UPWK - Upwork: Rocky Conditions Moving Forward

2023-12-20 00:20:25 ET

Summary

- Upwork's stock price has rallied over 40% this year, but is at risk of unwinding.

- Poor growth trends and slower upmarket push into enterprise are major risks for Upwork.

- Despite the company working rapidly to integrate AI into its services, in the long run more jobs will be automated and likely drastically reduce the need for freelancers.

Amid tremendous optimism for the stock markets in 2024, investors have to be careful to maintain strong discipline in stock-picking: particularly, weeding out stocks that have limited catalysts to outperform in the new year.

Upwork ( UPWK ), in particular, is a company that bears careful monitoring. This freelance/gig-based marketplace platform, a rival to Fiverr ( FVRR ), has seen its stock price rally more than 40% year to date - but in my view, that gain is at risk of unwinding.

I last wrote a bearish opinion on Upwork in August, when the stock was trading closer to $14 per share. Since then, amid a broad market rally, the stock has continued to rally, despite the release of what I considered to be a relatively weak Q3 earnings print. We'll cover the results in more detail in the next section, but in brief: Upwork saw accelerating revenue growth, but that was largely a function of pricing - and underlying gross services volume, meanwhile, continued to slow down.

All in all, I remain bearish on Upwork. The core risks that I see for this company are:

- Poor growth trends evidenced by low GSV expansion. Upwork's big appeal is the growth of its enterprise business, and in the long run, the company is supposed to be a recurring services provider to the Fortune 500. The reality, however, is that enterprise client additions have slowed; as has average spend per customer - indicating that the upmarket push is going much more slowly than planned.

- Pricing levers can't be used forever to chase revenue growth. Upwork is benefiting from a change in its pricing structure earlier this year that has boosted take rates and revenue, but the company can't indefinitely keep updating its prices to grab more revenue amid flat gross services volumes.

- Long-term AI risks. The company has dove headfirst into the AI space, creating an "AI Services Hub" on its platform and hoping to empower AI-enabled gig workers to take on new assignments. Over the long run, however, I think automation will eventually take over many of the gig functions that are core to Upwork's platform: tasks like website building, copyediting, translation and graphic design are all functions that are easy to see being cannibalized by AI.

To me, there is little incentive to staying invested in this name, and I don't see any upside catalysts for this stock to justify a rally in 2024. Steer clear here and invest elsewhere.

Q3 download

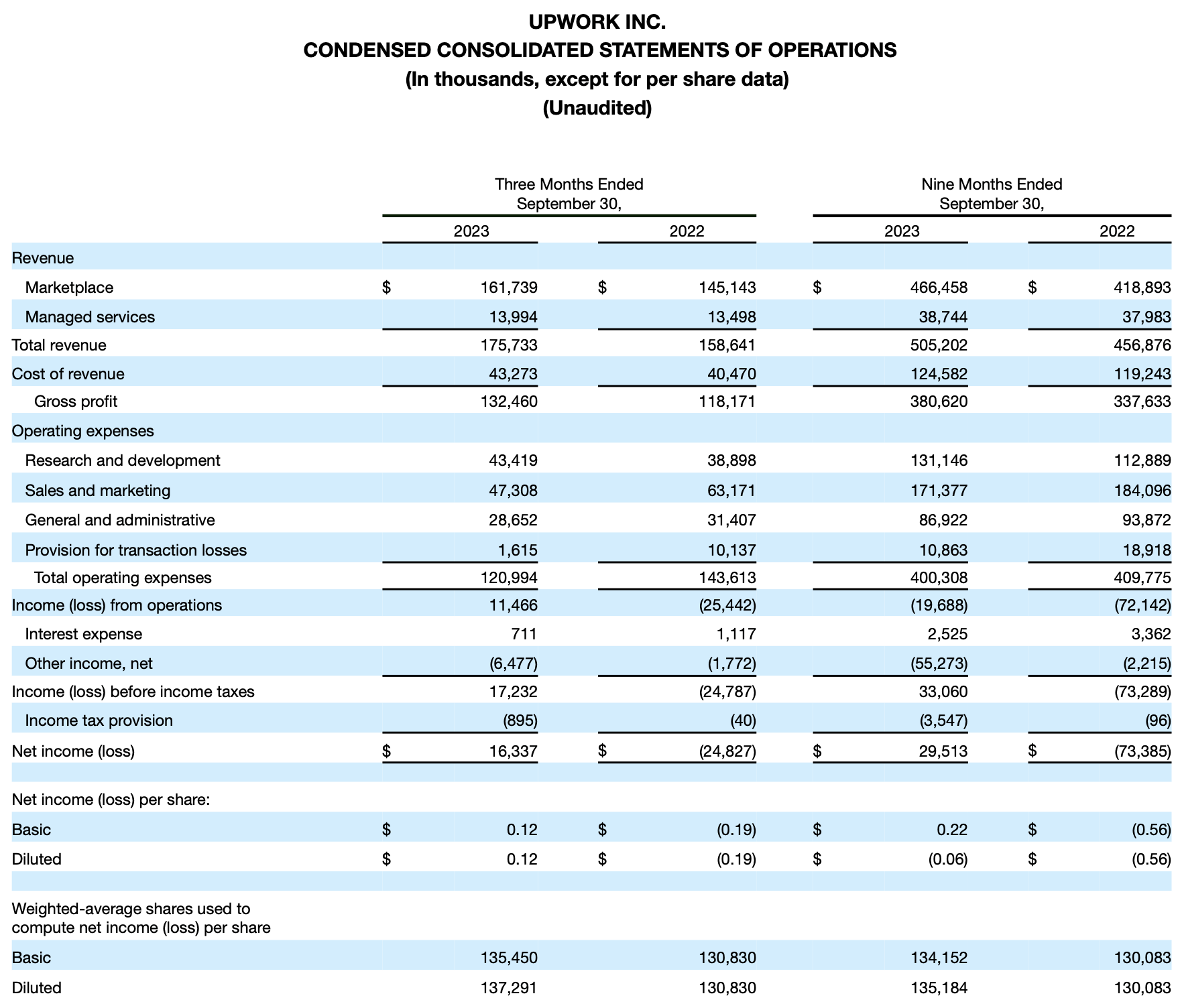

Let's now go through Upwork's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

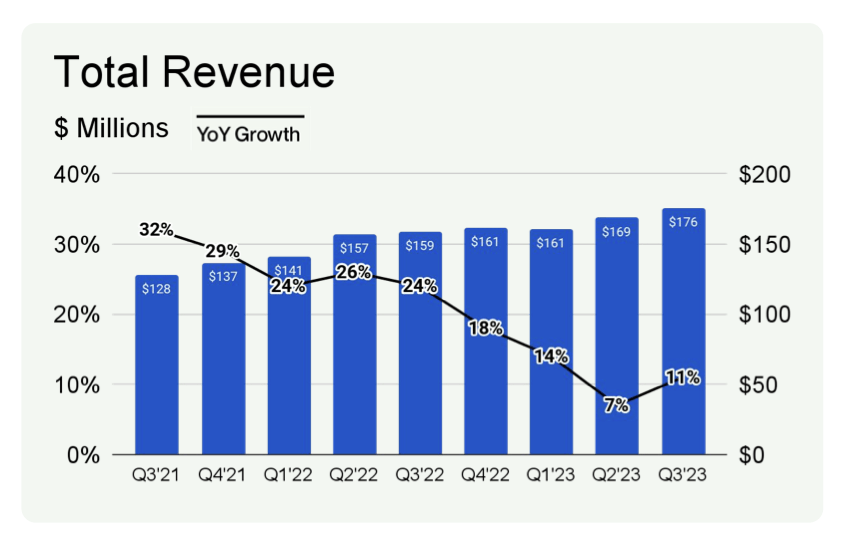

Upwork's revenue grew 11% y/y to $175.7 million, ahead of Wall Street's expectations of $168.1 million (+6% y/y) by a five-point margin, as well as accelerating four points versus Q2's 7% y/y growth rate. As shown in the chart below, it marks a relieving rebound from last quarter's slippage to single-digit growth:

{kind=link}

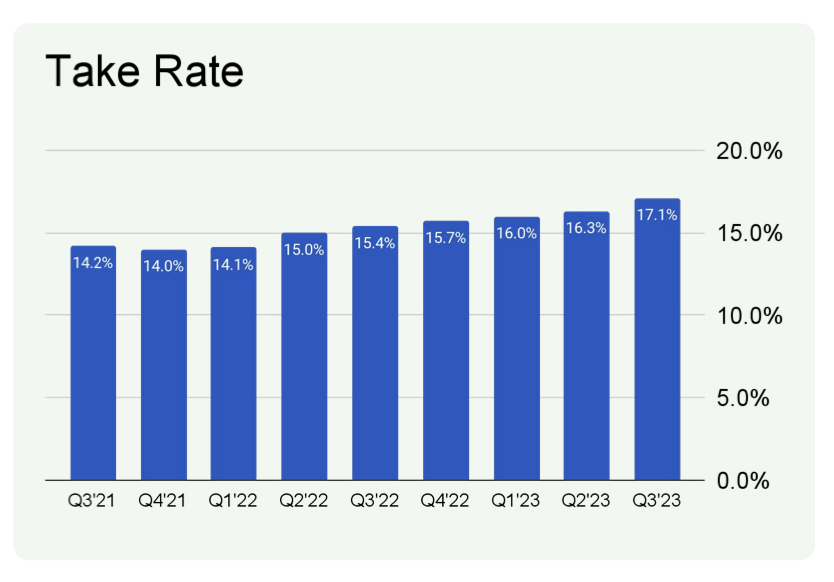

At the same time, however, we have to be cognizant of the underlying drivers. Upwork's take rate hit an all-time high of 17.1% in Q3, up 80bps sequentially and 170bps y/y. This is largely the result of the company moving to a flatter fee structure for freelancers in May of this year, which clearly yielded an effective price increase for the platform. Take rate was also, in smaller part, benefited by the performance of ads on the Upwork platform.

{kind=link}

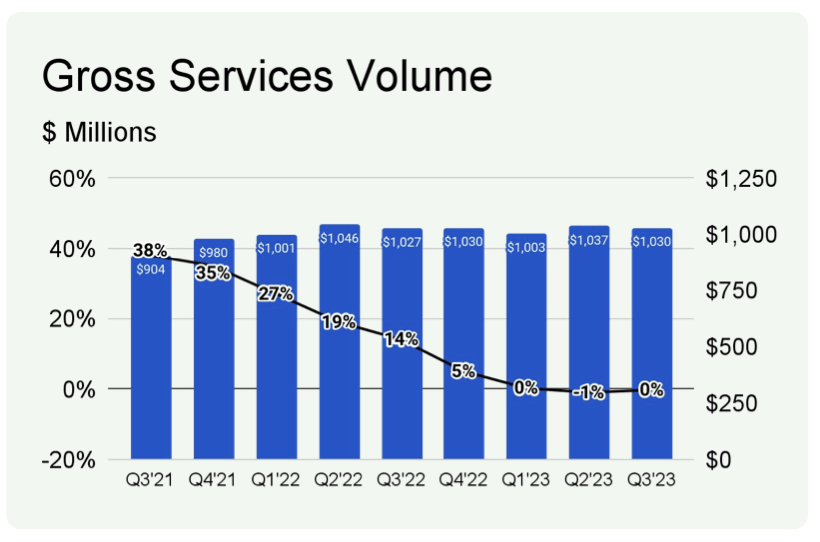

Meanwhile, as shown in the chart below, underlying gross services volume (the total value of all the projects that were undertaken on the Upwork marketplace over the course of the quarter) has actually been flat over the past three quarters. On a nominal dollar basis, Q3's $1.030 billion in GSV was actually lower than Q2 at $1.037 billion. The translation here: buyers just aren't picking up new projects at a growing rate.

{kind=link}

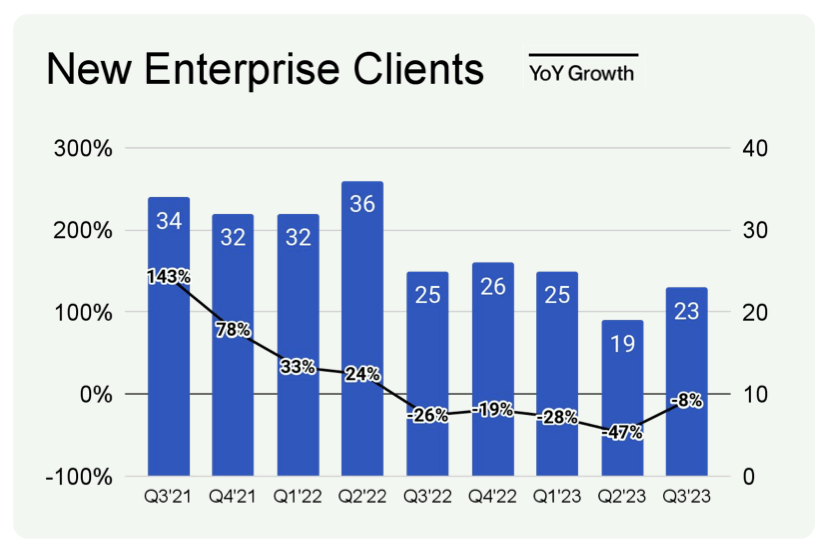

To add insult to injury, Upwork's trend of enterprise client additions has also been in a downward slide. The company did add some notable large companies to the fold this quarter, including Moderna ( MRNA ) and Dropbox ( DBX ), but the total of 23 net-new enterprise clients this quarter was down -8% y/y. In the past, Upwork had been able to add somewhere between 30-40 enterprise clients per quarter.

{kind=link}

Bringing in more AI-related projects, of course, is Upwork's primary goal toward reversing the slowdown. Per CEO Hayden Brown's remarks on the Q3 earnings call:

One of our most ambitious growth goals is to foster the most AI-empowered independent professionals in the world. In pursuit of this, we greatly enhanced our AI Services hub, which has seen a 10X increase in average monthly visitors since its launch in the second quarter, and just yesterday, announced an extension of the hub with a new suite of generative AI app offers and educational content especially designed for talent.

Our scale as the world's work marketplace has aided us in creating a deep and diverse ecosystem of partners that span education, technology and special offers for clients and talent. New features partnerships for AI-powered apps and offers for independent professionals include industry leading companies like Adobe, Amazon, ClickUp and Miro that have advanced integration of generative AI into their tools and services alongside educational AI skill based courses and content from leading providers like Coursera, Jasper and Udemy that form a new education marketplace on Upwork Academy."

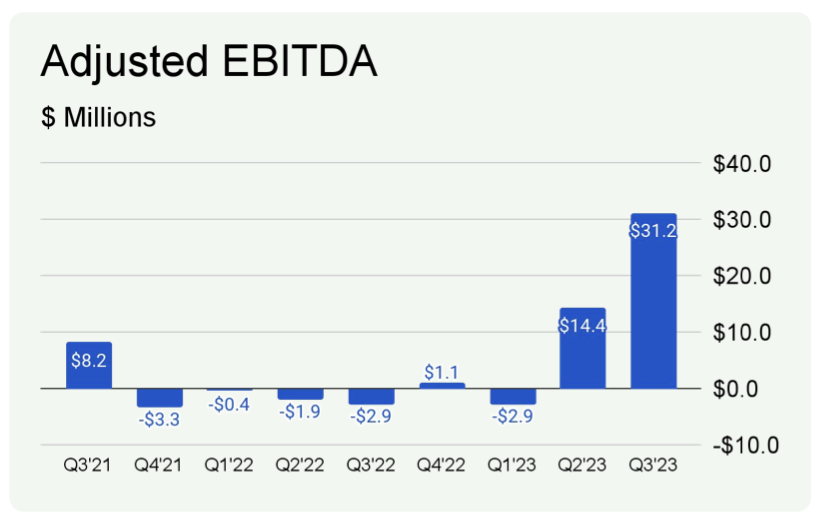

The one bright spot. here is profitability. Earlier this year, Upwork laid off 15% of its headcount .

{kind=link}

The combination of opex trimming plus higher take rates has helped the company generate $31.2 million in adjusted EBITDA in the third quarter, at an 18% margin. Still, however, annualizing Upwork's adjusted EBITDA doesn't help to rationalize the company's valuation from a bottom-line perspective.

Valuation and key takeaways

At current share prices near $15, Upwork trades at a market cap of $2.09 billion. After we net off the $555.2 million of cash and $355.6 million of debt on Upwork's most recent balance sheet, the company's resulting enterprise value is $1.89 billion.

Meanwhile, for next year FY24, Wall Street analysts are expecting Upwork to generate $777.6 million in revenue, up 14% y/y (quite aggressive considering it represents an acceleration from current-quarter growth rates, and Upwork will lap the implementation of its new pricing structure in Q2 of next year). Nevertheless, taking consensus estimates at face value, the stock trades at 2.4x EV/FY24 revenue. At face value, that's a cheap multiple, but it's on par with smaller rival Fiverr - and effectively representing the market's hesitation on freelance platforms, given rapid developments in AI.

While I think take rate-based revenue acceleration will help Upwork look stable at least over the next few quarters, in the long run Upwork faces big growth challenges - and we can see it already with flattening GSVs and lower enterprise adds. Avoid this stock in your portfolio.

For further details see:

Upwork: Rocky Conditions Moving Forward