USFD - US Foods Holding: An Attractive Opportunity In Spite Of The Market's Pushback

2023-10-19 11:55:29 ET

Summary

- US Foods Holding Corp. has seen its stock decline by 3.8% since February, while the S&P 500 has risen 9.3%.

- The company's financial performance has been impressive, with strong revenue growth and increased profitability.

- Management has increased guidance for the year, and the stock is reasonably priced compared to similar firms.

In investing, it is important to know that going against the grain is sometimes the best decision you can make. When you do go against what the market believes, you should be prepared to be on the wrong side of a trade for some time. But if you are adamant that your assessment is correct, it's best to continue enduring that pain until you either realize you're wrong or your stance on the matter is validated. One company that I have so far been proven wrong about since I last wrote about it in February of this year is US Foods Holding Corp. ( USFD ). It was in that article , bolstered by strong guidance from management and robust financial performance, that I ended up upgrading the stock from a ‘hold’ to a ‘buy’.

Since then, things have not gone according to plan. Consumer fatigue seems to be pushing down margins across many aspects of the food space. As a result of this, shares of US Foods Holding Corp. have actually declined by 3.8% since I last wrote about the company. By comparison, the S&P 500 is up 9.3%. Although the stock is not the cheapest compared to similar firms, financial performance on both its top and bottom lines has been really impressive. Add on top of this a recent increase in guidance provided by management, and I do believe that's the long-term outlook for investors will be worth the near-term pain.

Things keep getting better

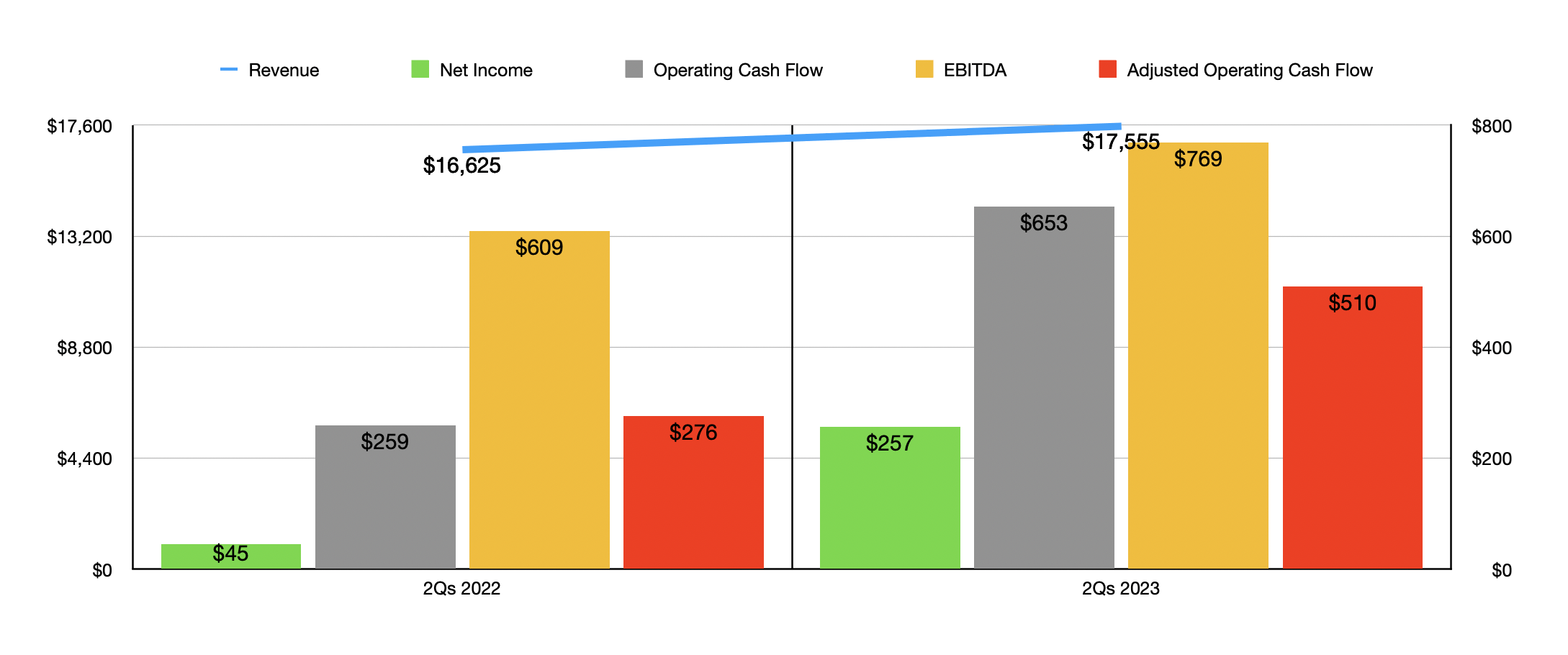

Back when I wrote about US Foods Holding Corp. earlier this year, the company had already reported financial results covering the entirety of its 2022 fiscal year. Since then, we have seen data come out regarding two additional quarters . That will be my primary focus in this piece. For the first half of the year as a whole, revenue has been quite strong, hitting $17.56 billion. That represents an increase of 5.6% over the $16.63 billion the company generated one year earlier. This rise in revenue, according to management, was driven by two primary factors. Total case volume shipped by the institution jumped 4% year over year, driven by a 6.2% rise in independent restaurant case volume, a 12.6% increase in hospitality volume, and a 6.3% rise associated with healthcare volume. Chain volume did drop slightly, to the tune of 2.9%. However, the company also benefited from inflationary pressures that they were able to push onto customers in the amount of 1.6%.

{kind=link}

Author - SEC EDGAR Data

This rise in revenue brought with it significant improvements in the company's bottom line. Net income of $257 million in the first half of the year dwarfed the $45 million reported one year earlier. The most significant improvement on this front came from an expansion in the company's gross profit margin from 15.5% to 17.2%. If applied to the revenue generated in the first half of the year, this would translate to $298.4 million in additional profits. While the increase in sales undoubtedly helped, management said that the gross profit margin improved because of increased freight income from improved inbound logistics, changes in pricing, and other factors. Other profitability metrics followed suit. Operating cash flow nearly tripled from $259 million to $653 million. On an adjusted basis, it grew from $276 million to $510 million. EBITDA for the company increased from $609 million to $769 million. And finally, adjusted net profits rose from $249 million to $324 million.

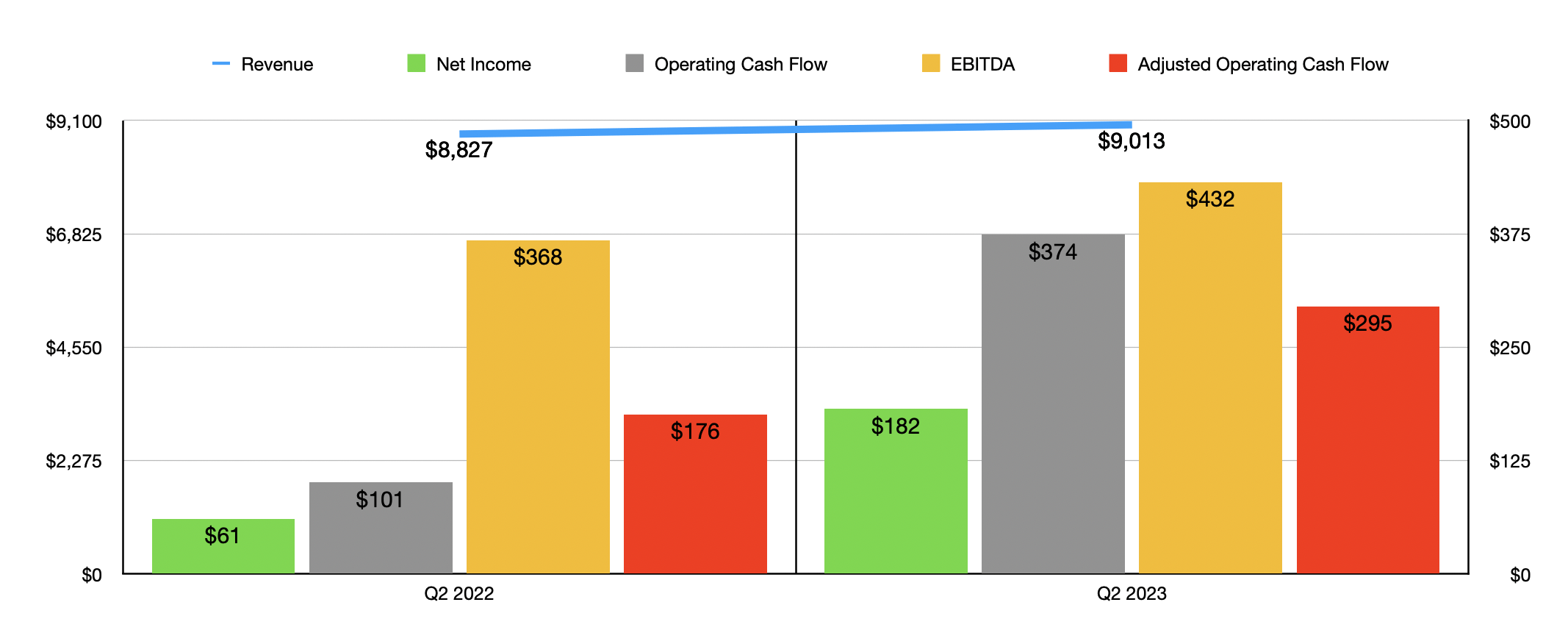

Given current economic conditions, I can understand why investors might be worried that more recent data would show some cracks. But even if we just confine the analysis to the second quarter of this year, the picture looks quite bullish. Revenue of $9.01 billion came in 2.1% above the $8.83 billion reported one year earlier. Net profits nearly tripled from $61 million to $182 million. Operating cash flow almost quadrupled from $101 million to $374 million, while the adjusted figure for it almost doubled from $176 million to $295 million. Adjusted net profits grew modestly from $169 million to $199 million. And lastly, EBITDA for the company expanded from $368 million to $432 million.

{kind=link}

Author - SEC EDGAR Data

In fact, performance for the company has been so strong recently that management even increased guidance for the year. Previously, earnings per share were forecasted to be between $2.45 and $2.65. The low end of that range has now been pushed up to $2.55. At the midpoint, that would translate to adjusted net profits of $652.6 million. Meanwhile, EBITDA has now been forecasted to be between $1.51 billion and $1.54 billion. That compares favorably to the prior range of between $1.45 billion and $1.51 billion. No guidance was given when it came to other profitability metrics. But if we assume that adjusted operating cash flow will rise at the same rate that EBITDA is expected to at the midpoint, that would give us a reading this year of $840.5 million.

{kind=link}

Author - SEC EDGAR Data

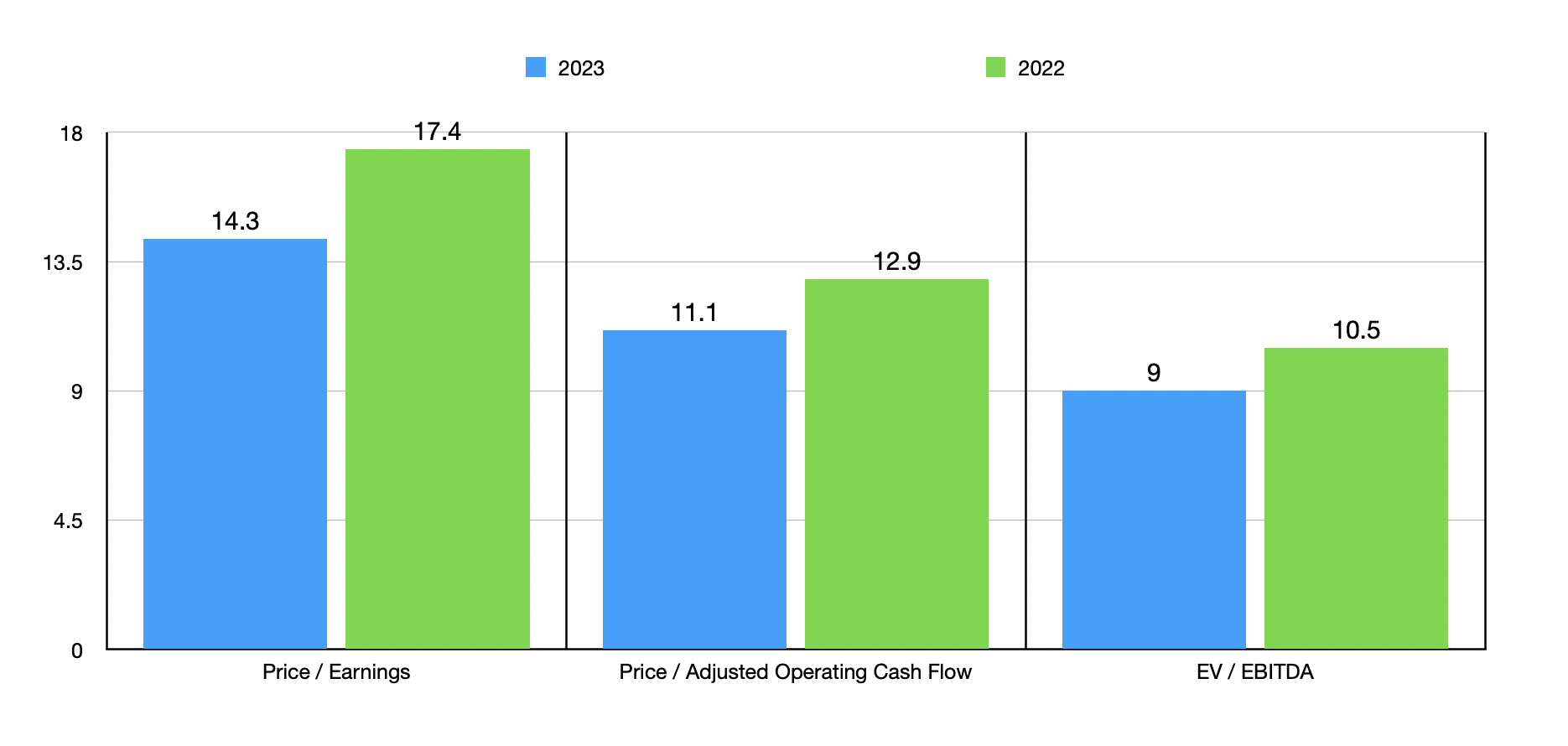

Using these figures, it becomes quite easy to value the company. As you can see in the chart above, shares are trading at a forward price to earnings multiple of 14.3. The forward price to adjusted operating cash flow multiple is 11.1, while the forward EV to EBITDA multiple should be 9. All of these numbers are more appealing than if we were to use the data, shown in the chart above, provided for the 2022 fiscal year. In the table below, I then compared the company to five similar firms. While it is the cheapest on a price to earnings basis, I found that four of the five companies were cheaper than it using the price to operating cash flow approach and three ended up being cheaper using the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| US Foods Holding Corp. |

| 14.3 |

| 11.1 |

| 9.0 |

| Performance Food Group ( PFGC ) |

| 22.0 |

| 10.5 |

| 9.6 |

| United Natural Foods ( UNFI ) |

| 45.6 |

| 1.6 |

| 6.4 |

| The Chefs' Warehouse ( CHEF ) |

| 37.3 |

| 57.0 |

| 10.5 |

| The Andersons ( ANDE ) |

| 21.1 |

| 1.5 |

| 8.7 |

| SpartanNash Company ( SPTN ) |

| 19.8 |

| 6.3 |

| 7.1 |

Takeaway

Operationally speaking, US Foods Holding Corp. is doing really well right now. The market does not seem to care too much for the company. But what's important is that fundamentals should shine through at the end of the day. It's also important to note that management is putting this capital to good use. In the second quarter of this year alone, the company allocated $166 million toward buying back 4.2 million shares. That leaves the enterprise with only $286 million remaining under its $500 million share buyback program. While I always prefer growth over share buybacks, the fact that the company is in a position to do anything at all in this environment is really impressive. Add on top of this the fact that guidance has already been revised higher and that shares look reasonably priced compared to similar firms, and I do still believe that the ‘buy’ rating I assigned the company in February of this year still makes sense.

For further details see:

US Foods Holding: An Attractive Opportunity In Spite Of The Market's Pushback