UWMC - UWM Holdings: Poised For Continued Dominance In 2024 Despite Cyclical Economics

2024-01-09 01:32:40 ET

Summary

- UWM Holdings doubled its share price in 2023 despite Federal Reserve rate hikes, driven by increased loan volumes and operational efficiency gains.

- The company dominated the industry with a $29.7 billion overall production and an increase of 97 basis points in total gain margin, showcasing resilience amid high interest rate environment.

- UWM is positioned better than it ever has been to take advantage of the refinance cycle in 2024 when rate cuts set in.

In 2023, UWM Holdings Corporation ( UWMC ) showcased remarkable resilience, more than doubling its share price despite facing challenges from Federal Reserve rate hikes. The company's strategic offensive stance, evident in substantial loan volumes, new services, and operational efficiency gains, fueled its performance. However, new challenges arise in 2024, including anticipated rate cuts and a dividend to maintain. I believe UWM's financial strength, operational excellence, and cash reserves position it favorably for continued outperformance, making it a compelling buy below $7/share.

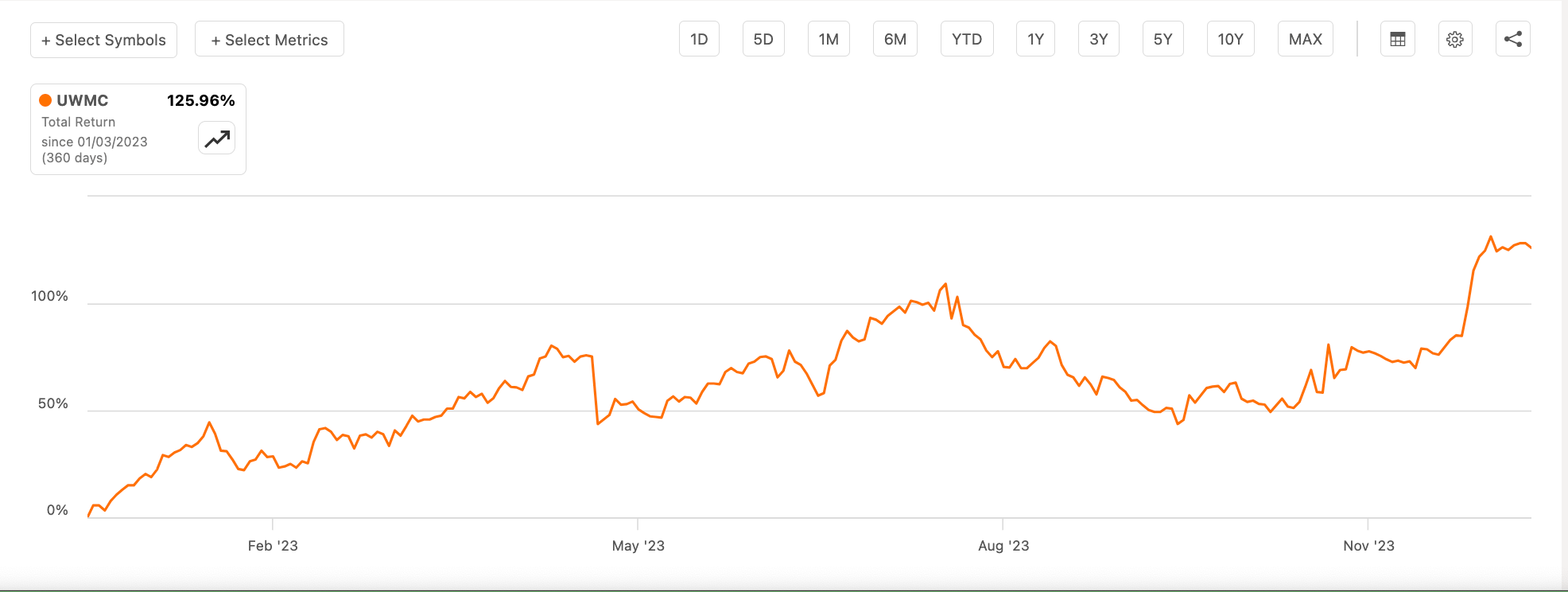

2023 Summary

UWMC 2023 Total Return (Seeking Alpha)

{kind=link}

2023 was an outstanding year for UWM, posting nearly a 126% total return for the year. One of the main market drivers for this is the company's resilience, reflected in multiple earnings reports, during a year of perpetual rate hikes by the Federal Reserve. These hikes directly impact mortgage lender's business model. Despite the challenging year, the company went on offense and continued originating substantial loan volumes, new services, and operational efficiency gains.

UWMC Total Return Since Inception 2020-2024 (Seeking Alpha)

{kind=link}

Let's keep in mind, the stock still has a -9.93% total return since its inception on the public markets. A genuinely odd shape for this graph given the drastically different interest rate cycles the company has and is continuing to go through. A quick look at their financials would suggest the market elevating this stock through 2022 and depressing it through 2023, but the opposite was or proactive reaction was reflected instead. Also, it may be because we are seeing two extremes of mortgage rates play out so quickly, with both record low and high interest rates within 3 years, causing investors to swing being both unimpressed and impressed with each performance, respectively.

Q3 2023 Results Highlights

Reading through the Q3 2023 results report, there are several positive indicators for this stock explaining its great comeback in 2023 and continuing good performance in 2024. The company had strong production and purchase volume, delivering $29.7 billion in overall production, dominating the industry. This reflects the powerful client & broker relationships, and internal process efficiency, and positions them well for refinancing transactions in the future. Additionally, the company posted an increase in its gain margin of 97 basis points. Gain margin refers to the difference between the selling price of the mortgage loans originated and their production cost. This increase reflects an operational efficiency & profitability improvement of the company's operations. Summarized below are the last three quarters of the company's loan volume, total gain margin, net income, and EPS.

| Metric | Q3 2023 | Q2 2023 | Q3 2022 |

|---|---|---|---|

| Loan Volume | |||

| $29.72M | |||

| $31.84M | |||

| $33.46M | |||

| Total Gain Margin | |||

| 0.97% | |||

| 0.88% | |||

| 0.52% | |||

| Net Income | |||

| $300.99M | |||

| $228.79M | |||

| $325.61M | |||

| Diluted EPS | |||

| $0.15 | |||

| $0.08 | |||

| $0.13 |

While the loan volumes did come down slightly, that is impressive resilience at a time when rates were and are at an all-time high. The improvement in total gain margin is also reflected in the net income and overall increase in EPS. Given the company's current operating model, we are really seeing it at its worst in my opinion. Interest rates are at 20-year highs, coming off of record high inflation as well. To be able to maintain revenue levels similar to 2022 with increased profitability demonstrates just how robust this mortgage company is. I think the market has priced this accordingly as well.

Challenges Ahead in 2024

While I feel UWM has a strong sustainable position, there are several concerns I have that can test their financials. At the macro level, there are the highly anticipated rate cuts this year, which will likely launch the company into a frenzy of refinancing activity that needs to be executed and reflected in the books. On the flip side to this, recessions are usually led out of periods with lower interest rates and while this could lead to increased refinancing activity and origination opportunities, it looms in the back of my mind as an '08 Millennial that many of these loan purchases made in the last few years could come crashing down should unemployment rise sharply, as only 48% of US adults say they have enough emergency savings to cover at least three months’ worth of expenses. Financial companies naturally carry a lot of debt and upticks in defaults directly impact the net income to the company.

UWMC Payout Ratio 2017-2023 (Seeking Alpha, Nicholas Bratto)

{kind=link}

Shifting toward a more company-specific point, the other thing I'd like to see improve is the dividend payout ratio, which I'm calculating as 194% in the table above. The payout has been running quite high for their 2023 fiscal period, despite management's confidence in the continued dividend amount and consistency moving forward, but management is always confident until their not. The previous years going back to 2017 show an appropriate payout ratio < 100%. It begins to call into question whether the dividend is actually sustainable or if this is just a blimp to correct for the last quarter of the company's fiscal year. The dividend has been set at $0.10/share since inception and does offer a juicy yield of about 6% currently, but at that yield it's more likely we need to see the share price increase, with increased net income, to see the dividend increase. Even the higher payout rates in 2021 and 2022 can also hinder the growth of the company and therefore the dividend growth with a lack of profitability to reinvest into the business. It's just been running a little close for comfort but is acceptable for now. Ultimately, I'd like to see this company grow its dividend over time with the massive market share it's achieved and resilience through different cyclical periods. It would solidify for me further as a long-term buy & hold.

Positioning Ahead

Looking ahead, I believe UWM's financial strength, operational excellence, and resilient business model will allow the company to outperform in a likely competitive 2024 market. The company still has $737M in cash on the sidelines, great liquidity with a current ratio of 1.95, and a wave of opportunity to continue demonstrating outperformance for the next several quarters. I rate the stock as a Buy below $7/share. I personally like my position size currently and plan to DRIP the dividends only, for now. Though, if we see a pullback below $6/share I will likely load up on more shares.

For further details see:

UWM Holdings: Poised For Continued Dominance In 2024 Despite Cyclical Economics