BHRB - Use This Bear Market As A Passive Income Accelerator

2023-10-28 08:30:00 ET

Summary

- The current bear market presents excellent buying opportunities for high-quality dividend stocks.

- Many stocks, especially dividend stocks, have dropped due to fear and uncertainty, creating attractive discounts and higher dividend yields.

- Investors should take advantage of the current market conditions to buy dividend stocks at higher yields and benefit from future dividend growth.

- For those who aim to grow their passive income from dividends, this bear market is a rare opportunity to accelerate your progress.

This is the best time to buy high-quality dividend stocks in years.

In a great many cases, the buying opportunities today are equally as attractive as the ones that briefly manifested during the initial selloff of the COVID-19 pandemic.

It makes sense. Back in March 2020, investors watched the news with horror as the virus spread like wildfire and hospitals became overwhelmed. Mobile medical tents were set up in New York City parks to take in the masses of infected since all the hospitals had reached full capacity. Fear gripped the planet as no one knew how many lives would be lost, how our behavior would have to change, how long the crisis would last, or what the world would look like when (or if ) it ended.

Those who bought stocks during this brief period did so without seeing any discernible light at the end of the tunnel. They just held their nose and trusted this wasn't going to be like the Bubonic plague that killed off 1/3rd of the European population during the Middle Ages.

The best times to buy are during those periods of fear, tragedy, and uncertainty.

That may seem trite. It may seem callous. But it is true.

As Warren Buffett has said, "Be greedy when others are fearful and fearful when others are greedy."

That sounds so easy, but it isn't. When others are fearful about some major event playing out before our eyes, most of us tend to be fearful about it too. That makes it feel easy and natural and smart during these panicky periods to hide out in cash and wait until there's light visible at the end of the tunnel.

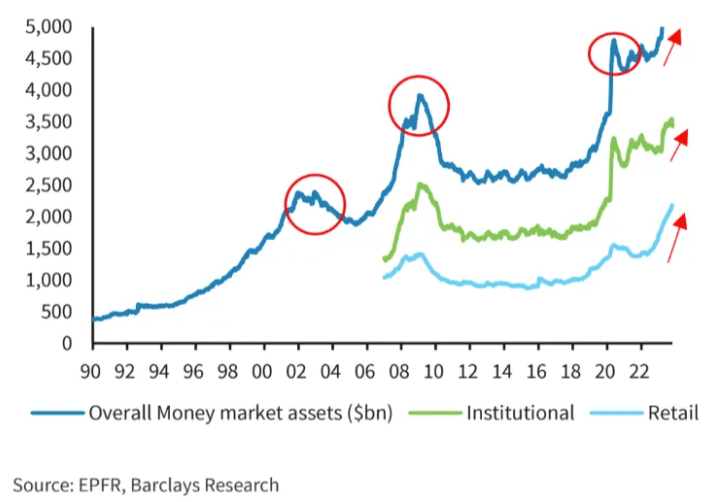

Notice below that during the post-dotcom bubble recession, the Great Recession, and the COVID-19 selloff, investors rushed into money market funds (cash equivalents):

{kind=link}

Almost by necessity, peaks in cash levels are strongly correlated with troughs in stock prices. Where else would the money come from?

Today, we have a similar situation playing out.

War has broken out in the Middle East (not to mention the one still raging in Ukraine), and no one knows how far or fast it may spread across the region. How long will this conflict last? Who will be pulled into it? What will the world look like when its over?

No one knows.

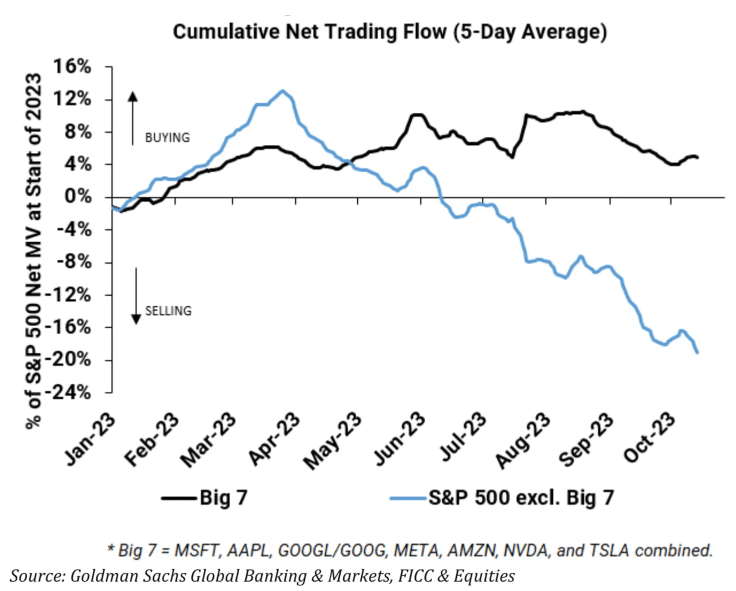

Most stocks have been dropping this year amid this fear and uncertainty. You may not think it looking at the S&P 500's 7.8% year-to-date increase (even after the recent selloff), but that is only because the index is being held up almost entirely by the Big 7 mega-cap stocks.

{kind=link}

Many investors are selling stocks outside this septet of corporate giants and putting the proceeds into money market funds.

That includes dividend stocks.

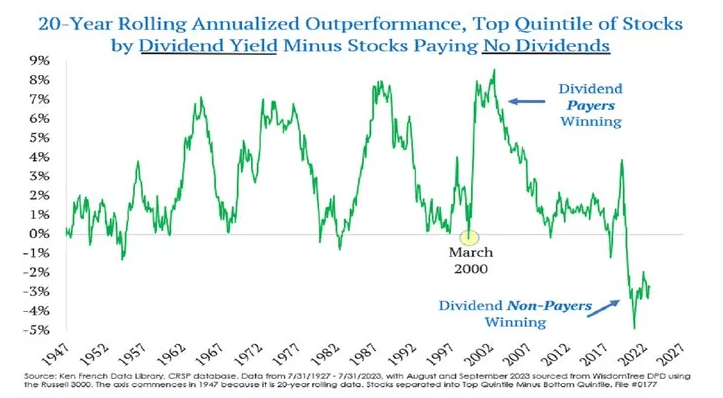

Here's an absolutely wild chart from Jeff Weniger , Head of Equity Strategy at WisdomTree:

{kind=link}

Writes Weniger:

This is the boldest outperformance by stocks who pay a 0% dividend since the data commenced in 1927. If we get a mean reversion of any magnitude on this thing, you can say goodnight to the growth-at-any-price framework that is so commonly embraced.

The only thing that seems to elicit any enthusiasm from investors in 2023 is artificial intelligence. Hence the Big 7's 81.5% average rise in stock price this year, compared to the cap-weighted S&P 500's ( SPY ) 7.5% and the equal-weight S&P 500's ( RSP ) -5.3% performance.

The nearly 13% divergence between SPY and RSP is huge, but it's way bigger for some of the traditional dividend darling sectors like real estate, utilities, and banks.

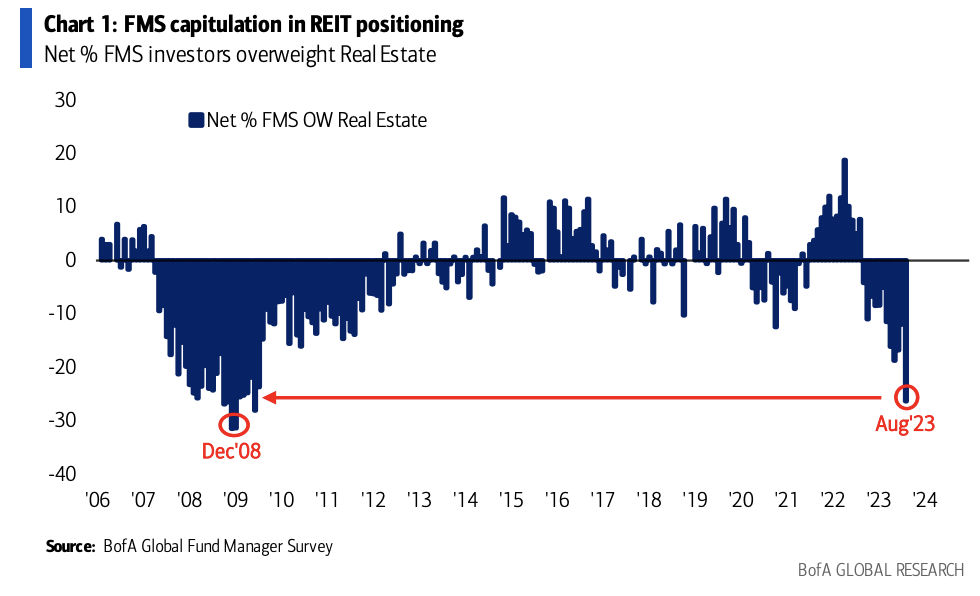

The poster child of boring, non-AI stocks that pay dividends and have been thrown out like last week's leftovers are real estate investment trusts ("REITs").

As of August, professional investors -- fund managers -- were more underweight REITs than at any time since the GFC.

{kind=link}

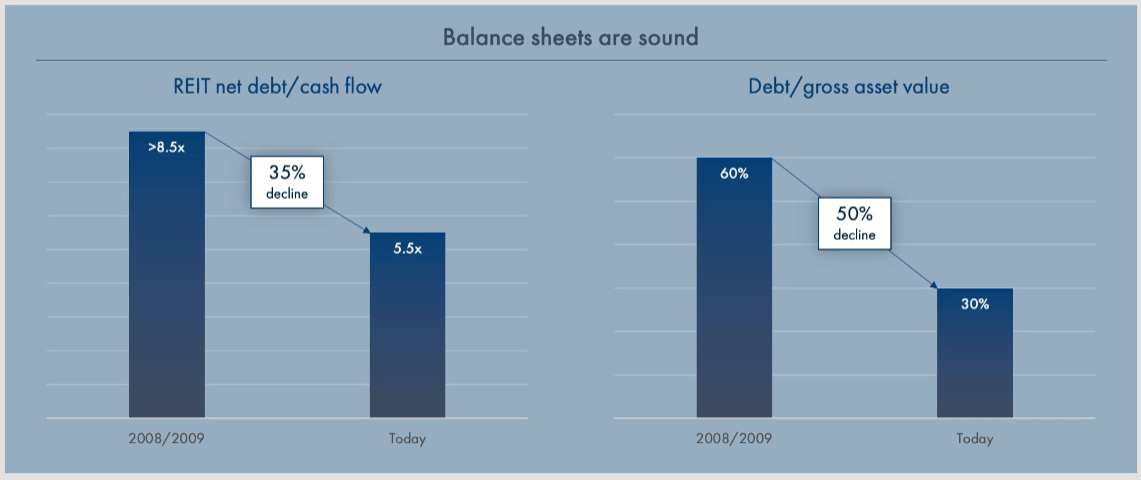

But REITs are far better positioned today than prior to the GFC. Balance sheets are far stronger, and dividend payout ratios are lower.

{kind=link}

Moreover, most REITs have handled rising interest rates just fine so far while continuing to grow rental revenues, cash flows, and often dividends.

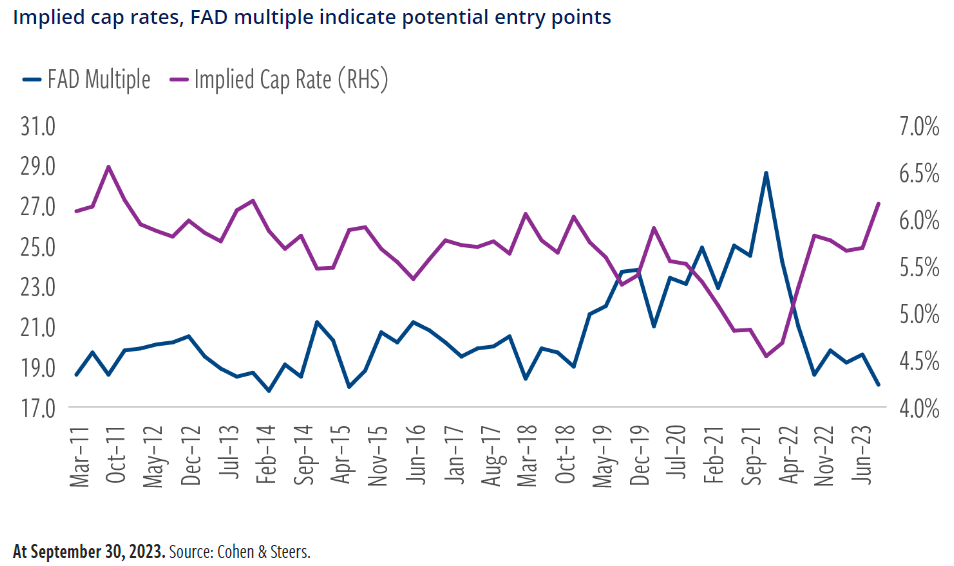

Here's the average FAD ("funds available for distribution," similar to free cash flow) multiple and implied cap rate for equity REITs as of September 30th:

{kind=link}

Since September 30th, though, REITs have continued to sell off, as we see in the chart below showing the Vanguard Real Estate ETF ( VNQ ):

After this further selloff, equity REITs' average FAD multiple has likely decreased from around 18x closer to 16x -- the lowest since the GFC.

Likewise, the average implied cap rate has likely surged above 6.5% -- the highest since the GFC.

Are there reasons why REITs have sold off this year? Of course .

But always remember that, just as investors search for ways to rationalize stocks rising far beyond what their fundamentals would justify during periods of market euphoria, many investors also search for ways to rationalize stocks falling far beyond what their fundamentals would justify during periods of fear and pessimism.

In retrospect, many investors will easily recognize that in late 2021 and early 2022, REIT stocks were euphorically priced for the unlikely scenario that interest rates would stay ultra-low forever.

But many of those same investors are now falling into the mental trap of extrapolating a current trend much further into the future than is realistic, assuming that nothing will stop the relentless rise of interest rates and the merciless downtrend in REITs.

In other words, some investors failed (at the time) to see the mismatch between price and value when REITs were overvalued, and now I think they fail to see the mismatch when REITs are undervalued.

The mind is a funny thing, isn't it?

Dividend Opportunities Galore

My professional background is in real estate, so I tend to focus a lot on REITs. But there are amazing buying opportunities in dividend stocks across many sectors.

My investment strategy is simple and can be applied to any sector of the stock market:

- Buy high-quality companies

- that pay a growing dividend

- at a discount to fair value (and thus an attractive dividend yield )

- and wait patiently as they compound over time .

Rinse and repeat.

The current bear market is a dream come true for any dividend investor still in the accumulation phase of their journey, and also for those retirees who are able to reinvest a portion of their passive income.

The reason for this is that the discounts to fair value for many stocks have grown way bigger, and thus their dividend yields have risen to much more attractive levels.

All else being equal, the higher the dividend yield at which one buys a stock, the greater one's dividend income, both today and into the future as the dividend grows.

Since there are so many great buying opportunities in the realm of dividend growth stocks right now, there's no shame in simply buying a large basket of them in one click through, for example, the Schwab U.S. Dividend Equity ETF ( SCHD ).

Since SCHD's inception as an ETF early in the 2010s, it has only offered a higher starting dividend yield once, briefly, during the initial COVID-19 market selloff.

I say "starting dividend yield" because, as you can see from the orange bar in the chart above, SCHD's dividend payout has steadily increased over time, albeit in a zig-zag pattern.

Unless SCHD's high-quality dividend payers uniformly stop raising their dividends going forward, the nearly 4% yield you can collect from SCHD today will grow larger over time.

Let's take a look at some other quality dividend stocks offering discounts to fair value and attractive starting dividend yields right now.

Crown Castle ( CCI )

The largest telecom infrastructure owner in the US (if you count both its tower and fiber segments) has had a rough go of it since Sprint announced the cancellation of some leases after its merger with T-Mobile ( TMUS ). Plus, the market doesn't like CCI's ~14% floating rate debt.

I think all of that is priced in, but none of CCI's defensiveness or stability is priced in. The dividend yield has reached 7.0%, the highest in its history since becoming a REIT in 2014.

The first half of next year will be the nadir for CCI's cash flow, after which management asserts that the rebound will begin.

EastGroup Properties ( EGP )

EGP owns infill, multi-tenant industrial parks in fast-growing Sunbelt markets. The market seems to worry about industrial supply deliveries over the next year, but I just worry about whether I own enough of this blue-chip REIT. Most new supply comes from big box buildings outside of population centers that don't really compete with EGP's last-mile distribution hub properties.

The current dividend yield doesn't sound that high at 3.2%, but you have to consider the double-digit dividend growth and massive mark-to-market rent growth EGP boasts.

Also, EGP yields more now than it did during the trough of the brief COVID-19 bear market, so there's that.

VICI Properties ( VICI )

The "Landlord of Las Vegas" is branching outside its wheelhouse of the famous strip with its most recent investments in properties leased to Great Wolf Lodge, Canyon Ranch, and Bowlero, but management have proven themselves to be shareholder-friendly capital allocators. I trust their judgement.

VICI's current dividend yield of 6.1% is the highest it has ever been outside of the initial COVID-19 selloff.

And did I mention VICI's rent collection rate is a perfect 100% since its inception, even through the worst pandemic in a century?

NextEra Energy, Inc. ( NEE )

NEE combines a best-in-class regulated utility (Florida Power & Light) with a best-in-class renewable energy infrastructure developer (NextEra Energy Resources) to reliably generate double-digit earnings and dividend growth year after year. The company has stumbled recently on the market's fears about refinancing risk, but management remain confident in the company's growth trajectory.

The current dividend yield of 3.3% is the highest its been since 2013.

NEE is one of those luxury items at the store that rarely goes on discount. It had literally been on my watchlist for years until I began buying some on the recent dip.

American Electric Power ( AEP )

AEP is a pure-play regulated utility with service territories in the Midwest and South, but it also boasts substantial transmission and distribution assets (power lines) as well as the ability to develop them. This is an underappreciated strength as the electric grid needs to transport more power from renewable generation assets in rural areas to population centers.

The current dividend yield is 4.7%, the highest its been since 2013.

Look at that steady, 6%-per-year dividend growth. It's beautiful!

Whirlpool ( WHR )

This blue-chip appliance maker is really getting tossed around in the spin cycle. Mortgage rates are sky-high and the housing market is virtually frozen, so people aren't buying homes and new appliances. Plus, consumer confidence is low, so discretionary purchases are down as well. The country (indeed, the world) appears to be in an appliance recession.

That has caused WHR's current dividend yield to spike up to 6.9%, the highest anytime in the last 35 years outside of a few weeks during the COVID-19 crash.

But get this: WHR has over $1.1 billion in cash and cash equivalents stashed away for just such difficult times as this. The expected $500 million in free cash flow this year will cover the $385 million dividend, and cash in the bank should be more than enough to cover any shortfall next year.

The company has paid a dividend for 67 years straight without a dividend cut, through many recessions and bear markets. I think they'll make it through this downturn with dividend intact as well.

Cullen/Frost Bankers ( CFR )

CFR is the largest regional bank based in and focused solely on Texas. I highlighted it as a strong buy in this recent article . The market seems to fret about CFR's commercial real estate loans, even though these loans are still performing quite well. But I'm more focused on the bank's strident conservatism, including the fact that 15% of its assets are in cash & equivalents. And the fact that its loan-to-deposit ratio is a very safe 0.44x.

The current dividend yield of 4.1% is near those few, rare peaks reached over the last 30 years.

This is a solid bank. Underestimate it at your own risk (of missing out).

Summit Financial Group ( SMMF )

Perhaps you're more inclined to fish in the small cap regional bank pond, where risk is ostensibly higher but so, perhaps, is the reward.

If so, check out SMMF, a small cap West Virginia bank that is about to merge with another small bank, Burke & Herbert ( BHRB ), in the Northern Virginia / Greater DC area. SMMF's proven ability to grow earnings via M&A and BHRB's positioning in the growthier DC market strikes me as a strong combo.

Plus, after SMMF's recent 10% dividend hike, the stock now yields 4.2%, almost as high as its peak yield from the COVID-19 selloff.

In the last five years, SMMF's dividend has increased at an average rate of 10% per year, and the payout ratio is still only a little over 20% of earnings!

Medtronic Plc ( MDT )

Finally, consider MDT, a medical device maker that has had a rough time in recent years, between input cost inflation, supply chain headwinds, elective surgeries making a slow comeback post-COVID, and now GLP-1 drugs threatening to make its diabetes monitoring products obsolete. Or are they?

We shall see, but I think in any case, an aging global population will create more demand for medical devices over time.

MDT's current dividend yield of 4.0% is the highest its been since dinosaurs roamed the earth (in a manner of speaking).

Or, at least, it is as high as its ever been since MDT began paying and raising its dividend 45 years ago. Keep in mind MDT is still only paying out about 50% of its earnings!

Bottom Line

I could keep going like this for a while, as there are tons of incredible, high-quality dividend stock bargains available right now. But I've held forth long enough. My keyboard is worn, and my fingertips are about to go on strike. ("If we all ten stick together and nobody scabs, he can't force us to type anymore!")

This bear market is a dream come true for any dividend investor with cash or income available to invest. For the investor who picks his or her investments wisely, a bear market acts as a powerful passive income accelerator.

It allows you to invest at higher yields, which generate more passive income that can be reinvested for yet more dividend income, and down the mountain the snowball goes.

I intend to use the current bear market for just such a purpose.

For further details see:

Use This Bear Market As A Passive Income Accelerator