UWMC - UWM Holdings: Hold On

2023-09-19 14:41:36 ET

Summary

- United Wholesale Mortgage is the #1 direct and wholesale Mortgage Lender in the USA with a dominant market share.

- The company has shown impressive growth in market share, maintained control over its headcount, and increased profit margins.

- Numerous economic risks and a dividend dilemma are driving me to hold this stock, for now.

Investment Thesis

In this article, I review United Wholesale Mortgage Holdings Corporation's ( UWMC ) latest investor presentation from August 2023 and reveal my key insights driving me to hold this stock, for now. While its market share, dividend, and operational efficiency are attractive, I feel more time is needed to complete the full interest rate cycle, realize a lower payout ratio, and see the effects of inflation with looming recession concerns.

Company Overview

United Wholesale Mortgage ((UWM)) was established in 1986 and went public in March 2020. It is currently the #1 direct and wholesale Mortgage Lender of market share and enterprise value in the USA. The company strategy leverages their proprietary technology and extensive broker relationships, over 52,000 loan officers, to scale their operations and maintain highly competitive rates, even during the high interest rate environment consumers face now. The result is a faster and cheaper mortgage process for clients like you and me. I can attest experiencing it first hand when I purchased my home, my broker was a partner with UWM. The process was exceptionally fast and easy, with a rate so competitive, the notary had to double check it at closing.

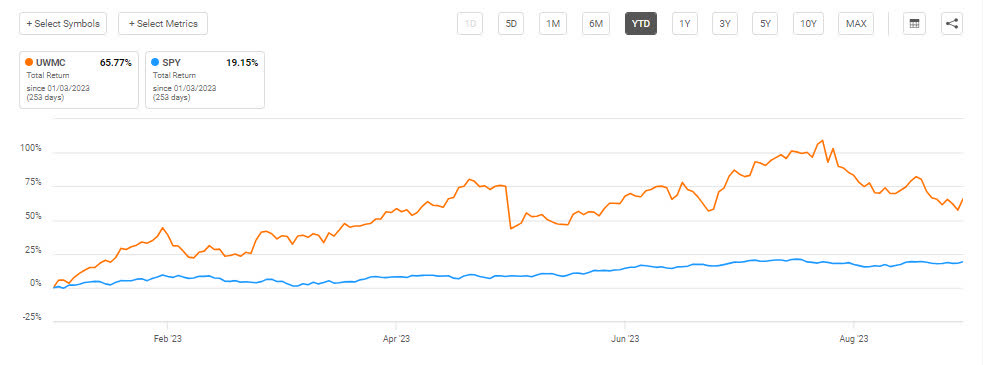

UWM vs. S&P500 Performance

Year to date, UWM has outperformed the S&P500 considerably, with a total return of about 66% vs. SPY 's 19%. Having been beat up quite a bit when the fed began announcing rate hikes, UWM has steadily rallied in 2023 all while maintaining a $0.10 quarterly dividend or 7.41% dividend yield.

UWM vs. S&P500 YTD (Seeking Alpha)

{kind=link}

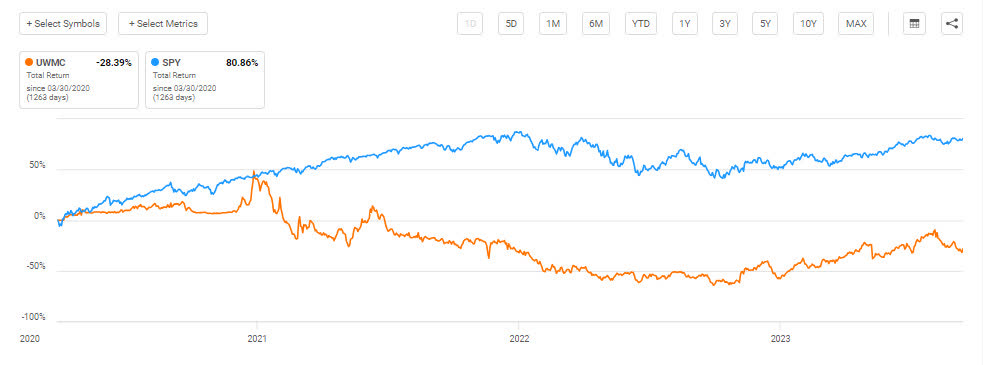

Though, if we zoom out about 3.5 years to UWM's inception in March 2020, we see a significant negative total return of about -28% vs. SPY's 81%, which may make an investor think this was a bad investment however, 3 years is not enough time to make such a determination long term. With a dominant market share, $2.8B in cash, and a profitable business model, UWM isn't going anywhere anytime soon.

UWM vs. S&P500 Inception (Seeking Alpha)

{kind=link}

What I'm Liking

Three things stand out to me when reviewing the Q2 Investor Report from August 2023

- Market share

- Headcount conscientious

- Increased profit margins

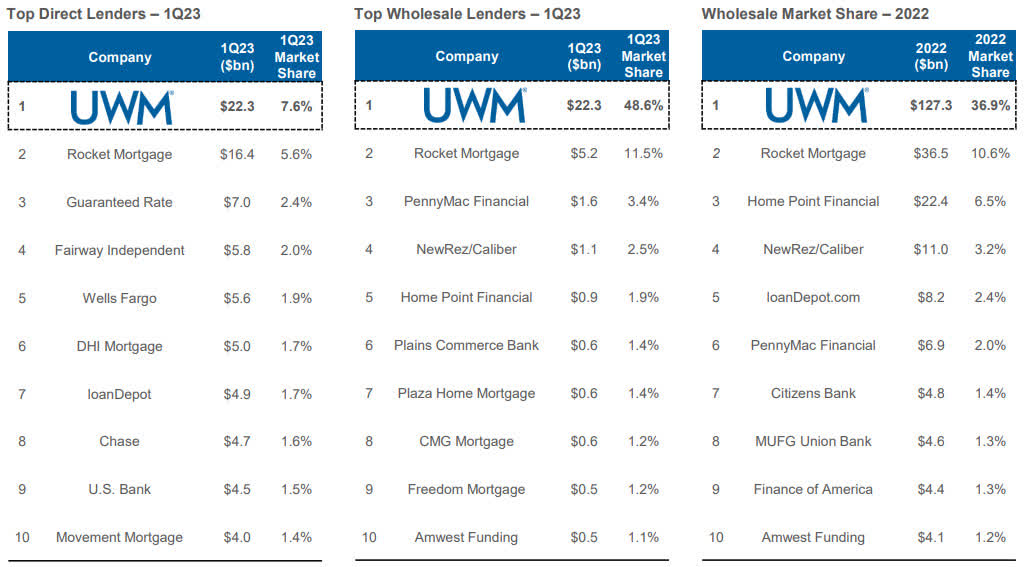

UWM's market share has grown to dominate in direct lending, wholesale lending, and overall wholesale market share to 7.6%, 48.6%, and 36.9% respectively. Its wholesale market share is markedly impressive and has continued to increase as interest rates have almost tripled and fluctuating volumes. This is one of the reasons they are able to maintain competitive rates for customers, on average 0.2% lower, than its competitors.

UWM Market Share (UWM Investor Presentation)

{kind=link}

Next, UWM has demonstrated conscientious headcount control throughout the rate cycle, actually ending up with 700 less employees in 2022 compared to 2018 , again while gaining market share. I feel with AI integration and focus on continuous improvement of operations, UWM should be able to keep headcount in check moving forward, combining it with its proprietary technology and broker model. It will be interesting to see when rates begin to lower and refinancing volume spikes again, what happens to their staffing levels. While an efficient staff level is good for profitability, wild swings in headcount are not good for business or employee morale. I would like to see a more consistent and sustainable headcount control. Nonetheless, I see this trend as an overall positive for the company.

UWM Total Employees (UWM Investor Presentation, Nicholas Bratto)

{kind=link}

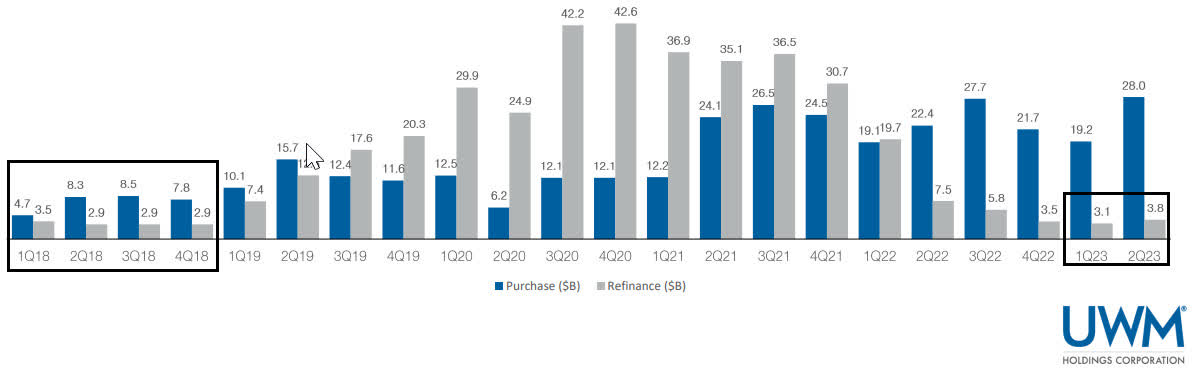

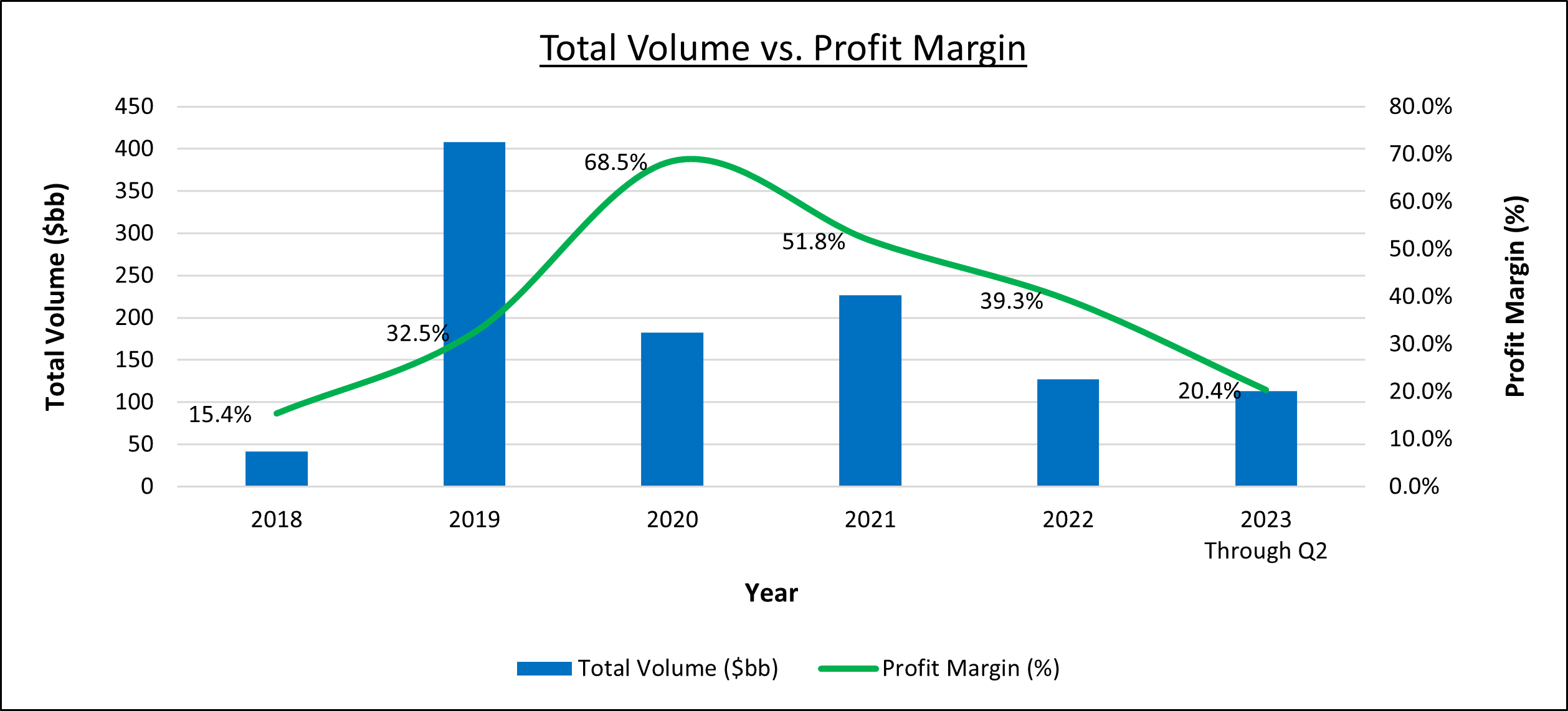

Finally, I took a look at UWM's profit margins. Given the rate cycle, inflation, and the housing market through 2023, UWM has reflected a higher profit margin in 2023 at 20.4% compared to 2018 at 15.4%. Not only is this the largest spread of time but more importantly, 2018 and 2023 don't represent years with a lot of refinancing activity but purchase volumes increased, indicating its operations are becoming more efficient even during difficult industry times as shown in the table and graphs below. I thought that was pretty impressive.

UWM Environments of Operations (UWM Investor Presentation) UWM Key Financial Results (UWM Investor Presentation, Nicholas Bratto) Total Volume vs. Profit Margin (UWM Investor Presentation, Nicholas Bratto)

{kind=link}

{kind=link}

Risk Analysis

There are also some things I'm concerned with about UWM moving forward

- Full interest rate cycle completion

- EPS realization to reduce payout ratio

- Housing market, inflation, and looming recession concerns

UWM's data from 2018 and 2019, the good ol' days, represents a more tame business operation prior to further rate cuts driven by COVID and now rate increases driven by inflation. As of now we are seeing the highest interest rates in decades and still may climb higher yet. Eventually, rates will decline again, but we have yet to see how UWM will perform during this era of slower declining rates to finish the last of this cycle.

Next, I'd like to point out UWM's dividend payout ratio of 500% is obviously high and concerning. There are forward projections regarding an exponentially growing EPS which implicitly affects the payout ratio to be about 26% in the next year, but this is yet to be realized. Personally, I'd like to see the share price rise to reflect a dividend yield in the 3-5% range, preferably in the 4% range. I don't want UWM to end up like a mortgage REIT with unsustainably high dividend payouts, eroding share price, and no dividend growth. I want to own (part of) a well-run business that can pay a stable, growing dividend.

Last, there's the overall consumer challenges with the intertwine of the housing market, inflation, and looming recession concerns. Should rates remain high for another year, we have yet to see if UWM will continue to process a high enough volume and revenue share of loans and maintain profitability. With inflation, equities in general have significant downward price pressure at this point in 2023. Should mortgage defaults rise, like a 2008 situation, UWM will not fare well, it's getting really tight out there and a lot of analysts think something's got to give in the next year. If it's a big housing crash, companies like UWM are not going to be attractive investments.

Forward Looking Sentiment

Overall, with what I'm liking and what I'm concerned about, I rate UWM as a Hold, for now. I'll continue to reinvest my dividend and keep my cost basis under control, but I won't be actively buying more shares for a little while, until results of the risk management are realized. UWM is in a great position, with a profitable and efficient operation I can get behind. I think we just need a little more time to demonstrate its leverage and results during these difficult times in the market.

For further details see:

UWM Holdings: Hold On