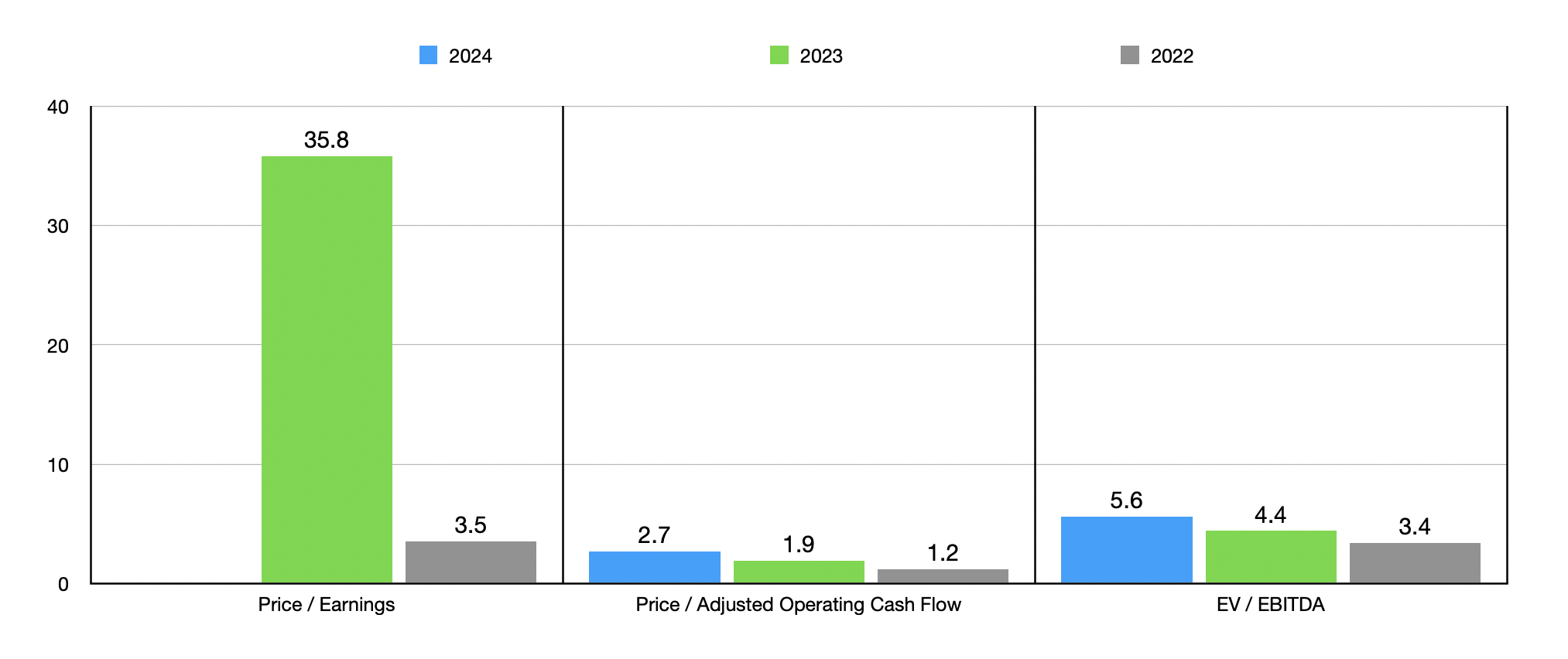

Using these figures, we can appropriately value the company. As you can see in the chart above, we can't value it on a price to earnings basis for 2024. But we can when it comes to the other profitability metrics. Relative to both 2022 and 2023, shares of the enterprise do look more expensive. But when it comes to cash flow, the stock looks very cheap. In the table below, I also compared it to five similar firms. But those also are trading at fairly cheap levels. The price to operating cash flow multiple of United Natural Foods makes it cheaper than all of the five competitors that I compared it to, with the exception of one. And the EV to EBITDA multiple makes it the cheapest. So while the other companies might be cheap, they don't hold a candle to our target.

| Company |

| Price/Operating Cash Flow |

| EV/EBITDA |

| United Natural Foods |

| 2.7 |

| 5.6 |

| Andersons ( ANDE ) |

| 1.4 |

| 8.6 |

| Performance Food Group Co. ( PFGC ) |

| 11.1 |

| 10.1 |

| SpartanNash Co. ( SPTN ) |

| 5.9 |

| 6.8 |

| US Foods Holding Corp. ( USFD ) |

| 8.4 |

| 10.9 |

| Sysco ( SYY ) |

| 11.7 |

| 11.7 |

Naturally, when fundamental performance starts to deteriorate like this, something that I start thinking about is the broader health of the enterprise. As of this writing, United Natural Foods has a market capitalization of $859 million but has net debt of $1.95 billion. That's quite a large amount of debt in the grand scheme of things. There's both good news and bad news associated with this. The good news is that debt was once considerably higher. If we look at financial performance for 2019 , which was the final year that we saw before the COVID-19 pandemic ravaged the planet, the company had a net debt of $2.61 billion. At that time, the adjusted operating cash flow of the enterprise was $265 million, while EBITDA totaled $562.9 million. These numbers are not terribly different from the forecasted figures for 2024. So by definition, United Natural Foods is still healthier on a forward basis than it was before the pandemic.

The bad news is that this could mean limited upside for shareholders. This time in 2019, United Natural Foods had a market capitalization of about $616 million. Its enterprise value totaled $3.22 billion. When we apply the figures for that year, the company was trading at a price to adjusted operating cash flow multiple of 2.3, and it was trading at an EV to EBITDA multiple of 5.7. Those numbers are very close to the 2.7 and 5.6, respectively. The enterprise is trading at on a forward basis now. To be fair, in the 12 months after that time, shares spiked 32.4%. So it's not unthinkable that we could see further upside because of how cheap the stock is. However, unless we return to the kind of performance seen in the past few years, which would be unlikely, an extremely bullish outlook for the company is unrealistic.

Takeaway

Naturally, I'm rather disappointed in United Natural Foods and its performance. The final quarter of 2023 was problematic and the outlook for 2024 is objectively negative. But based on all the data I'm looking at now, the worst case seems to be that shares are more or less fairly valued. But when you look at the valuation of the company compared to similar enterprises, and you look at how its financial condition has changed since 2019, I think it tilts more in the bullish direction, leading me to keep the firm rated a soft "buy" for now.

For further details see:

United Natural Foods: An Unappetizing Downgrade