OTGLY - Unraveling CD Projekt's Success Story: The Witcher Saga And Beyond

2023-09-14 11:39:30 ET

Summary

- CDP has a strong reputation for the development of RPG games, with two highly valuable titles.

- Management's intention is to expand this to three, while also increasing the frequency of content releases, implying strong growth is ahead.

- We consider CDP to be one of the most commercially attractive businesses in the gaming industry, reducing execution risk.

- CDP has market-leading margins, with an EBITDA-M of 45%. We expect this to trend up over time, as new content is released.

- Despite the positive outlook, the business looks far too expensive. New game releases are years away, and so investors risk holding a stock that will trade sideways.

Investment thesis

Our current investment thesis is:

- CDP is a fantastic business. The developer is consistently producing incredibly entertaining games while backing this up with financial excellence. The business is outgrowing its peers and has margins that are unrivaled.

- The pipeline looks positive, especially when considering the new titles expected in the coming decade. We see the coming years as a process of taking this business into the mainstream, with incremental increases in the content output from the business.

- CDP is unfortunately far too expensive. Unless the developer was to release a new Witcher game and its new IP within the next 5 years, which is almost impossible in our view, we do not see the returns necessary to justify this valuation.

Company description

CD Projekt ( OTGLY ) ( Referred to as CDP throughout this paper ) is a renowned Polish video game development company known for its critically acclaimed titles, including The Witcher series and Cyberpunk 2077. The company is based in Warsaw, Poland, and has established a global reputation for producing high-quality and immersive RPG games. The Witcher series has sold over 75m copies and the Cyberpunk 2077 game has sold over 20m copies.

In addition to this, the company owns GOG.COM, a digital distributor of games with over 7000 titles. The digital distributor industry is dominated by "Steam", with GOG as one of its closer competitors.

Share price

CDP's share price has performed exceptionally well in the last decade, at one point generating over 1000% returns. These gains have subsequently been lost but the appreciation remains in excess of the S&P 500. The share price performance is a reflection of the company's strong development during this period, with volatility a byproduct of changing expectations from investors.

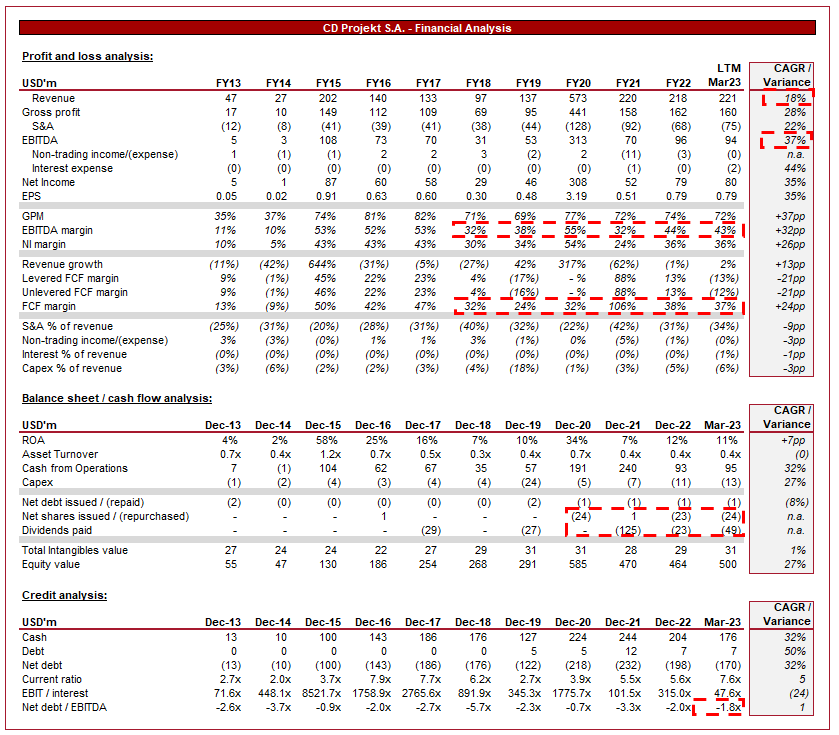

Financial analysis

CD Projekt financials (Capital IQ)

{kind=link}

Presented above is CPD's financial performance for the last decade.

Revenue & Commercial Factors

CDP's revenue has grown at an impressive 18% rate in the last 10 years. As a publisher reliant on 2 primary IPs (1 for most of this period), its YoY growth is highly volatile around new game/content releases. The trajectory, however, is clearly upward.

Business Model

CDP's business model primarily revolves around developing and publishing single-player role-playing games (RPGs) with deep narratives and open-world environments. The company focuses on providing captivating storytelling, memorable characters, and high-quality gameplay experiences to its players. The company's objective has been to develop a strong reputation for high-quality games, creating greater certainty over the success of new releases as consumers feel confident that each new release will be worth the financial and time investment. Cyberpunk 2077 was a new IP release and despite the drama around its release (which we will discuss later), it sold over 20m copies. This perfectly illustrates that CDP has developed this trust in the community. Management is looking to accelerate the business in the coming decade, with heightened recruitment and faster development of new content.

CDP's business model incorporates diversified revenue streams, including game sales, downloadable content ((DLC)), expansions, merchandise, licensing, and adaptations. Further, the company has expanded into mobile games, following a similar strategy to its peers. This diversification has become mandatory in the industry and made it incredibly attractive in our view, as it reduces the financial risk of releasing games and has contributed to significantly higher monetizable potential for each game. Historically, a publisher sold a game once to consumers and that was broadly it. Now, future DLC is almost guaranteed, and there is also scope for in-game purchases (creating recurring revenue). We would like to see CDP develop its monetization further, as it is currently focused primarily on DLC only.

CDP's commitment to a player-centric approach has been a key driver of its growth. The company actively engages with its community, listens to player feedback, and incorporates suggestions and improvements into its games through updates and expansions. Unlike its larger peers, the business still gives the impression it is "for the gamers", rather than an "evil corporation". This approach fosters strong player loyalty and word-of-mouth marketing, which contributes to the success of its games. It cannot be understated how much of the success of CDP is underpinned by its reputation. This comes with excellent game development no doubt, but marketing is just as important financially.

CDP has established an effective distribution and marketing strategy, ensuring its games reach a global audience. The company offers its games on Steam, but importantly, heavily promotes them on its own platform GOG (as well as, console storefronts). The GOG platform has a good reputation in the industry, providing DRM-free games and many older, classic games. The GOG platform is not necessarily highly profitable or a lucrative segment for the business, but we see it as a strategic investment to drive further interest in its games (and an outside bet on breaking Steam's grasp on the industry). As previously mentioned, Steam has a monopolistic position in the industry, deterring competitors. This gives GOG the ability to quietly develop its position as the second in line, winning customers through its consumer-friendly approach and then advertising CDP's games to them.

"The Witcher" series has been a monumental success for CDP, and the company has capitalized on the franchise's popularity through expansions, spin-offs, and merchandise. The "The Witcher" TV series on Netflix has further developed an interest in the franchise, although the departure of Henry Cavil and mediocre reviews could mean the show will not last much longer.

In the development of CP77, CDP broke all of the characteristics we discussed above and paid a high price. We will not regurgitate an old story but we believe the business essentially released an unfinished game, while working its employees into the ground. Consumers were unhappy, the business faced a large number of returns, and its reputation was diminished in our view. Subsequently, the game has been fixed and now has a "Very Positive" rating on Steam, with over 540k reviews. We consider this a cautionary tale for Management and do not think it will have a long-term negative impact so long as this is never repeated. As the old saying goes, fool me once, shame on you; fool me twice, shame on me.

Cyberpunk 2077 (Steam)

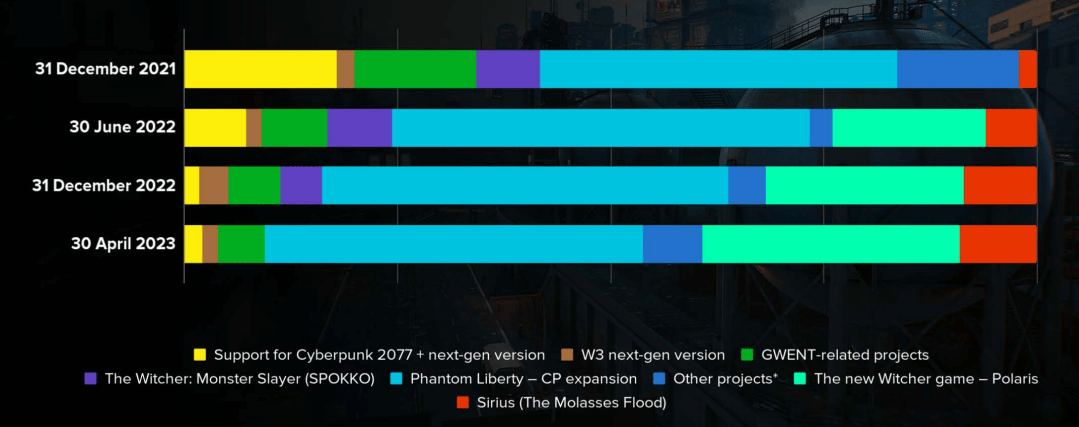

CDP's long-term objective involves the creation of a third title, as well as the development of new games and DLCs under its existing IP. It is critical to increase the number of titles it produces, to extend the time between releases for its existing IP. The risk otherwise is that consumers become bored of an idea and CDP's developers are overly pressured to create new ideas. We do not doubt the success of this new IP, given the quality the team has shown thus far and the tough lessons it has learned in recent years. Current development time is committed primarily to CP77 DLC and a new Witcher game, implying there are still several years until a new game is released.

{kind=link}

CDP competes with various game development companies, including Electronic Arts ( EA ), Ubisoft Entertainment ( UBSFY ), Bethesda Softworks ( MSFT ), Rockstar Games ( TTWO ), Capcom ( CCOEY ), and Activision Blizzard ( ATVI ).

Margins

CDP has fantastic margins, with an EBITDA-M of 43% and a NIM of 37%. Similarly to revenue, this fluctuates YoY with content releases. The impressive level is a reflection of the company's development success, with strong inherent demand for its games over time. We see no reason to suggest margins will fall below 40% but should trend upward once a new Witcher game is released.

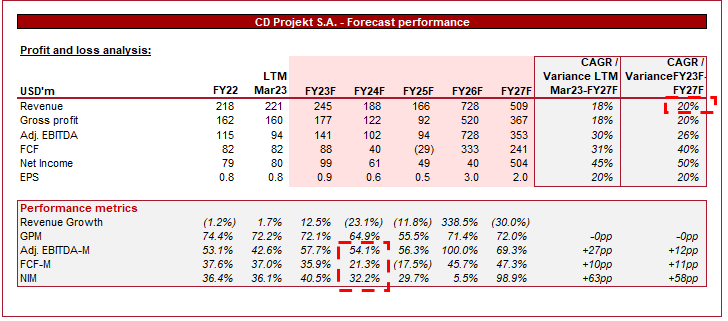

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

This data is useful for understanding when new releases are expected to occur. With 21% growth in FY23F, it is reasonable to assume this will be the year for the CP77 expansion. Following this, a significant jump in FY26F, likely being driven by the new Witcher game. Based on this, we believe investors have a long time to wait for bigger returns.

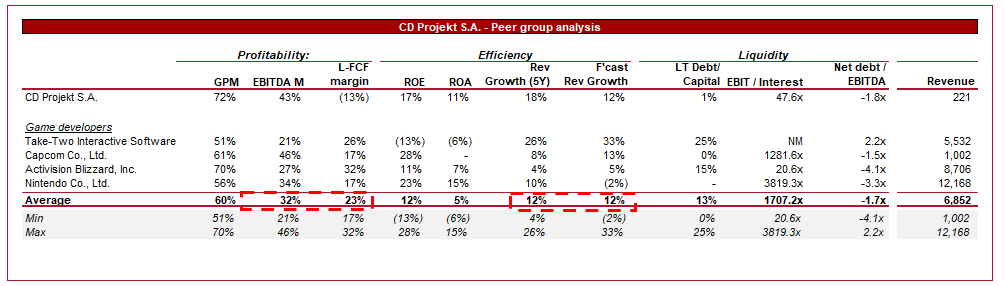

Peer analysis

{kind=link}

Presented above is a comparison of CDP to a cohort of high-performing peers.

CDP performs exceptionally well when comparing the businesses. Its margins are the highest of the pack, while still managing to exceed both the historical and forecast growth rates. The key criticism for CDP would be its size, it is substantially smaller and is unlikely to exceed any of the others bar Capcom. Further, it has the smallest portfolio of games, increasing development risk.

Nevertheless, we believe the development team is extremely talented and the trajectory of the business will remain upward, at least in the next decade. For this reason, a premium valuation is justifiable.

Valuation

Valuation (Capital IQ)

CDP is currently trading at 39x LTM EBITDA and 29x NTM EBITDA. This is a 40%/19% LTM/NTM EBITDA premium to the chosen peer group. We suggest a 25% premium would leave some room for gains, even still the business is substantially overvalued.

The current premium looks impossible to justify. If CDP had several more titles and a few more billions in revenue, then maybe. At $211m in revenue and 2 successful titles, we cannot see a reason for this.

Analysts' consensus price target currently has the stock overvalued by 22%, one of the largest levels we've ever seen.

Final thoughts

We very much like CDP. The future looks incredibly bright, as incremental content releases, such as DLC, supplement the cycle of new games. Once a new title is developed, we believe the business will be propelled substantially.

Its impressive commercial standing is also reflected in its financials. The business is growing quickly and has incredible margins, unrivaled by its peers. Unfortunately, at this price point, investors have very little to gain.

We suggest this stock should be monitored intently and if an opportunity presents itself, you shouldn't think twice

For further details see:

Unraveling CD Projekt's Success Story: The Witcher Saga And Beyond