UPMMY - UPM-Kymmene: Destocking Hits But Ramp Ups Mitigate

2023-10-13 13:36:46 ET

Summary

- UPM-Kymmene is growing pulp production by over 50% and expanding capacity in other areas of their business.

- Energy and pulp prices have declined, putting pressure on EBIT evolutions, but volume increases are offsetting some of the negative impacts.

- Sequential destocking improvements are being observed in the Raflatac business, and stabilizing markets in China are offsetting declines in Europe.

- The business is clearly heading up in H2, and should be up further at full-ramp in 2024. But it's only fairly valued considering the multiple already acknowledges that.

UPM-Kymmene Oyj ( UPMKF ) is a paper player but not a pureplay. They do a couple of things and are partially vertically integrated. They are growing pulp production by more than 50%, and the per tonne cash costs are pretty attractive, although not as good as Suzano ( SUZ ). They are also growing other areas of their business in terms of capacity. Communications papers is being downsized, and the Raflatac business is being hit by destocking trends. In general, we see decent evolutions sequentially in H2 thanks to both volumes and prices. Not a bad situation, but we don't love the valuation.

Breakdown

The following are UPM's businesses.

{kind=link}

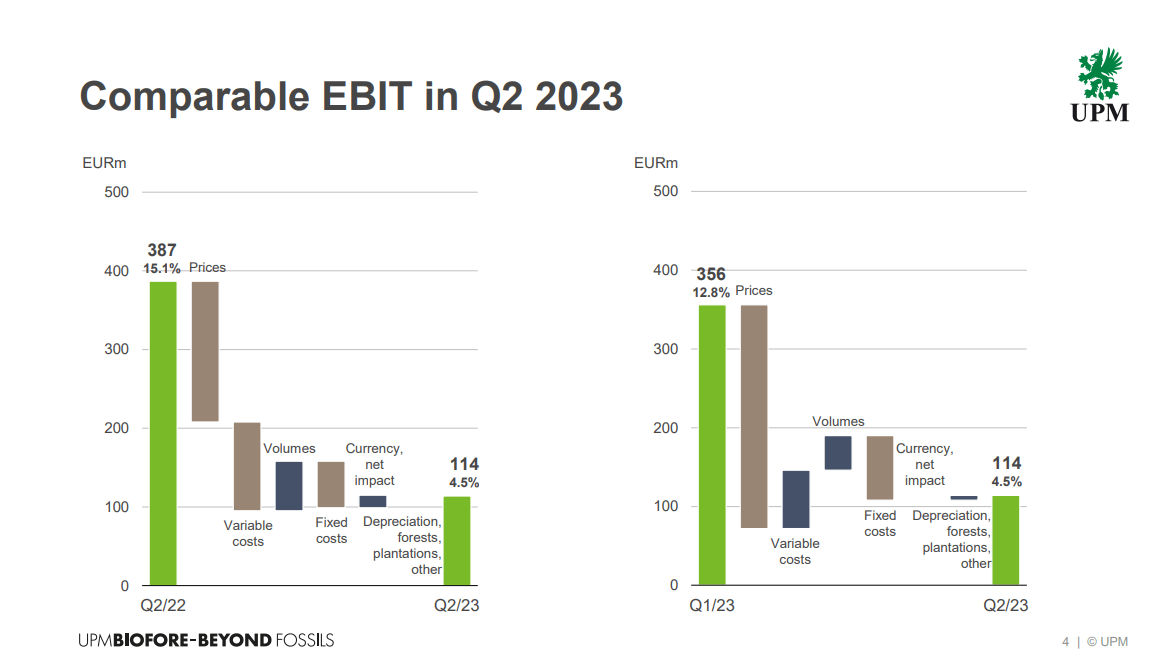

Energy and pulp prices have come down meaningfully, causing a price pressure on overall EBIT evolutions. Variable costs hadn't come down either in line with the pulp declines. While very vertically integrated , pulp is a product that is sold internally to the paper businesses at fair costs and has to clear inventories which results in the current expensing being at pulp's high historical prices , hitting margins as sales are happening on pulp's lower prices in the pulp business. This effect goes away next quarter as run-rates start resetting to a newer normal with lower variable costs. Offsets have seen nice volume increases, in particular due to the ramping up of production in the new Uruguay plant .

Energy is UPM's large electricity business, and it's falling due to pressure on electricity prices, but there are benefits in terms of volumes that help limit the EBIT impact due the first production at some new plants.

Other businesses have been more stable, with good profit management, but some overhang from destocking, although the only major negative volume deltas are coming from the Raflatac and specialty papers business which are exposed to labels and other paper that gets directly affected by consumer destocking trends the most.

The communications paper business is being restructured. 18% of the capacity is being retired to generate savings, which will of course hit volumes but not negatively affect profits.

All businesses have suffered on account of maintenance.

{kind=link}

Bottom Line

Sequential destocking improvements are being observed in Raflatac according to management, at least being tentatively observed. It is easily assumed that the destocking trends will be temporary as immediate supply chain threats pass.

Moreover, some of the negative impacts in markets like pulp in China has stabilised, and this is offsetting the declines that are likely yet to come in Europe. Margin expansion from catch-up effects should also kick in and help profits, on top of meaningful capacity expansions in the energy and pulp businesses.

For the pulp business in particular, capacity is ramping up on a newly completed factory that increases UPM pulp capacity by about 50%. Cash costs are decent at this factory at around $280 per tonne, but it's a lot higher than Suzano which is best in class at $180 per tonne , but does carry sustainability risks that are certainly non-negligible. This is a rare instance where sustainability matters and UPM is already established in this respect.

Energy and pulp increases on the volume side should win share to UPM and help increase volumes in those businesses. Others are also raising capacity so there are likely going to be some continued down effects in price over the next year or two, including Suzano with the Cerrado project.

We believe annualised EBIT could hit around 1 billion EUR, meaning around 19x EV/EBIT multiples for the business. We think EBITDA will exceed 1.5 billion, but that puts the EV/EBITDA multiples above 10x for this year. This is because full ramp up in pulp, which is a major UPM business, still hasn't happened yet. Likewise for the new plant. The chemicals initiative is still in early stages and has been delayed due to supply chain issues and cost inflation so we'll ignore it.

UPM is quality. It will grow certainly as volumes grow, and we think prices are bottoming out to some extent. Its assets are valuable, but it will have to be after FY 2023 that multiples start coming down to more reasonable levels under 10x where they belong considering a certain degree of volatility, economic risks, and the higher cost of capital. Not compelling, but also deserving of a premium at this point in time.

For further details see:

UPM-Kymmene: Destocking Hits But Ramp Ups Mitigate