IGIC - Universal Insurance Holdings: Still Undervalued After The YTD Rise Of 62%

2023-11-21 04:02:08 ET

Summary

- Universal Insurance Holdings is a U.S.-based insurance holding company with a $480-million market cap, specializing in personal residential insurance, covering homeowners, renters, condo unit owners, and dwelling/fire.

- Margins showed significant improvement, with the GAAP operating loss margin at 1.7% compared to 29.3% in the prior year.

- The company saw a substantial turnaround in net income and adjusted net income, driven by improved underwriting income and net investment income.

- I see an upside potential of ~22.2% in UVE stock, not to mention its generous dividend yield of ~3.86%.

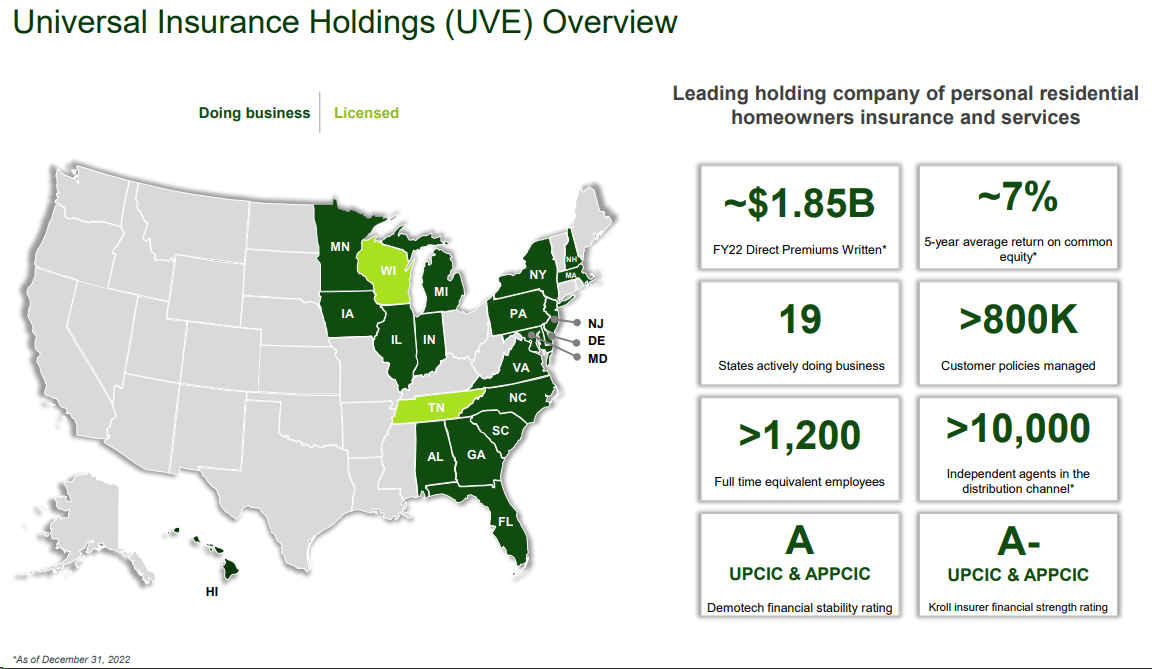

The Company

Universal Insurance Holdings ( UVE ) is a $480-million market cap U.S.-based integrated insurance holding company that focuses on personal residential insurance, including homeowners, renters, condo unit owners, and dwelling/fire coverage. The company offers additional coverages such as allied lines, personal property, liability, and personal articles. It provides various services, including advising on actuarial issues, claims administration, policy underwriting, and reinsurance management. Universal Insurance Holdings distributes its products through independent agents and online solutions, including its digital agency, Clovered.com.

{kind=link}

Source: Q3 FY2023 IR presentation

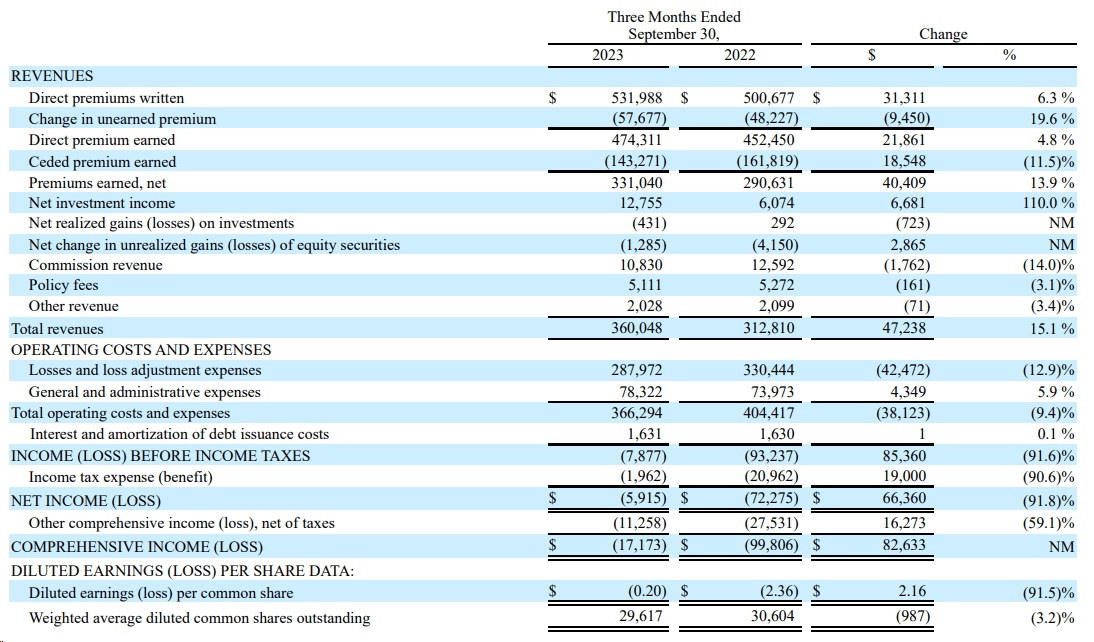

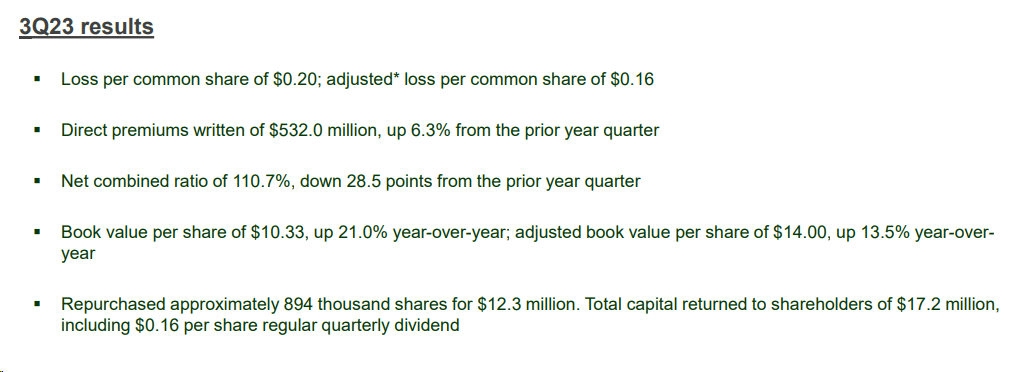

In Q3 FY2023 , Universal Insurance Holdings generated $360.0 million in total revenues, marking a notable 15.1% YoY increase. Core revenue, driven by higher net premiums earned and increased net investment income, stood at $361.8 million, marking a 14.2% rise. Direct premiums written climbed to $532.0 million, propelled by growth in Florida (+4.4%) and other states (+14.7%) due to rate increases, partially offset by a decline in policies in force.

{kind=link}

The ceded premium ratio decreased to 30.2%, reflecting improved efficiencies in the reinsurance program and growth in direct premiums earned, offset by higher reinsurance pricing and costs tied to increased home values. Net premiums earned saw a substantial 13.9% increase to $331.0 million, driven by higher direct premiums earned and a lower ceded premium ratio. Net investment income surged to $12.8 million, up from $6.1 million, supported by higher fixed-income reinvestment yields and cash yields.

Margins showed significant improvement, with the GAAP operating loss margin at 1.7%, compared to 29.3% in the prior year. The adjusted operating loss margin improved to 1.3% from 27.7%, mainly attributed to a lower net combined ratio and increased net investment income. In terms of net income and adjusted net income, there was a substantial turnaround. Net loss available to common stockholders improved significantly to $5.9 million, compared to a loss of $72.3 million in the prior year quarter. Adjusted net loss available to common stockholders also showed improvement, reaching $4.6 million, compared to a loss of $69.4 million in the prior year quarter. This positive shift was largely driven by improved underwriting income and net investment income.

{kind=link}

Notably, the net loss ratio dropped to 87.0%, down 26.7 points, reflecting a lower current accident year net loss ratio, primarily stemming from reduced weather-related losses. The net expense ratio decreased to 23.7%, down 1.8 points, primarily due to lower renewal commission rates paid to distribution partners. Overall, the net combined ratio decreased to 110.7%, down 28.5 points, showcasing lower net loss and expense ratios.

In capital deployment, the company repurchased approximately 894 thousand shares during Q3 at an aggregate cost of $12.3 million, leaving $7.8 million in share repurchase authorization.

{kind=link}

Recently, UVE declared a quarterly cash dividend of $0.16/share, payable on December 15 to shareholders of record as of December 8, with an ex-dividend date of December 7 for new shareholders to be ineligible for the upcoming dividend.

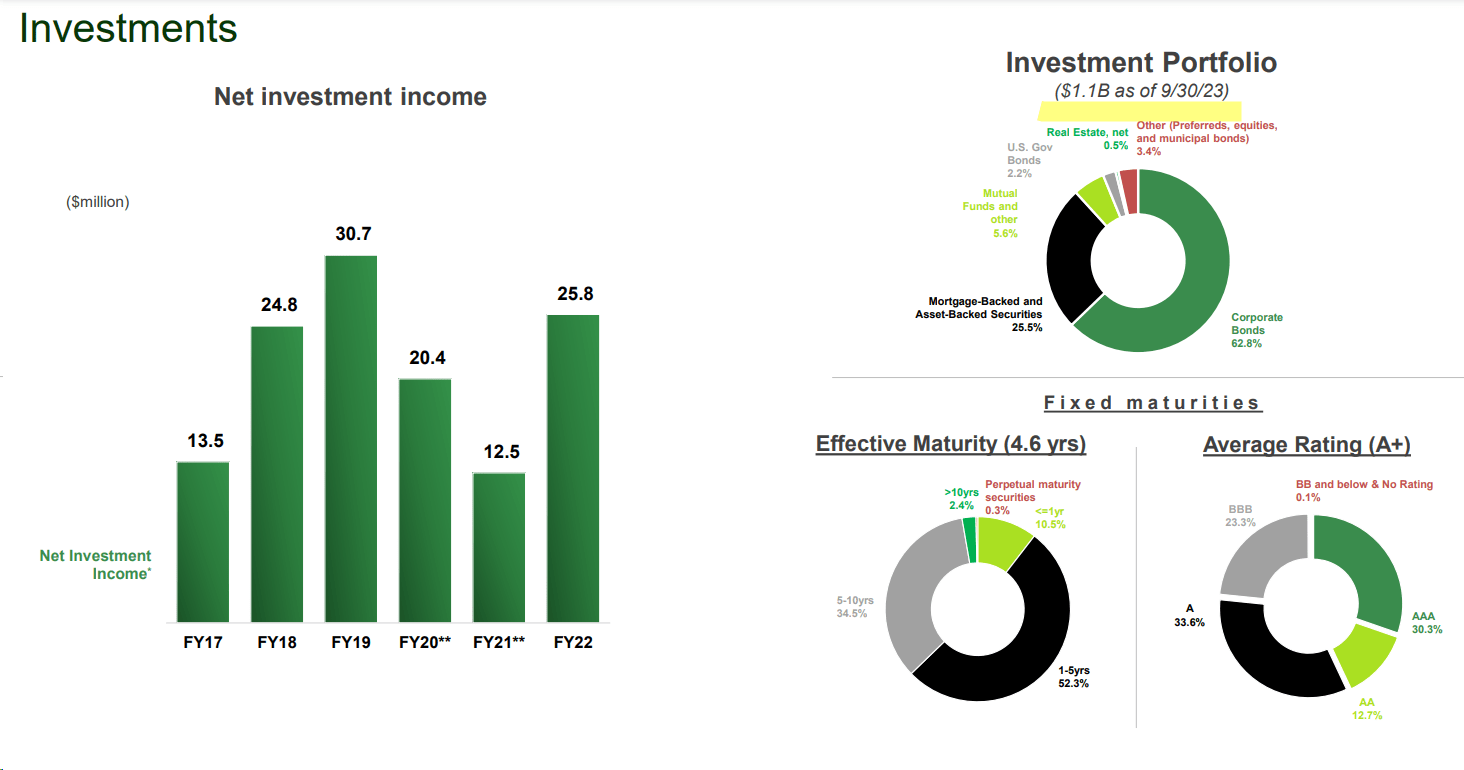

In my opinion, UVE's investment portfolio looks more than solid with a 62.8% allocation to corporate bonds with an effective maturity of ~4.6 years and an average credit rating of 'A+'.

{kind=link}

In recent years, UVE has fallen sharply in price, fundamentally following its tangible book value:

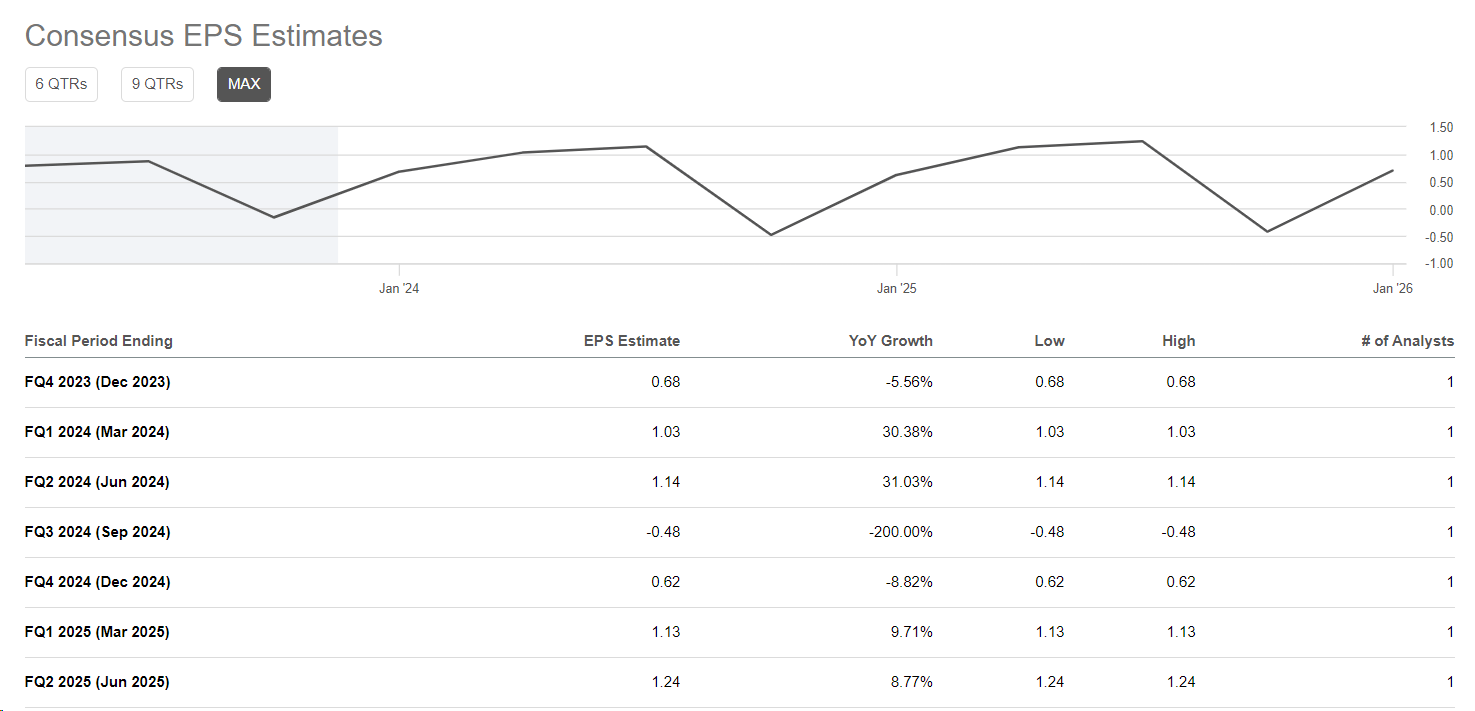

However, it is encouraging that UVE is very quickly leaving its unprofitable period: The company is rapidly reducing its losses and, according to 1 analyst's forecasts , will report positive EPS in the next quarter:

{kind=link}

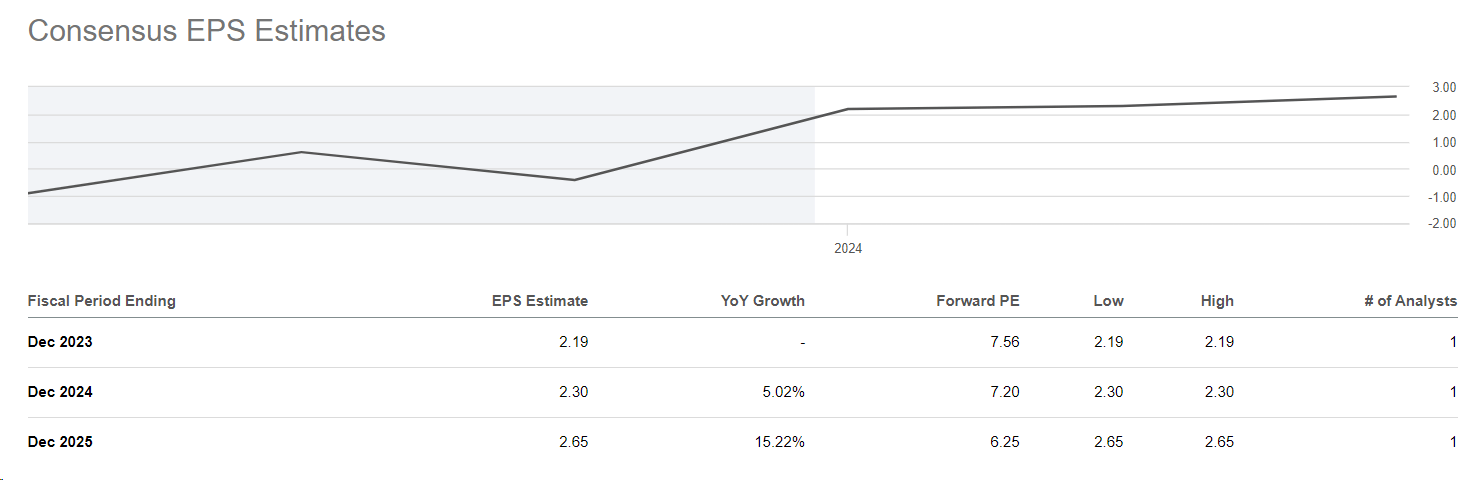

In the longer term, this recovery should continue:

{kind=link}

I believe that UVE's earnings per share will continue to recover following the expansion in revenue: Since 2017, the company has seen ~11.8% annualized revenue growth ((CAGR)), according to IR materials. Earnings look volatile, but that is a feature of the industry.

In the last quarter, the company significantly increased its total shareholder return through buybacks and dividends, which is also good news:

But what about UVE's valuation?

The Valuation

I already mentioned UVE's valuation in my recent article on International General Insurance ( IGIC ) - I used the company's ratios for comparison:

Seeking Alpha

As you can see, UVE is trading at a relatively low price-to-earnings ratio compared to its peers, although its EPS growth is also relatively low. If we look at the price-to-book ratios, UVE looks like a relatively fairly valued player in its niche:

Given the speed with which the company is coming out of the red, I wouldn't be surprised if the recent earnings surprise continues for several more quarters (Wall Street, represented by 1 analyst who forms the consensus, will probably be too slow to adjust expectations).

If we assume that UVE's P/E ratio rises to just 8x (versus the sector median of 9.75x) and that actual earnings per share in fiscal 2024 exceed consensus by 10% (which is close to the historical norm), then UVE stock's fair value should be ~$20.24. That's 22.2% more than what I see on my screen today.

The Bottom Line

Investing in Universal Insurance Holdings stock carries various risks, including:

- vulnerability to weather-related events such as hurricanes;

- potential adverse impacts from changes in insurance regulations or legislation;

- susceptibility to economic downturns affecting demand and investment returns;

- the competitive nature of the insurance industry;

- the possibility of inaccurate underwriting assumptions or insufficient reserves;

- market-related risks affecting the investment portfolio;

- exposure to catastrophic events that could result in significant claims.

Additionally, the company's performance is influenced by broader economic conditions, interest rates, and real estate market fluctuations.

But despite this long (and incomplete) list of risk factors, UVE stock is still an undervalued company after rising 62% in YTD. I rate the stock a 'Buy' and see an upside potential of ~22.2%, not to mention the dividend yield of ~3.86%.

Thanks for reading!

For further details see:

Universal Insurance Holdings: Still Undervalued After The YTD Rise Of 62%