IS - Unity: More Discounts Coming - Monetization Is On The Horizon

Summary

- We expect to see a successful match between Unity and ironSource ahead, once voting closes by early October.

- We are of the opinion that Unity needs the adtech's help for a successful monetization in the Metaverse, given the former's continuous cash burn thus far.

- Several Big Tech giants like Amazon, Alphabet, and Meta report billions in advertising revenue annually, making it a highly profitable industry.

- However, we do not see many catalysts ahead for U's stock recovery, given its cash burn, share dilution, and worsening macroeconomics.

- The low $30s will be here again for the Metaverse fans. Patience for now.

Investment Thesis

Unity Software Inc. ( NYSE: U ) continues to be a speculative play in the Metaverse, given its massive potential in the worsening macroeconomics scene. The stock performance also reflects Mr. Market's uncertainty, with a -51.6% plunge in price since our previous article. Combined with its penchant for share dilutive acquisitions and cash burn thus far, it is unlikely that we will see a meaningful stock recovery for U ahead.

Therefore, investors should take a good look at their portfolios before adding more Unity at this current level, given the potential downside and slower monetization of the Metaverse. Even Meta ( META ) has trouble explaining its billion-dollar losses in Reality Labs .

U Continues To Grow Aggressively At A Break Neck Pace

{kind=link}

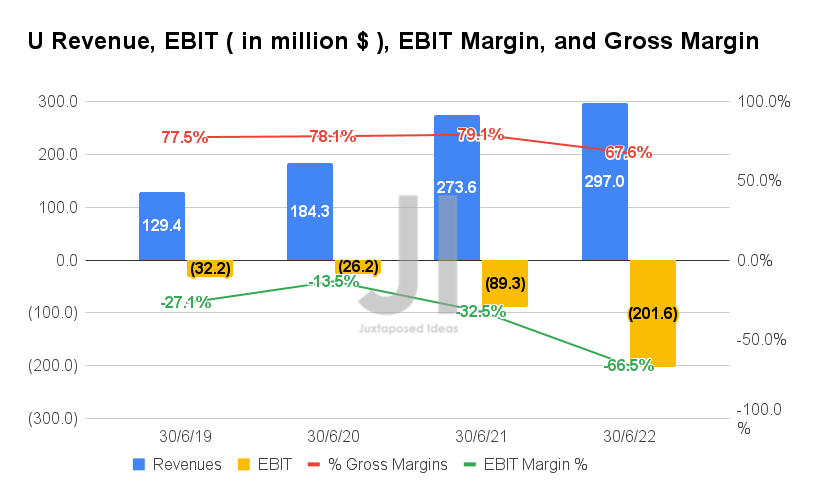

In FQ2'22, U reported revenues of $297M and gross margins of 67.6%, representing a minimal increase of 8.5%, though a decline of -11.5 percentage points YoY, respectively, attributed to rising costs and QoQ fall in revenues. This has directly impacted its profitability, with an EBIT of -$201.6M and an EBIT margin of -66.5% in the latest quarter. It represented a drastic decline of -225.7% and -34 percentage points YoY, respectively.

{kind=link}

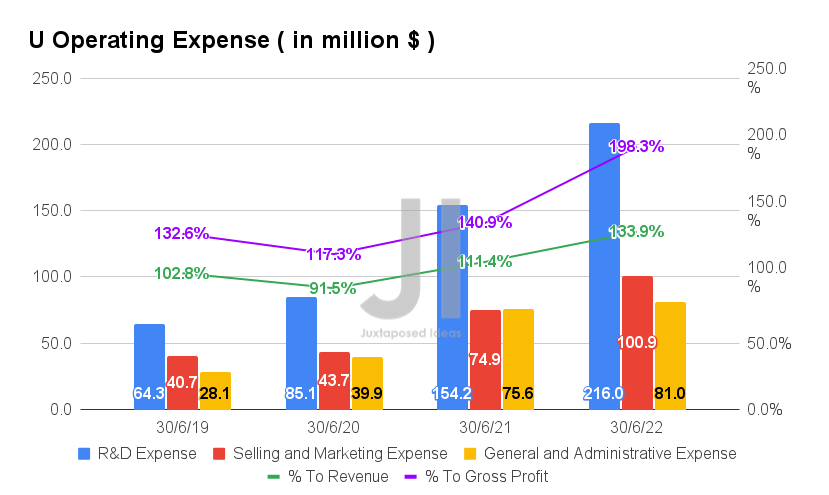

By FQ2'22, U reported massively elevated operating expenses of $397.9M, representing an increase of 30.5% YoY and 298.9% from FQ2'19 levels. Given the odd balance in its exponentially growing R&D expenses accounting for 72.7% of its revenues in FQ2'22 and 56.3% in FQ2'21, we can surmise that the company is at a growth-at-all-costs stage, with aggressive investments across the broad. Assuming smashing success in its investments, we may see a potential top and bottom line growth over the next few years.

In the meantime, this strategy has led to the unsustainable growth in U's ratio of operating expenses to its slowing sales, at 133.9% of its revenues and 198.3% of its gross margins in FQ2'22. It indicated a massive increase from FQ2'21 levels of 111.4% and 140.9%, respectively. Thereby, highlighting the reason for the company's deepening losses at the moment.

{kind=link}

Fortunately, U still maintained its previous 2026 Notes of $1.7B since November 2021, without the need to add on to its long-term debts by FQ2'22. With stable net PPE assets of $205.1M and capital expenditure of $15.4M by the latest quarter, indicating relatively in line over the past three years, the management appears to be highly prudent about its debt leveraging during a time of elevated interest rates.

{kind=link}

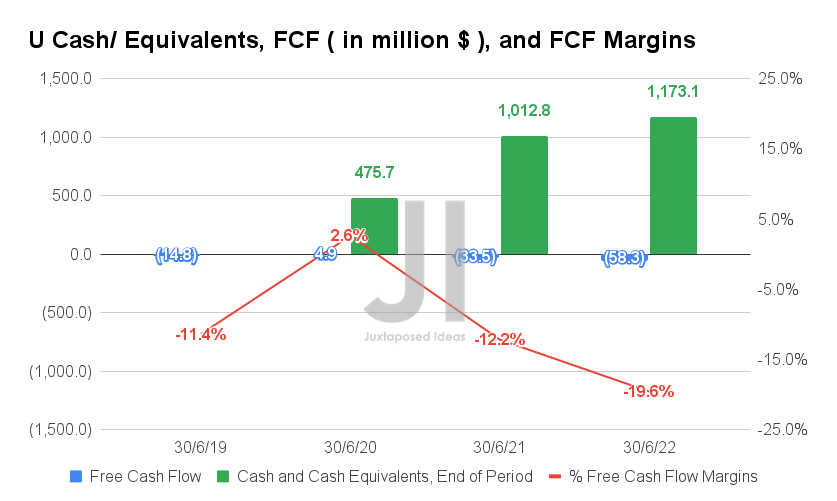

Given the lowered profitability and sustained capital expenditures thus far, we are not surprised that U continues to report negative Free Cash Flow (FCF) generation at -$58.3M and an FCF of -19.6% in FQ2'22. This represents a tremendous decline of -74% and -7.4 percentage points YoY, respectively. However, the company still reports a more than decent $1.17B of cash and equivalents by the latest quarter, solidifying its balance sheet for the next few quarters.

{kind=link}

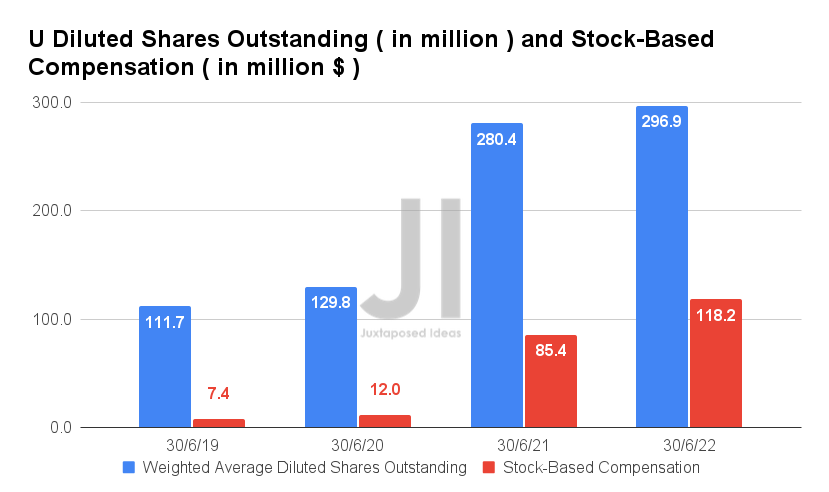

Nonetheless, it is also evident that U relied heavily on Stock-Based Compensation (SBC), with $118.2M of expenses reported in FQ2'22, representing an increase of 14.3% QoQ and 38.4% YoY. Assuming a similarly elevated rate ahead, we may expect to see the company report up to $511.36M of SBC expenses in FY2022. It will represent a massive increase of 47.2% YoY, further contributing to U's share dilution ahead.

Assuming that the ironSource ( NYSE: IS ) acquisition goes through, we may expect to see another share dilution of 37.2% from the current share counts to 407.59M upon closing. Therefore, speculatively, representing a continuous dilution of 49.8% since its IPO in September 2020. Alarming indeed.

By FQ2'22, U already reported 296.9M of diluted shares outstanding, representing an increase of 5.8% YoY. Though partly attributed to its recent acquisition of Weta Digital, investors must also take note that the company is not expected to report significant profitability over the next three years. Thereby, highlighting the company's further reliance on stock-based acquisitions ahead, despite the $2.5B share repurchase authorization since the latter is contingent upon exercise.

{kind=link}

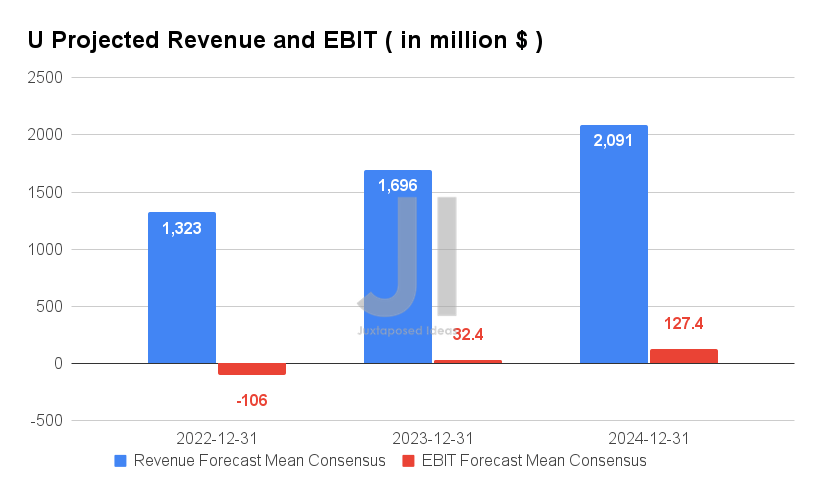

Over the next three years, U is expected to report revenue growth at a CAGR of 23.5% while speculatively reporting EBIT profitability from FY2023 onwards. However, it is impressive that the company is expected to close the gap in its EBIT margins by H2'22, given the projected improvement from -27.1% in FY2019 to -42.1% in FY2021, and finally to -8% by the end of FY2022. We shall see, since U remains rather unprofitable with an EBIT of -$373.18M and an EBIT margin of -60.4% in H1'22.

For FY2022, analysts are projecting that U will report revenues of $1.32B and an EBIT of -$106M, representing tremendous YoY growth of 18.9% and 80%, respectively. However, it is also apparent that these numbers represent a notable downgrade by -11.3% in revenue estimates since our previous analysis in March 2022. Thereby, pointing to a weaker and more realistic market demand after the Metaverse hype has died down, given the worsening macroeconomics.

In the meantime, we encourage you to read our previous article on U, which would help you better understand its position and market opportunities.

- Unity Software: Speculative Buy At 60% Discount

So, Is U Stock A Buy , Sell, Or Hold?

U 2Y EV/Revenue and P/E Valuations

{kind=link}

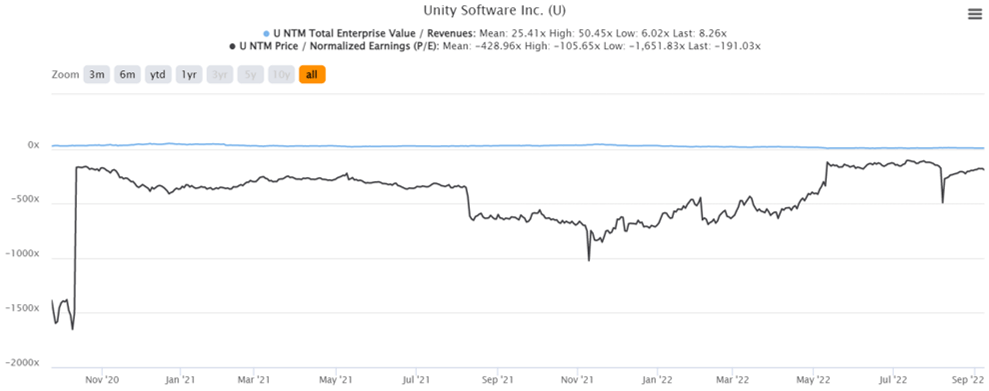

U is currently trading at an EV/NTM Revenue of 8.26x and NTM P/E of -191.03x, lower than its 2Y EV/Revenue mean of 25.41x, though massively improved from its 2Y P/E mean of -428.96x. The stock is also trading at $41.30, down -80.3% from its 52-week high of $210, though at a premium of 41.9% from its 52-week low of $29.09.

U 2Y Stock Price

{kind=link}

Consensus estimates remain bullish about U's prospects, given their price target of $63.25 and a 53.15% upside from current prices. Those that have missed the recent bottom at the $30s may still jump back in at the next dip, given the company's long-term potential and growth trajectory in the Metaverse. However, we would also like to remind investors to size their portfolios accordingly, given the potential volatility ahead from the upcoming shareholder voting and the Fed's upcoming hike in interest rates through 2023.

In the meantime, it would be prudent to observe the stock a little longer, since U is unlikely to take off over the next few quarters, prior to improvements in its profitability.

For further details see:

Unity: More Discounts Coming - Monetization Is On The Horizon