LNT - UTF: This 7.49%-Yielding Infrastructure CEF Is A Solid Buy Today

Summary

- Infrastructure companies are a favorite of income-focused investors due to their general stability and high yields.

- The companies in which Cohen & Steers Infrastructure Fund is invested held up very well in 2022 and will likely continue to be solid holdings through any recession that occurs in 2023.

- The UTF closed-end fund has one of the best track records in terms of its distribution and currently boasts a 7.49% yield.

- The fund can probably maintain its yield and is currently trading at a discount to the net asset value.

- The fund could deserve to be a core holding in any investor's portfolio.

For many years, infrastructure companies have been among the favorite holdings of income-focused investors. There are many reasons for this, including the fact that these companies tend to be very resistant to economic cycles and enjoy remarkably stable cash flows. Unfortunately, it can be difficult to put together an appropriately diversified portfolio of these firms without having a significant amount of capital. In addition, some infrastructure companies enjoy tax advantages, such as master limited partnerships, and can be quite difficult to include in an individual retirement account or similar structure.

Fortunately, there are a few ways around some of these problems. One of the best of them is to purchase shares of a closed-end fund that specializes in investing in infrastructure companies. These funds are quite nice because they provide an easy way to obtain a professionally-managed and diversified portfolio of infrastructure companies. In many cases, these funds can deliver a much higher yield than any of the underlying assets possesses. Finally, as most of these funds are structured as corporations, they avoid the tax problems that can be associated with master limited partnerships.

In this article, we will discuss one of the more popular infrastructure companies on the market, the Cohen & Steers Infrastructure Fund ( UTF ). I have discussed this 7.49%-yielding closed-end fund ("CEF") quite often at Energy Profits in Dividends but have not generally made the reports publicly available. As such, this article will make an effort to discuss the changes since the last time that we discussed the fund while still including enough information to allow someone that has not seen my previous work on the fund to make an informed decision about its credentials as an investment.

About The Fund

According to the fund’s website , the Cohen & Steers Infrastructure Fund has the stated objective of providing its investors with a high level of total return. This is not exactly uncommon for an equity fund as common equities are by themselves a total return vehicle. After all, we primarily buy equities both for their potential to generate capital gains as well as the dividends that many of these securities pay to the investors. With that said, many infrastructure companies boast very high dividend yields. This is due to the fact that infrastructure companies tend to have fairly low growth rates. As such, they pay out a much higher percentage of their cash flows than a company that wants to conserve its capital to invest in growth.

In addition, their low growth rate tends to result in the market assigning lower multiples to their stock prices, which results in the dividend being a higher percentage of the stock price than would be the case at a high-growth firm. As might be expected from this dynamic, the fund focuses its efforts to generate a high total return on direct payments made to its investors. The fund’s attempts to generate capital gains are secondary but no less important.

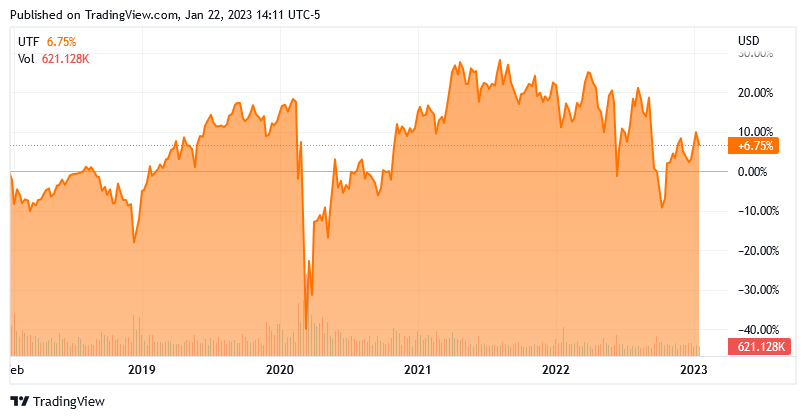

This focus on providing direct payments to investors is not unusual for a closed-end fund. In fact, many of them aim to keep their own share price relatively stable while paying out all of their capital gains and dividend income to investors. The Cohen & Steers Infrastructure Fund has been somewhat successful at this over time. As we can see here, the fund’s price has only increased by 6.75% over the past five years:

{kind=link}

Other than the steep drop in 2020, we do not see very much movement over the period. In fact, the fund’s price was between $23.00 and $27.00 per share for most of the period. This is exactly as intended though since the shareholders of the fund get their returns in the form of the monthly payment that they receive from the fund. It would be logical to assume that this will continue going forward so anyone looking for substantial capital appreciation from the fund itself would be best served to look elsewhere. Of course, there is still very much the potential to grow the size of your position in the fund by simply reinvesting the distributions that it pays you. That reinvestment would also allow you to reap the benefits of compounding until such time as you are ready to simply stop the reinvestment and begin using the fund as a source of income.

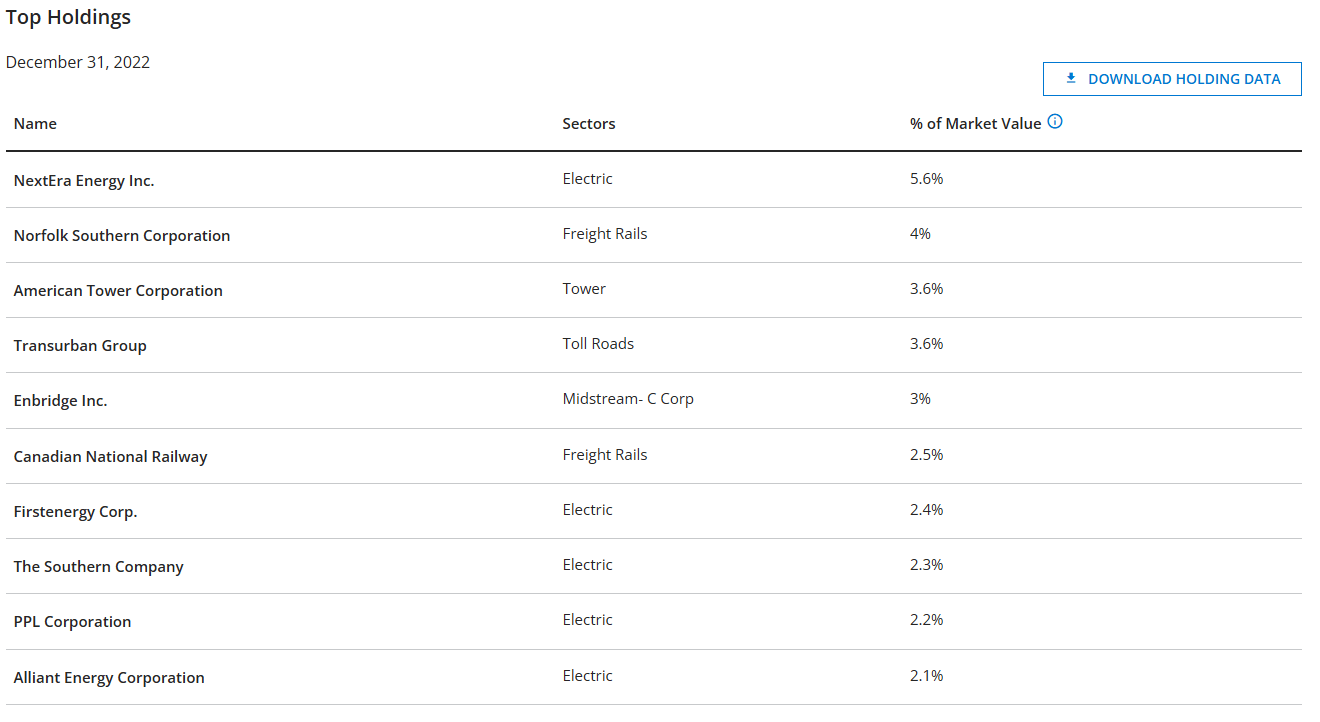

As my long-time readers are certainly well aware, I have spent a great deal of time discussing various infrastructure companies on this site. These companies are things like utilities, railroads, pipeline companies, and toll road companies that provide the things that many people take for granted in modern society. As I have discussed these companies fairly extensively, many of the largest positions in this fund will likely be familiar to many readers. Here they are:

{kind=link}

Indeed, I have discussed most of these companies at one point or another. There are also quite a few that I have never discussed, though, which include the two railroads, Transurban Group ( TRAUF ), and The Southern Company ( SO ). For the most part, though, these companies are exactly what we would expect to see in an infrastructure fund. We see a few utilities, railroads, a toll road operator, one of the largest pipeline companies in North America, and American Tower ( AMT ).

American Tower certainly does fit in with many of the rest of these companies at first glance. American Tower owns a number of cellular towers located around the country and internationally that it then leases out to telecommunications companies like AT&T ( T ) and Verizon ( VZ ). When we consider how important cellular phones are to most people in today’s world though, it is pretty easy to see how American Tower can be considered as providing a critical part of the infrastructure that allows modern society to function.

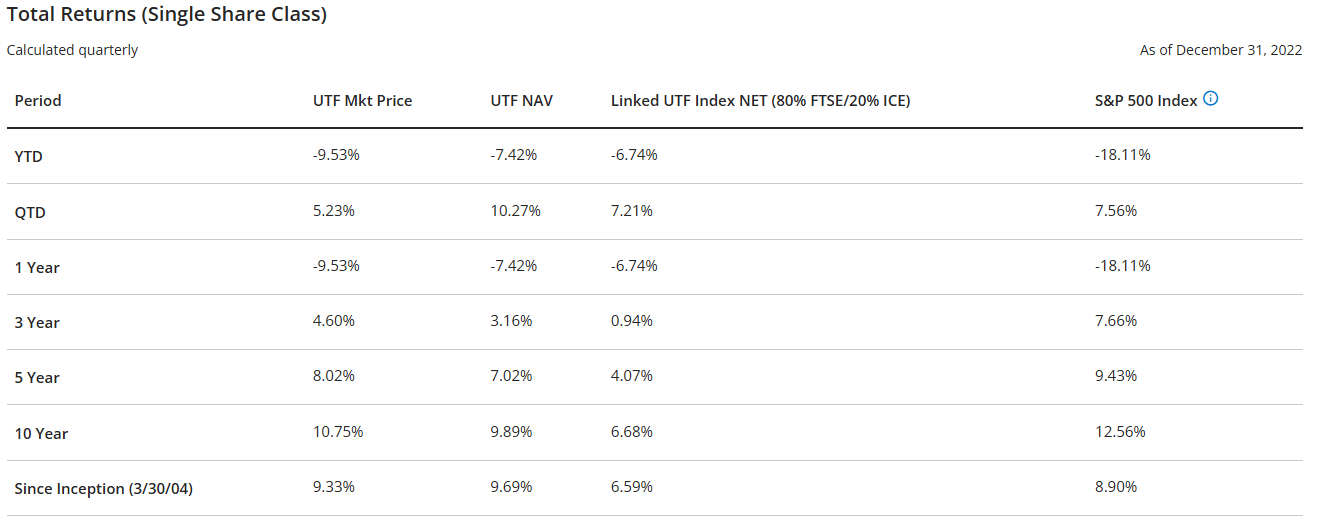

The majority of the holdings on the fund’s largest position list have been in the fund for quite some time. In fact, there have only been two changes since I discussed the fund a year ago. These two changes are the removal of Duke Energy ( DUK ) and Cheniere Energy ( LNG ) in favor of PPL Corporation ( PPL ) and Alliant Energy ( LNT ). As there have been so few changes over an entire year, one might be led to think that the fund has a very low turnover. However, this is not exactly correct as the Cohen & Steers Infrastructure Fund has a 47.00% annual turnover. Admittedly, that is not especially high for an equity fund but it is still higher than we might expect. The reason that this is important is that it costs money to trade stocks or other assets, which is billed to the shareholders. This creates a drag on the portfolio’s performance and makes things somewhat more difficult for the fund’s management. This is because management will need to generate sufficient returns to cover these costs and still deliver a good enough return after covering the costs to satisfy the shareholders. This is a task that few management teams have been able to accomplish on a consistent basis. This is one reason why index funds tend to outperform actively managed funds. The management of the Cohen & Steers Infrastructure Fund has enjoyed some reasonable success at this task, however. As we can see here, the fund has outperformed its benchmark index during most, but not all, periods:

{kind=link}

The fund’s performance over 2022 was particularly noteworthy. That was a period in which just about everything lost money:

| Index |

| Performance in 2022 |

| Nasdaq Composite (COMP.IND) |

| -33.1% |

| Russell 2000 (RTY) |

| -21.6% |

| S&P 500 Index (SP500) |

| -19.4% |

| Dow Jones Industrial Average (DJI) |

| -8.8% |

The Cohen & Steers Infrastructure Fund held up much better, however. As we can see above, during 2022 the fund’s market price was down 9.53% (worse than the Dow but better than all the other indices). However, the fund’s net asset value, which is a better measure of how well the fund’s portfolio performed, was only down 7.42%. Thus, the fund outperformed all of the major broad market indices. That is certainly a respectable performance during a bear market and it is an indication that this is the type of investment that one should want in their portfolio during challenging conditions, such as 2023 is likely to be.

One of the reasons why the Cohen & Steers Infrastructure Fund should hold up better in a recession or bear market is because of the financial stability that most of the companies in the portfolio have. As we have already seen, a significant percentage of the portfolio consists of electric utilities. In fact, these utilities comprise 30.11% of the fund’s portfolio. Electric utilities are famous for their stability since they provide a necessary service for modern life. Thus, most people will prioritize paying their electric bills ahead of discretionary expenses during times when money gets tight. The same characteristic is shown by midstream companies, which comprise 12.16% of the portfolio and also enjoy remarkable stability regardless of economic conditions. I have shown that in numerous past articles. The same thing is certainly true of American Tower, since it is very hard to believe that any of the major cellular carriers will reduce the reach of their networks due to a recession.

Thus, over half of the fund’s portfolio should generally be very resistant to any recession that may occur in 2023. That is something that is certainly going to appeal to any investor that is interested in capital preservation, which is a category that would include most retirees.

Distribution Analysis

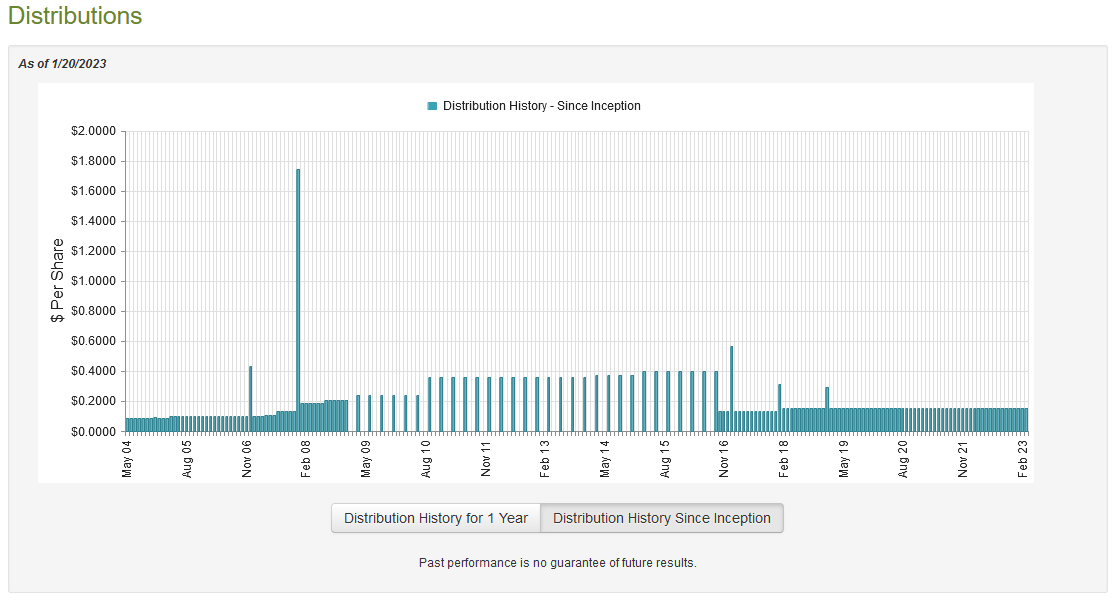

As stated earlier in this article, many infrastructure companies boast fairly high dividend yields. The Cohen & Steers Infrastructure Fund’s primary objective is total return but it aims to deliver this primarily in the form of current income to its investors. As such, we might assume that the fund will have a suitably high dividend yield. This is certainly the case as it pays out a monthly distribution of $0.1550 per share ($1.86 per share annually), which gives the fund a 7.49% yield at the current price. The fund has been remarkably consistent about its payout over its lifetime, with the current distribution being maintained since 2018:

{kind=link}

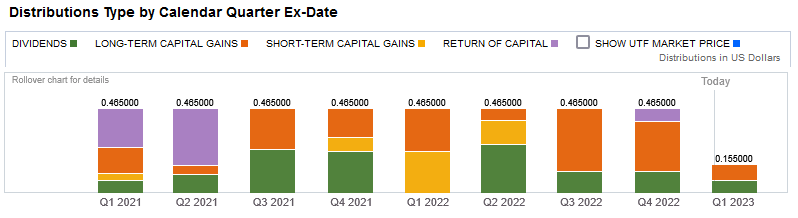

This actually gives the Cohen & Steers Infrastructure Fund one of the better track records among all infrastructure closed-end funds. It is also one of the few funds that did not cut the distribution in response to the collapse of the energy infrastructure sector back in 2020. The fund’s strong history is almost certainly going to be appealing to those investors that are looking for a safe and consistent source of income with which to pay their bills. Another thing that these conservative investors may appreciate is the fact that the fund’s distributions are almost entirely classified as dividend or capital gains income, and include a minimal return of capital:

{kind=link}

The reason why this is likely to be comforting is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, capital gains may also not be sustainable over extended periods since they obviously require the fund to generate capital gains. That can sometimes be a difficult task, as few stocks outside of the energy sector actually delivered a positive return in 2022, and pretty much everything declined significantly in the fourth quarter of 2018. As such, we should investigate the fund’s finances in order to determine exactly how it is financing its distributions and how sustainable they are likely to be.

Unfortunately, we do not have an especially recent document to consult for that purpose. The fund’s most recent financial report as of the time of writing corresponds to the six-month period that ended on June 30, 2022. As such, it will not include any information about the fund’s performance in the second half of the year. That could be an important omission as energy infrastructure companies generally performed much better in the first half of 2022 than in the second half of the year. Nonetheless, the document should give us a good idea of how well the fund handled the Federal Reserve’s switch to a hawkish monetary policy, which has been blamed for much of the market weakness that we saw during the year. During the six-month period, the Cohen & Steers Infrastructure Fund received a total of $43,544,207 in dividends and $8,027,265 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund had a total income of $52,048,276 during the period. It paid its expenses out of this amount, leaving it with $25,818,721 available for the stockholders.

Unfortunately, this was nowhere close to enough to cover the $88,527,060 that it paid out in distributions during the period. Thus, the Cohen & Steers Infrastructure Fund quite clearly failed to generate enough income to cover its distributions during the first half of the year, which is quite concerning at first glance.

With that said, the fund does have other methods that it can employ in order to obtain the money that it needs to cover its distributions. One of these methods is through capital gains. As might be expected from the weak capital markets during the first half of the year, the fund delivered mixed results at this. It did manage to achieve net realized gains of $70,866,162 during the period but this was more than offset by $266,991,266 of net unrealized losses. Overall, the fund’s assets declined by $249,517,783 after accounting for all inflows and outflows during the six-month period.

This may be concerning, but it is important to point out that the fund’s net realized gains plus net investment income was sufficient to cover the distributions with money left over. The same was true during the full-year 2021 period and overall, the fund’s assets did increase from January 1, 2021, to June 30, 2022, even after paying out its distributions. While we will still want to have a look at the fund’s full-year 2022 results when they are released, it does appear that the distribution is probably sustainable unless the market continues to handle the fund more losses over an extended period. The takeaway is that everything appears to be okay here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Infrastructure Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s holdings minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. That is fortunately the case with this fund today. As of January 19, 2023 (the most recent date for which data is available as of the time of writing), the Cohen & Steers Infrastructure Fund had a net asset value of $25.12 per share but it only trades for $24.84 per share. This gives the fund a 1.11% discount to net asset value at the current price. This is slightly worse than the 1.52% discount that the shares have traded at on average over the past month but it is still not really a horrible price to pay. Overall, the Cohen & Steers Infrastructure Fund looks like a decent buy at the current price.

Conclusion

In conclusion, the Cohen & Steers Infrastructure Fund looks like a very solid core holding for anyone that is looking for some safety and security in today’s market. The companies in which the fund invests should prove to be highly resistant to any recession or other economic trouble, which nearly everyone expects to occur in 2023. The fund also pays a reasonably attractive 7.49% yield that appears to be sustainable. When we combine this with an attractive valuation, the Cohen & Steers Infrastructure Fund appears to be a solid purchase today.

For further details see:

UTF: This 7.49%-Yielding Infrastructure CEF Is A Solid Buy Today