OILX - USO: Why Oil Is Crashing And Could Fall More

2023-03-19 09:08:04 ET

Summary

- USO has fallen by around 17% from its March peak as fears around a collapse of several FDIC-insured banks become visceral.

- This negative sentiment, which forms a material headwind for oil prices, will likely dominate the financial markets far into spring.

- Whilst OPEC could follow through with a cut, I view this as unlikely due to the heightened geopolitical blowback it would bring.

The United States Oil ETF ( USO ) invests in listed crude oil futures with the primary objective of reflecting the daily changes in the spot price of WTI oil. USO is now down around 17% from its peak in March as market angst spreads over the state of the economy following the collapse of three FDIC-insured banks. Critically, the events of the last week have rapidly raised the specter of a recession and lent major weight to bearish oil arguments that buoyant expectations going into 2023 of strong global demand on the back of the full reopening of the Chinese economy will be entirely countered by weak economic growth elsewhere.

Hence, with the Fed unlikely to take a dovish pivot with inflation still 3x higher than its target, the near-term positive catalysts for oil seem limited. That said, oil bulls might be right to highlight that some of the weakness can be attributed to speculative capital leaving the derivatives oil markets on the back of heavy downside volatility.

With the mini-banking crisis spreading across the Atlantic to afflict Credit Suisse ( CS ), the haunting prospect of a global economic recession has now likely risen to its highest level since the pandemic. The implications for oil would be dire with prices of WTI oil during the 2008 financial crisis falling to as low as $42 per barrel. Hence, the situation could get worse and oil bulls need to be cognizant of the risks to broader oil sentiment through 2023.

The Bearish Oil Argument

There are further reasons to be bearish. Firstly, the mini-banking crisis is likely to dominate the financial markets far into spring to continue to form a headwind for WTI. Whilst there has been no known dislocation in the fundamental demand for oil, the prospect of a banking crisis feeding through to consumer confidence, regional business lending, and the overall health of the economy will radically dial up the prospect of a recession affecting the US and some other OECD countries.

{kind=link}

Whilst I do not think the current mini-banking crisis will be comparable to the 2008 crash, the extreme worst-case scenario would obviously see oil prices mirror their 2008 move down. Hence, a move down to $60 per barrel could be in play in the coming weeks as we move into the zenith of the crisis. The US economy was projected by the IMF to grow by about 1.4% through 2023, this growth rate now stands to be disrupted by the effects of the collapse of Silicon Valley Bank and Signature Bank.

The big uncertainty is how OPEC will respond. Comments from members of the oil cartel so far have been quite considerate with the Saudi Energy Minister stating that they intend to stick with already announced cuts last October. The cartel has its next ministerial meeting scheduled for June in Vienna but could bring this date forward if required. There is considerable risk for OPEC following through with a second reduction in its oil production targets. Firstly, there is the No Oil Producing and Exporting Cartels ("NOPEC") bill which was recently reintroduced in the US Congress and could open members of the cartel to antitrust lawsuits. The bill is opposed by the White House and the broader US oil industry, but it fundamentally underlies the charged backdrop OPEC will have to operate in. Two production cuts in the same year would not be seen as anything other than a gift to Russia. Further, Russia has already announced production cuts going into March of 500,000 barrels per day , around 5% of its total output, but that failed to boost prices.

Something Finally Broke

The other near-term catalysts would be strong Chinese economic data or the US government announcing that it will begin refilling the strategic petroleum reserve ("SPR"). The White House stated that it would consider purchases again when WTI oil was trading at or below $67 to $72 per barrel. The current price of WTI at $66.75 per barrel is around $0.25 lower than the bottom range of the target purchasing range.

However, the Department of Energy is actually still selling oil from the SPR due to congressionally mandated sales and has stated that purchases can't happen at the same time due to logistics. The DoE was slated to sell another 26 million barrels of oil in February to set the backdrop for the SPR falling to 345 million barrels, its lowest level since 1983. This comes as US crude inventories continue to build, up 1.6 million barrels last week versus a consensus for 1.19 million barrels .

{kind=link}

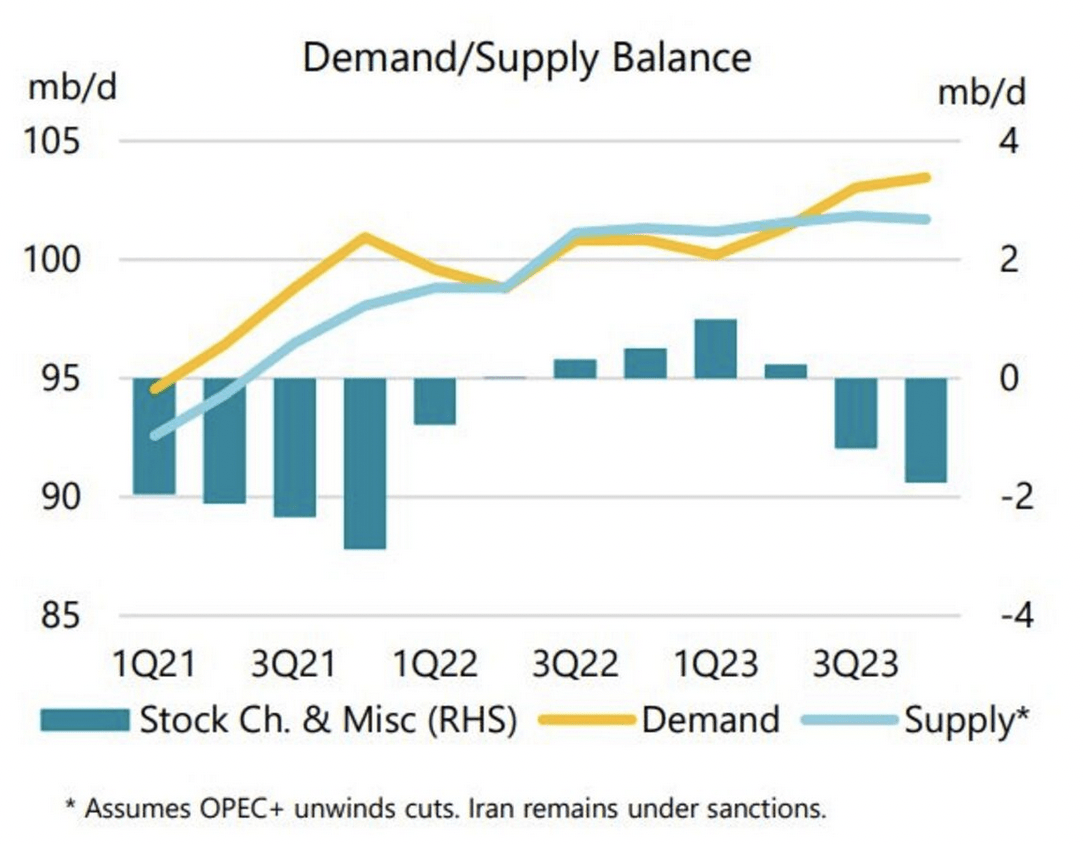

There are no clear near-term demand catalysts until the second half of the year when demand is expected to outstrip supply according to the International Energy Agency. This would see oil demand exceed its supply by more than 1 million barrels a day between July and September, a figure that would increase to 1.5 million barrels a day from October to December. However, the IEA forecasts assume a collapse in Russian production which has remained in the market. Russia had an output of 11.4 million barrels a day in January. Faced with the loss of the lucrative European natural gas market, a G7-led price cap, and large discounts on its oil from selling to India and China, Russia has no choice but to keep on pumping. Crude oil sales form the main driver of foreign earnings and its federal tax budget.

This dynamic likely highlights why a near-term restart of an SPR refill is unlikely. Oil is critical to the Russian economy and the main life source of its war economy. Hence, refilling the SPR now would be a boost to Russia that the White House is seeking to avoid. To be clear here, Russia's ability to finance its war economy becoming materially eroded is the core foreign policy objective of the White House and its NATO allies. Hence, there could simply be no reason to restart the SPR refill this year. Oil could fall more on the back of continued macroeconomic angst with no near-term catalysts to support prices.

For further details see:

USO: Why Oil Is Crashing And Could Fall More