USAP - Universal Stainless & Alloy Products: Operational Improvements Should Boost The Deleveraging Phase

2023-11-07 09:57:45 ET

Summary

- Sales have soared boosted by rising product prices and a recovery in the aerospace industry.

- Profit margins have expanded considerably thanks to higher product prices and increased volumes.

- Capital expenditures will soon decrease thanks to the completion of the growth project at the North Jackson plant, and the new equipment should provide improved margins from 2024.

- The company should be able to start deleveraging its balance sheet as inventories are unusually high.

- Despite the recent surge in the share price, it is still not too late for investors as the share price is 51% below 2018 levels.

Universal Stainless & Alloy Products

In January 2022, I wrote an article about Universal Stainless & Alloy Products (USAP) because the impact of the coronavirus pandemic was particularly serious for the company as 70% of its revenues were generated in the aerospace industry at a time marked by global travel restrictions. Furthermore, strong inflationary pressures were causing a significant contraction in profit margins. By then, the company's shares accumulated a 73% decline from mid-term highs as profit margins entered negative territory due to lower volumes and higher raw material costs, but these headwinds seemed temporary as the restrictions derived from the coronavirus pandemic were expected to eventually be lifted and the rise in the price of raw materials had been so sudden and extreme that there had not been time for recent product price increases to be fully reflected in operations. Also, the company reduced its debt load in recent years, which contributed to a significant reduction in interest expenses.

Although it is true that long-term debt has increased by $22.8 million since then, operations have shown strong improvements during the three quarters of 2023 as revenues and profit margins have increased significantly, which has allowed the company to generate relatively strong cash from operations. Furthermore, the company still continues to increase the price of its products while inventories are significantly higher than long-term debt, which should allow for stronger cash from operations in the medium term with which to start deleveraging the balance sheet soon. In this regard, we are currently in a moment of strong optimism compared to 2022, but there are still serious doubts as to whether recent operational improvements will be sustained over time and whether the company will be able to convert inventories into actual cash to reduce debt levels as interest expenses have skyrocketed in recent quarters due to higher interest rates while concerns of a global recession caused by recent interest rate hikes continue to grow. For this reason, the share price is still 51% below the peak of $31.20 reached in 2018, and since operations are expected to continue improving in 2024, I believe that it is still not too late to invest in Universal Stainless & Allow Products as projected strong cash from operations should pave the way for a deleveraging process that should open the door for future growth projects.

A brief overview of the company

Universal Stainless & Alloy Products is a manufacturer of semi-finished and finished specialty steel products, including stainless steel, nickel alloys, tool steel, and other premium alloyed steel products for service centers, forgers, rerollers, and original equipment manufacturers. The company was founded in 1994 and its market cap currently stands at $140 million as it employs over 600 workers.

Stainless & Alloy Products logo (2023 Jefferies Industrials Conference) Stainless & Alloy Products logo (2023 Jefferies Industrials Conference)

{kind=link}

Since 2012, the company has been dedicated to reducing its debt levels following the major acquisition of Patriot Special Metals in 2021 for ~$105 million, and long-term declined from $105.24 million in 2012 to $49.13 million by the time I wrote the last article in January 2022, but lower profit margins derived from strong inflationary pressures and lower volumes have reversed much of these efforts, which is one of the main reasons for the share price to remain partially depressed. Even so, it is important to note that reducing debt levels again should not take so long as inventories are very high while profit margins are once again at high levels.

Currently, shares are trading at $15.36, which represents a 50.77% decline from mid-term highs of $31.20 on March 13, 2018, as the damage that declining revenues caused to the balance sheet during the pandemic crisis in 2020 and in 2021, as well as lower profit margins due to declining volumes and higher raw material costs have caused a lot of frustration for investors who, despite having seen operations improve dramatically in 2023, are still not convinced due to the apparent risk of a global recession as a consequence of the recent interest rate hikes. Even so, the increase in the cost of raw materials in recent years caused significant increases in the prices of the company's products which, added to the recent recovery in volumes, have caused a significant increase in revenues that should allow significantly dilute debt now as profit margins begin to improve.

Revenues are skyrocketing boosted by pricing actions

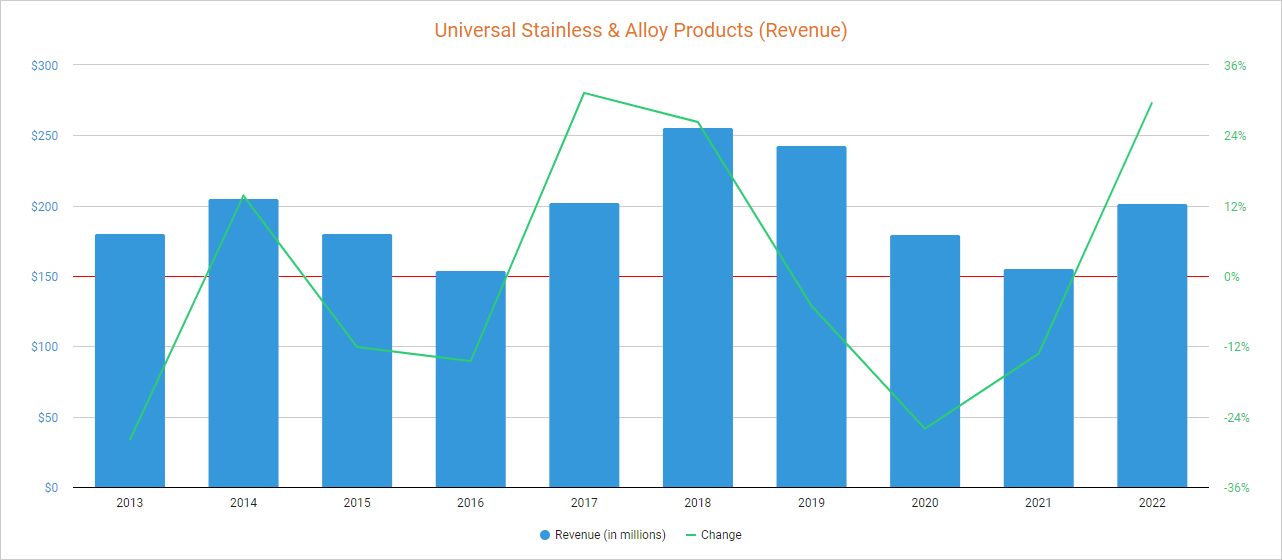

Revenues have remained relatively stagnant in recent years as the company has gone through a deleveraging phase after the major acquisition of Patriot Special Metals in 2011, and the coronavirus pandemic crisis caused a 26.04% decline in 2020 and a further 13.24% decline in 2021. Still, revenues broke their negative trend in 2022 as they increased by 29.62% compared to 2021, and although they are still 21.02% below the sales achieved in 2018, 2023 is expected to close marking a new sales record.

{kind=link}

In this regard, revenues increased by 38.48% year over year in the first quarter of 2023, by 32.32% in the second quarter, and by 54.31% in the third quarter (also year over year) as the company keeps raising the price of its products. In this regard, revenues are expected to increase by 38.20% in 2023 (and therefore exceed 2018 sales by 9.14%) and by a further 4.54% in 2024. The backlog increased to $345 million during the third quarter of 2023 (vs. $ 246.3 million during the same quarter of 2022) as the aerospace industry is expected to continue growing in the foreseeable future, and 37% of that backlog is of high-margin premium products, which means both revenues and profit margins should remain high in the foreseeable future.

But despite the fact that revenues have skyrocketed in recent quarters, the P/S ratio is at 0.541, which is still 13.85% below the average of the past 10 years. This means that the company currently reports annual revenues of $1.85 for each dollar held in shares by investors.

Furthermore, this ratio represents a 63.52% decline from decade-highs of 1.483, which reflects that there is still a lot of pessimism and doubts among investors despite recent improvements in operations due not only to the recent increase in long-term debt, higher interest expenses, and concerns of a potential recession, but also because profit margins, despite the recent recovery, have suffered strong volatility in recent quarters, and a potential new contraction is still not a risk to be ruled out.

Profit margins have recovered boosted by base price raises

Since the coronavirus pandemic crisis back in 2020, declining volumes due to travel restrictions, as well as subsequent inflationary pressures due to higher raw material costs, pushed both gross profit and EBITDA margins into negative territory in 2020 and 2021, but they have been improving to high levels today. In this regard, the trailing 12 months' gross profit margin currently stands at 11.76%, and the EBITDA margin at 9.52%.

Furthermore, the gross profit margin improved to 15.2% in the third quarter of 2023 (vs. 14.3% during the same quarter of 2022) and the EBITDA margin to 12.61%, which are the highest profit margin levels reported in the post-pandemic era, as the company has continued raising the price of its products in 2023 while higher premium alloys sales enabled a better price mix. In this regard, sales of premium alloys doubled year over year in the third quarter of 2023, and the management plans to keep increasing capacity production for these alloys with the aim of maintaining high profit margins in the long run. Nevertheless, higher volumes also helped in boosting profit margins in recent quarters. This allowed the company to report net income of $1.9 million during the quarter (vs. -$1.3 million in the same quarter of 2022), which essentially reflects recent dramatic operational improvements.

The company has raised base product prices 15 times since late 2021 and keeps raising them as it announced a base price increase of 5% to 10% on bar products on July 31, 2023, and on October 13, 2023, it also announced a base price increase of 5% to 10% on premium products, which means profit margins and sales should continue to increase in the coming quarters (or at least maintain current high levels), which should help in keeping diluting long-term debt as cash from operations is increasing significantly thanks to higher dollar sales and the recent margin recovery.

The company is ready to start a new deleveraging phase

The year 2022 was very frustrating for investors as the increase in long-term debt undid much of the efforts carried out in the past 10 years as the company's main goal has been to reduce its debt levels after the acquisition that took place in 2011. After closing 2012 with $105.24 million in long-term debt, the company managed to pay a big portion of it to $32.4 million by 2020, but declining volumes, contracted margins, and higher capital expenditures due to premium capacity expansion projects caused a surge in long-term debt as 2022 closed with an exposure of $89.4 million, a figure that increased to $93.1 million during the first quarter of 2023. Still, the deleveraging process seems to have started as the company reduced long-term debt by $4.2 million in the second and third quarters to $88.9 million.

The positive part is that reducing inventory levels again should not be a major problem now that inventories are at record levels of $150.75 million (when long-term debt was $32.4 million in 2020, inventories were $111.4 million), and although the management doesn't expect a significant reduction in 2024 due to an inventory shift towards premium products, these inventories should eventually be partially emptied. This is a good example of how inflation helps in diluting debt in the long run as the company should be able to eventually convert these inventories into actual cash with which to pay down debt.

In this regard, trailing 12 months' cash from operations currently stands at $15.2 million as inventories declined by $8.1 million while accounts payable only increased by $1.8 million in the same period. But still, accounts receivable increased by $13.9 million in the same period, which means that cash from operations should remain robust in the foreseeable future.

Furthermore, trailing 12 months' cash from operations should significantly improve in the coming quarters as net income has improved sequentially in the three quarters of 2023 while the fourth quarter of 2022 was actually a very bad quarter as the company reported negative cash from operations of -$2.6 million and negative net income of -$3.7 million. During the third quarter of 2023, both results were significantly higher as cash from operations was $6.7 million and net income was $1.9 million, and therefore, the data for the last 12 months should improve significantly once the fourth quarter of 2023 replaces the same quarter of 2022.

Now, it is important to take into consideration that interest expenses have begun to increase significantly not only due to a higher debt load but also as a consequence of higher interest rates as trailing 12 months' total interest expenses currently stand at $7.80 million.

The company reported total interest expenses of $2.14 million in the third quarter of 2023, which means annual interest expenses currently stand at $8.56 million. Still, capital expenditures are expected to decrease significantly in 2024 now that growth projects are about to finish, which should almost fully offset the increase in interest expenses. In this regard, trailing 12 months' capital expenditures currently stand at $10.78 million, and the company expects 2023 to close with capital expenditures of $14 million to $16 million as the company is adding two VAR (Vacuum-Arc Remelt) furnaces to its North Jackson plant, which are expected to be operational in the first quarter of 2024 and provide a 20% increase in the company's bar capacity. Once the project is completed, capital expenditures are expected to be cut almost by half, which should free up significant cash with which to cover interest expenses. Furthermore, as these are two more technologically advanced VAR furnaces, they will be used for the production of premium alloys, which is why they are expected to contribute positively to profit margins.

In this sense, rising interest expenses are putting pressure on management to reduce the company's debt, but decreasing capital expenditures, very high inventories, the recent surge in accounts receivable, and higher revenues and profit margins should enable a successful deleveraging process in the long run, which should ultimately pave the way for future acquisitions and/or growth projects.

Risks worth mentioning

Before venturing to invest, it is very important to understand that the risk profile of Universal Stainless & Allow is high as it is a micro-cap company with a high cyclical nature, and the recent increase in the share price already reflects part of the recent operational improvements and part of the growing optimism of a part of the investment community. Therefore, there are certain risks that I would like to highlight especially for the short and medium term.

- Recent interest rate hikes could trigger a global recession, which could have a significant impact on the company's operations as it has strong exposure to the aerospace industry.

- The company could have difficulty converting its inventories into actual cash in case demand does not maintain at least current levels in 2024 and beyond.

- A new surge in inflation rates (especially regarding raw material prices) could cause further contractions in the company's profit margins.

- Annual interest expenses of over $8.5 million could pose a very serious problem for the company if it does not manage to maintain current cash from operations, so a new contraction of profit margins or difficulty in reducing inventories in the middle term would likely be translated into a significant deterioration in the company's prospects.

- We must not forget that we are currently living in a very volatile macroeconomic landscape, with war conflicts between Russia and Ukraine and Israel and Palestine, as well as high-interest rates to contain high inflation rates, so those investors with a more conservative approach could choose to invest in tranches in order to buy shares at lower prices in case they fall again, and thus reduce the average purchase price.

Conclusion

Since I wrote my last article in January 2022, the situation has improved significantly for Universal Stainless & Alloy Products, and the share price has increased by 81.20% as a consequence. Both sales and profit margins are at very high levels compared to the average of past years, and the situation is expected to continue improving in the foreseeable future. Although revenue growth for 2024 is expected to be very modest at 4.54%, this is actually good news in the sense that it means that sales are expected to remain at 2023 levels after the significant increase that is taking place.

The 15 base selling price increases since 2021 have allowed the company to recover its profit margins and greatly dilute its debt load as revenues are dramatically increasing. In addition, profit margins, which are already at maximum levels, still have room to improve due to two factors: firstly, because the price of the company's products continued to increase in October 2023, and secondly because the opening of the two new VAR furnaces at the North Jackson plant will significantly increase production capacity for premium alloys as soon as the first quarter of 2024.

Taking into account that the increase in the production capacity of premium alloys will likely provide a superior profitability profile from 2024 and that a successful deleveraging process should open the door to the next stage of growth, I consider that, despite the 81.20% surge in the share price since the last article I wrote, it is still not too late to invest as the share price is still 51% below 2018 levels.

For further details see:

Universal Stainless & Alloy Products: Operational Improvements Should Boost The Deleveraging Phase