USFD - US Foods Holding: A Buy At 12x Earnings

2023-10-19 14:00:00 ET

Summary

- US Foods shares have outperformed the market and competitor Sysco, but trade at a 20% discount to Sysco's P/E.

- The company has competitive advantages in purchasing power, operational efficiency, and a broad product and geographical footprint.

- New CEO Dave Flitman may drive operational performance improvements, narrowing the gap in margins between US Foods and Sysco.

Shares of US Foods Holding (USFD) have performed well over the past year with shares up nearly 35%, outperforming the broader market as well as peer Sysco ( SYY ) which has seen its stock decline 15% over the same period. Despite the strong share price performance, US Foods shares trade at a ~20% P/E discount to Sysco. Further, US Foods may see a long-term boost in operational performance under new CEO Dave Flitman which could drive superior medium term EPS growth.

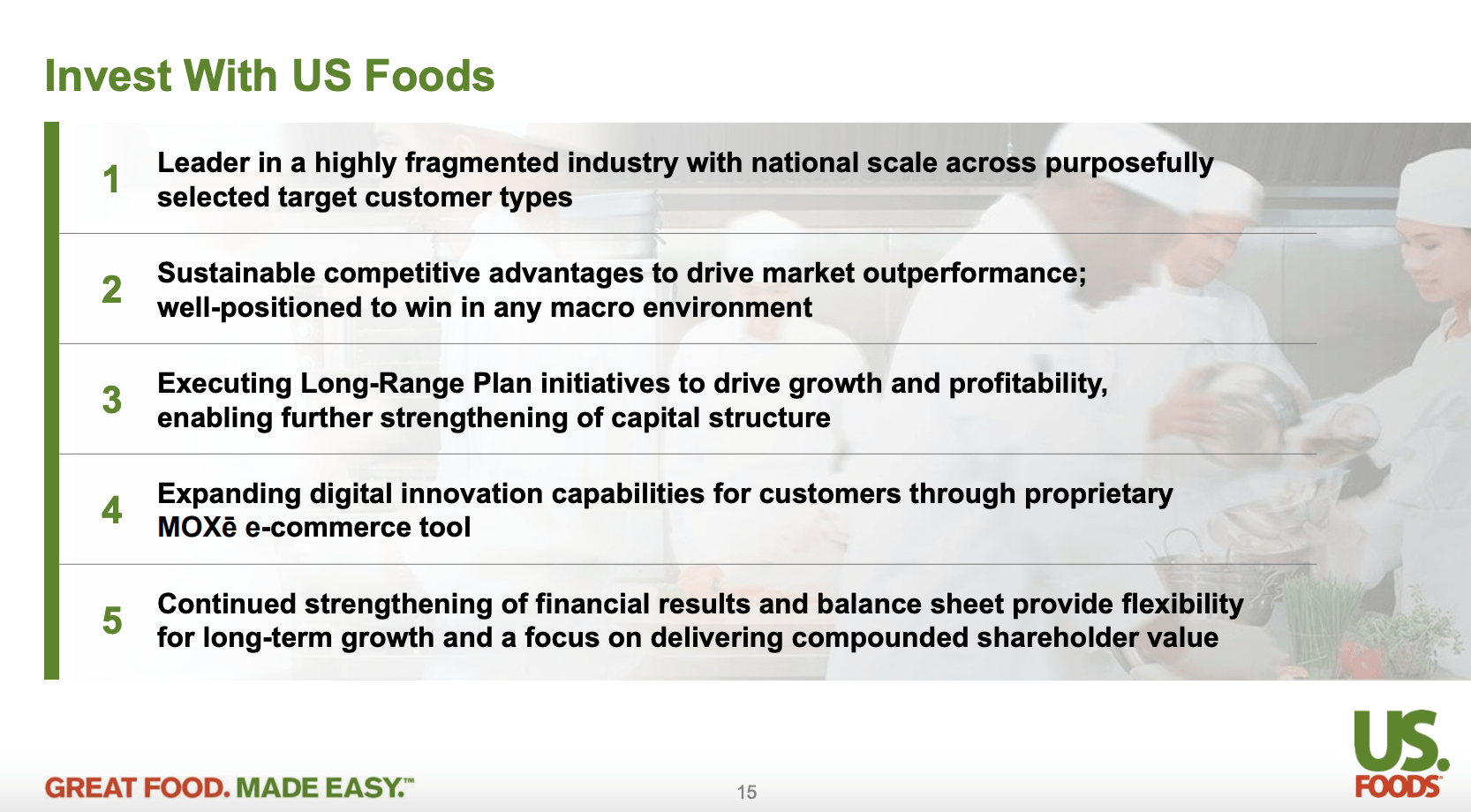

Background

US Foods Competitive Advantages (US Foods Investor Presentation)

{kind=link}

US Foods is the second largest food service distributor, behind Sysco, with ~8% market share and annual sales of nearly $36 billion. Despite consolidation over the past three decades, the top-3 players control just 33% of the US food service distribution industry, suggesting opportunities for continued share gains given the significant competitive advantages held by large players versus local/regional competitors. Competitive advantages include:

- Greater purchasing power - US Foods purchases nearly $30 billion worth of food related supplies annually.

- Operational efficiency - the ability to leverage logistical and overhead costs. US Foods' relatively high market share ensures it has high route density, allowing it to serve customers at a lower cost per delivery. Similarly US Foods has developed leading digital ordering and operating capabilities (lowering the cost to serve customers, and more flexible delivery scheduling which enhanced customer satisfaction). Some of these lower operating costs are passed on in the form of lower prices (allowing US Foods to gain market share) and some are retained in the form of higher operating profit. This creates a virtuous circle where growth begets higher profitability (some of which can be reinvested) stimulating further market share gains and growth.

- Scope - US Foods has a broad product and geographical footprint. A nationwide platform allows the company to meet the needs of restaurant chains looking for a reliable source of consistent supply.

- Private label - US Foods scale and scope has afforded the company the ability to invest in private label products (represent ~35% of revenue). Private label is a win-win for US Foods and its customers- US Foods generates higher margins on private label products while customers benefit from lower priced products (which are generally indistinguishable from branded products).

Food distribution is a 'many-to-many' distribution model. US Foods is not overly reliant on any one supplier of food, and no customer represents a significant percentage of sales. This limits the threat of disintermediation. Overall, I believe US Foods is an above average business.

New Management/Operating Margin Improvement Potential

In January, Dave Flitman took over as CEO of US Foods. Flitman has built a long track record of success in distribution businesses most recently at Builders FirstSource (BLDR) and Univar ( recently acquired by Apollo ). Leaving a company as successful as Builders FirstSource (which admittedly has been aided by a very favorable industry backdrop) to join US Foods suggests that he sees significant opportunity at US Foods.

While the company hasn't formally announced any long term profitability targets since Flitman's arrival, the company is focused on simplifying its organizational structure, increasing digitization, and streamlining its supply chain. Like Sysco (as well as Builders FirstSource and Univar), US Foods was built through many acquisitions and it stands to reason that there are efficiencies to be gained from business process improvement. Of course, this is a multi-year process which will require investor patience.

As we sit today, US Foods EBITDA margins are 100-125 bps below Sysco's US business (including SYGMA). While I expect that Sysco's margins should remain higher than US Foods' margins (owing to larger size & increased benefits of scale), there is an opportunity to narrow the gap which would lead to relatively faster EBITDA and EPS growth for US Foods.

Valuation

US Foods presently trades at just under 12x consensus 2024e EPS estimates. On an absolute basis, I consider this to be an attractive valuation given the competitively advantaged nature of the business and opportunity for continued margin improvement. Moreover, US foods trades at a 20% discount to Sysco which trades at 15x P/E (year end 6/30/24). While it may be appropriate for Sysco to trade at a slight premium, the magnitude of the valuation discrepancy seems too large, particularly if US Foods is able to grow margins and EPS faster than Sysco as it streamlines operations.

Assuming a 17x P/E multiple for US Foods (note that I appraised Sysco's fair valuation multiple at 20x , so I'm not suggesting that US Foods should trade at a premium to Sysco) points to a fair value of $54 per share or 44% above today's price.

Of course there is the potential for earnings headwinds owing to a weaker consumer spending environment. Similar to my expectations for Sysco , I believe this could negatively impact US Foods EPS by 15-20% (possibly a bit less given the self-help initiatives which could bolster profitability in a downturn). In this recessionary scenario, US Foods would be trading at ~15x what I would consider trough-ish EPS.

Conclusion

With a strong competitive position, opportunities for margin expansion, and a relatively low valuation, I see US Foods shares as attractive for long-term investors.

For further details see:

US Foods Holding: A Buy At 12x Earnings