UHS - Universal Health: Retain Buy As Systematic Defensive Overlay

Summary

- Universal Health Services continues to present as an attractive name as part of a systematic defensive overlay for equity portfolios.

- Despite a tight year in post-tax earnings, UHS still represents value by estimation.

- On FY22E earnings, we estimate it fairly valued at 16x P/E.

- Net-net, reiterate buy.

Investment Summary

Since our last publication on Universal Health Services, Inc. (UHS), where we rated the stock a buy, shares have clipped another 35% to the upside to the time of writing. The stock continues to present as a defensive holding for equity investors and here I'll run through additional factors for consideration in demonstrating why we continue to be rate UHS as a long-term buy to smooth portfolio returns in strategic equity allocations. Net-net, UHS is still fairly priced, and we rate it a buy at ~16x forward earnings. I also encourage you to read our previous UHS publication:

Exhibit 1. UHS recaptured most of the FY21-22 leg down, testing previous highs

{kind=link}

UHS continues compounding value for equity holders

Here I'll take a long-term approach in exhibiting why UHS remains in contention as a defensive overlay to achieve convexity in equity portfolios. As a reminder, convexity, although usually a fixed income measure, when applied in the equity sense, refers to a portfolio strategy [either long only, long/short, or beta neutral] that is expected to perform best at the extremes of market performance - both in rallying and bear markets - but with a bias for downside protection. Convexity should be systematic and research from the Man Group shows long-term outperformance for convex portfolios with risk-reducing overlays.

For those observing Exhibit 2, you'll note that inflows have been distributed with an upside bias over the past 6-years to date. Moreover, periods of outflows have been reversed swiftly with subsequent price rallies over this time. Hence, we look to the most recent period of inflows in a positive light, and believe this is fundamentally based, as discussed below.

Exhibit 2. Equity inflows have been biased to the upside last 6-years

{kind=link}

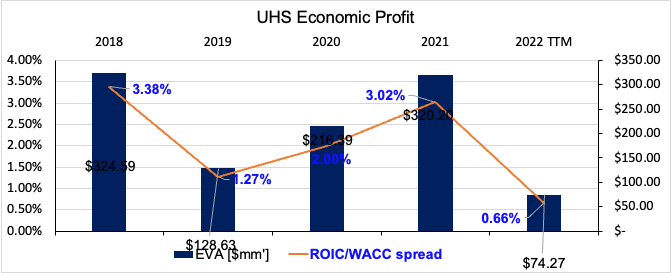

A firm creates value for its shareholders when it generates a high return on invested capital ("ROIC") above the cost of capital. This looks beyond the accounting reality and focuses on an economic one. As such, a positive ROIC above the hurdle rate represents an economic profit ("EP"). It's a meaningful exercise to examine this for UHS over the last decade to extrapolate its propensity to deliver down the line. We'll do this to the TTM [Q3 FY22']. Over the FY18-TTM period, UHS has maintained a healthy EP, although this has narrowed in substantially as the broad market's cost of capital has shifted higher in 2022'.

Exhibit 3. UHS maintained positive EP despite tightening up over the TTM

{kind=link}

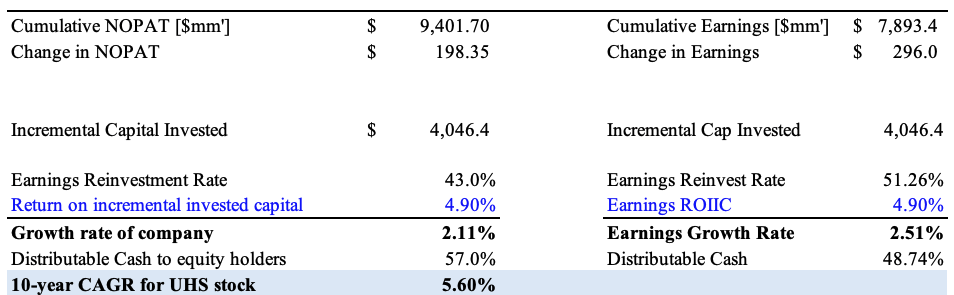

Delving further into this, it's worth pointing out that since FY12', UHS has generated a cumulative $9.4Bn in net operating profit after tax ("NOPAT"), representing an additional growth of $198mm in NOPAT over the last decade [Exhibit 4]. In order to achieve this, it required the investment of an additional $4Bn in capital.

Exhibit 4. UHS NOPAT, Invested Capital, progression 2012-TTM

Data: Author, using data from UHS SEC Filings

Consequently, the return on incremental invested capital ("ROIIC") over this time is ~5%, leading to a NOPAT and earnings growth rate of 2.1% and 2.5%, respectively [Exhibit 5]. Noteworthy, when winding back to FY21', the ROIIC was 11.7% and the growth rate was 5% - in-line with the company's 10-year CAGR stock price of 5.6% [reinvestment rate remains unchanged]. Hence, it increased capital investment by 54% to grow NOPAT by 32% to the TTM.

In view of this, the company has maintained its distribution of earnings to shareholders at ~50-57%, including its dividend that's increased at CAGR 15% since FY18'.

Exhibit 5. UHS long-term ROIIC at ~5%, was 11.7% at FY21' before broad market and economic turbulence

{kind=link}

Valuation and conclusion

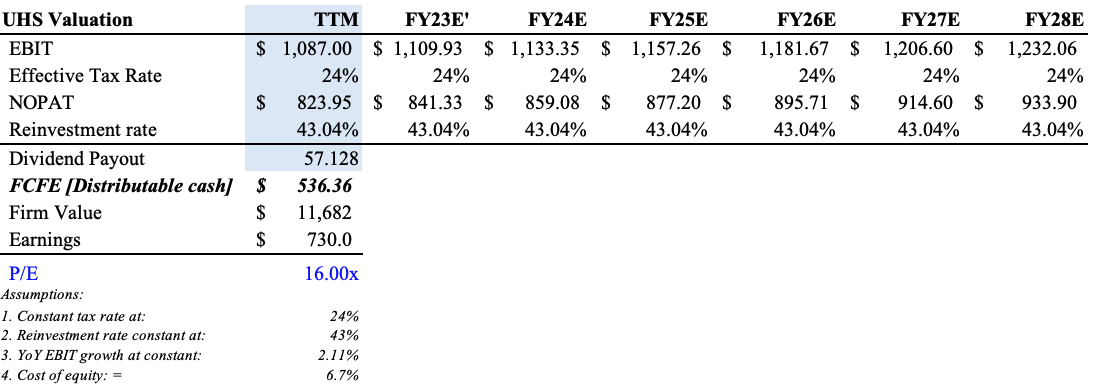

UHS currently trades at 15x earnings both on a GAAP and non-GAAP basis. It also looks attractively priced at 1.8x its book value of equity. Given the company's relatively stable, predictable cash flows, we believe it is reasonable to presume it can continue its growth rates described above, at the corresponding earnings reinvestment rate. Consensus also forecasts ~$730mm in earnings for FY22E', a figure we are aligned with. Hence, discounting the estimated free cash flows to equity ("FCFE") at the cost of equity, that Roberts (1991) describe we can obtain from the growth rate and earnings yield, and factoring in UHS' dividend, we see the stock fairly valued at 16x forward earnings.

Exhibit 6. UHS Estimated fair P/E at 16x

{kind=link}

Net-net, we continue to rate UHS a long-term buy for reasons stipulated in this note. We'd look for the company to re-rate to 16x P/E as an estimate of fair value, with further revisions with earnings growth down the line.

For further details see:

Universal Health: Retain Buy As Systematic Defensive Overlay